Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

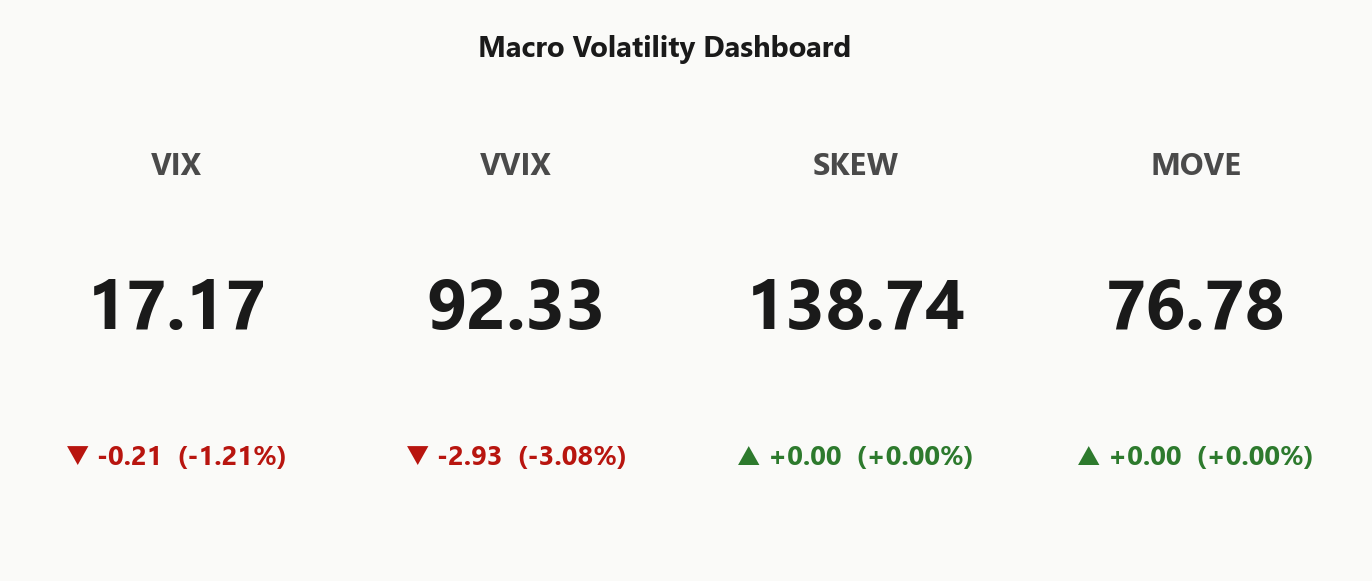

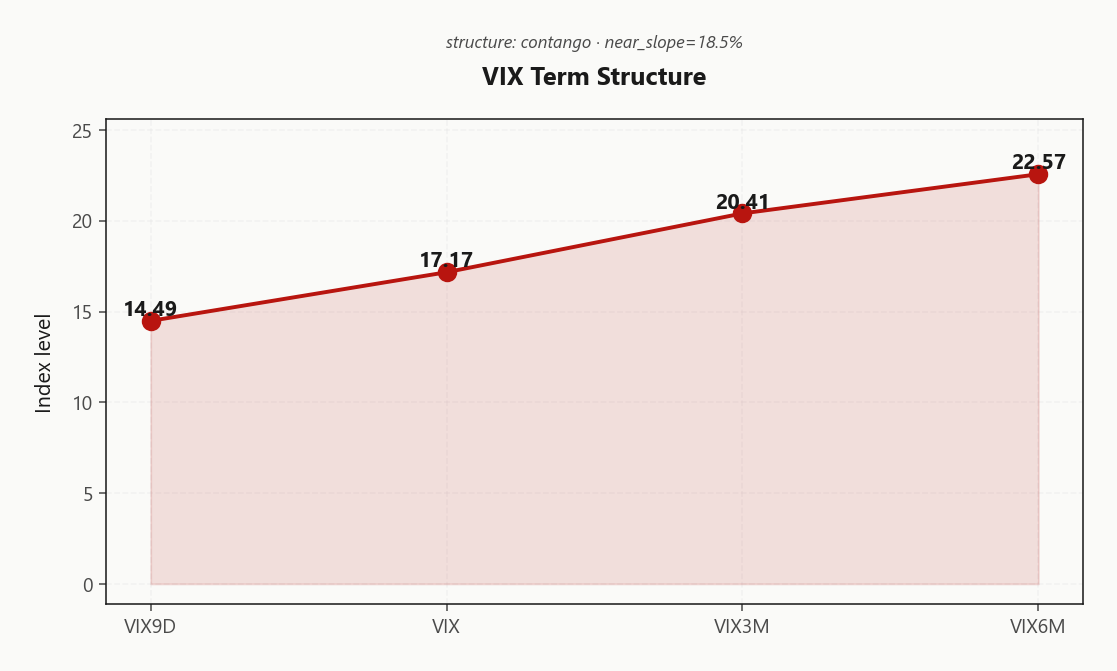

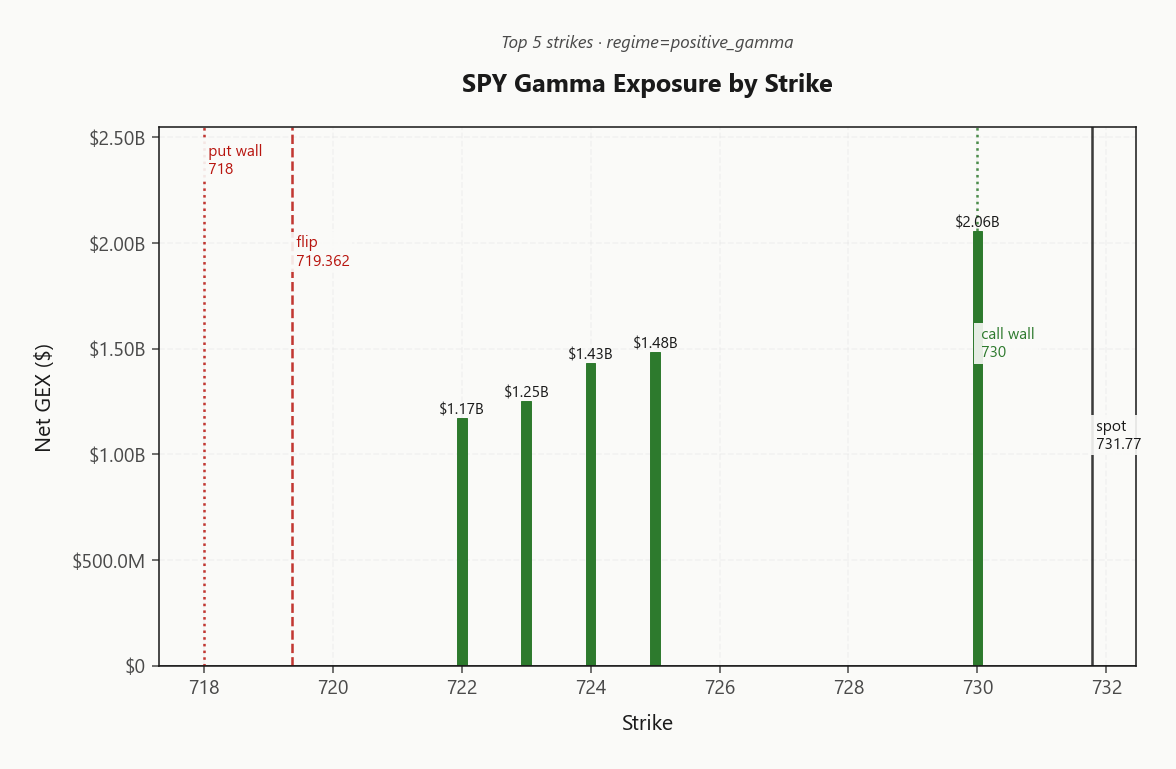

SPY trades at 731.77 with net GEX at $12.7B - dealers are firmly long gamma and the regime is Positive Gamma. The call wall sits at 730.00, put wall at 718.00, gamma flip at 719.36; spot is comfortably above flip, giving the tape a deep dampening cushion. Dealer vanna at -$297.05B means a vol spike would force delta supply - the asymmetry on a downside surprise is real even with gamma cushioning. Charm at -$1.66B skews dealer flow to selling into the close, capping upside. VIX at 17.17 with term structure in Contango and VIX9D at 14.49 signals carry-rich front end; VVIX at 92.33 is normal - no jump premium baked in. VRP at 2.6% confirms options remain rich to realized. Bottom line: fade extensions toward 730.00, lean iron condors in the 30-45 DTE bucket, keep cheap tail hedges on given Elevated / Watchful backdrop.

Positive gamma across index complex with VIX in steep contango and Elevated / Watchful regime persisting

Index complex sits in Positive Gamma with spot well above 719.36, dealers absorbing supply on dips and trimming on rallies. VIX term structure in Contango and VVIX at 92.33 confirm a vol-seller's tape, but Elevated / Watchful regime keeps tail hedges relevant. Iran de-escalation headlines have unwound risk premium, leaving carry trades dominant into the close.

Regime Assessment

The tape sits squarely in Elevated / Watchful territory - VIX at 17.17 isn't pricing panic, but it isn't the slumbering low-vol regime either. Transition probability to a panic state over the next handful of sessions reads 0.05, while the path down into a low regime over the medium window prints 0.45 - a Elevated middle ground that resolves lower more often than it explodes higher.

The half-life of 15 sessions is the operative number. That is sticky enough to lean into carry without being so entrenched that complacency pays - the regime persists, but it persists watchfully. Lean carry, not directional: short premium harvests the drift, while cheap convexity hedges the non-trivial tail that the transition matrix refuses to zero out.

Cross-asset reads Aligned with the equity complex uniformly in positive gamma, reinforcing the watchful-but-not-fragile read. Size standard, harvest the curve, but keep the put-spread on - this regime rewards patience, not heroics.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life and asymmetric transition probabilities favoring decay over escalation. Lean into carry while keeping cheap tail hedges live.

Trading readVIX softening, VVIX normal, MOVE benign, F&G in greed - all four confirming. No divergence flagging an incoming regime shift; the tape is internally consistent.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward 30-60 vol prints 21.8505766514 while 60-90 forwards extend to 24.5406132768, leaving the belly of the curve rich and the back end stickier than the front. That asymmetry is the trade: long-dated vol shorts bleed slowly against persistent backwardation in forwards, while short-dated theta harvests the steepest part of the slope without warehousing tail.

Edge concentrates in the 30-45 DTE bucket where carry is fattest and roll-down most reliable. Calendars and condors structured against the forward 30-60 print are the cleanest expression - short the front, own the belly, let contango do the work.

What it means for your trading

Steep contango from 14.49 through 22.57 hands vol sellers a paid curve; forward 30-60 at 21.8505766514 marks the 30-45 DTE bucket as the harvest zone. Favor short-dated theta over long-dated vol shorts where forwards stay sticky.

Trading readFront-end discount of VIX9D vs VIX with VIX3M/6M layered above = steep contango, vol carry is paid. Market does not price imminent stress.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 12.42% sits well clear of HV20 at 9.82, leaving VRP at 2.6% - options are paid up nicely versus how much the tape is actually moving. Short premium is the path of least resistance here; the carry is fed and the realized print is not catching up.

HV60 at 14.93 still carries the imprint of prior stress - it's in the rearview, not the windshield, but it's the reason long-dated vol shorts don't price as cleanly as the front. Lean the carry trade where the spread is widest: front-to-mid, not the back end.

Across the complex, IWM VRP at 4.78% tops QQQ at 4.5% with SPY at 2.6% - small caps pay the fattest premium per unit of risk. Short vol carry is intact index-wide; the dispersion of richness is the trade tell.

What it means for your trading

VRP at 2.6% with ATM IV running above both HV20 and HV60 confirms options are rich to realized - short premium is the carry trade, with IWM at 4.78% the richest seat in the house.

Skew Convexity

Quarter-delta skew remains steep across the index complex - SPY's put wing prints 13.95% against ATM at 11.84%, while the call side sits at 11%. Skew at 2.95% with smile ratio 1.27% tells the story: downside is bid, upside is flat - no chase into strength even as spot lifts through the call wall.

Cross-asset, the picture is uneven - QQQ at 3.78% and IWM at 2.66% show small-caps materially less skewed than SPY, consistent with the index being the cleanest hedge vehicle and absorbing the bulk of macro tail demand. Tails carry a bid, not a panic - Iran de-escalation has compressed the front-month vol, but the wing has not surrendered.

Trade construction: with the put curve this rich relative to ATM, financed structures dominate - put-spreads beat naked puts on cost-per-unit-protection, and call-side overwrites screen poorly given how flat upside vol sits. Defensive bid + flat call skew = collars cheap, but only if you accept the cap.

What it means for your trading

Steep put skew with flat call wing argues for spread-based downside hedges over naked puts; the wing's persistent bid is the market's reminder that Elevated / Watchful is the prevailing regime even as spot grinds higher.

Vol-of-Vol Structure

VVIX prints 92.33 against VIX at 17.17, putting the ratio at 5.38 - squarely Normal. The option-on-option market is not pricing bimodality; there is no jump premium baked into the front of the VIX surface, and the convexity bid that typically front-runs a regime break is absent.

That clears the runway for short-vol structures. Sizing guidance reads Standard Size - no haircut for jump risk, no defensive trim. Combined with steep contango and a Positive Gamma dealer book, the vol-of-vol read is the green light, not the speed bump.

The watch is asymmetric: a reversal of the Iran de-escalation tape would expand the VVIX/VIX ratio first and the VIX print second. Track the ratio rather than the level - ratio expansion through the Normal band is the signal to cut size before realized catches up. Until then, carry collects cleanly.

What it means for your trading

Vol-of-vol at Normal with the VVIX/VIX ratio at 5.38 clears short-premium structures at Standard Size; ratio expansion is the early-warning trigger if headline risk reverses.

Dispersion Spread

Index vol sits moderate against single-name elevation - SPY ATM IV at 12.42% versus QQQ at 18.1% with IWM topping the complex at 20.08%. Correlation is neither collapsing nor spiking; the index basket is dampening while idiosyncratic names carry the risk premium. That gap is the dispersion trade - long single-name vol against short index vol still prints positive carry into the close.

IWM holds the fattest small-cap risk premium of the three, a clean signal that single-stock event risk lives downstream of the index. Index hedges still work mechanically, but the uncorrelated single-name tail is what the basket isn't pricing. Lean SPY/SPX premium selling where liquidity and dampening compound; reserve long-vol exposure for the names where idiosyncratic catalysts haven't decayed into the curve.

What it means for your trading

Spread between IWM at 20.08% and SPY at 12.42% keeps dispersion modestly attractive: short index, long single-name where the gamma cushion doesn't reach.

Liquidity & Microstructure

The book's center of gravity sits at 700 - legacy OI mass parked well below spot - but the live battle is at the 730.00 call wall, where dealer pinning is hardest into the bell. Top-strike GEX concentrates $2.06B at 730.00, magnetizing the tape and capping any reflexive grind higher.

Spot trades comfortably north of the gamma flip at 719.36, leaving the regime firmly Positive Gamma: dealers absorb supply on dips toward the put wall at 718.00 and trim into rallies that press the call wall. Below flip, that flow inverts - dampening becomes amplification, and the cushion that's quieting today's tape becomes tomorrow's accelerant.

Trade the corridor between 718.00 and 730.00; the gamma flip is the regime breaker, not the mid-range OI clusters.

What it means for your trading

OI legacy at 700 is a relic; live dealer flow is anchored at the 730.00 call wall with the put wall at 718.00 as a downside cushion. Watch the gamma flip at 719.36 - that's where dampening flips to amplification.

Trading readGamma stacks heavy at the call wall 730.00 and thins below the gamma flip - dealers actively dampen extensions higher and cushion dips, but lose grip if spot breaches flip.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$297.05B - deeply negative and the most actionable second-order read on the book. Vol up = dealers sell delta - downside amplified if vol spikes: a vol pop forces dealers to dump delta into the move, which is the exact mechanism that converts today's gamma cushion into tomorrow's accelerant if VVIX wakes up. The cushion is real at this vol level; it is not regime-invariant.

Trade implication: fade extensions toward the call wall, but do not press shorts naked - the negative-VEX asymmetry punishes you on a vol surprise. Keep tail hedges live; harvest theta in the belly.

What it means for your trading

Positive-gamma cushion is intact but conditional - VEX at -$297.05B flips dealers from dampeners to amplifiers the moment vol moves, while CHEX at -$1.66B caps upside into the close around the Call Wall pivot at 730.

Cross-Asset Confirmation

Cross-asset confirmation reads Aligned: SPY, QQQ at 692.23, and IWM at 285.31 all sit in Positive Gamma, with VIX the lone counterparty in negative gamma where vol moves still get amplified. There is no fragile pocket in the equity complex to hide behind — the dampening is uniform, and dispersion across index ETFs offers no divergence trade as the lead story.

The macro overlay reinforces the carry tape rather than threatening it. MOVE at 76.78 keeps rates vol benign, removing the cross-asset transmission channel that typically hijacks equity vol regimes. Fear & Greed at 69 prints Greed — trending but not yet at contrarian extremes. Cross-asset tone resolves Unknown; absent credit or rate stress, this is an isolated equity-led carry tape, not a macro shock to fade.

What it means for your trading

With MOVE at 76.78, F&G at Greed, and SPY/QQQ/IWM uniformly in Positive Gamma, the regime is Aligned — lean carry structures with confidence, but watch VIX gamma as the asymmetric tail.

Scenario EV

The EV scoreboard prints clean: Iron Condor at 60 edges the put spread at 51, with the best composite landing at 60. Positive gamma cushion, Steep Contango term, and Normal VVIX all converge on the same trade - symmetric premium harvest, not directional bets. VRP assessment reads Unknown, but ATM IV at 12.42% against HV20 of 9.82 tells you what the scoreboard already knows.

Sweet spot is the 30-45 DTE bucket - fattest part of the contango slope, far enough from gamma pin to breathe, close enough to harvest theta cleanly. Sizing per VVIX comes in at Standard Size; no half-sizing for jump risk, no leveraging for low vol. Anchor wings outside the 730.00 / 718.00 band where dealer flow does the defending for you.

Put spread is the runner-up but the risk-adjusted gap is real - taking directional shape into a Elevated / Watchful regime with a sticky 15-session half-life burns optionality you don't need to spend.

What it means for your trading

Iron condor is the trade: 60 beats put spread 51 in the 30-45 DTE bucket at Standard Size. Symmetric premium harvest fits the regime; directional shape doesn't pay enough to justify the convexity spend.

Actionable Summary

Synthesis: Positive Gamma across the index complex, VIX in Contango, VVIX Normal, and a Elevated / Watchful regime overlay - this is an iron condor tape, not a directional one. Optimal expression is Iron Condor in the 30-45 DTE bucket where forward vol carry sits fattest. Sizing: Standard Size - no jump premium baked in to justify a haircut.

The pivot to watch is 730 (Call Wall); above it dealers shed delta into the bell, capping drift. Avoid chasing through the 730.00 call wall and avoid naked puts below 718.00 - skew steepness makes spread protection the cleaner hedge. Keep cheap OTM put-spreads on; the regime is sticky but Elevated / Watchful, and a vol pop weaponizes -$297.05B against the cushion.

Bottom line: harvest premium, fade extensions, respect the 719.36 flip as the regime breaker.

What it means for your trading

Iron condor in the 30-45 DTE bucket is the highest-EV expression while spot holds above 719.36 and VVIX stays Normal. Cap upside chase at 730.00, hedge with put-spreads rather than naked puts given skew, and treat the flip as the kill-switch on the carry trade.

One-page memo to end the war is the single highest-impact macro headline today - vol curves are pricing the resolution path.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.22 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 719.36 against a spot of 731.77. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.42% with a volatility risk premium of 2.6%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.17. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime