Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

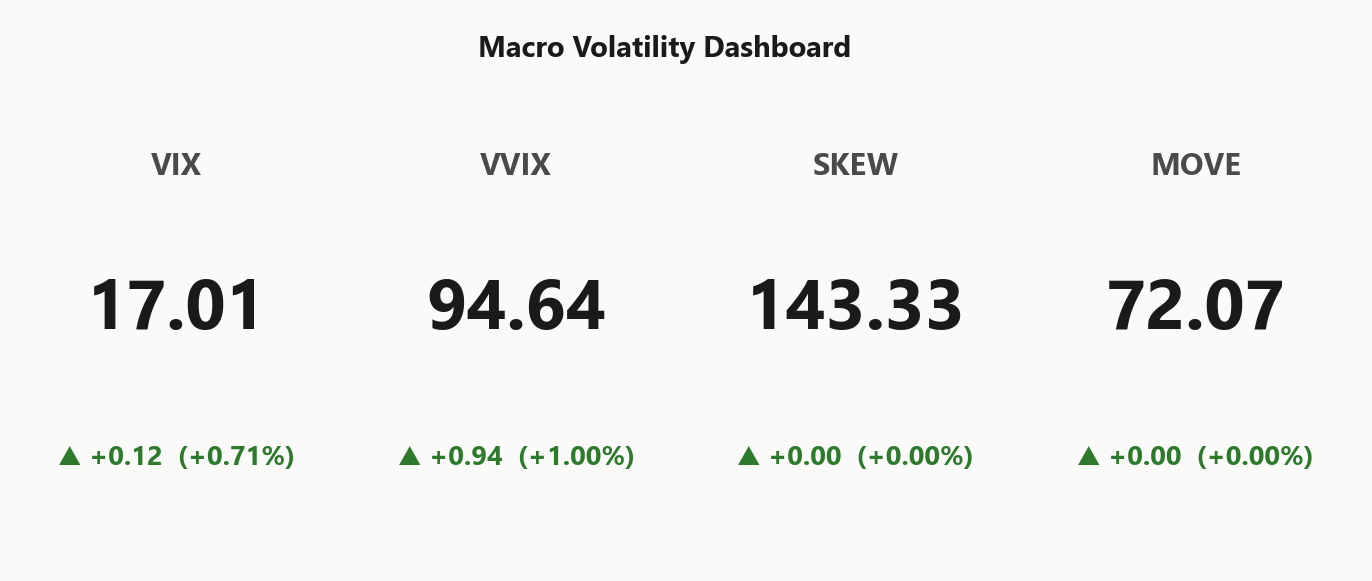

SPY closes at 720.20 with the index in Positive Gamma and net GEX at $7.55B - dealers long gamma, moves dampened. Call wall sits at 720.00, put wall at 710.00, gamma flip at 713.62 - spot is pinned at the call wall, meaning upside is capped without a flow regime change. Dealers are Neutral on charm pivot with vanna exposure at -$243.58B - vol up would force dealer delta selling, so the cushion is conditional on VIX behaving. VIX prints 17.01 with VIX9D at 14.18 and VIX3M at 20.38 - Steep Contango, vol carry trade is paying. VRP at 0.18% with VVIX at 94.64 confirms premium is real and vol-of-vol benign. 0DTE accounts for 50.4% of total gamma - heavy intraday pin force into next session's open. Bottom line: structure short premium between put wall and call wall, prefer iron condor in 30-45 DTE; cut sizing only if VIX breaks above VIX3M.

Positive gamma cushion intact across index complex with VIX at 17.01 and steep contango

Index complex closes with positive gamma cushion holding across SPY, QQQ, and IWM while VIX in Steep Contango keeps vol sellers' carry alive. Spot pinned at the call wall amid Neutral dealer bias, with VVIX at 94.64 signaling no jump-risk premium. Iron condor structure scored highest given Elevated / Watchful regime and 30-45 DTE sweet spot.

Regime Assessment

Regime sits in Elevated / Watchful with VIX at 17.01 - above the floor but well shy of stress. Half-life of 15 sessions says this is sticky tape, not a transient print, and the carry trade has runway to compound. Short-vol structures earn their roll-down so long as we stay in this band.

Tail probability to panic over five sessions reads 0.05 - cheap enough that a small VIX call wing remains rational ballast against the negative VEX backdrop. The larger asymmetry is the other way: probability of mean-reverting to low over ten sessions prints 0.45, and a vol crush compresses the very premium short-condor structures depend on.

Base case is grind. Position for stickiness, hedge the panic tail cheaply, and respect that the dominant risk to short premium is regime decay downward, not a blow-up upward.

What it means for your trading

Regime is Elevated / Watchful at VIX 17.01 with a 15-session half-life - short-vol carry favored, with the bigger threat being mean-reversion to a low-vol regime rather than a panic break.

Trading readVIX subdued, VVIX normal, SKEW elevated, MOVE benign - vol complex confirming each other rather than diverging. Elevated SKEW with calm VIX is the one quiet flag worth watching: tail still being bid even as the body sleeps.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

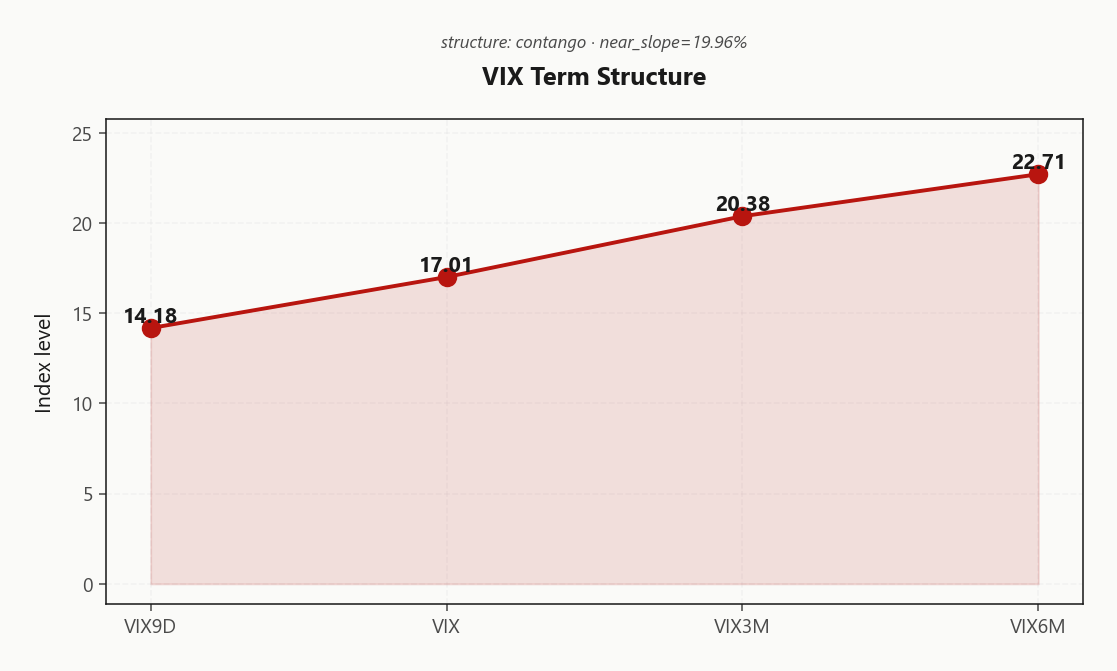

Forward Vol Geometry

The VIX term structure prints Contango from front to back, with VIX9D at 14.18 sitting decisively below spot VIX at 17.01 - no near-term event premium is being paid into the weekend, and the carry trade is clean.

The slope from VIX through VIX3M at 20.38 out to VIX6M at 22.71 registers a near-curve steepness of 19.96%, which the regime engine flags as Steep Contango - Steep contango - vol sellers favored. The market is calmly pricing forward risk higher than spot, not panicking; that is roll-down fuel, not a warning.

The cleanest edge sits in the belly. Selling front vol against the 20.38 pole captures the steepest roll-down without inheriting 0DTE pin chaos - structure short premium in the thirty-to-forty-five-session window, where carry is densest and gamma risk is still hedgeable.

What it means for your trading

With VIX9D at 14.18 well under VIX at 17.01 and the curve climbing through VIX3M to VIX6M in Steep Contango, the forward vol geometry endorses short-vol carry - concentrate the harvest in the belly of the curve, not the front.

Trading readSteep contango through six months says the carry trade is paying - sellers of front vol and buyers of back vol both win in this curve. Break in this slope is the signal that regime is changing, not the absolute VIX level.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 12% trades rich to HV20 at 11.82, leaving VRP at 0.18% - short-vol structures are earning carry over what the tape is actually printing. The premium is real, not optical, and it's the cleanest setup for iron condor harvest in the 30-45 DTE window.

HV20 sitting below HV60 at 15.42 tells you realized has been compressing into the close - recent tape calmer than the two-month average, reinforcing the Positive Gamma backdrop and the mean-reversion bias dealers are enforcing. That compression is the suppressive engine: positive gamma caps range, realized fades, and the IV-over-HV gap stays open for sellers to lift.

Net result - sell premium against this divergence, not into it. The structural edge is ATM IV pricing forward risk that HV20 isn't delivering, and until HV20 closes the gap toward HV60 or VIX breaks above 20.38, the carry trade pays.

What it means for your trading

VRP at 0.18% with HV20 of 11.82 compressing below HV60 of 15.42 is the textbook short-premium setup - ATM IV at 12% overprices realized in a Positive Gamma regime. Structure iron condor in 30-45 DTE; the carry pays until realized catches up.

Skew Convexity

Quarter-delta put skew prints 2.92% with the smile ratio at 1.4% - wings still cost up versus the body even as VIX sits at 17.01. Put 25d IV at 10.14% trades richer than ATM at 8.68%, confirming the downside tail remains bid despite the suppressive forward curve and benign vol-of-vol backdrop.

Call wing tells the opposite story - call 25d IV at 7.22% sits flat to the body, signalling no upside chase from end-users. That asymmetry is exactly what you'd expect with dealers long gamma and spot pinned at 720.00: the tape has no room to breathe higher, so call premium dies on the vine while put hedges keep paying.

Trade implication: structure short premium with defined put-side risk rather than naked, since the wing is bid for a reason. The flat call wing argues for selling upside calls inside the wall as part of an iron condor in 30-45 DTE - that's where the body-vs-wings geometry pays cleanest.

What it means for your trading

Skew at 2.92% with smile ratio above parity says downside hedges still command a premium while upside conviction has evaporated - sell the flat call wing inside 720.00, define risk on the put side.

Vol-of-Vol Structure

VVIX prints 94.64 against VIX at 17.01, parking vol-of-vol squarely in the Normal zone. No panic premium, no jump-risk being bid into the wings - the surface is calm and the surface of the surface agrees. That alignment is the tell: when VVIX disconnects upward from a sleepy VIX, it's the early warning of a binary the tape hasn't priced. Today it isn't.

The VVIX/VIX ratio at 5.56 sits elevated but not extreme - a function of VIX compression, not VVIX stress. Read it as carry-supportive rather than warning. There is no hidden bimodality embedded in the vol surface, and convexity-of-convexity isn't whispering about a weekend gap.

Translation for sizing: Standard Size. Short premium structures get full clip, not the half-size haircut you'd take if VVIX were flagging a latent jump. Pair this with the Steep Contango curve and the iron condor in 30-45 DTE earns its book weight. Cut size only if VVIX accelerates while VIX stays pinned - that's the genuine warning shot.

What it means for your trading

Vol-of-vol in Normal with VVIX at 94.64 clears the path for Standard Size on short premium - no hidden binary, full clip on the iron condor.

Dispersion Spread

Index vol stays well-anchored with SPY ATM at 12%, QQQ at 16.66%, and IWM at 18.75% - a clean stair-step that mirrors the cap-weight risk premium without any idiosyncratic leak from the single-name complex. Realized is tracking implied tightly across the trio, and the IWM-to-SPY spread reflects beta, not stress. Dispersion is moderate, contained.

The trade reads at the index level, not the constituent. With single-name vol failing to overflow into 16.66% ATM despite active mega-cap movers, long-dispersion carry is negative here - you'd be paying single-name premium against a calm index print. Sell index vol where the cushion is broadest and the spreads tightest.

Preferred expression: short premium on SPY and QQQ in the 30-45 window, leaning iron condor given Aligned regime alignment. Skip dispersion books until single-name realized starts pressuring index ATM - not happening yet.

What it means for your trading

Index ATM holds 12%/16.66%/18.75% with no single-name spillover - short index vol beats long dispersion until that calculus flips.

Liquidity & Microstructure

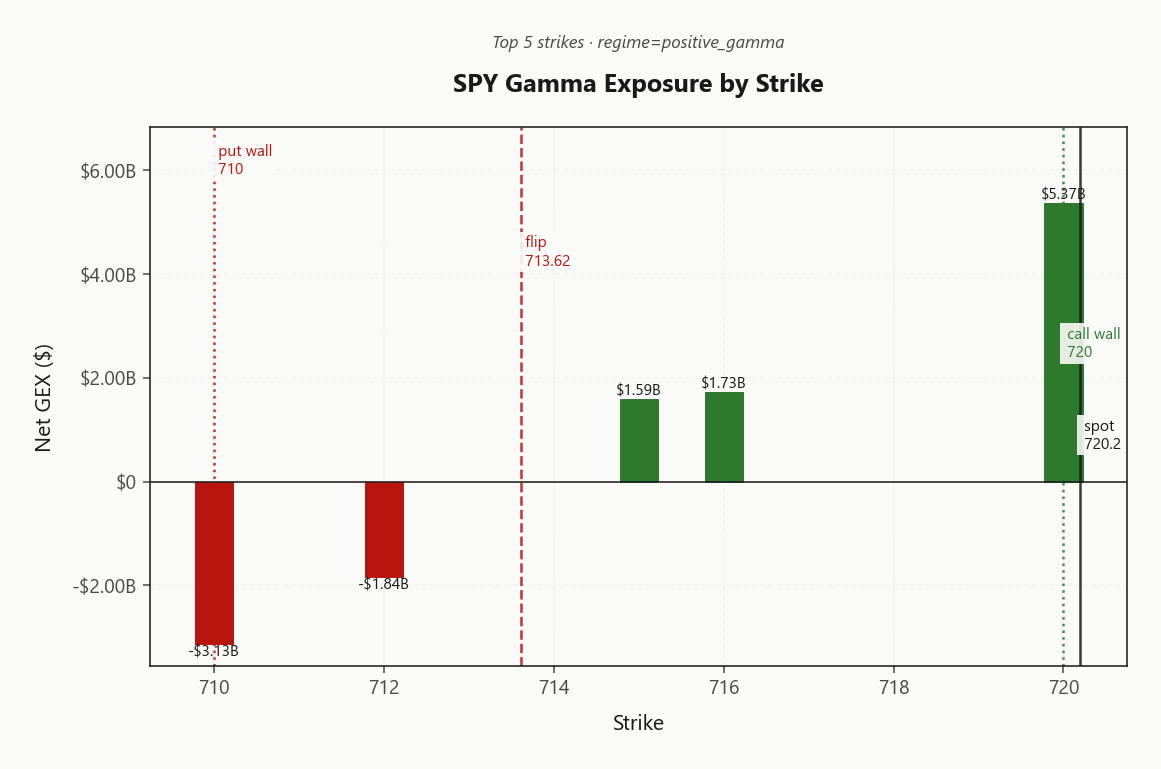

Open interest concentration tells the cleanest story in the book: the 720.00 call wall coincides with the dominant OI strike at 700 and the top gamma node at 720.00 carrying $5.37B of net GEX. That stack is the dealer ceiling - hedging flow absorbs upside drift mechanically as spot presses into it, which is exactly the behavior the tape printed into the close.

The cushion below is deep but not unconditional. Gamma flip at 713.62 sits well under the 710.00 put wall, giving a wide positive-gamma corridor for dealer mean-reversion to operate. Below the flip, dealer flow inverts - that is the line that converts an orderly drift into an amplified selloff. Until spot threatens it, the microstructure remains Positive Gamma and pinning forces dominate; through it, every hedge runs the other way.

What it means for your trading

Trade the 710.00 - 720.00 band as a dealer-enforced channel; 713.62 is the single level that flips the regime from absorptive to amplifying.

Trading readHeavy positive gamma stacked at the call wall says dealers will sell into strength and buy weakness in this band - fade rallies into the wall, only break the regime if spot pierces the gamma flip. The big negative cluster below shows where dealer support inverts and selloffs would amplify.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$243.58B - a deeply negative book that flips the risk asymmetry. Spot is cushioned by positive gamma, but a vol pop forces dealers to sell delta into the move; the cushion is conditional on VIX behaving, not absolute. Charm is mild at -$4.28B, so time-decay flow into the close stays modest - not the dominant driver here.

The pivot to watch is the Call Wall at 720. Current dealer bias reads Neutral with spot pinned right at the wall - a clean break above flips dealer flow direction and re-prices the cushion. Below it, dealers absorb; through it, they chase. One level, binary outcome.

Tilt is toward fading strength into the wall while the regime stays Positive Gamma and VIX holds 17.01. Hedge the asymmetric leg with a small VIX call wing - that's the trade negative VEX demands, not spot puts.

What it means for your trading

Negative VEX makes vol-up the asymmetric risk, not spot-down - size short premium accordingly and carry a small VIX wing. The Call Wall at 720 is the single level that flips dealer flow direction.

Cross-Asset Confirmation

MOVE prints 72.07 - rates vol is dormant, removing the credit/duration channel as a shock amplifier. With Fear & Greed registering Greed at 67, sentiment is leaning long into a tape that dealers are already cushioning; the contrarian read is that crowded positioning, not macro fragility, is the asymmetric risk here.

Bottom line: this is an isolated equity-vol calm, validated by benign rates and aligned dealer positioning - not a macro all-clear. Run short premium with size, but watch IWM's flip distance as the early-warning leg.

What it means for your trading

Benign MOVE at 72.07 and aligned positive-gamma across SPY/QQQ/IWM confirm the cushion is mechanical and broad-based; the only quiet flag is Fear & Greed at 67, where crowded sentiment becomes the contrarian risk into any vol pop.

Scenario EV

Scoring resolves to Iron Condor at 45 versus put spread at 34 - the two-sided dealer cushion between the 710.00 put wall and 720.00 call wall is what tips the structure. With Positive Gamma intact and VRP carrying at 0.18%, body-around-spot with wings outside the walls is the cleanest expression of the regime.

Optimal window is 30-45 DTE - far enough out to harvest roll-down on the Steep Contango curve from 14.18 through 20.38, but inside the belly to dodge the 50.4% 0DTE pin chaos. Calendars compete on the steepest part of the slope; condors win on the cushion.

VVIX prints 94.64 in the Normal band - guidance is Standard Size, no half-size required. Cut only on a VIX breach above 20.38; that is the single line that flips the carry trade.

What it means for your trading

Iron condor at 45 beats put spread at 34 because contango, active VRP, and benign VVIX are three legs of the same trade - structure in 30-45 DTE between 710.00 and 720.00, standard size.

Actionable Summary

Bottom line: structure short premium as an Iron Condor in 30-45 DTE, body around spot at 720.20 with wings outside the 710.00 put wall and 720.00 call wall. Regime reads Elevated / Watchful with the cushion intact above the 713.62 flip - sticky enough to harvest, not so calm that tails are mispriced.

Avoid naked upside calls into the 720 charm pivot - that's the dealer ceiling, and chasing strength fades against the same flow you're trying to monetize. Watch the call wall for any flip in dealer bias and the gamma flip as the cushion-break level; a breach below pulls the regime into negative gamma and the trade thesis with it.

Hedge the asymmetry with a small VIX call wing - net VEX at -$243.58B means a vol pop forces dealer delta selling. Sizing stays standard with VVIX at 94.64; cut only on a VIX breach above 20.38.

What it means for your trading

Sell the body, defend the wings: Iron Condor in 30-45 DTE between 710.00 and 720.00, with the 713.62 flip as the line that kills the trade.

Geopolitical de-escalation headline matters because the war-powers deadline removes a tail-risk overhang, supporting the calm forward vol curve and benign MOVE.

Walked-back Iran proposal language injects uncertainty back into the same headline that just calmed markets - watch for VIX9D to twitch on weekend gap risk.

Retirement-wealth executive order has medium-term equity flow implications - passive bid into broad index ETFs supports the structural positive-gamma backdrop.

Index-heavyweight earnings miss tied directly to the geopolitical narrative - single-stock vol matters less than the cross-confirmation that the macro headline has earnings teeth.

Mega-cap post-earnings continuation calls reinforce the QQQ call-wall pinning thesis - dealers are short calls and need to chase if these names break out.

Software earnings shock cuts against the SaaS-pocalypse narrative - single-name vol dispersion staying contained is what's keeping QQQ ATM IV anchored.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 16.99 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.62 against a spot of 720.20. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12% with a volatility risk premium of 0.18%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.01. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime