Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

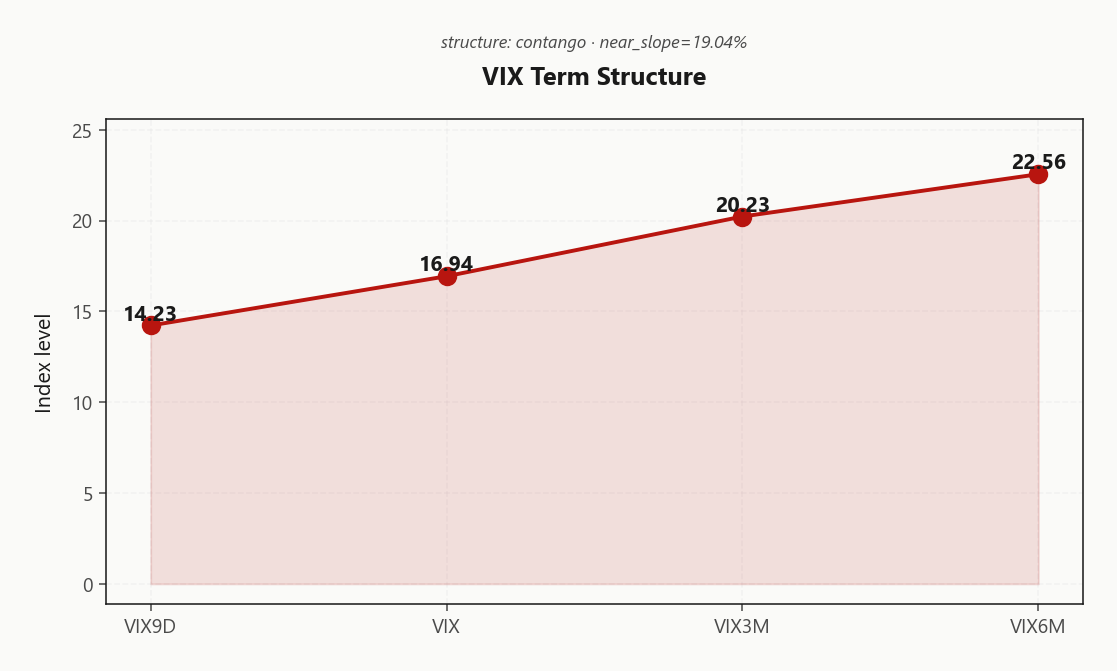

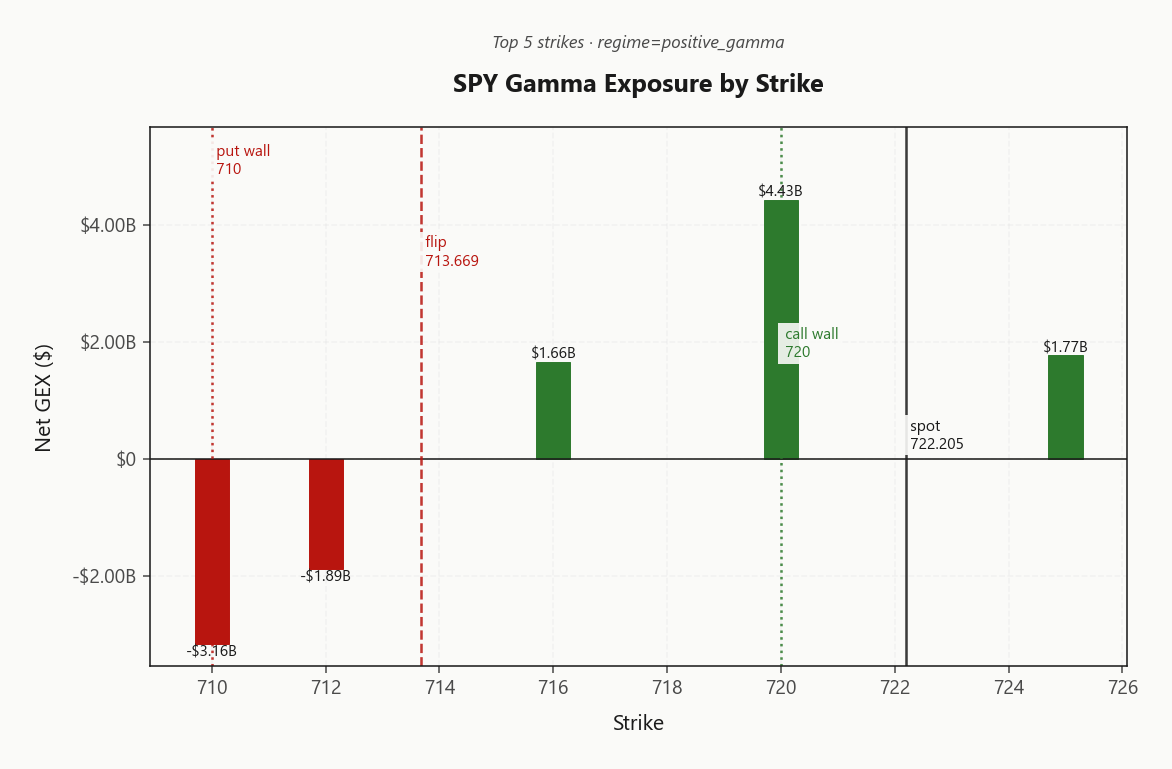

SPY at 722.21 sits in Positive Gamma with net GEX $7.68B and dealers long gamma - moves get dampened, mean-reversion wins. Key levels: call wall 720.00, put wall 710.00, gamma flip 713.67 - spot trades above flip, putting us deep in the cushion zone with the call wall acting as today's magnet ceiling. Dealer positioning is supportive: net DEX $133.24B long, but vanna -$260.01B negative - meaning a vol spike would force dealers to sell delta, accelerating any selloff if VIX breaks higher. Vol read: VIX 16.94 with VIX9D at 14.23 and 3M at 20.23 - steep Contango with near slope 19.04%%, VRP 0.63% so options are paid above realized 11.8. Bottom line: sell premium in the 30-45 DTE window via Iron Condor, fade strength into 720.00, and use IWM net GEX as the canary for regime breaks.

Positive gamma across index complex with steep VIX contango - vol sellers favored, mean-reversion regime intact

SPY trades inside a positive-gamma cushion with spot above 713.67 and dealers long $7.68B of gamma - moves dampen, walls hold. VIX term structure remains in Contango with VVIX at 93.90 signaling no jump-risk premium. The lone fragility: IWM net GEX flipped to -$235.8M, the first crack worth watching as the macro/Iran tape evolves.

Regime Assessment

Regime read: Elevated / Watchful with VIX anchored at 16.94. The transition matrix prints a 0.05 probability of escalating to panic over the next five sessions versus a 0.45 probability of drifting into the low-vol bucket in ten - the path of least resistance is down the vol surface, not up.

Half-life of 15 sessions makes this a sticky state. Combined with SPY parked in Positive Gamma above the 713.67 flip and a Contango term structure, the regime carries itself - mean-reversion dominates, dealer cushion holds, and vol carry compounds barring a fresh Iran headline that snaps the curve.

Trade the persistence: lean into Iron Condor in the 30-45 DTE window, fade strength into 720.00, and use -$235.8M as the canary - that's the only crack in an otherwise Aligned index complex.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life and panic transition probability of just 0.05 - drift toward low vol is the higher-probability path, favoring premium-selling structures into the persistence.

Trading readVIX, VVIX, SKEW, and MOVE all confirming benign regime - no divergence flagging hidden stress. Long-dated SKEW 143.33 is the one elevated read, but it's been there a while; the lack of divergence is itself a signal that the carry can persist.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve prints textbook geometry: 14.23 on the front, 16.94 spot, 20.23 at three months, 22.56 at six - a clean, monotonic Contango with near slope 19.04%%. The carry is on the table, and the curve is paying sellers to lean into it.

Forward 30→60 implied lands at 21.6886502577, with the 60→90 forward extending to 24.6709201288. Translation: no event premium is being priced into the front, no kink is forming in the belly, and the regime label resolves to Steep Contango. The absence of a backwardation flag is the signal - the tape is not bracing for a near-term shock, it is funding the seller.

The edge concentrates in the 30-45 DTE window, where roll-down is maximized and the curve is steepest. Structure of choice is the Iron Condor, with VVIX at 93.90 in the Normal band greenlighting Standard Size. Watch the front for any flattening - that is the first tell the carry is breaking.

What it means for your trading

Forward vol is in Steep Contango with the curve paying carry from 14.23 through 22.56 - sell premium in the 30-45 DTE window and watch the front slope for the first sign the regime cracks.

Trading readContango with VIX9D 14.23 well below VIX3M 20.23 - vol carry trade is paid generously, market does not expect imminent stress. The slope steepness is the green light for vol selling in the 30-45 DTE window.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 12.43% trades a clean premium to HV20 11.8, with VRP printing 0.63% vol points - the tape is paying for risk that hasn't shown up in realized. Short-premium structures collect this carry directly; the VRP read confirms options-cheap-to-realized is not the regime, and any framework leaning on long-vol mean-reversion is fighting the math here.

The texture underneath matters: HV60 at 15.44 sits well above HV20, meaning recent realized has cooled hard off a higher base. That cooling is what's funding the VRP - but it's also what makes the carry fragile. A single Iran headline that re-accelerates RV closes the gap from the wrong side, and the cushion compresses fast.

Trade the regime as it sits - harvest the spread via defined-risk shorts in the 30-45 DTE window - but size for the scenario where realized snaps back toward HV60 rather than staying anchored at HV20.

What it means for your trading

VRP active at 0.63% with ATM IV 12.43% over HV20 11.8 - short-vol carry is paid, but HV60 15.44 running hot warns the realized floor could lift on any fresh shock.

Skew Convexity

Front-expiry 2.84% skew with smile ratio 1.37% tells the story cleanly: put 25d at 10.52% sits well above ATM 9.19%, while call 25d prints 7.68% - inverted to the body. Downside is being paid for in an ordered, not panicked, way; the upside wing is begging for a bid that isn't coming.

The dealer book reads as hedged, not positioned for chase. With the call wing trading below ATM, there is no upside conviction embedded in vol - any rally into 720.00 gets sold by the same pin mechanics already running through the gamma profile. Skew geometry this steep on the put side, this flat on the call side, makes naked puts a bad-vega proposition.

Trade the geometry, not the level. Favor put spreads over outright premium for tail - the wing is rich enough that selling the further OTM put recaptures meaningful vega while preserving convexity. On the call side, fading strength outright beats buying upside vol. The skew is telling you exactly how the book is leaning.

What it means for your trading

Skew at 2.84% with smile ratio 1.37% reflects ordered downside hedging and an inverted call wing - structure tail risk via put spreads, not naked premium, and avoid paying up for upside convexity the dealer book isn't endorsing.

Vol-of-Vol Structure

VVIX prints 93.90 against VIX 16.94, putting the ratio at 5.54 - squarely in the Normal band. No bimodal pricing, no jump-risk premium embedded in the vol surface; the market is paying for variance, not for the right to gap.

That read clears the runway for vol selling at Standard Size - full clip on short-premium structures is on the table, not a half-position out of caution. Pair with the Positive Gamma backdrop and Contango curve and the carry case is intact across both vega and theta legs.

The break level is mechanical: VVIX through 110 is the first warning the carry trade snaps, and that's where vol-of-vol re-prices the iron condor wings overnight. Until then, fade vol bids; respect the trigger.

What it means for your trading

VVIX in the Normal band with sizing flagged Standard Size means short-vol structures are approved at full size - but VVIX through 110 is the line where the regime breaks and the trade comes off.

Dispersion Spread

SPY ATM IV at 12.43% trades materially under QQQ's 18.07% and IWM's 19.52% - the index hedge is the cheapest piece of paper on the screen, and the dispersion premium is being paid in single names while the index itself sits muted. Idiosyncratic risk is concentrated; correlation is not. That's the dispersion regime in one line.

The trade follows the geometry: harvest SPY/SPX premium over single-stock straddles. Selling vol at 12.43% against an index that's pinned in Positive Gamma with VIX term in Contango compounds the carry - index gamma cushions the path, single-name vol pays the dispersion bill. Avoid the inverse: short single-name vol gets steamrolled when name-level idiosyncrasy resolves into the tape.

Watch the IWM line - net GEX -$235.8M is the canary; if small-cap dispersion bleeds into correlation, the index-vol carry compresses and the trade shifts.

What it means for your trading

SPY IV at 12.43% compressed beneath QQQ 18.07% and IWM 19.52% argues for selling index premium over single-name straddles. Dispersion is paid in names, not the index - stay there until correlation re-couples.

Liquidity & Microstructure

The book pins to 720.00 as the dominant magnet, with $4.43B of net GEX concentrated at that strike doubling as the 720.00 call wall - dealers are pressed long gamma into a ceiling, and every rally gets sold mechanically against it.

Spot trades above the gamma flip at 713.67, keeping the cushion regime Positive Gamma: dips get bought, rips get faded, and intraday range compresses. Max pain anchors lower at 700 with the 710.00 put wall as the downside shelf - a clean bracketing structure for premium sellers.

The flip is the regime line. Hold above 713.67 and mean-reversion keeps printing; lose it and dealer hedging inverts from stabilizer to accelerant, with the OI cluster at 700 becoming the gravity well rather than a passive marker.

What it means for your trading

Bracket the tape: fade strength into 720.00, buy weakness toward 713.67, and treat a break of the flip as the signal that mean-reversion has expired.

Trading readMassive positive GEX cluster at 720.00 and 720.00 means dealers dampen rallies into those strikes - fade strength there. Below 713.67, dealer behavior flips and selling becomes amplified, so that's the line where mean-reversion stops working.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Vanna sits hostile: net VEX -$260.01B means a vol uptick forces dealers to sell delta into weakness, converting today's positive-gamma cushion into an accelerant the moment VIX trades through its near-term range. The book is calm, not robust - the second derivative is the trap.

Charm cuts the same direction. Net CHEX -$1.72B negative means time-decay flow tilts dealers toward selling into the bell absent a rally; the longer spot drifts sideways into close, the heavier the mechanical supply. Morning chop, afternoon drift lower is the path of least resistance unless buyers reclaim momentum.

The single line that matters: pivot 720 (Call Wall), current bias Neutral. Above it dealer flow stays cushioning; through it, vanna and charm align with gravity and the regime inverts. Trade the carry, but size against pivot - not against spot.

What it means for your trading

Positive gamma masks a fragile dealer book: vanna -$260.01B and charm -$1.72B both negative mean a vol spike or a quiet drift into close both feed the same selling reflex. Pivot 720 is the line where cushion becomes accelerant - bias currently Neutral.

Cross-Asset Confirmation

Cross-asset tape confirms the equity vol read: MOVE at 72.07 sits at benign levels with no rates or credit stress bleeding through, while Fear & Greed prints 67 (Greed) - sentiment supportive, no panic bid in the put book. This is the signature of an isolated geopolitical tape, not a systemic shock.

QQQ at 674.14 and IWM at 278.55 trade in lockstep with SPY's regime, leaving cross-asset tone Aligned. No fixed-income tell, no credit widening, no sentiment capitulation - the Iran headline tape is being absorbed by the vol surface, not metabolized by the underlying funding complex.

Geopolitical setups without credit confirmation mean-revert. Carry the short-vol book; treat the next escalation headline as a fade-able vol pop rather than the start of a regime break.

What it means for your trading

MOVE at 72.07 and F&G at 67 (Greed) confirm the equity tape is digesting an isolated geopolitical premium with no credit or sentiment fracture. Cross-asset alignment (Aligned) supports holding the short-vol carry through Iran headline risk.

Scenario EV

Scoring lands on Iron Condor at 52, comfortably ahead of the put spread at 40. The setup is clean: SPY anchored in Positive Gamma above the 713.67 flip, VIX term in Contango with near slope 19.04%%, and VVIX Normal at 93.90. Both wings sell without paying jump premium - the prerequisites are aligned, not just present.

Target the 30-45 DTE pocket where the curve is steepest and roll-down is maximized, bracketing 710.00 and 720.00. That window captures carry without inheriting gamma exposure into expiry - the structural reason this regime favors the condor over directional spreads. Sizing is Standard Size per the VVIX read.

The trade breaks if VVIX cracks higher or IWM net GEX at -$235.8M deteriorates further - those are the canaries, not the trigger. Until then, fade strength into 720.00, buy weakness toward 713.67, harvest the 0.63% VRP.

Trade the regime, don't fight it: with SPY in Positive Gamma above the 713.67 flip and dealers long $7.68B of gamma, the call wall at 720.00 is today's magnet ceiling. Sell premium via Iron Condor in the 30-45 DTE window, bracketing 710.00/720.00. Fade strength into the call wall, buy weakness toward flip - VRP at 0.63% and steep Contango pay you to wait.

Avoid: naked long calls (call skew inverted, no upside conviction in the dealer book), single-name short vol given the dispersion regime, and anything betting on backwardation. Watch: charm pivot 720 as the level where dealer flow inverts, IWM net GEX at -$235.8M as the canary for regime breaks, and VVIX north of triple digits as the first crack in the carry.

What it means for your trading

Regime is Elevated / Watchful with half-life 15 sessions - sticky enough that Iron Condor in the 30-45 window is the high-conviction trade, with IWM net GEX -$235.8M as the single canary worth watching.

Gold turning positive while oil eases on Iran-talks hope is the macro tell of the day - risk markets get a tailwind, vol sellers get carry, and the geopolitical premium that's been propping up VIX backwardation in front-month is unwinding.

Exxon production hit by Iran war confirms the operational damage is real, not just headline risk - energy earnings drag is a single-stock story, but it explains why MOVE stays bid even as VIX softens.

Iran formally proposing negotiations via Pakistan is the catalyst behind today's risk-on bid and oil softening - if talks hold, expect VIX9D to compress further into the curve, accelerating the contango carry.

US officially declaring the Iran truce 'terminated' for war powers purposes is a procedural marker - markets are pricing dialogue, but this keeps the optionality of escalation live and explains the persistent skew in long-dated SPY puts.

Trump-Merz public friction over Iran policy adds geopolitical tail risk that won't show in spot vol but quietly bids long-dated SKEW - the tail is being paid for, just not screaming.

Iran threatening 'painful response' if attacks resume keeps the binary outcome on the table - the reason VVIX stays bid even with VIX low; the market is paying for the right to reprice fast.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 16.96 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.67 against a spot of 722.21. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.43% with a volatility risk premium of 0.63%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.94. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime