Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

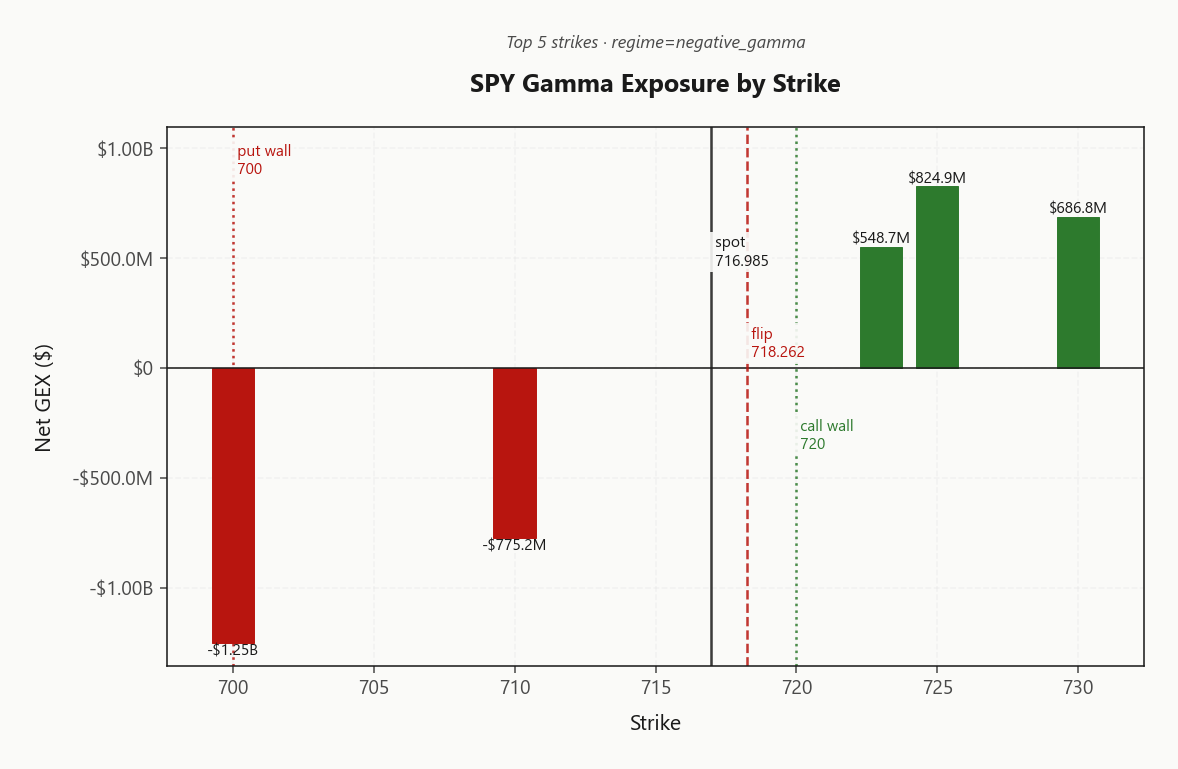

SPY is at 716.99, sitting just below the gamma flip at 718.26 with net GEX at -$3.71B - dealers are short gamma and the tape will amplify, not dampen, intraday moves. Call wall at 720.00 is the immediate resistance, put wall at 700.00 is the air-pocket; max pain pinned at 700.00 marks the magnet if vol cools. 0DTE is carrying 58.7% of total gamma - nearly all of today's chop is short-dated. Dealer vanna at -$194.76B means a VIX uptick (already +11.3%% to 18.91) forces more delta selling - vanna is a hostile accelerant here. Term structure is in steep contango (Contango, slope 3.9%%) with VVIX at 100.20 - vol-sellers' carry is intact but the front is bid on Hormuz tape risk. VRP runs 2.61% vol points rich to 20d realized at 12.32, so premium is paid. Bottom line: fade strength into 720.00, respect downside thrust below 718.26, and harvest the rich VRP via 30-45 DTE iron condors per Iron Condor - half-size around event tape.

SPY negative gamma below flip at 718.26; QQQ positive gamma diverges, Iran shock bid VIX to 18.70

SPY at 716.99 sits just below the gamma flip at 718.26, flipping dealers short and amplifying the Iran-driven tape. QQQ at 671.32 remains in positive-gamma territory above its flip at 599.78, marking the cleanest cross-asset divergence (Qqq Heavier). Steep VIX contango with VVIX at 100.20 keeps vol sellers paid, but charm pivot at 718.2616511008 is destabilizing into the close.

Regime Assessment

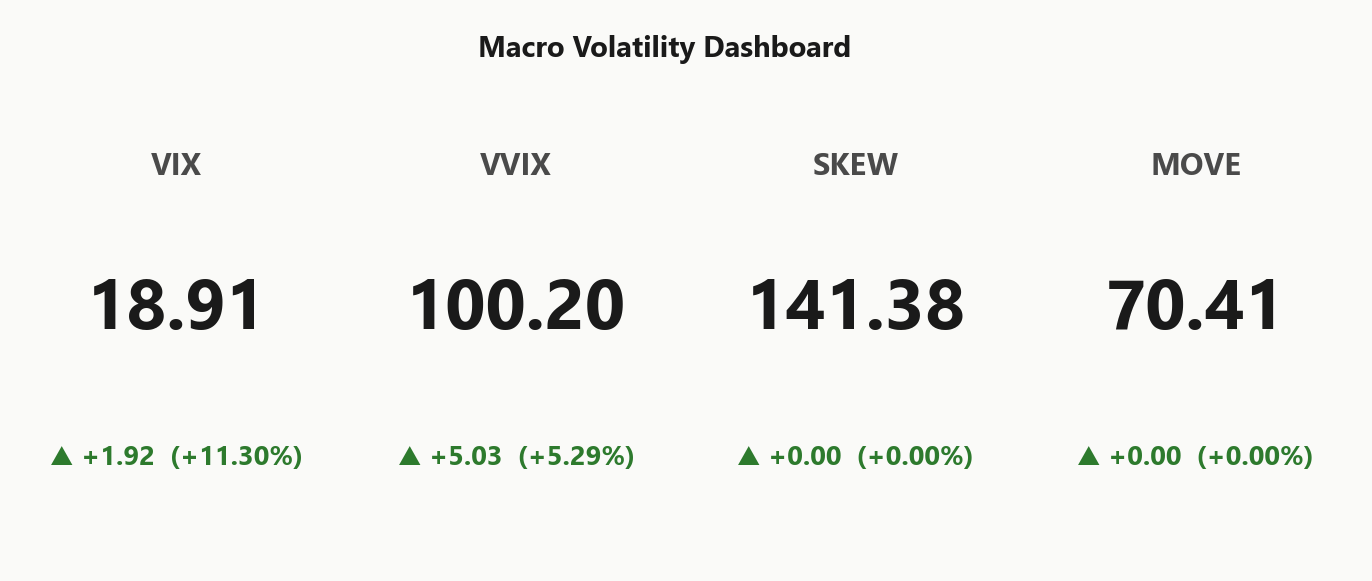

Regime reads Elevated / Watchful with the tape parked at VIX 18.91 - not panic, not complacency, but the in-between zone where dealer hostility and rich premium coexist. The transition matrix prices escalation to panic over five sessions at 0.05 while a cool to low-vol over ten sessions runs at 0.45; the asymmetry is a clean tell that mean-reversion is the base case, escalation the tail.

Half-life of 15 sessions is the operative number: sticky enough that today's setup is tradeable as a regime, not a passing tape, but short enough that overstaying through the Hormuz event window is its own risk. Pair this with the destabilizing charm pivot at 718.2616511008 and the call is straightforward - deploy Iron Condor at 30-45 DTE, harvest the asymmetry, and respect the regime's expiration date.

What it means for your trading

Elevated/watchful regime with a 0.45 cool-down probability dwarfing the 0.05 panic tail - play for mean-reversion within the 15-session half-life, exit before it stales.

Trading readVIX up 11.3%%, VVIX up 5.29%%, MOVE flat at 70.41 - vol-of-vol confirms the equity stress but bonds aren't biting. Equity-isolated risk-off, not systemic.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

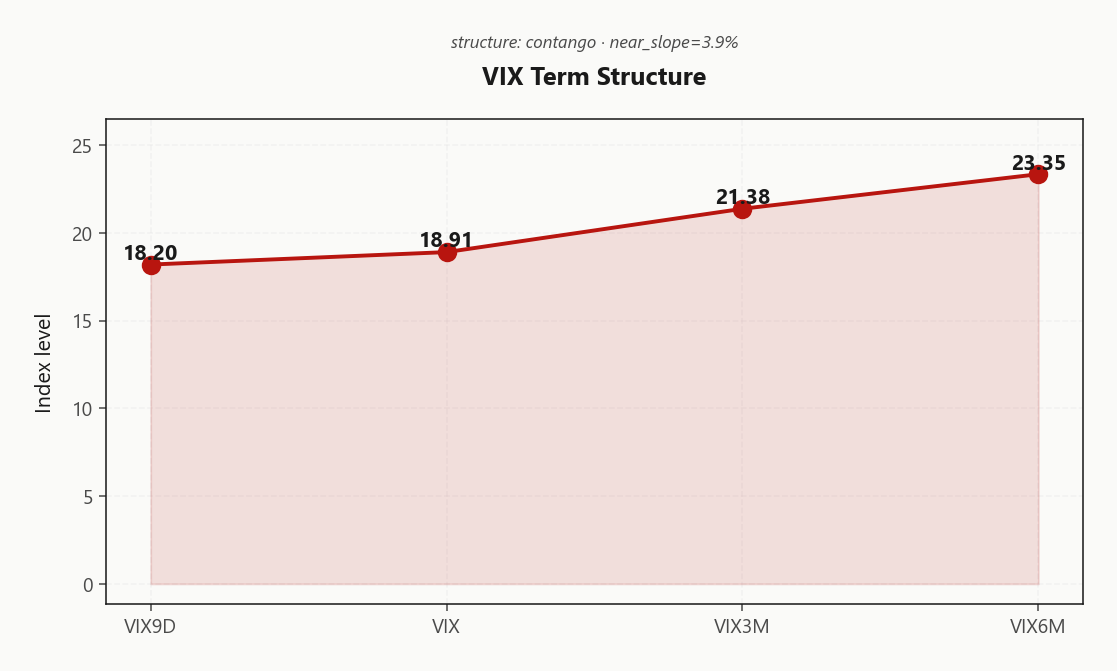

The curve sits in Contango with VIX9D at 18.20 beneath VIX at 18.91, sloping out to VIX3M at 21.38 and VIX6M at 23.35. That is Steep contango - vol sellers favored - vol sellers are paid the carry, but the front-end bid into the Hormuz tape concentrates event premium in the 0 - 30 DTE bucket where the curve is cheapest to roll.

Forward 30→60 vol prices at 22.5136081071 versus forward 60→90 at 25.1662591578 - the back is paying fair carry while the belly is the kink. Sell the 30 - 45 DTE sweet spot: long enough to dodge the geopolitical front-end overpay, short enough that theta still works against the Steep Contango term shape.

Trade construction: calendar the front against 30 - 45 DTE shorts, or harvest the belly outright. Avoid naked front-week premium - that is where the Hormuz risk lives.

Trading readContango at 3.9%% slope says the market still expects mean-reversion in vol - vol-sellers' carry trade is on, but front-end bid signals event premium needs respect.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 14.93% is printing well clear of HV20 at 12.32, leaving VRP at 2.61% vol points solidly positive - options are rich to the tape dealers are actually hedging. HV60 at 15.22 sitting above HV20 says realized has been decelerating, not accelerating into the Hormuz bid; the implied premium is reaching for a tail the cash hasn't delivered.

Premium harvest remains the structurally paid trade here, and the iron condor at 30-45 DTE is the cleanest expression - the realized backdrop is doing the work for short-vol carry. The watch is 5-day realized: a sustained Hormuz spillover that drags HV20 toward ATM IV at 14.93% compresses the VRP edge fast, and that's the trigger to pull size, not the headline itself.

What it means for your trading

VRP at 2.61% vol points with HV60 above HV20 confirms premium sellers are paid against a decelerating tape; defend the thesis only as long as 5-day realized stays anchored below ATM IV at 14.93%.

Skew Convexity

Quarter-delta puts mark 20.16% against an ATM print of 17.66% and a call wing trading 15.7% - a put-over-call skew of 4.46% vol points and a smile ratio of 1.28%. Steep, but ordered - the curve is being repriced for the Iran tail, not capitulating into it.

The asymmetry is the signal: downside is bid, upside is dead. A flat call wing tells you no one is paying for an upside chase here; the entire convexity premium is concentrated in the left tail and reads geopolitical, not systemic - consistent with MOVE flat at 70.41 and a Qqq Heavier cross-asset tape.

Tactically, that geometry punishes naked downside: outright puts overpay for the steepness already in the curve. Prefer put spreads - finance the long leg by selling the still-rich body - and let skew compression work for you on any Hormuz de-escalation. Carry the convexity, don't buy it outright.

What it means for your trading

Skew at 4.46% with smile ratio 1.28% is steep but ordered - geopolitical tail bid, no panic. Express downside via put spreads, not naked puts; outright protection is overpriced relative to the suppressed call wing.

Vol-of-Vol Structure

VVIX prints 100.20 against VIX at 18.91, pinning the ratio at 5.30 - squarely Normal. The tape is bidding jump risk into the Hormuz headline but refusing to price a bimodal blow-up; the convexity bid is contained, not capitulatory.

That keeps sizing at Standard Size for premium-harvest structures. With contango still paying carry and VVIX nowhere near stress thresholds, the vol-of-vol surface is corroborating the iron-condor thesis rather than threatening it - gamma-of-gamma isn't fighting you here.

The watch is asymmetric into the weekend: a VVIX print through the elevated threshold on Hormuz escalation is the cue to halve clips and tighten wings. Until then, the vol-of-vol read is permission, not warning - but the permission expires at the first sustained convexity bid through the front.

What it means for your trading

VVIX/VIX at 5.30 reads Normal - convexity is bid but ordered, keeping sizing at Standard Size. Trim if VVIX rips through the elevated band on weekend Hormuz escalation.

Dispersion Spread

The cross-sectional vol map reads Moderate: SPY ATM at 14.93% sits well below QQQ at 19.89%, with IWM stretched to 22.8%. Small-caps are carrying the heaviest single-name vol load - the IWM premium isn't index beta, it's idiosyncratic fragility bleeding through the basket as correlation refuses to pin to one.

QQQ's elevated print versus SPY is a single-name beta tax - the megacap concentration that keeps QQQ above its flip is the same concentration making its index vol expensive. With Qqq Heavier divergence and SPY's Negative Gamma versus QQQ's Positive Gamma, an index hedge is only a partial cover for a single-name shock - the dispersion delta won't be neutralized by an SPX put.

Trade the structure: sell index vol where the basket discount is doing the work, and avoid single-name shorts where the idiosyncratic bid is being paid for a reason. SPY/SPX premium harvest at 30-45 DTE is the cleaner expression than picking off a rich IWM or single-name wing into geopolitical tape.

What it means for your trading

Dispersion is Moderate with IWM at 22.8% leading SPY at 14.93% - sell index vol via Iron Condor, not single-name premium, because index hedges only partially cover idiosyncratic shock in this regime.

Liquidity & Microstructure

Strike concentration anchors the book at 700, with the call wall at 720.00 capping rallies and the put wall at 700.00 marking the next air-pocket. Max pain at 700.00 sits inside the same cluster - a magnet zone that will pin the tape if vol cools, and rupture cleanly if it doesn't.

The regime line is the gamma flip at 718.26. With spot at 716.99 trading just below it, dealers are Negative Gamma - selling into weakness, fading strength, the opposite of the cushioned tape from the open. The top strike at 700.00 carries net GEX of -$1.25B, dense enough to dominate hedging flow into the bell.

Trade the levels: fade strength into 720.00, respect downside thrust below 718.26, and treat 700.00 as the line where short-gamma amplification gets violent.

What it means for your trading

Concentration at 700 pins the magnet; the gamma flip at 718.26 is the regime switch - sustained reclaim flips dealer flow back to supportive, sustained loss opens the path to the put wall at 700.00.

Trading readSPY's gamma profile shows dealers short below 718.26 and long above the call wall at 720.00 - moves below the flip get amplified, rallies into the wall get faded. The put wall at 700.00 is the next air-pocket if 718.26 fails.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order greeks are stacked against the tape. Net VEX prints -$194.76B - deeply negative - meaning every uptick in implied vol forces dealers to sell more delta, not absorb it. With VIX bid to 18.91 on the Hormuz tape, vanna is acting as an accelerant, not a cushion.

Charm compounds the problem. Net CHEX at -$3M means time decay is bleeding dealer long-delta into the close, manufacturing a structural sell-pressure drift independent of news flow. The charm pivot sits at 718.2616511008 - that is the bias flip line - and current read is Destabilizing on a Red signal.

This is the day's most hostile dealer-flow setup: short gamma, hostile vanna, decay-driven charm, all pulling the same direction. Buy-the-dip mechanics are off until spot reclaims 718.2616511008; below it, expect amplification on every vol uptick into 700.00.

What it means for your trading

Vanna and charm are both pressing dealers to sell - vol-up forces more delta supply via VEX at -$194.76B, and CHEX at -$3M bleeds long-delta into the bell. Until spot reclaims the charm pivot at 718.2616511008, the Destabilizing bias dominates.

Cross-Asset Confirmation

Cross-asset tape reads isolated geopolitical shock, not credit contagion. MOVE sits at 70.41 - rates vol is dead flat through the Hormuz tape, and that is the single most important tell on the page: if this were systemic, the bond market would already be screaming. It isn't.

Sentiment confirms: Fear & Greed at 64 still reads Greed, meaning positioning is complacent into a vol bid - the gap between price action and conviction is the contrarian fuel. Within equities the divergence is sharp: QQQ at 671.32 holds positive gamma above its flip while SPY and IWM at 277.02 have rolled negative - divergence reads Qqq Heavier, the megacap complex is doing the load-bearing work.

Historical playbook for flat-MOVE / bid-VIX / greed-sentiment shocks is mean-revert, not compound. Sell into the front-end vol bid, respect the QQQ bid as the cross-asset anchor, and treat any MOVE breakout as the kill-switch on the short-vol structure.

What it means for your trading

Flat MOVE plus complacent F&G at 64 confirms an equity-isolated geopolitical event, not credit-driven risk-off - historically these mean-revert. Watch the QQQ-heavier divergence (Qqq Heavier) as the structural floor; a crack there flips the framing.

Scenario EV

Structure selection lands on Iron Condor with a score of 46, beating the put spread alternative at 38. The logic stacks: VRP at 2.61% vol points is positive, term structure runs Contango paying carry, and vol-of-vol reads Normal at a 5.30 VVIX/VIX ratio. When directional edge is absent, symmetric premium harvest dominates the EV table.

Optimal tenor is 30-45 - far enough to dodge the 0DTE gamma chop carrying 58.7% of total book, close enough to monetize the front-end event premium without warehousing back-month vega. Wings frame around the call wall at 720.00 and put wall at 700.00, with the gamma flip at 718.26 as the regime tripwire on the downside short.

Sizing stays Standard Size - VVIX hasn't cleared the panic threshold and MOVE at 70.41 confirms no rates contagion. Scale back only on a sustained VVIX break or a charm-pivot flip through 718.2616511008.

What it means for your trading

Deploy Iron Condor at 30-45 DTE in Standard Size - the EV table favors symmetric premium harvest over directional bets while VRP, contango, and vol-of-vol all align in the seller's favor.

Actionable Summary

Regime reads Elevated / Watchful with SPY pinned just under the gamma flip and dealers Negative Gamma - vanna at -$194.76B and charm at -$3M stack as a Destabilizing accelerant into the bell. Deploy Iron Condor at 30-45 DTE: VRP runs 2.61% rich to HV20 at 12.32, contango pays the carry, and vol-of-vol prints Normal - symmetric premium harvest beats directional bets when no edge exists.

Watch 718.2616511008: a sustained reclaim flips dealer flow back supportive and re-arms the long-gamma cushion. Until then, fade strength into the 720.00 call wall, respect the air-pocket toward 700.00, and hedge via SPY put spreads - outright tail puts are punitive at 4.46% skew. Avoid chasing the wall, naked downside, and single-name shorts while dispersion runs Moderate. Size Standard Size until VVIX at 100.20 breaks higher.

What it means for your trading

Sell rich premium via Iron Condor at 30-45 DTE; treat 718.2616511008 as the regime-flip line and cap directional exposure into the 720.00 call wall.

Fire and explosion on a tanker in the Strait of Hormuz is the proximate cause of today's VIX bid - every basis-point of risk premium in the front-end vol curve traces back to this headline.

Bessent leaning on China to mediate Iran ahead of a Trump-Xi summit signals diplomatic off-ramp probability - a meaningful tail risk against any short-vol position is whether this de-escalates by Friday.

Reuters confirming the index reaction to US-Iran tensions validates the geopolitical-shock framing rather than a domestic catalyst - informs the mean-reversion thesis.

The 'misplaced euphoria' and oil-shock recession warning is the contrarian sentiment marker that matters for positioning - Fear & Greed still in greed territory underscores the gap.

Hormuz shipping at a standstill is the supply-chain transmission mechanism - if it persists into the weekend, the front-end VIX bid extends and short-vol structures need defensive sizing.

Reports of a US warship being struck moved the dollar and European bonds - this is the cross-asset confirmation that the move is risk-off geopolitical, not technical.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.70 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 718.26 against a spot of 716.99. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.93% with a volatility risk premium of 2.61%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.91. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime