Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

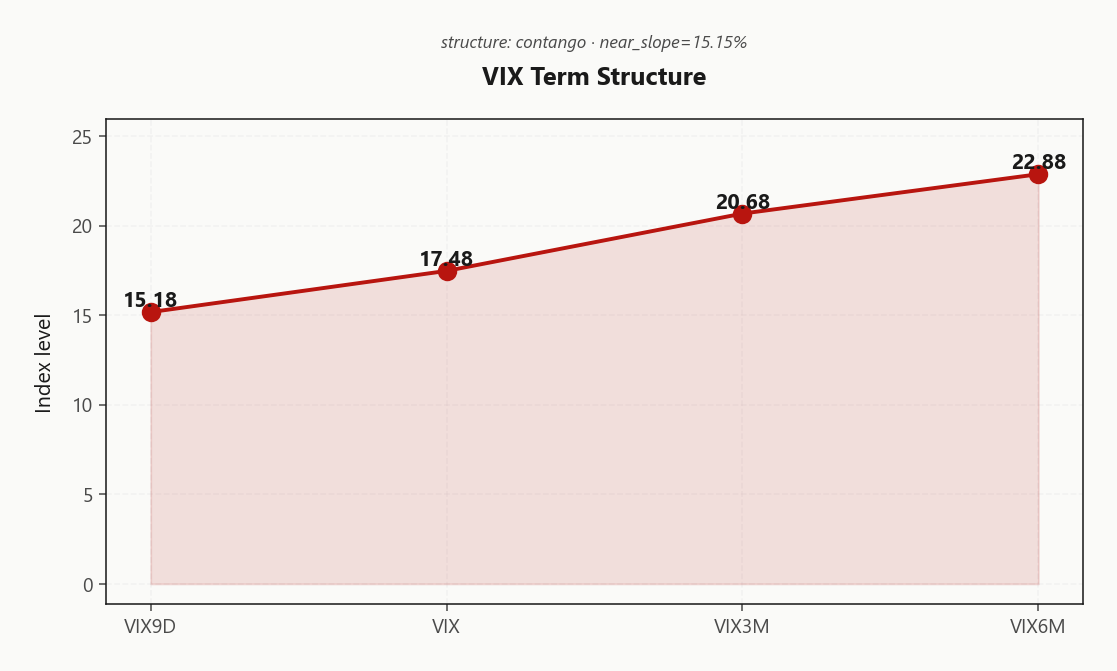

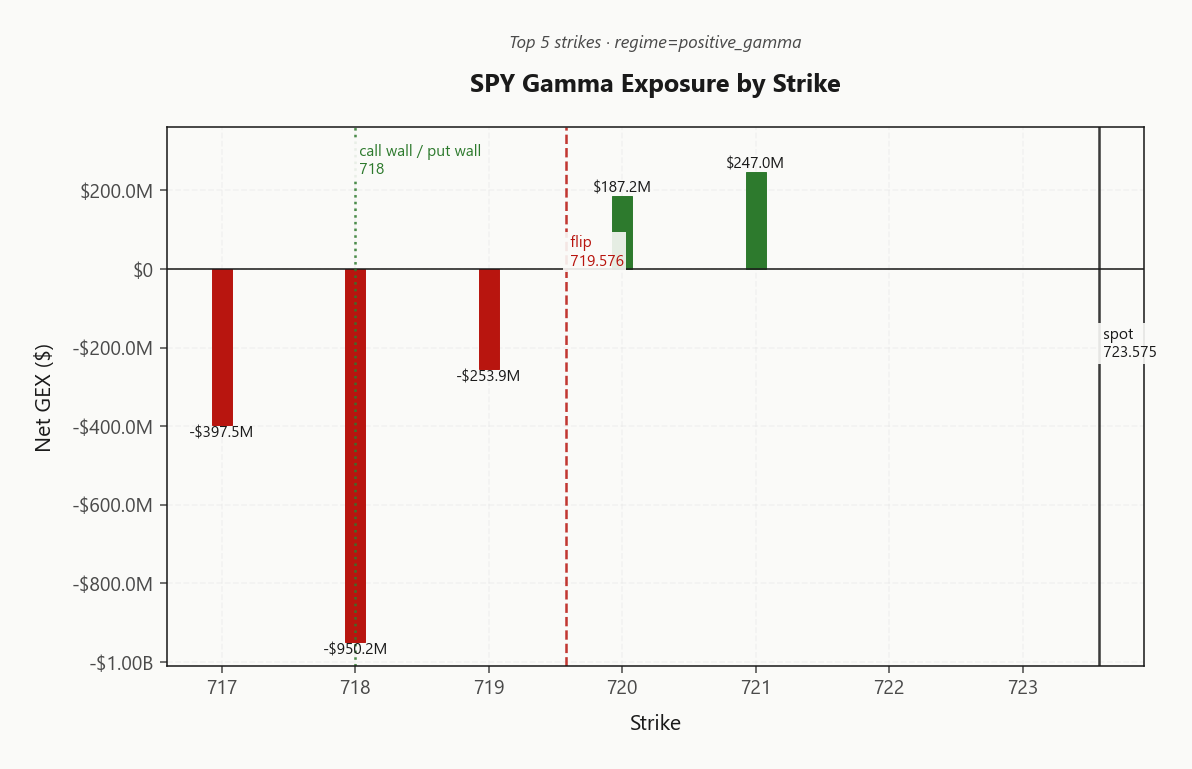

SPY at 723.58 sits above the gamma flip at 719.58, with the index complex in Positive Gamma regime - dealers dampen moves, mean reversion wins. Call wall and put wall both anchor at 718.00, with max pain at 720.00 and the heaviest OI cluster at 710. Dealer vanna at -$51.4M and charm at -$370M suggest pressure to sell into close if vol drifts higher. VIX at 17.45 with term structure in Contango (15.18 → 20.68) keeps vol-sellers' carry intact, and VVIX at 95.79 is normal - no jump-risk premium. VRP across SPY/QQQ/IWM is positive (SPY 0.66%, QQQ 3.15%, IWM 3.34%) so options remain rich to recent realized. Bottom line: lean iron condor in the 30-45 DTE window, fade strength into the 718.00 wall, and only flip defensive if SPY breaks below 720.

Positive gamma across index complex with Steep Contango VIX curve - vol sellers favored, mean reversion dominant

SPY trades above gamma flip at 719.58 with dealers long gamma, dampening intraday moves while VIX in Contango signals structural carry. Iron condor scores best given Unknown VRP and normal vol-of-vol. Watch the charm pivot at 720 - bias flips below it.

Regime Assessment

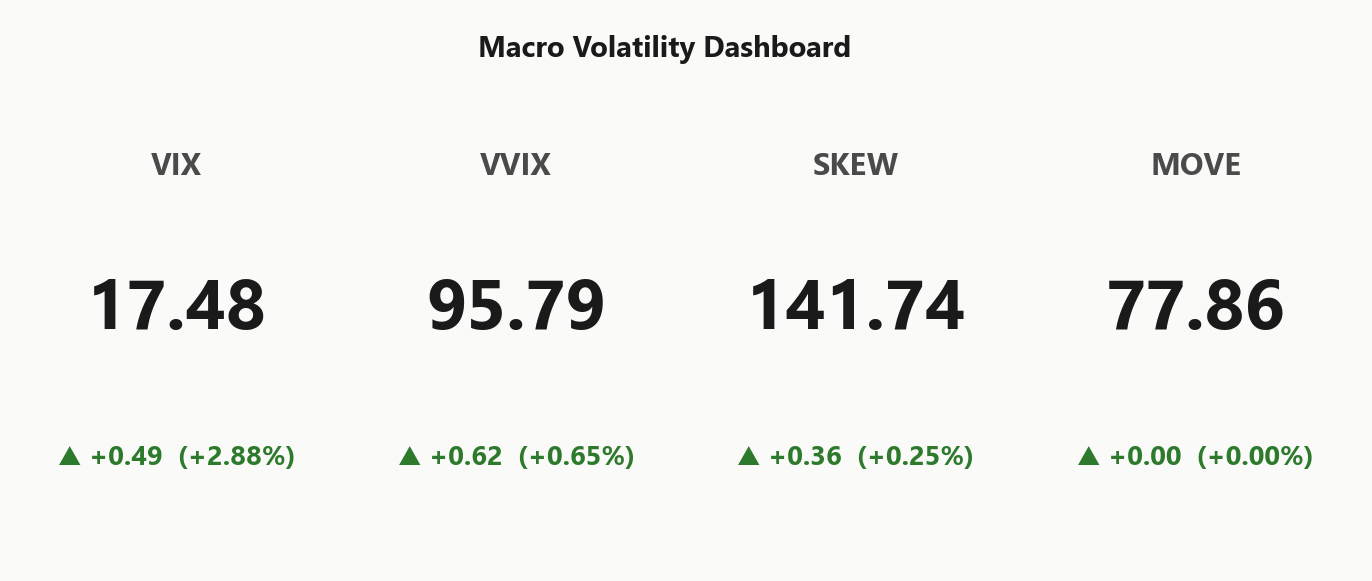

The tape sits squarely in Elevated / Watchful territory, with VIX at 17.48 bid into a green tape - a quiet warning that the market is paying for protection even as spot grinds higher. Panic-transition odds over the next handful of sessions read 0.05, and the regime carries a half-life of 15 sessions - sticky, not fragile, but not cooling on its own either.

Cross-asset reads Aligned: SPY, QQQ, and IWM all anchored above their flips in positive_gamma, MOVE quiet, F&G in Greed. No credit shock is incubating; the elevated VIX print is geopolitical noise priced into the wing, not a structural break. Probability of regime cooling within ten sessions sits at 0.45 - material, but not the modal path.

Trade it as elevated-but-contained: harvest the contango, fade extremes into 718.00, and treat a break of 720 as the trigger that flips the regime classification, not a level to pre-hedge.

What it means for your trading

Regime is Elevated / Watchful with VIX at 17.48 - sticky for 15 sessions, with panic odds at 0.05. Stay in carry mode; let the charm pivot, not the headlines, dictate any defensive shift.

Trading readVIX modestly bid, VVIX normal, SKEW elevated, MOVE flat - equity vol slightly nervous but rates calm and tail-protection bid. Divergence between SKEW and MOVE worth watching.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve prints a textbook ladder: 15.18 on the front, 17.48 at spot, 20.68 at the belly - Steep contango - vol sellers favored. Front-end carries no event hump; the market is not pricing imminent stress despite Iran headlines, and the Contango read confirms vol sellers retain the structural bid.

Forward vol tells the same story with sharper teeth: the 22.1069762745 and 24.8862693066 segments sit well above spot VIX, meaning long-dated vol stays bid even as the front collapses. That's where the slope steepens hardest, and where calendar roll-down compounds.

Trade the slope, not the level. Best edge lives in the 30-45 DTE window - long the back, short the front, harvest theta into the curve's natural pull. No backwardation flag means no defensive pivot required; Steep Contango is the regime to lean into until the front-end inverts.

What it means for your trading

Curve in Steep Contango with 15.18 < 17.48 < 20.68 - vol sellers paid, calendars favored, no front-end event premium to fade.

Trading readSteep contango with VIX9D well below VIX3M - vol-sellers' carry is paid. Market is not bracing for stress; calendar trades and short front-month structures favored.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 12.82% sits a hair above HV20 at 12.16, leaving the index VRP at 0.66% - positive but compressed. Options are slightly rich to actuals, not fat. This is a textbook carry tape: premium exists, but not enough to pay you for index-level convexity risk if realized snaps higher.

The dispersion picture rewires the trade. QQQ VRP at 3.15% and IWM VRP at 3.34% both run multiples of the SPY spread, with the index complex Aligned in Positive Gamma. Tech and small-cap implieds are paying for idiosyncratic risk that diversifies out at the index level - that's where the harvestable premium lives.

Bottom line: rotate vol-selling out of SPY into QQQ and IWM strangles or condors in the 30-45 DTE window. Reserve SPY for the delta hedge, not the premium leg.

What it means for your trading

SPY VRP at 0.66% is too thin to justify naked index short vol; QQQ at 3.15% and IWM at 3.34% are the richer premium pockets. Sell single-name index proxies, hedge with SPY.

Skew Convexity

Quarter-delta put skew remains steep at 3.77% with the smile ratio printing 1.37% - left tail is bid, OTM puts at 14.03% trade a clear premium to ATM at 11.57%. This is ordered skew, not panic skew; the curve is doing its job pricing downside convexity while the tape grinds higher.

The call wing tells the more interesting story: OTM calls at 10.26% sit below ATM, a flat-to-inverted right side that says no one is paying up for upside convexity. Defensive positioning underneath a green tape - hedges retained, melt-up calls untouched.

Trade implication: convexity is paid for on the put side, so structure downside hedges as put spreads rather than naked puts to monetize the skew you're buying. On the call side, overwriting and call-spread financing of put protection screens cleanly given the inverted right wing. Iron condors in the 30-45 DTE window collect asymmetric premium from the steep left and cheap right.

What it means for your trading

Steep put skew at 3.77% with smile ratio 1.37% flags retained downside hedges, while flat-to-inverted call skew signals zero upside conviction - favor put spreads over naked puts and finance with overwrites.

Vol-of-Vol Structure

VVIX prints 95.79 against VIX at 17.48, putting the vol-of-vol ratio at 5.48 - squarely in the Normal band. No bimodal pricing in the wings, no jump-risk premium stacked on top of spot vol. The tape is paying you for vega, not for the volatility of vega.

Sizing guidance reads Standard Size: full clip on the recommended Iron Condor in the 30-45 DTE pocket. Tail hedges are optional here, not mandatory - the convexity bid that forces defensive trims is absent. Pair the vol sale with the Steep Contango curve and you collect both theta and roll-down without paying up for a kurtosis hedge that the market itself isn't bidding.

Watch for VVIX/VIX drifting toward the upper band: that's the signal to halve clips, not today's print.

What it means for your trading

VVIX at 95.79 and a 5.48 ratio confirm Normal vol-of-vol - deploy Standard Size on short-vol structures with tail hedges optional.

Dispersion Spread

Index vol is the cheap pocket today: SPY ATM IV at 12.82% sits well inside QQQ at 18.66% and IWM at 20.88%, with cross-strike dispersion at 52.55. SPY VRP at 0.66% is thin tape; QQQ at 3.15% and IWM at 3.34% carry the fat premium, and that gap is where the edge lives.

The asymmetry is idiosyncratic, not macro - single-name tech and small-cap noise inflates QQQ/IWM vol surfaces while SPY's cap-weighted blend dampens the print. Index hedges are not capturing that risk, so paying SPY puts to short QQQ/IWM premium is the cleaner expression. Dispersion is alive, correlation is soft, and the regime is Aligned across the index complex.

Trade: harvest QQQ and IWM strangles in the 30-45 DTE window, finance the wing with SPY put structure rather than naked short index vol. Single-name premium harvest beats index vol-selling here on every score.

What it means for your trading

Dispersion regime - QQQ/IWM VRP carries meaningful premium over SPY, so rotate vol-selling to the index proxies and use SPY puts as the hedge leg rather than the short-vol vehicle.

Liquidity & Microstructure

OI clusters at the call/put wall convergence around 718.00, with the heaviest concentration stacked at 718.00 carrying -$950.2M of dealer gamma. The top OI strike sits at 710, anchoring the book into a tight band where put wall and call wall converge - a classic pin geometry.

The gamma flip at 719.58 sits a hair from spot, currently -0.4940745603 away. Above the flip, dealer buying dampens rallies and reinforces the Positive Gamma dampening regime; below it, dealer selling amplifies and inverts flow direction. The proximity is the tell - there's no buffer here.

Trade the structure: fade strength into 718.00, lean on the 718.00 shelf for support, and treat 719.58 as the single binary level. Break it and dealer flow flips from suppressive to accelerant in a single tick.

What it means for your trading

Microstructure is deep but knife-edge - OI converges at 718.00 while the gamma flip at 719.58 sits adjacent to spot, leaving dealer flow supportive above and amplifying below with no cushion in between.

Trading readGamma stacked above spot all the way to the call wall - dealers will sell into rallies, fade strength into 718.00. Below the flip at 719.58, flow reverses and amplifies selloffs.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order Greeks tell a more cautious story than the headline gamma print. Net VEX at -$51.4M means books are short vanna - any uptick in implied vol forces dealers to sell delta, mechanically pressuring spot. Net CHEX at -$370M compounds the problem: charm bleeds long deltas off dealer inventory as the clock runs, translating into a structural sell-into-close impulse that grows with each passing hour.

The pivot to watch is 720, anchored at max pain - current bias reads Neutral, but that label is a knife-edge given the negative vanna/charm pair. Above the pivot, dampening still wins; below it, charm and vanna align with negative gamma to amplify weakness. The single inflection remains the gamma flip at 719.58, where dealer flow inverts outright.

What it means for your trading

Long gamma masks a hostile vanna/charm setup - a vol bid or a slip through 720 turns dealers into sellers, and the regime breaks decisively at 719.58.

Cross-Asset Confirmation

Cross-asset tape reads Aligned: QQQ at 681.04 and IWM at 282.32 both sit above their gamma flips, mirroring SPY's Positive Gamma stance. No index is leaking - the dealer-dampening regime is a complex-wide phenomenon, not an SPY-only artifact, which means mean-reversion gravity is reinforced rather than diluted.

Rates volatility is the tell. MOVE at 77.86 is quiet - no credit-shock signal bleeding through from the Iran headline churn, no rates-driven repricing of equity risk. Fear & Greed sits at 67 in Greed, which combined with elevated put skew flags complacency under the surface but no panic bid in fixed income. Equity vol is doing the worrying alone.

Bottom line: geopolitical noise is mean-reverting, not compounding. Treat Iran/UAE airspace headlines as transitory; the credit channel is clean. Stay with the carry trade until MOVE wakes up or QQQ/IWM lose their flips.

What it means for your trading

Index complex is Aligned in positive gamma with MOVE at 77.86 signaling no credit stress - geopolitical headlines are noise, not a regime trigger. Carry stays paid until rates vol bids or QQQ/IWM break their flips.

Scenario EV

Scenario scoring lands cleanly on Iron Condor at 51, with the put spread alternative trailing at 41. The setup is textbook: SPY locked in Positive Gamma above the flip at 719.58, VIX curve in Contango from 15.18 through 20.68, and VVIX parked at 95.79 - no jump premium to underwrite.

Optimal window is the 30-45 DTE band where the contango slope pays steepest theta and dealer-dampening still applies. VRP assessment reads Unknown on SPY, but QQQ at 3.15% and IWM at 3.34% mark the richer pockets - rotate the wings into the single-name proxies for fatter premium.

Sizing is full. Standard guidance from the vol-of-vol read means no defensive trim - the only override is a break below the charm pivot at 720, which flips dealers short gamma and invalidates the carry.

What it means for your trading

Iron condor at 51 wins the regime - Positive Gamma, Contango, and normal VVIX line up for full-size carry in the 30-45 DTE window. Defensive flip only if SPY breaks 720.

Actionable Summary

Index complex anchors in Positive Gamma with SPY trading above the gamma flip at 719.58 and dealers actively dampening intraday range. The trade is Iron Condor in the 30-45 DTE window, where contango slope from 15.18 through 20.68 pays the steepest carry and VVIX at 95.79 keeps sizing at Standard Size.

Fade strength into the 718.00 call wall and respect the charm pivot at 720 - that is the line where dealer flow inverts. Avoid naked short SPY vol; VRP at 0.66% is too thin, rotate the premium harvest into QQQ at 3.15% and IWM at 3.34% where the carry actually pays.

Defensive trigger is unambiguous: a SPY break below 719.58 flips dealers short gamma and inverts the dampening regime. Until then, regime read stays Elevated / Watchful - mean reversion dominates, fade extremes, do not chase.

What it means for your trading

Lean Iron Condor in 30-45 DTE with single-name premium rotation into QQQ/IWM; flip defensive only on a SPY break below 719.58.

Iran ceasefire with US holding despite Strait of Hormuz exchange - geopolitical tail risk that the vol curve says is mostly priced; watch oil and MOVE for any compounding signal.

Fortune 500 tracking AI usage at individual level - structural tailwind for mega-cap AI names (MSFT/GOOGL/AMZN), reinforces the dispersion thesis favoring single-name vol over index.

UAE airspace restrictions after Iranian missile/drone attack - geopolitical noise to monitor; if it escalates beyond UAE airspace, MOVE and oil are the early warning, not VIX.

European shares rally on earnings outweighing Mideast worries - global risk appetite confirms the U.S. positive gamma read; cross-asset alignment intact.

Reuters Morning Bid framing on Iran 'Project Freedom' - narrative-shaping read; market is treating geopolitical headlines as transitory, not structural.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.45 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 719.58 against a spot of 723.58. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.82% with a volatility risk premium of 0.66%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.48. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime