Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

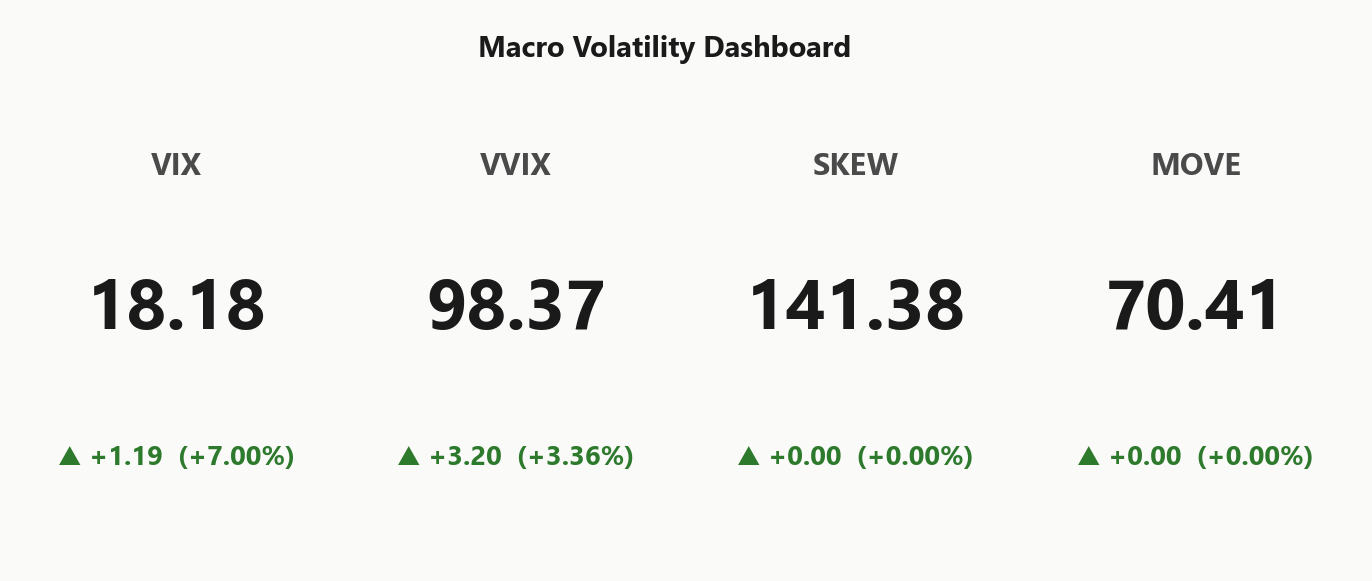

SPY closes at 717.53, sitting fractionally below the 719.36 gamma flip in a Negative Gamma regime with net GEX at -$2.31B. Call wall and put wall converge at 718.00 / 718.00, with the heaviest OI cluster down at 700 - meaning today's tape will trend rather than mean-revert until spot reclaims the flip. Dealer vanna at -$200.54B is hostile (vol-up triggers more selling), and charm at -$372.8M adds late-day downside pressure per Time decay pushing dealers to sell - pressure into close. VIX at 18.18 with Contango term structure (9d 16.43 → 3m 20.94) keeps vol-sellers' carry alive, and VRP at 2.26% is constructive. VVIX at 98.37 is normal but climbing - sizing stays Standard Size, not aggressive. Bottom line: book Iron Condor structures in the 30-45 window above the flip; do not press naked short gamma until SPY reclaims 719.36.

Negative gamma index complex with VIX contango - Elevated / Watchful regime, mean-reversion fragile near 719.36

SPY at 717.53 sits just under the 719.36 flip with dealers short gamma across the index complex, meaning intraday moves get amplified rather than dampened. VIX term structure remains in Contango and VRP is positive at 2.26%, so vol sellers retain carry - but VVIX at 98.37 and a 4.25% put-skew tilt say the tape is paying up for downside convexity. Best edge is patient premium-selling in the 30-45 bucket, not naked short gamma into the close.

Regime Assessment

Modal regime reads Elevated / Watchful with VIX anchored at 18.18 - a half-life of 15 sessions says this state is sticky, not transitional. Base case for the next two weeks is more of the same: contango intact, dealers short gamma below the flip, premium-sellers paid but not aggressively.

Transition probabilities tell the real story. Jump-to-panic over five sessions sits at 0.05 - low enough that tail hedges are cheap insurance, not the core trade. Mean-reversion to a low-vol regime over ten sessions runs 0.45, materially skewing the distribution toward normalization rather than escalation.

Translation: patience pays. Hold structural carry in the 30-45 bucket, keep convex tail protection on as a side-pocket given the 4.25% skew tilt, and resist the urge to chase a panic bid that the regime model says is unlikely to print.

What it means for your trading

Regime is Elevated / Watchful and sticky over a 15-session half-life, but transition odds - panic 0.05, normalize 0.45 - favor eventual mean-reversion, making patience the dominant edge over chasing tails.

Trading readVIX bid, MOVE flat, SKEW 141.38 elevated, VVIX climbing - equity vol diverging from rates vol means today is an equity-positioning event, not a macro break. Watch MOVE; if it joins the move, regime escalates fast.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

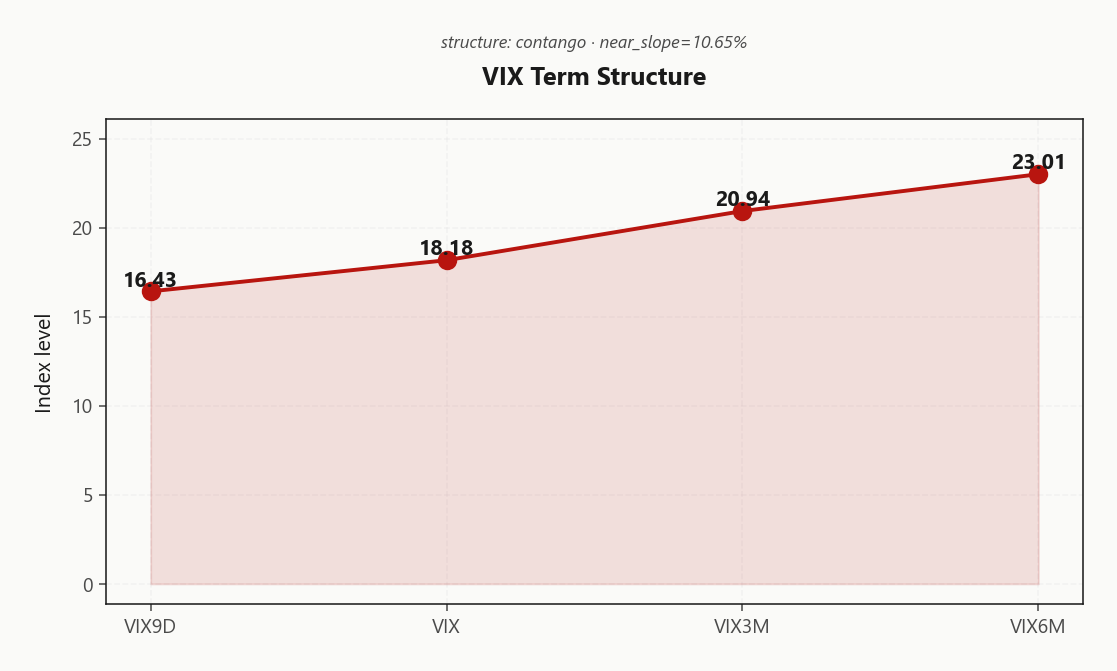

The VIX curve holds a clean Contango stack from VIX9D 16.43 through spot VIX 18.18 out to VIX3M 20.94 and VIX6M 23.01 - Steep contango - vol sellers favored keeps systematic vol-carry alive in the belly. The front-end gap between VIX9D and spot VIX confirms the contango is structural rather than a one-day artifact, but today's lift in the front narrowed the cushion that pays the roll.

Forward 30-to-60 implied prints around 22.1916470772, with 60-to-90 extending to 24.9085647921 - mid-curve pricing is stable and consistent with a Steep Contango read. Best structural edge is carry in the 30-45 bucket where roll-down is densest; avoid 0-7 DTE where dealer short gamma and charm bleed dominate the signal.

What it means for your trading

Curve geometry endorses Steep contango - vol sellers favored as the carry trade of record, but with the front lifted to 18.18, position the harvest in 30-45 rather than the front week.

Trading readVIX9D 16.43 → VIX 18.18 → VIX3M 20.94 in Contango - vol-carry trade still pays in 30-90 DTE, market is not pricing imminent stress. A flatten or invert here is the first warning bell.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 14.45% sits comfortably above HV20 12.19, with VRP printing 2.26% - options remain rich to recent realized and the Moderate Premium read validates premium-selling as the structural carry trade. The IV-RV20 spread is constructive without being extreme, so this is harvest territory, not the fat-tail giveaway we saw earlier in the cycle.

Under the hood, RV5 at 9.38 has decelerated meaningfully versus RV20 12.19 - realized has cooled into the close, telling us shorts are being paid less than the two-month average even as IV holds firm. That decel is the tell: vol path is normalizing, not collapsing, and crush trades that worked off the panic highs are now lower-edge.

Translation for the book: keep selling premium, but size to a normalizing path rather than a one-way grind lower. Wing-selling beats body-loading here, and the Moderate Premium tag means cushion exists if realized re-accelerates - it just doesn't pay you to press.

What it means for your trading

VRP at 2.26% keeps the carry trade alive with IV 14.45% comfortably over RV20 12.19, but RV5 9.38 cooling into HV20 says shorts are paid less than the two-month average - harvest, don't press.

Skew Convexity

Quarter-delta skew prints 4.25% with a smile ratio of 1.33% - put wing at 17.03% trades a clean step over ATM 14.22%, while the call wing at 12.78% sits visibly under the body. Put-25d > ATM > Call-25d is the textbook risk-off bid: protection is being lifted in an ordered way, not a panic-priced one.

The asymmetry matters for structure. A smile ratio of 1.33% says the left tail is steeper than the right but not yet pricing a jump - meaning the call side is cheap funding, not a giveaway. Naked downside is the wrong expression here; verticals capture the same convexity without paying the full skew tax.

Trade it accordingly: short the call wing first to monetize the depressed 12.78% against ATM, and hedge the put wing with a vertical - owning the 17.03% strike outright forfeits carry the ordered skew is already paying you to spread.

What it means for your trading

Skew geometry at 4.25% with smile ratio 1.33% reads as ordered downside bid, not panic - favors short-call-wing financing and put-spread hedges over naked downside structures.

Vol-of-Vol Structure

VVIX at 98.37 against VIX 18.18 prints a ratio of 5.41 - squarely in the Normal band. No bimodal jump-risk premium is being demanded by the vol-of-vol surface, which means the tape is not pricing a regime break, just a wobble. Sizing guidance reads Standard Size; carry trades clear at full clip without the haircut a stressed VVIX would force.

That said, the direction matters more than the level here. VVIX is creeping higher on the day even as VIX has only marginally lifted - the classic leading tell that vol-buyers are paying up for convexity before spot vol confirms. Treat it as an early-warning gauge, not a stop signal: full size remains defensible, but the next leg of any VVIX uptick - particularly a divergent one with VIX flat - is the cue to trim gamma exposure and re-check the 718 pivot before adding.

What it means for your trading

VVIX/VIX in the Normal band greenlights Standard Size on premium-selling structures, but the intraday VVIX creep is a leading indicator - respect divergent upticks against a flat VIX as the first reason to cut size.

Dispersion Spread

Index vol screens cheap versus the satellites: SPY ATM IV at 14.45% sits well under QQQ 19.38% and IWM 23.99%, with cross-strike dispersion at 74.47 and cross-expiry at 2.46. Correlation has not collapsed - idiosyncratic risk is being paid in single-names while index hedges remain efficient carry.

IWM at 23.99% is the richest leg of the complex, consistent with persistent small-cap fragility and the Negative Gamma stance below its flip. QQQ at 19.38% running over SPY signals factor risk concentrated in mega-caps - exactly where AMZN, AAPL, and NVDA dealer GEX swings have been telegraphing repositioning.

Trade expression: harvest premium in SPY/SPX over single-names - index VRP is the cleaner canvas. For beta hedging, IWM puts deliver cheaper convex downside than SPY given the small-cap richness skew. Avoid paying up for QQQ vol when the dispersion is doing the work for you in the underlying mega-cap names.

What it means for your trading

Index-vs-satellite vol gap stays orderly: IWM richest, QQQ over SPY, dispersion Moderate - sell index premium, hedge beta through IWM puts, leave single-name vol alone.

Liquidity & Microstructure

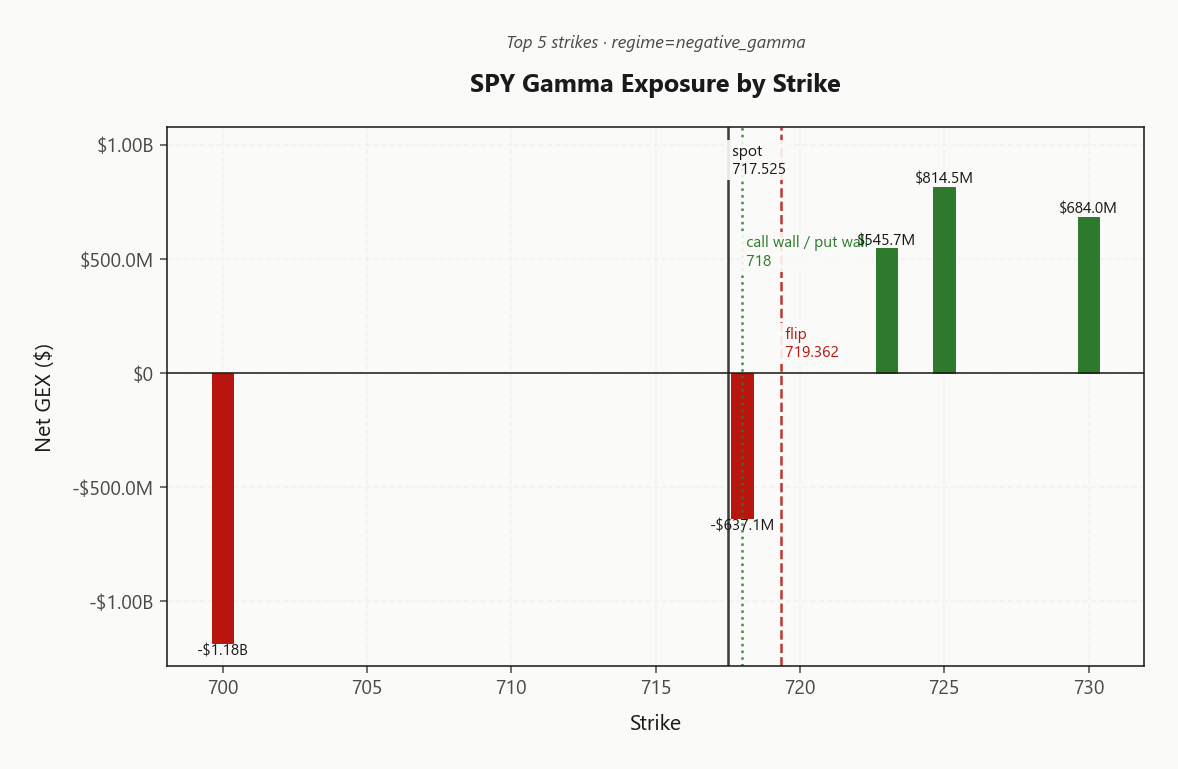

The book's center of gravity sits at 700, where the largest negative-GEX strike stacks -$1.18B of dealer-short-gamma weight directly beneath spot. With the gamma flip pinned at 719.36, that level is the single decision line for today's flow - reclaim it and dealer hedging dampens; lose it and the same flow amplifies every tick lower.

Above 719.36, dealer rebalancing supports rallies as gammas turn cooperative; below it, the 700.00 anchor - chart 513480 OI - exerts gravitational pull and gets respected on every test. The convergence of call wall and put wall at 718.00 / 718.00 sets up a clean pin magnet into tomorrow's expiry, with regime tagged Negative Gamma.

Trade the level, not the narrative: fade strength into 718.00, do not press shorts below 700.00, and reserve adds for a clean reclaim of 719.36.

What it means for your trading

Microstructure is binary around 719.36: above it dealer flow is dampening, below it amplifying, with 700 as the gravitational anchor and walls converging at 718.00 for an expiry pin.

Trading readNegative gamma cluster anchors at 700 below spot while positive gamma walls stack just overhead - translation: dealers amplify moves until SPY reclaims 719.36, then dampening flow takes over above.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$200.54B - deeply negative and structurally hostile. Any further lift in 18.18 mechanically forces dealers to sell more delta, a self-reinforcing vanna feedback loop that turns vol-up days into accelerating spot-down days. This is not a tape to fade with naked short premium while VIX is bid.

Charm reads -$372.8M, adding a steady late-session bleed: dealers shed long delta into expiry per Time decay pushing dealers to sell - pressure into close, compounding the vanna pressure as the clock runs. The two greeks are pulling the same direction, not offsetting - aligned dealer mechanics, not divergent.

Single decision level is the charm pivot at 718 with current bias Neutral. Reclaim flips the regime; rejection extends the trend. Trade above the pivot, hedge below, and do not press short gamma into the close while spot sits south of 719.36.

What it means for your trading

Vanna and charm both negative and aligned - vol-up and time-decay each pull dealers to sell, with the bias flip living at 718. Stay defensive on short-gamma exposure until that level is reclaimed.

Cross-Asset Confirmation

MOVE holds at 70.41 while VIX presses higher to 18.18 (+7%%) - the bid is equity-only, with no spillover into rates or credit. This is an isolated positioning wobble, not a macro shock; the absence of MOVE confirmation strips the regime of escalation fuel and keeps the convexity bid contained to index vol.

QQQ at 672.26 and IWM at 277.52 track SPY weakness in lockstep - cross-asset reading is Aligned, no divergent index lead to fade. Fear & Greed at 63 still prints Greed, leaving sentiment constructive while structure turns fragile - the classic late-cycle setup where positioning, not narrative, dictates the next leg.

Tone reads Unknown. Watch MOVE: any sympathetic lift here is the trigger that converts an equity-only wobble into a cross-asset risk-off. Until then, treat the complex as uniformly short-gamma fragile, but contained.

What it means for your trading

Equity vol is bid in isolation with the index complex Aligned and rates vol flat at 70.41 - fragile but not a macro break, with sentiment at Greed (63) still leaning contrarian-cautious.

Scenario EV

Scenario engine picks Iron Condor as the optimal structure with score 36 versus put-spread 29 - the edge stacks cleanly: positive VRP at 2.26%, VIX term in Contango, and an ordered put-skew bid at 4.25% that pays the call wing as funding leg.

DTE sweet spot is 30-45, where forward-vol carry from 22.1916470772 peaks and you sit clear of the 0-7 DTE jump zone. Avoid front-week naked short gamma - dealer net VEX at -$200.54B and CHEX at -$372.8M turn intraday whip into a tax, not an edge, while spot trades below the 719.36 flip.

Size Standard Size per the VVIX read at 98.37; full clip is acceptable but VVIX upticks against a flat VIX cut size first.

What it means for your trading

Book Iron Condor in the 30-45 window at Standard Size, harvesting VRP and contango carry while skipping the front-week gamma-and-charm whip below 719.36.

Actionable Summary

Bottom line: book Iron Condor structures in the 30-45 DTE bucket above the 718 charm pivot, run Standard Size sizing, and do not press naked short gamma into 0DTE while SPY trades below the 719.36 flip. Regime reads Elevated / Watchful with VIX in Contango and VRP at 2.26% - carry intact, but VVIX at 98.37 is climbing and warrants respect.

GO:Iron Condor in the 30-45 window, full clip. WATCH:718 for the bias flip and any VVIX upticks as the cue to cut size. AVOID: 0-3 DTE naked short gamma and single-name vol-selling versus the index. HEDGE: put-wing convexity remains cheap given 141.38 SKEW and the ordered tail bid in 4.25% 25d. FADE: only fade strength into the 718.00 call wall; no buy-the-dip until spot reclaims 719.36.

What it means for your trading

Negative-gamma complex with Contango and constructive VRP keeps Iron Condor the cleanest expression in 30-45, but the 718 pivot and 719.36 flip are the two lines that govern sizing and stance.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.28 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 719.36 against a spot of 717.53. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.45% with a volatility risk premium of 2.26%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.18. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime