Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

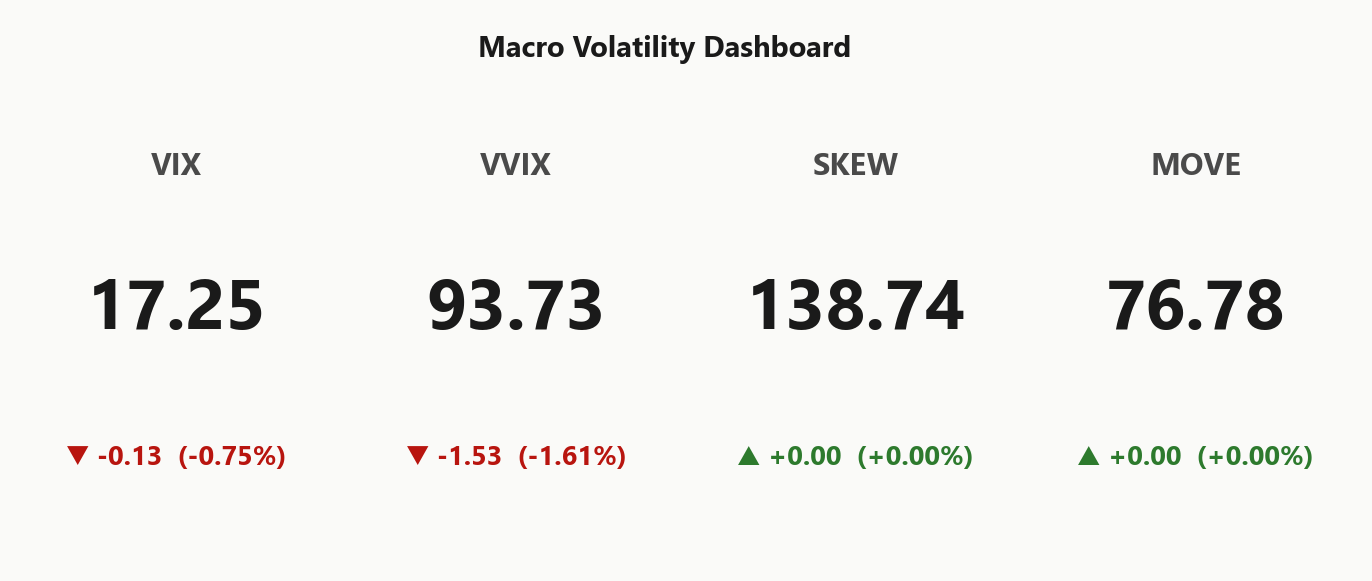

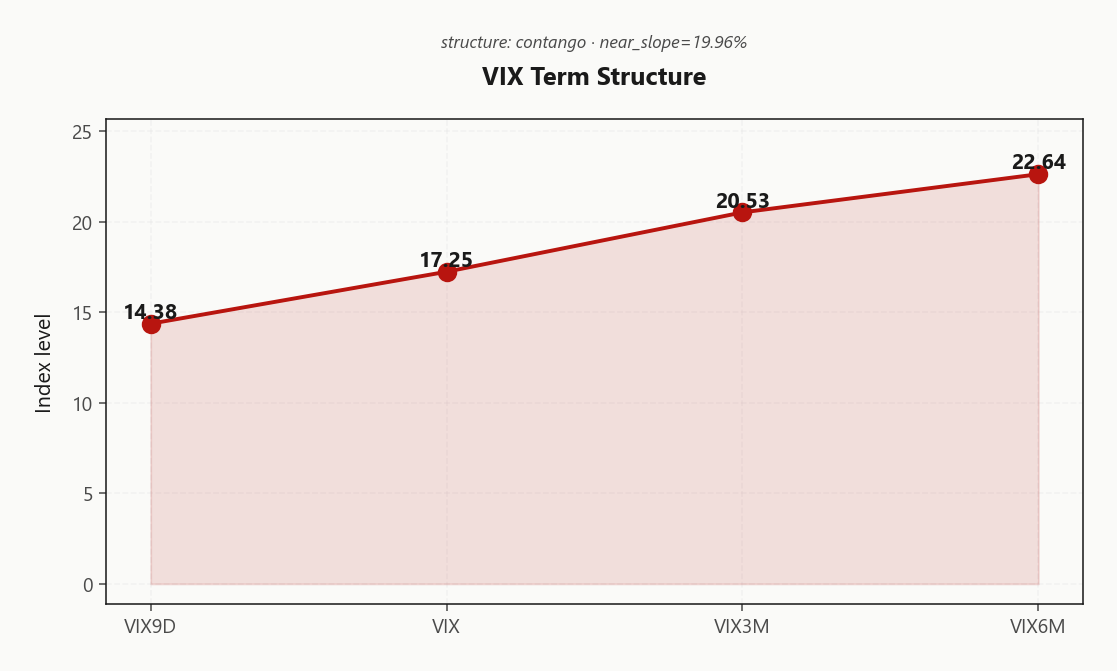

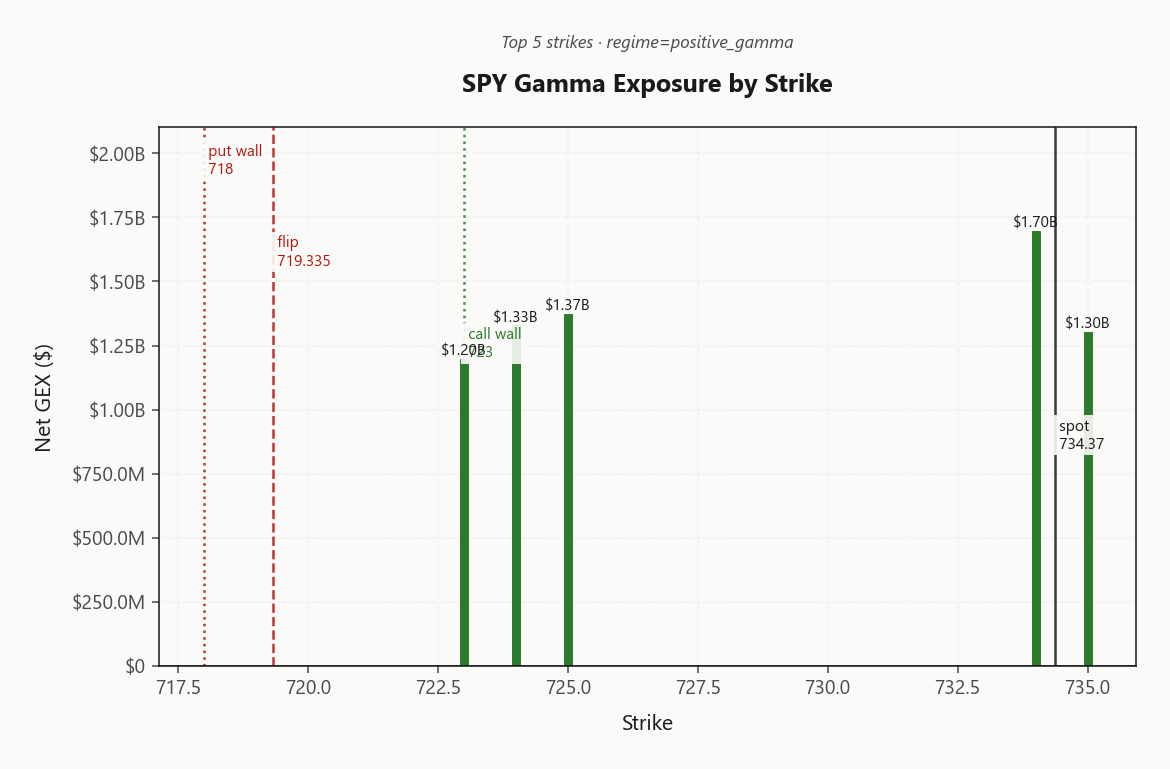

SPY at 734.37 sits in positive gamma with net GEX of $12.48B - dealers long gamma, moves dampened, mean-reversion the dominant intraday flow. Call wall stacks at 723.00, put wall at 718.00, gamma flip at 719.33 - spot trades comfortably above flip, deep cushion in place. Net VEX at -$294.56B means a vol spike would force dealers to sell delta, so downside accelerates if VIX breaks higher; charm at -$2.4B drips selling pressure into close. VIX prints 17.25 with term structure in Contango (14.38 → 20.53) and VRP at 2.71% - options are paid over realized, vol carry is alive. VVIX at 93.73 sits in normal range, no jump-risk premium being demanded. Fear & Greed reads Greed at 69 - sentiment lean cautions against chasing strength. Bottom line: sell premium structures preferred - Iron Condor in the 30-45 DTE window, fade rallies into 723.00, only flip defensive if SPY breaks 719.33.

Positive gamma across index complex with steep VIX contango - vol sellers favored, mean-reversion dominant

Index complex sits firmly in positive gamma with SPY at 734.37 above its flip at 719.33, dealers long gamma and dampening every move. VIX term structure prints Contango with VVIX at 93.73 confirming a benign vol-of-vol backdrop. The setup pays carry sellers - the Iron Condor scores best with 30-45 DTE the sweet spot.

Regime Assessment

Regime classifies as Elevated / Watchful with VIX anchored at 17.25 - elevated enough to keep the desk honest, far enough from stress to keep carry structures live. The transition matrix prints a 0.05 probability of escalating to panic over the next week, with a 15-session half-life - this state is sticky, not coiled.

Cross-asset reads Aligned: SPY, QQQ, and IWM all sit in Positive Gamma above their flips, with VIX itself the only short-gamma leg. VVIX at 93.73 and the term structure printing Contango argue the path of least resistance is grind, not gap. No bimodal jump premium is being demanded, and the dealer cushion above the flip at 719.33 remains deep.

Posture: watchful, not defensive. Stay in carry mode - Iron Condor in the 30-45 DTE window - and only pivot defensive on a VVIX expansion or a clean break of 719.33.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life and panic-transition probability at 0.05 - persistent, not fragile. Stay in carry; the regime breaks before the trade does only if VVIX expands or spot loses 719.33.

Trading readVIX easing, VVIX in normal, MOVE suppressed, SKEW elevated - three of four confirm benign, but elevated SKEW is the quiet warning that tail bids haven't fully gone away.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

VIX term structure prints Contango with the front-end at 14.38 sitting well below spot VIX at 17.25 - no near-term stress is priced in, and the curve stacks higher into 20.53 at three months. This is a structural carry signal, not event premium pricing in a known catalyst.

Forward vol from front to belly implies mean-reversion higher but stops well short of panic - the slope is paying sellers to absorb the gap between suppressed realized and the term-curve's reflexive drift. Regime reads Steep Contango, and the steepest roll-down sits in the belly of the curve.

Best edge is in selling 30-60 DTE where the slope steepens hardest - calendars selling front-month against the back-end harvest the contango cleanly without taking outright vol direction. Front-end is too compressed to short naked; the back-end too far to buy as a hedge. The belly is where the carry concentrates.

What it means for your trading

Steep Contango from 14.38 through 20.53 with regime Steep Contango hands vol sellers the cleanest carry of the cycle. Calendar spreads in the 30-60 DTE belly are the highest-conviction structure for harvesting the slope.

Trading readSteep contango with no kink says the market expects no near-term stress - vol carry trade is fully alive, sellers paid across the belly.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV prints 12.85% against HV20 at 10.14 - a clean, positive VRP of 2.71% sitting on the tape. Recent realized has been suppressed and options are paying premium over actual movement, so short-vol structures collect the spread without leaning on a directional call. With HV20 trailing HV60 at 15.02, realized is decelerating, not regime-shifting - the carry signal is the trade.

Options stay rich versus the recent tape, which is the textbook VRP harvest setup. Outright short straddles aren't the play; defined-risk structures lock in the spread without exposing to a single-print gap. Calendars and condors are the cleanest expressions - they monetize the IV-RV gap while the dealer cushion does the heavy lifting around spot.

Net-net: premium sellers are paid here, and the path of least resistance is to harvest the VRP with structure, not size. Stay defined-risk, stay inside the corridor, and let realized's deceleration keep doing the work.

What it means for your trading

VRP at 2.71% is positive and active with HV20 of 10.14 running below HV60 at 15.02 - short-vol via calendar or condor, not naked straddle, captures the edge without tail exposure.

Skew Convexity

Quarter-delta skew prints 2.8% with a smile ratio of 1.26% - an ordered downside premium, not a panic bid. The put wing pays 13.7% against ATM at 12%, while the call wing sits compressed at 10.9%. Tail demand is present but disciplined - desks are funding standing protection, not chasing convexity.

The compressed call wing is the tell: no upside conviction premium being demanded even on a record-print tape, which keeps overwriting and call-side condor wings cheap to sell. On the put side, the modest steepness makes spread protection materially cheaper than naked downside - finance the put leg into a debit spread rather than paying the full put-25d carry. With VVIX at 93.73 and the regime tagged Elevated / Watchful, convexity is harvestable without a half-size haircut.

Net: skew is steep enough to pay sellers but flat enough to keep wings affordable - a textbook Iron Condor backdrop in the 30-45 DTE window, with put spreads as the preferred tail-hedge expression.

What it means for your trading

Skew at 2.8% and smile ratio 1.26% signal ordered tail demand without panic - sell the call wing, finance puts via spreads, and harvest the Iron Condor carry.

Vol-of-Vol Structure

VVIX prints 93.73 against VIX at 17.25, putting the ratio at 5.43 - squarely in the Normal band. No bimodal jump premium is being demanded; the tape isn't pricing a crush-or-spike binary, and the convexity bid that normally fattens short-vol left tails is absent.

That reads through directly to sizing: Standard Size on the recommended Iron Condor in the 30-45 DTE window - no half-size haircut, no defensive notional cap. Carry sellers get to deploy full clip into the contango slope without paying up for vol-of-vol asymmetry.

Tail hedges remain cheap as ballast - wing protection isn't bid, so layering OTM puts as a portfolio overlay costs little and converts a clean short-premium book into a hedged carry trade. Watch VVIX expansion above the normal band as the first sizing trigger; until then, the regime pays you to stay full-size.

What it means for your trading

VVIX at 93.73 with the ratio at 5.43 clears the desk for Standard Size short-vol deployment. Cheap wings make hedged condor structures the clean expression - no jump premium to fight, no haircut to take.

Dispersion Spread

Index vol prints cheap to its components: SPY ATM IV at 12.85% runs well under QQQ at 19.25% and IWM at 20.96%. With the complex Aligned in positive_gamma, realized correlation stays bid and the index basket suppresses its own vol while single names retain their idiosyncratic premium - classic dispersion geometry, but on the wrong side for selling component vol blindly.

The cleaner harvest is at the index, not the leg. Sell SPY premium where dealer cushion does the dampening for you; resist the temptation to short QQQ or IWM straddles ahead of earnings clusters where single-name tape risk dominates the carry. The relative-value lean is a SPY-versus-QQQ vol pair - long index gamma against short component gamma - which monetizes correlation if it stays anchored without taking on idiosyncratic event risk.

Bottom line: index hedges and index condors carry the cleanest edge in the 30-45 DTE window. Single-name short vol is the trade that prints the P&L screenshot until one earnings gap erases the quarter.

What it means for your trading

Dispersion geometry favors selling index vol over component vol - SPY at 12.85% is cheap relative to QQQ 19.25% and IWM 20.96%, but that means index hedges, not single-name short straddles, are the clean carry. SPY-vs-QQQ vol pair is the relative-value expression.

Liquidity & Microstructure

The OI map and the live gamma map are telling different stories - highest OI sits down at 700, but the magnet that matters intraday is stacked at 734.00 where $1.7B of dealer length is parked. Spot trades above the flip at 719.33, so dealer flow leans supportive on dips and suppressive into rips, funneling the tape toward that top-strike pin.

The corridor is clean: 723.00 caps upside as dealers sell into strength, 718.00 is the floor where bid reappears. Fade pushes into the call wall, lean long the cushion above the put wall, and treat the gamma flip at 719.33 as the line in the sand - a break flips the regime and dealer flow inverts.

What it means for your trading

Live gamma at 734.00 is the intraday magnet inside a 718.00 - 723.00 corridor; only a break of 719.33 flips the dealer-flow regime.

Trading readHeavy positive gamma stacked at and above spot through the call wall says dealers dampen every push higher - fade strength into 723.00, mean-reversion is the dominant intraday flow until spot clears 719.33.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$294.56B - a vol pop forces dealers to sell delta, so any VIX expansion becomes a vanna accelerant on the downside rather than a benign repricing. The cushion from positive gamma is real, but it is conditional on VIX staying anchored; lose that anchor and the same book that dampens flips into a procyclical seller.

Charm reads -$2.4B, dripping mechanical dealer sales into the close as long calls bleed delta - a quiet headwind that compounds against intraday strength. The flow pivot sits at the call wall 723: below it, dealers lean against rallies and bid dips; through it, the vanna/charm signs invert and the cushion thins fast.

Bias stays Neutral until spot clears the wall. Trade the corridor, fade pushes into 723.00, and treat a VVIX break out of normal as the trigger to cut short-vol size - that is the path where vanna does the damage before charm can close the day.

What it means for your trading

Negative VEX plus negative CHEX means the dealer book is supportive at rest but procyclically short on a vol shock; stay in carry while spot holds below 723 and bias is Neutral, flip defensive only on a VVIX expansion or a clean break of the wall.

Cross-Asset Confirmation

Cross-asset tape prints Aligned - MOVE at 76.78 sits suppressed, no rates or credit stress leaking into the equity book, and the dovish duration bid is travelling alongside risk rather than against it. QQQ at 697.56 and IWM at 286.71 both hold positive_gamma alongside SPY, so the dealer cushion is broad-based rather than mega-cap concentrated - no rotation break to fade, no small-cap warning shot.

Fear & Greed reads Greed at 69, the one yellow flag in an otherwise green print. Sentiment is supportive of the carry regime but the contrarian risk is rising - crowded long into a record tape is where chasing strength pays the worst risk-reward. Iran-deal optimism is the macro tailwind compressing front-end vol; if the headline reverses, the suppressed MOVE is the first place stress shows up.

What it means for your trading

Cross-asset signals confirm the carry regime - MOVE at 76.78 and QQQ/IWM aligned with SPY in positive gamma leave no divergence to lead with, but Fear & Greed at Greed flags crowded sentiment as the contrarian watch.

Scenario EV

Synthesis pays the carry seller. With SPY in Positive Gamma, VIX term structure printing Contango, and VVIX at 93.73 in normal range, the EV scoring lands on Iron Condor with a best score of 54 - the structure that monetizes the slope without leaning directional inside the dealer corridor.

Sweet spot is 30-45 DTE, where the contango steepens hardest and theta compounds against suppressed realized. VRP read is Unknown, but the volatility geometry - IV at 12.85% over HV20 at 10.14 - keeps the premium harvest live. Strikes work outside the 718.00 floor and 723.00 ceiling, with the gamma flip at 719.33 as the kill-switch.

Sizing stays standard - VVIX/VIX at 5.43 tags Standard Size, no half-size haircut warranted. Bias remains Neutral with the pivot stacked at 723; only flip defensive if spot loses the flip.

What it means for your trading

Iron condor in the 30-45 DTE window is the cleanest expression of positive gamma plus contango - strikes outside 718.00 and 723.00, standard sizing, kill-switch at 719.33.

Actionable Summary

Setup is textbook carry: SPY anchors Positive Gamma with net GEX at $12.48B, spot trading comfortably above the gamma flip at 719.33 and pressed into the 723.00 call wall. VIX term structure prints Contango from 14.38 through 22.64, and VVIX at 93.73 sits in normal range - no jump premium, standard sizing applies.

Trade: sell premium via Iron Condor in the 30-45 DTE window, strikes outside 718.00 and 723.00 to harvest the 2.71% spread. Fade rallies into the call wall - dealer flow caps follow-through. Avoid long vol and naked upside chase; Greed at 69 says sentiment is crowded long.

Triggers: regime breaks if SPY loses 719.33 - flip defensive, cut shorts. Sizing tightens if VVIX clears normal. Charm pivot at 723 defines the flow line; bias Neutral until cleared. Regime label Elevated / Watchful - watchful, not defensive. Let the dealer cushion work.

What it means for your trading

Carry regime confirmed across positive gamma, Contango, and normal vol-of-vol - sell Iron Condor in 30-45 DTE, fade strength into 723.00, only flip defensive if 719.33 breaks.

CMA CGM vessel hit in Strait of Hormuz is the geopolitical tail-risk reminder - keeps tail hedges relevant even with Iran-deal headlines compressing front-end vol.

Iran reviewing US proposal with sources signalling deal proximity is the catalyst behind the day's vol crush - risk premium compression directly visible in MOVE and VIX9D.

Europe's STOXX 600 up 2% on Iran-deal optimism confirms global cross-asset risk-on alignment - supports the no-divergence read in the cross-asset section.

US crude and fuel inventories falling as Iran war roils energy markets is the lingering inflation/rates risk if the deal falters - relevant for bond/equity correlation watch.

Iran war pausing global central bank easing is the under-the-radar macro story - if the deal closes, dovish repricing is the next catalyst the curve will need to absorb.

Stocks and bonds rallying together on US-Iran deal headlines is the rare risk-on/duration-on combo - confirms today's benign cross-asset alignment.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.39 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 719.33 against a spot of 734.37. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.85% with a volatility risk premium of 2.71%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.25. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime