Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

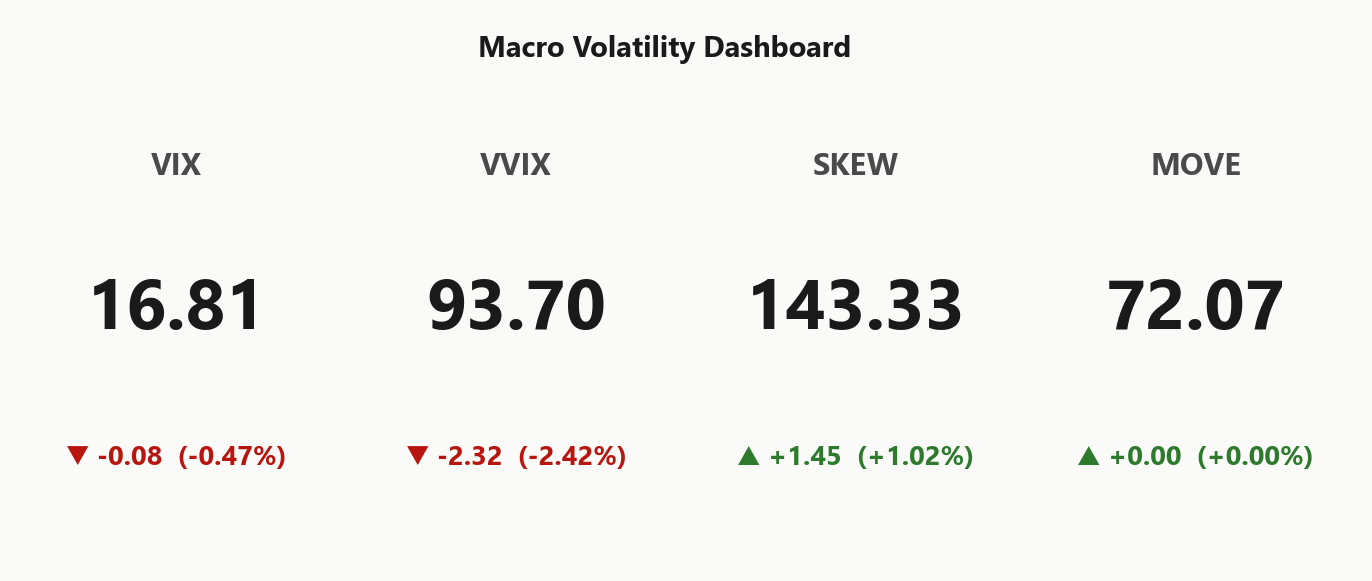

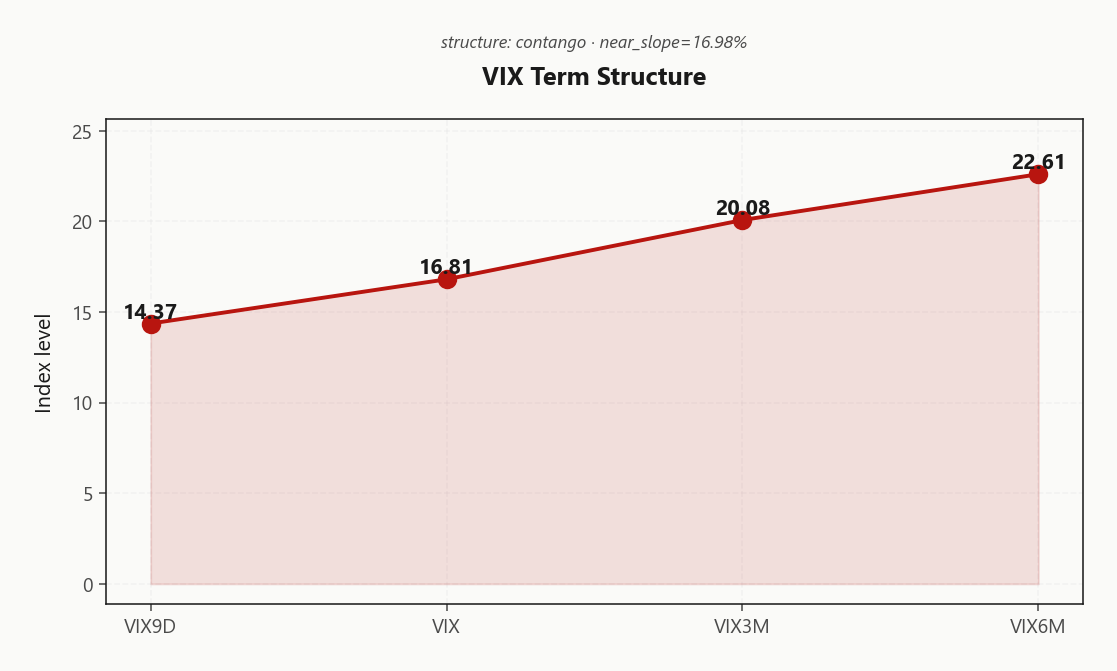

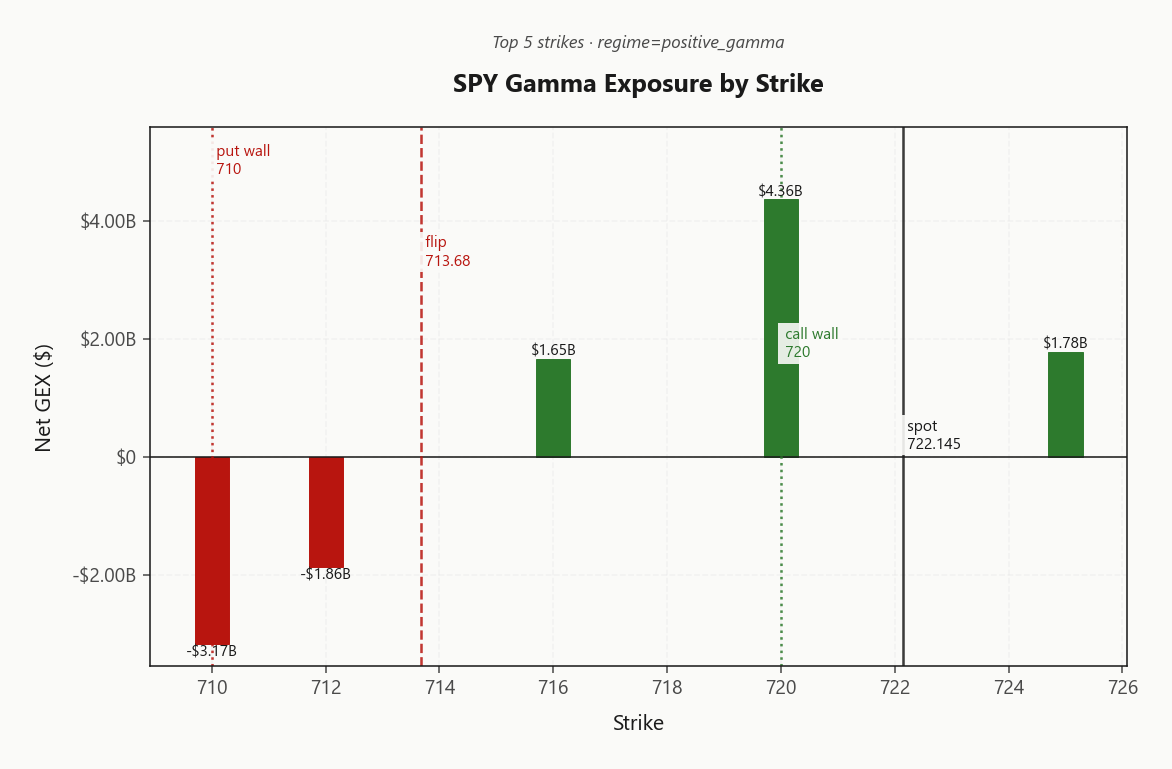

SPY at 722.15 trades in Positive Gamma with net GEX at $7.64B - dealers long gamma, intraday range compression is the base case. Call wall at 720.00 caps upside, put wall at 710.00 backstops, gamma flip at 713.68 sits well below spot - deep cushion intact. Dealer vanna at -$265.06B is net short - any vol pop forces them to sell delta and amplifies a downside flush, so the regime is fragile to a VIX spike even though VIX itself printed 16.81. Term structure in steep contango (14.37 vs 20.08, slope 16.98%%) and SPY VRP at 0.71% keep premium sellers paid; VVIX at 93.70 is normal but Iran-tape risk argues for cheap tails. Bottom line: sell premium in the 30-45 bucket via Iron Condor structures, fade pushes into 720.00, watch 713.68 as the regime-break trigger.

Positive gamma cushion across index complex with VIX in steep contango - vol sellers favored

SPY at 722.15 sits above the gamma flip at 713.68 with dealers long gamma - moves get dampened, mean-reversion wins. VIX term structure shows steep contango (14.37 → 22.61) backing a vol-selling regime, but VVIX at 93.70 and persistent Iran headlines argue for keeping cheap left-tail convexity on. The single break level is the call wall at 720.00 - pinned underneath into 0DTE with 38.1%% of gamma stacked there.

Regime Assessment

Regime tags Elevated / Watchful with the current state reading Elevated at VIX 16.81 - the dampening cushion is intact across the index complex, but the signal color Yellow is the tell: this is watchful, not green. SPY, QQQ and IWM all print Positive Gamma with spot above flip, while VIX itself sits in Elevated / Watchful territory - the front of the curve is the fragile leg, not the equity book.

Half-life of 15 sessions says this regime is sticky - the base case is more of the same, premium-seller math keeps working, dealer flow keeps fading the chasers. Transition probability to panic over five sessions prints 0.05; drift to a low-vol state over ten sessions prints 0.45 - the distribution skews toward calm but with a live left tail.

Path-dependent because of the Iran tape: persistence priors are clean, but headline risk doesn't respect half-lives. Run the regime as the base case, keep cheap convexity on for the jump.

What it means for your trading

Regime is Elevated / Watchful at VIX 16.81 with a 15-session half-life - sticky enough to lean on, fragile enough to hedge. Trade the persistence, respect the path.

Trading readVIX, VVIX, SKEW, MOVE all confirming the same story - calm now, tails priced. No divergence flag, but SKEW elevation reminds you the left tail is not free.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve prints Contango from front to back - VIX9D at 14.37 sits below spot VIX 16.81 with the three-month at 20.08 and the six-month tagging 22.61. Forward vol regime reads Steep Contango - Steep contango - vol sellers favored. Near-term slope of 16.98%% is wide enough to lean short the front without flirting with backwardation risk.

The carry hurdle lives in the belly: forward 30-to-60 prices 21.5295506223, with forward 60-to-90 stretching to 24.8840872848 - that's the structurally higher far vol the back end pays you to own. Best edge sits in the 30-45 bucket where front vol still trades a discount to the three-month 20.08 print.

Calendar spreads are the cleanest expression - sell the depressed front, own the bid back end, harvest the slope. Vol-seller regime confirmed; no curve signal arguing against it.

What it means for your trading

Steep contango from 14.37 through 22.61 with forward 30-to-60 at 21.5295506223 backs short-front, long-back calendars in the 30-45 bucket - the carry trade is live and unconflicted.

Trading readSteep contango with front below long-dated says the market expects calm now and elevated vol later - classic carry environment. Slope wide enough to lean short the front without a near-term inversion fear.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 12.51% sits firmly above HV20 at 11.8, leaving VRP at 0.71% - options are paid for realized that has already cooled. The IV-RV spread is persistently positive, and that's the signature of an active premium-harvest regime, not a one-print artifact. Short-strangle math keeps working as long as HV20 stays anchored beneath ATM IV.

The cleaner short-vol vehicles sit one rung out the risk curve. QQQ VRP at 2.64% prints as the richest of the index complex, and IWM VRP at 2.48% keeps small-cap premium fat versus realized - both pay more carry per unit of vega than SPY. Index dispersion is doing the work; selling the basket beats selling the constituents here.

The historical reminder lives in HV60 at 15.44 - the print panic vol leaves behind. Keep it on the desk as the sizing anchor: the harvest is on, but tails are not free.

What it means for your trading

VRP at 0.71% with HV20 cooled to 11.8 validates active short-premium harvest; QQQ VRP at 2.64% is the richest venue, with IWM at 2.48% close behind.

Skew Convexity

The quarter-delta put-over-call skew prints 2.76% with a smile ratio of 1.33% - left tail bid, right wing flat. Put quarter-delta IV at 11.23% trades meaningfully over the ATM reference of 9.83%, while call quarter-delta sits at 8.47%. Hedgers are paying for protection; nobody is chasing upside.

Smile ratio above one tells you the surface is asymmetrically rich - naked puts overpay for the convexity you're shorting, so spread structures are the cleaner harvest. The flat call wing means short upside premium prices in without giving away tail. SKEW index at 143.33 corroborates the tail bid without flagging panic curvature.

Net read: structure short-vol as put-spreads or iron condors rather than naked strangles, and let the asymmetric pricing pay for the wings you'd want anyway.

What it means for your trading

Quarter-delta skew at 2.76% with smile ratio 1.33% keeps the left tail richer than the right - favor put-spread and iron-condor structures over naked premium, with SKEW at 143.33 confirming hedger demand without panic.

Vol-of-Vol Structure

VVIX prints 93.70 against VIX at 16.81, a ratio of 5.57 that sits squarely in Normal territory. The vol surface is not pricing bimodal jump risk - there is no convexity premium being demanded for a vol-of-vol shock, which clears short-premium books to run at Standard Size.

That matters because the dampening regime is mechanically dependent on VVIX staying contained. With dealer vanna at -$265.06B deeply negative, any kink higher in VVIX forces dealers to sell delta into weakness - the accelerant we keep flagged but isn't priced today. Throttle-down trigger is a VVIX print through 110; below that, the calm front confirmed by VIX at 16.81 remains the operating reality.

Bottom line: standard sizing on iron condors and short strangles is cleared, but Iran-tape gappiness argues for keeping cheap left-tail convexity on. The vol-of-vol gauge is the single cleanest tell on whether the regime breaks - watch it, don't fight it.

What it means for your trading

VVIX at 93.70 versus VIX at 16.81 reads Normal - premium sellers run Standard Size, with a VVIX break through 110 as the throttle-down line.

Dispersion Spread

Index vol is doing nothing while the constituents carry the load. SPY ATM IV at 12.51% sits well below QQQ at 17.88% and IWM at 19.44% - the dispersion gap says single-name vol is absorbing the catalyst risk and the index is being held down by correlation collapse. That's a tell, not a tradable edge in the index alone: idiosyncratic AAPL/NVDA/AMZN catalysts won't hedge cleanly through SPY because the basket is averaging out the moves the names are actually making.

The actionable read flips the usual reflex. With QQQ VRP at 2.64% running richer than SPY at 0.71%, QQQ is the cleaner short-strangle vehicle - you get paid more for the same dampening regime. Own correlation, sell index. Selling single-name vol into elevated dispersion is the wrong side of the trade; the premium is rich for a reason.

What it means for your trading

Index IV compressed against sector IV - sell index premium (QQQ VRP at 2.64% the richest vehicle), avoid single-name vol selling while dispersion stays bid.

Liquidity & Microstructure

SPY's open interest spine clusters at 700 with the gamma flip parked at 713.68 - spot trades comfortably above flip, so dealer flow is mechanically buy-the-dip, sell-the-rip and the dampening regime is intact. The call wall at 720.00 is the magnetic ceiling: top-strike net GEX of $4.36B stacked at 720.00 means rallies into that level get absorbed, not extended.

The put wall at 710.00 backstops downside - first liquidity shelf if tape softens, with dealer hedging supportive above flip. The trade is to fade pushes into 720.00 and lean on 710.00 as the dip-buy reference. Lose 713.68 and the polarity flips: dealer flow turns amplifying, mean-reversion math breaks, and the cushion narrative goes with it.

What it means for your trading

Microstructure is constructive: spot above 713.68 with the 720.00 wall acting as a pin and 710.00 as the backstop - fade extremes, but treat the flip as the single regime-break trigger.

Trading readMassive positive gamma stack at the call wall says dealers are net long gamma into upside - fade pushes into that level, expect pin-style behavior into the close. Negative gamma cluster at the put wall is the trapdoor if spot breaches the flip.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$265.06B - deeply negative, and that is the asymmetry of the tape. Dealers are forced to sell delta as vol expands, which is exactly the accelerant a downside flush needs. Spot above the flip looks calm; cross the flip with a VVIX kick and the same book that dampened the rally amplifies the dip. Vol up = dealers sell delta - downside amplified if vol spikes.

Charm tells the closing-bell story. Net CHEX at -$1.71B drags spot toward the pivot at 720 - a Call Wall magnet - with current bias Neutral. Expect the tape to gravitate, not trend, into the cash close.

The break level is unambiguous: dealer flow flips below 713.68. Above it, fade pushes into 720.00 and let charm do the work. Below it, vanna takes the wheel and the regime inverts - keep cheap left-tail convexity on for that exact scenario.

What it means for your trading

Gamma is constructive but vanna is the silent risk: net VEX at -$265.06B means a VVIX pop converts the dampening regime into a forced-selling cascade. Trade the charm pin into 720, abandon the thesis below 713.68.

Cross-Asset Confirmation

MOVE at 72.07 stays subdued - credit isn't pricing the Iran headline tape, confirming this is geopolitical-risk-on rather than a credit shock. Bond vol calm removes the cascade signal that would otherwise force equity dealers to defend, and the absence of a MOVE bid is the cleanest tell that the headline flow is being faded by rates desks.

Sentiment corroborates: F&G prints 67 in Greed territory, supportive but not euphoric. QQQ at 672.25 and IWM at 277.26 sit aligned in positive gamma alongside SPY - no cross-asset divergence to exploit, with regime read Aligned across the index complex.

Cross-asset tone reads Unknown, which keeps the dampening regime intact: fade equity reactions to Iran headlines until MOVE itself starts bidding. That's the line where geopolitical noise converts into financial signal.

What it means for your trading

Bond vol at 72.07 and F&G in Greed with QQQ/IWM aligned positive gamma confirm the dampening regime - fade Iran-tape equity moves until MOVE bids.

Scenario EV

The book pays you to be short two-sided premium here, not directional. Recommended structure resolves to Iron Condor with a score of 53, edging the put-spread alternative at 41 - the gap is the skew tell. Downside is bid one-sided while the call wing stays flat, so wrapping the short put inside a condor harvests the same VRP without the naked-tail exposure a put-spread leaves on the table.

DTE sweet spot lands at 30-45, the bucket where forward vol 21.5295506223 against front 14.37 sets the cleanest carry hurdle. VRP assessment prints Unknown on the tape, but VVIX at 93.70 (Normal) clears Standard Size - vol-of-vol is not pricing tail panic, so books run normal weight rather than throttled.

Fade pushes into 720.00 as the upside cap; 713.68 remains the abandon-thesis trigger where dealer flow flips amplifying.

What it means for your trading

Iron condor in the 30-45 bucket is the highest-EV expression with score 53 - VRP active, VVIX normal, skew bid one-sided. Standard size, fade 720.00, kill the trade below 713.68.

Actionable Summary

SPY trades in Positive Gamma with net GEX at $7.64B and spot perched above the gamma flip at 713.68 - dealer flow dampens, mean-reversion wins, and the Elevated / Watchful tag says sized standard with tails kept cheap. The trade is short premium via Iron Condor in the 30-45 DTE bucket, where forward vol 21.5295506223 and VRP at 0.71% back the carry.

Fade pushes into the 720.00 call wall - that's also the charm pivot at 720, the magnetic close. Put wall at 710.00 backstops, but with net VEX at -$265.06B deeply negative, a VVIX kick - currently 93.70, normal - would force dealers to sell delta into the hole. Avoid naked downside until vol-of-vol rolls over.

Abandon thesis below 713.68 - that's where the regime breaks and dampening flips to amplifying. Keep cheap left-tail convexity on the back of MOVE at 72.07 staying contained while Iran headlines stay live.

Iran-US negotiation proposal via Pakistan is the macro tail risk on the tape - any de-escalation would compress front-vol and steepen contango further; escalation would invert it.

Exxon beating despite the Iran hit signals the energy complex is absorbing the supply shock - equity vol in the energy sector tracks Iran headline cadence.

Truce-language ambiguity on war powers keeps the Iran headline tape live - the single biggest source of bimodal-outcome risk for vol sellers this week.

Steady oil prices with weekly gain reinforces that the Iran premium is in but not exploding - supports MOVE staying contained and equity vol sellers staying paid.

Iran threatening response if US renews attacks is the live-ammo headline that would force a VIX spike and flip the dampening regime - primary watch item.

ConocoPhillips trimming production guidance over Qatar LNG flags real corporate revenue impact from the Iran conflict - earnings-season vol stays bid in energy.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 16.72 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.68 against a spot of 722.15. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.51% with a volatility risk premium of 0.71%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.81. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime