Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY at 724.07 closed in Positive Gamma territory with net GEX at $6.83B - dealers long gamma, moves dampened. Call wall at 725.00 is the magnet; gamma flip at 719.24 sits well below spot, leaving a deep cushion. Dealer vanna at -$248.78B flags accelerant risk if vol spikes, but charm at -$1.65B is muted into the weekend. VIX at 17.40 with VIX9D at 14.66 versus VIX3M at 20.83 prints steep contango - front-end carry is paid, term VRP is rich. VVIX at 95.58 keeps sizing standard. Bottom line: iron condor structure scores best at 43 in the 30-45 window - fade strength into 725.00, lean short vol on rich term VRP, only flip defensive on a break of 719.24.

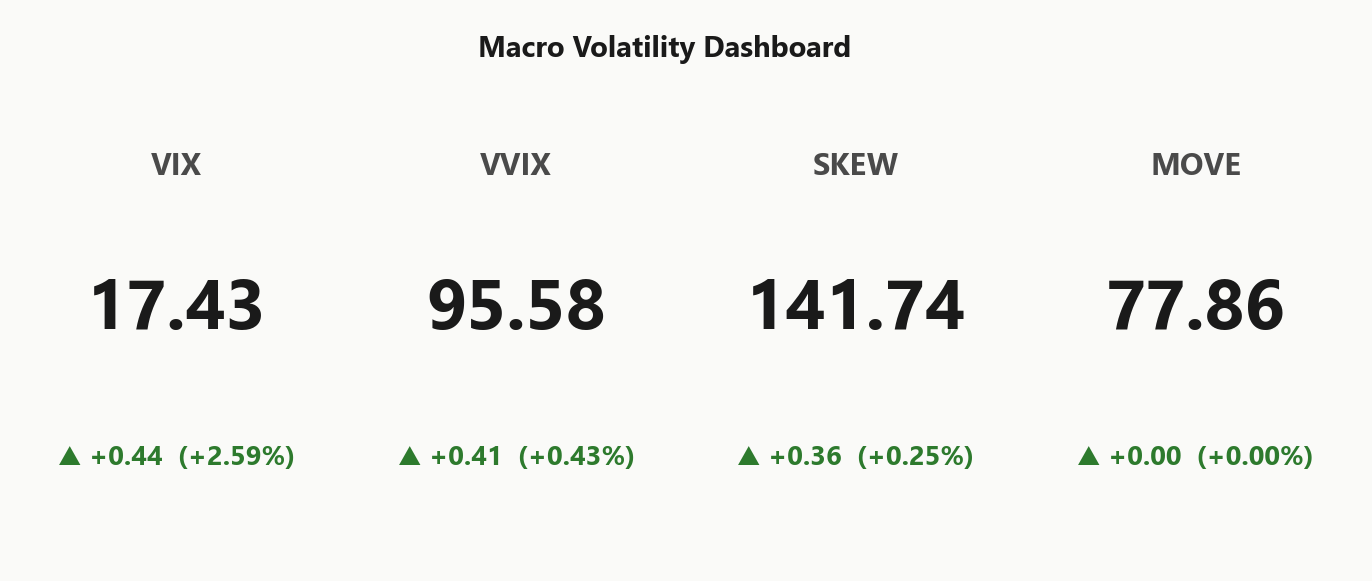

Positive gamma index complex with steep contango - vol sellers favored at 17.43

SPY closes pinned just under the call wall at 725.00 with dealers long gamma and the term structure in steep contango - a textbook vol-seller's tape. VVIX at 95.58 signals no jump-risk panic, while VIX at 17.40 sits in the elevated-but-watchful band. Cross-asset regime is aligned across SPY/QQQ/IWM, leaving idiosyncratic single-name dispersion as the only fragility.

Regime Assessment

Current tape sits in Elevated / Watchful territory with VIX anchored at 17.43 - not stress, not complacency, the watchful middle band where carry pays but you keep one eye on the door. Half-life of 15 sessions makes this regime sticky, not transitional; the base case is persistence, not phase shift.

Transition math reinforces the read: probability of a panic break over the next week prints at 0.05 - negligible - while the path to a low-vol drift over two weeks sits at a meaningful 0.45. Asymmetry favors the downside-in-vol scenario, not the upside spike. Cross-asset alignment at Aligned removes the divergence flag that typically precedes regime change.

Trade implication: short vol here is not chasing a fade - it's leaning into a regime with structural persistence and an asymmetric drift toward lower realized. Size standard, harvest the contango, and let the half-life work.

What it means for your trading

Regime is Elevated / Watchful with VIX at 17.43 and a 15-session half-life - sticky, not transitional, with panic-transition odds at 0.05 versus low-vol drift at 0.45. Short vol is leaning with the regime, not fading it.

Trading readVIX, VVIX, SKEW, MOVE all confirm the same orderly elevated-but-watchful regime - no divergence flag, no leading indicator screaming. Boring is bullish for short-vol carry.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

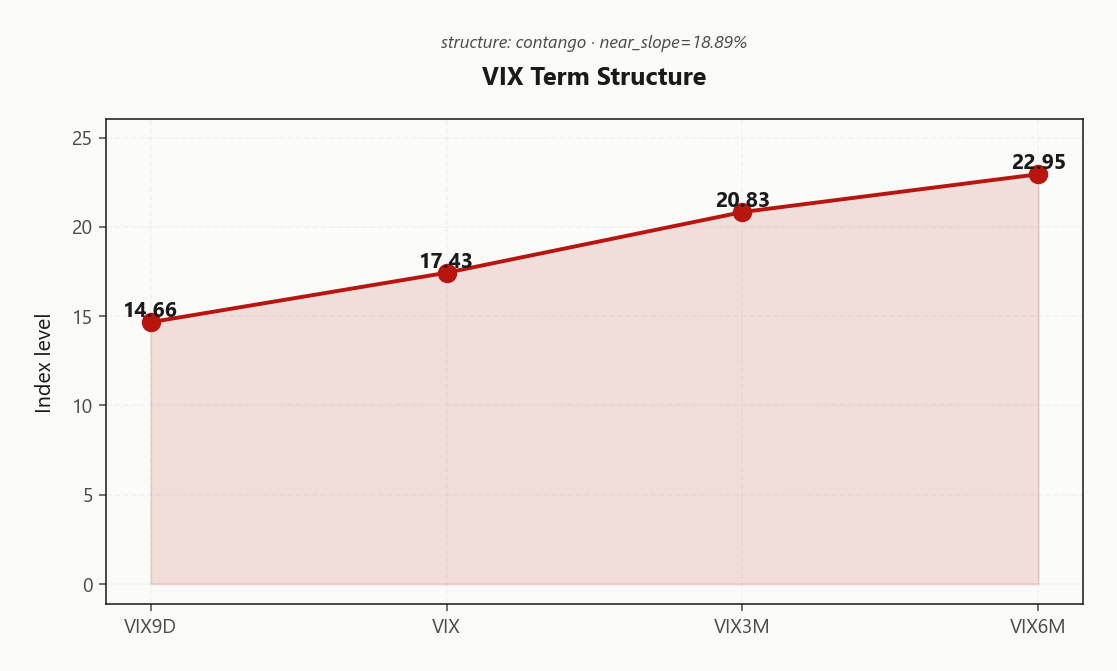

Forward Vol Geometry

The curve is doing the talking. VIX9D at 14.66 versus spot VIX at 17.43 prints a clean front-end discount - the market is paying you to absorb near-dated gamma. From there, VIX3M at 20.83 and VIX6M at 22.95 stack the contango wall, and the near slope at 18.89% is structural, not stress-driven. Term structure is unambiguously Contango.

Forward implied 30-to-60 at 22.3367611797 and 60-to-90 at 24.8900803534 step monotonically higher - calm path priced near, real event premium parked further out. Regime tag: Steep contango - vol sellers favored. The trade writes itself: short front-week premium where carry is fattest, hedge in the three- to six-month bucket where the curve flattens and event risk lives. Calendars long the belly, short the front, are the cleanest expression; avoid owning naked front-end gamma against this slope.

What it means for your trading

Curve is Steep Contango with VIX9D 14.66 through VIX6M 22.95 - short front-week vol, hedge in 3-6m, no event kink to fade.

Trading readSteep contango from VIX9D through VIX6M means the carry trade is paid all the way out - short front-end vol, hedge in 3-6m where curve flattens. No event premium kink.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 12.56% sits a hair above HV20 at 12.16, leaving index VRP at 0.4% - razor-thin and effectively unrewarded. Selling naked SPY vol here is paying for screen time, not edge. HV60 at 14.8 printing above HV20 confirms realized has decelerated into the close - IV is the mean-reverting variable, not the floor.

The asymmetry is in the smaller indices. QQQ VRP at 3.08% and IWM VRP at 3.19% both pay materially better than the index - single-name correlation is doing the work, with constituents not realizing what's being implied. SPY is the cleanest realization name; QQQ and IWM are the cleanest premium-sellers.

Bottom line: rotate short-vol exposure away from SPY toward IWM and QQQ where the carry is actually compensated. Index hedges underprotect against idiosyncratic moves regardless.

What it means for your trading

SPY VRP at 0.4% is functionally breakeven against HV20 at 12.16; QQQ at 3.08% and IWM at 3.19% carry the cleanest premium and are where short-vol size belongs.

Skew Convexity

Skew is ordered, not panicked. The quarter-delta put prints 13.4% against an ATM of 11.91% for a vol-point spread of 3.13% - textbook downside hedging, not a tail grab. The call wing at 10.27% sits below ATM, telling you nobody is paying up for upside convexity; there is no chase priced in.

Smile ratio at 1.31% is moderate, well shy of stress regimes, and the SKEW index at 141.74 corroborates orderly hedging rather than a bimodal bid. With VVIX at 95.58 and the term structure in Contango, convexity is not where the edge lives today.

Trade: downside is cheap relative to recent regimes but spreads dominate naked length - put debit spreads finance better than outright puts, and the flat call wing makes call ratio spreads attractive into strength toward 725.00. Skew this ordered rewards structure over outright premium.

What it means for your trading

Quarter-delta skew at 3.13% with smile ratio 1.31% reflects ordered hedging, not panic - confirmed by SKEW at 141.74. Put debit spreads and call ratios beat naked premium in this convexity regime.

Vol-of-Vol Structure

VVIX at 95.58 sits firmly below jump-risk thresholds, and the VVIX/VIX ratio at 5.48 prints squarely in normal territory - no bimodal panic priced into the wings, no crush priced into the body. The vol-of-vol surface is not flagging a binary outcome; it is pricing an orderly tape with VIX at 17.43 mean-reverting around its elevated-but-watchful band.

Sizing guidance reads Standard Size - full conviction on the iron condor and short-front-vol carry trades, no need to half-size for a jump scare that the surface refuses to price. When VVIX confirms the VIX print rather than leading it, the regime is Normal and the trade is to lean into the carry, not hedge the hedge.

What it means for your trading

Vol-of-vol at Normal with the ratio at 5.48 clears the path for Standard Size on conviction structures - no tail-bid premium to fade, no hidden jump risk to underwrite.

Dispersion Spread

Index ATM IV at 12.56% sits well below QQQ at 18.62% and IWM at 20.82% - a single-name premium spread wide enough to tell you correlation is moderate, not crushed. Index hedges are underprotecting against idiosyncratic dispersion: SPY is realizing what's implied while the smaller-cap and tech complexes carry the real vol bid.

IWM at 20.82% prints the richest of the complex, with QQQ at 18.62% a clear second - both materially above SPY. That asymmetry is the dispersion trade: short the index, keep single-name long-vol exposure live into earnings windows where idiosyncratic moves don't get netted away by the basket.

Preferred expression: lean SPY/SPX short premium where the carry is paid by structure, not by realized; resist the urge to short single-name vol into print risk. Cross-asset regime is Aligned, so the dispersion edge is name-level, not regime-level.

What it means for your trading

Index ATM IV at 12.56% versus IWM at 20.82% and QQQ at 18.62% prints a moderate-correlation tape - short index vol, keep single-name long-vol on earnings names where dispersion pays.

Liquidity & Microstructure

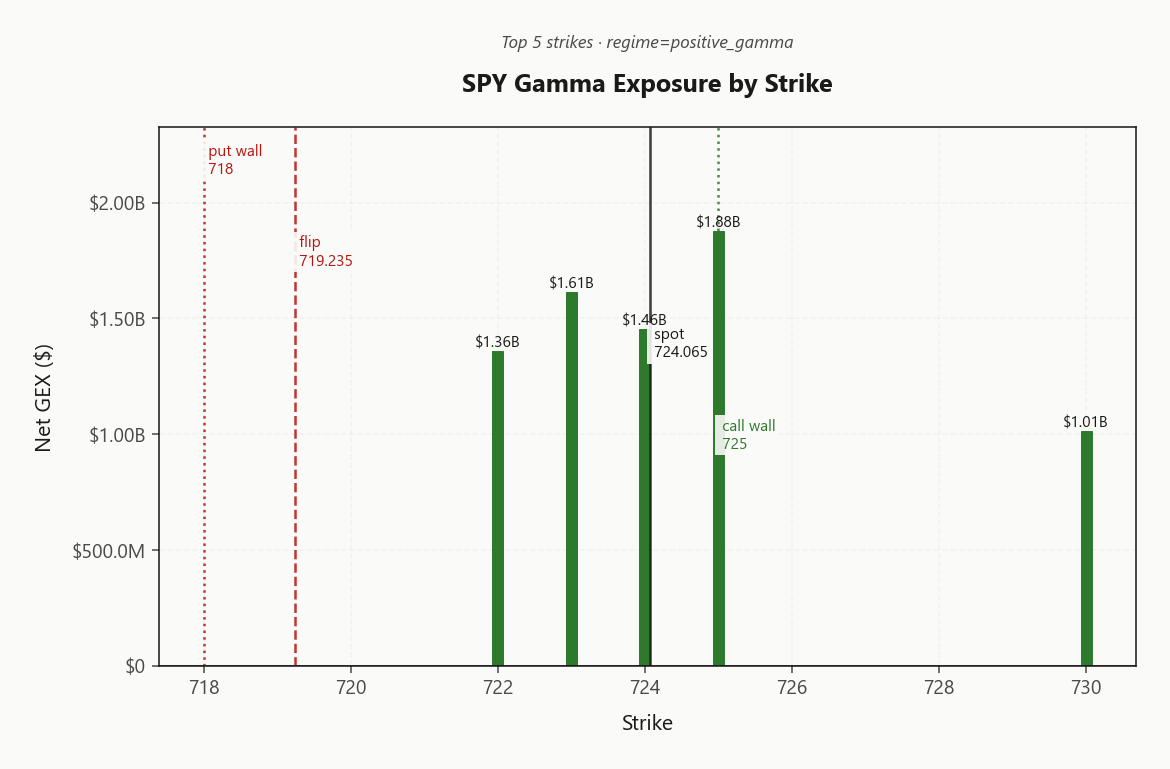

OI clusters tightly between the 718.00 put wall and the 725.00 call wall, with spot pinned just under the upper barrier and the 725.00 strike carrying $1.88B of net gamma - the dominant magnet on the board. The 700 level anchors the longer-dated max-pain, framing the structural floor of the book.

Gamma flip at 719.24 is the line that matters: above it, dealer hedging buys the dip and dampens every routine pullback; break it and the cushion inverts into a slide as hedges flip from supportive to procyclical. Distance to the call wall sits at 0.1291320531 of spot - close enough that pin dynamics dominate intraday tape.

With dealers deep in Positive Gamma and spot kissing the wall, expect chop, not trend: range-bound action between the walls, fade strength into 725.00, only flip defensive on a clean break of 719.24.

What it means for your trading

Spot pinned beneath the 725.00 magnet with a deep cushion down to the 719.24 flip - fade extremes, defend only on a flip break.

Trading readDeep positive-gamma stack with the 725.00 call wall as the dominant magnet - dealers dampen all the way down to the 719.24 flip, fade strength into the wall, only switch tactics on a flip break.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$248.78B - materially negative and the hidden accelerant under this tape. A vol bid mechanically forces dealers to sell delta, meaning any VIX impulse from 17.40 drags the gamma cushion down with it. The positive-gamma stack flatters the surface only while vol stays anchored.

Charm sits at -$1.65B - mildly negative, a manageable late-tape bleed rather than a forced-pin event. With spot at 724.07 kissing the call wall at 725 and bias reading Neutral, dealer flow is balanced on the knife's edge - the wall is the magnet on the upside, the gamma flip at 719.24 the trapdoor below.

Dampened tape today, but negative VEX of -$248.78B means the cushion thins fast on any VIX impulse - the call wall at 725 is the pivot where dealer flow flips.

Cross-Asset Confirmation

Cross-asset tape reads Aligned with zero fragility flag. MOVE at 77.86 sits unchanged - rates vol is asleep, and credit is offering no confirmation to the geopolitical headline tape. Fear & Greed prints Greed at 67, supportive without tipping into contrarian extreme.

SPY at 724.07, QQQ at 682.01, and IWM at 282.81 all close in Positive Gamma territory - full index-complex alignment, with VIX the lone short-gamma seat as expected in a risk-on regime. No divergence to lead a stress narrative off; if fragility surfaces, watch IWM where the gamma stack is thinnest.

Distinction matters: UAE/Iran headlines are noise, not signal. Credit calm and rates-vol flat say markets price the geopolitical tape as mean-reverting - this is risk-on alignment, not a stress regime. Carry the short-vol book without flinching on headline prints.

What it means for your trading

Cross-asset is Aligned with MOVE at 77.86 and F&G at 67 - no credit/rates confirmation of geopolitical noise, structurally risk-on. Stay with the short-vol carry; reassess only if MOVE bids or IWM breaks regime first.

Scenario EV

The scenario engine ranks Iron Condor as the highest-conviction structure at 43, with the put spread alternative trailing at 31. The logic stacks: steep contango from 14.66 through 22.95 pays the carry, positive gamma anchors the realized path between the 718.00 floor and 725.00 magnet, and VVIX at 95.58 clears Standard Size.

Sweet spot is 30-45 DTE - far enough out to harvest the contango term decay, close enough that gamma walls still bracket the path. VRP assessment prints Unknown at the index level, so the structure earns from term-curve roll, not flat-vol shorting.

Condor over strangle is the deliberate call: dealer-long-gamma walls cap the realized excursion, removing the tail-risk premium a strangle would demand. Defensive trigger remains a clean break of 719.24 - until then, fade strength into 725.

What it means for your trading

Iron condor at 43 in the 30-45 window is the cleanest expression of contango carry plus positive-gamma containment. Flip to defensive only on a break of 719.24.

Actionable Summary

Tape closes Positive Gamma with SPY pinned beneath the 725.00 call wall and the gamma flip well below at 719.24 - a deep dealer cushion, not a fragile one. Cross-asset regime reads Aligned across SPY/QQQ/IWM, VIX sits at 17.40 with the curve in Contango, and VVIX/VIX at 5.48 rules out jump-risk pricing. Regime label: Elevated / Watchful with a half-life of 15 sessions - sticky, fade extremes.

Trade:Iron Condor in 30-45 DTE scores best at 43 - contango pays the carry, positive gamma caps the realized path, sizing stays Standard Size. Watch the charm pivot at 725 as the call-wall magnet; fade strength into it. Avoid naked SPY vol - index VRP at 0.4% is too thin; rotate short-premium exposure into IWM at 3.19% and QQQ at 3.08%.

Defensive trigger: a clean break of 719.24 flips the cushion into a slide - until then, structure is condor, bias is mean-reversion.

Iran ceasefire status with active fire exchanges keeps a tail bid on energy and skew, but cross-asset shows no panic transmission - geopolitical mean-reversion regime.

German export flatline tied to Mideast uncertainty is the macro signal worth watching - if European credit cracks, it's the first cross-asset confirmation lever.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.40 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 719.24 against a spot of 724.07. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.56% with a volatility risk premium of 0.4%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.43. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime