Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

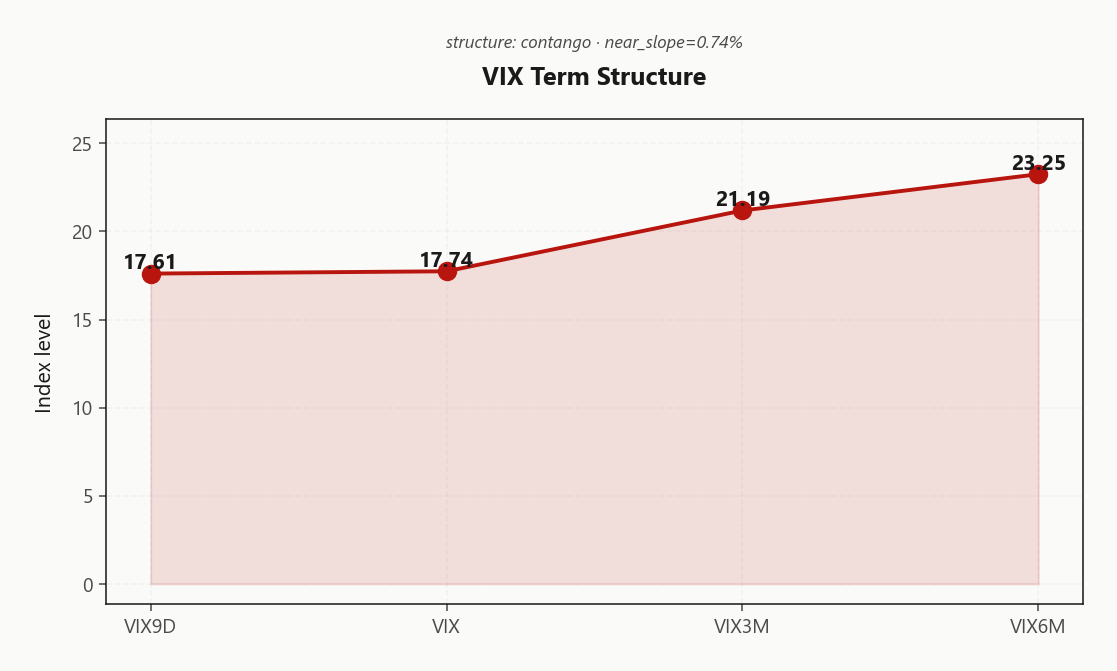

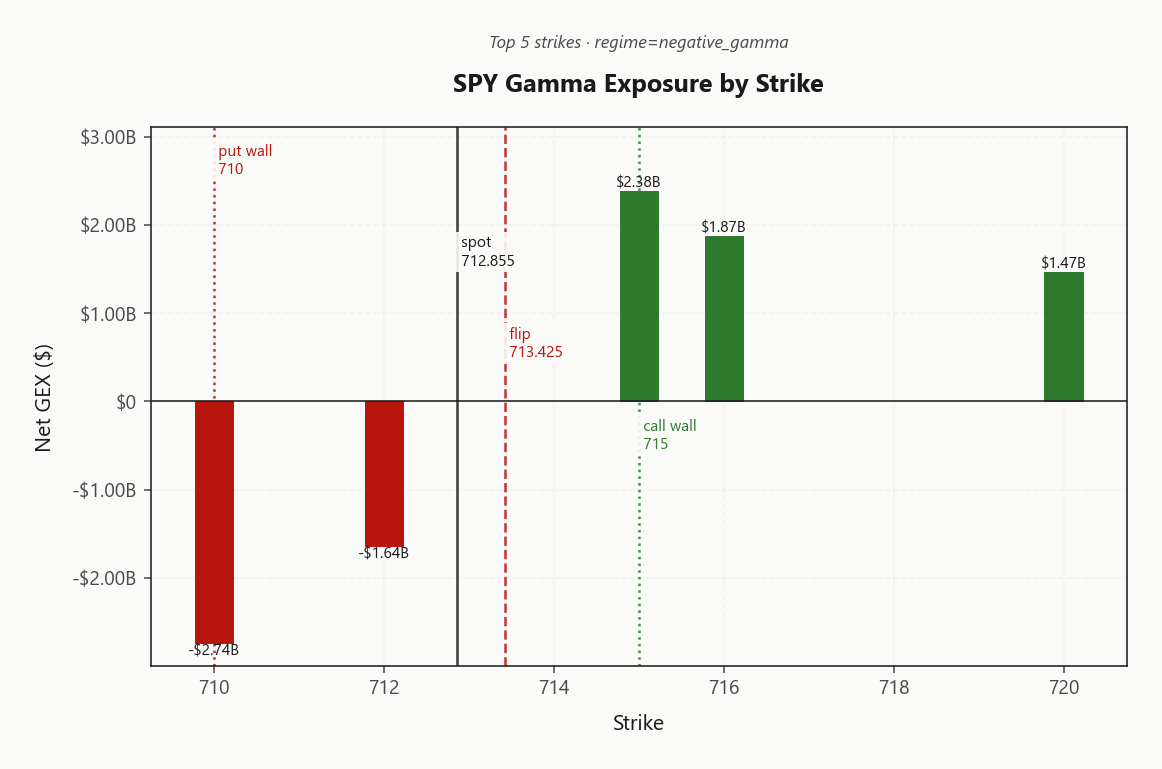

SPY at 712.86 is hovering on its gamma flip at 713.42, with net GEX at -$2.46B confirming a Negative Gamma regime - moves get amplified, not dampened. The day's box is the put wall at 710.00 and call wall at 715.00; max pain at 700.00 sits well below spot, with the heaviest OI cluster at 700. Dealers are short delta with vanna at -$206.02B and charm at -$1.14B - that's the Destabilizing setup, time decay pulls dealers to sell into close. VIX at 17.97 ticked lower on a Contango curve (VIX9D 17.61 → VIX3M 21.19), with VRP at 3.13% keeping options rich to realized at 11.75. VVIX at 96.02 popped 5.48%% - vol-of-vol normal, but the bid is real. Cross-asset is split: QQQ (Positive Gamma) and IWM (Positive Gamma) hold positive-gamma cushions, SPY does not - that's the divergence. Bottom line: fade strength into 715.00 and weakness into 710.00, sized half on the SPY structure given the flip-line risk; iron condors in the 30-45 DTE window are the cleanest harvest.

SPY pinned at flip with VIX in contango - fade extremes, dealer charm destabilizing into close

SPY is sitting precisely on its gamma flip at 713.42 - dealers are short gamma so any breach amplifies the move, while QQQ and IWM hold positive-gamma cushions above their flips. VIX term structure in Contango with VVIX at 96.02 keeps vol sellers in the carry seat, but the Destabilizing charm setup means time decay is pulling dealers the wrong way. Watch SPY's call wall at 715.00 and put wall at 710.00 - that's the day's range until proven otherwise.

Regime Assessment

Tape sits in a Elevated / Watchful regime with VIX anchored at 17.74 - not panic, not complacency, the awkward middle where carry still pays but tail hedges keep their bid. The current state reads Elevated, and the half-life of 15 sessions tells you this is a sticky equilibrium, not a hair-trigger setup waiting to flip on the next headline.

Transition math favors decay over escalation. Probability of jumping to a panic regime over the next handful of sessions sits at 0.05 - negligible - while the odds of cooling toward a low-vol state over a longer window run at 0.45. That asymmetry is the trade: the regime drifts lower more often than it breaks higher.

Implication: size short-vol carry to the regime, not the headline tape. Half-life 15 sessions is your mean-revert horizon - match DTE to it, don't fight it with front-week shorts.

What it means for your trading

Regime is Elevated / Watchful at VIX 17.74 with a 15-session half-life - sticky, drift-lower bias, low panic odds at 0.05. Carry the vol; don't chase the tape.

Trading readVIX cooling, VVIX bid, MOVE flat, SKEW elevated - partial divergence; equity vol is being sold but tail bid is holding up, classic late-stage carry-with-a-tail-hedge regime.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve sits in Contango with VIX9D at 17.61 barely beneath spot VIX at 17.74 and VIX3M parked well above at 21.19 - that is Steep Contango, and the carry is paid, not threatened. Forward 30-to-60 vol implied by the curve sits comfortably above spot VIX, which means the slope is not a roll-down trap; sellers of belly vol are getting compensated for the calendar, not picking up dimes.

The edge is not in the front week. Front-dated IV at 19.03 stays bid for sticky event premium and 0DTE charm risk - that piece prices what it prices, harvest it elsewhere. The 30-45 DTE window is where the contango actually pays: term premium rich, realized cooling, and far enough out to dodge the binary at the SPY flip.

What it means for your trading

Term structure is Steep Contango with forward vol implied by the curve well above VIX - short-vol carry in the 30-45 DTE belly is the cleanest expression. Leave the front week alone; that is event-risk premium, not edge.

Trading readContango from 17.61 to 23.25 is paid carry for vol sellers; the front-month basis at 19.45%% is wide enough to call the curve healthy.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 14.88% sits well above 20-day realized at 11.76, with VRP at 3.13% confirming a Moderate Premium premium that is being paid, not theoretical. This is the harvestable kind of richness - options are bid for protection while actual tape movement is decelerating underneath.

The cooling is structural: 5-day RV at 7.17 has collapsed beneath the 20-day at 11.76, and the 20-day sits below 60-day at 15.34. Realized is mean-reverting downward into a regime where implied has yet to follow - that's the gap shorts get paid to close.

Setup favors short-vol structures sized to the Elevated / Watchful regime, with carry harvested through Iron Condor in the 30-45 DTE belly rather than front-week where event premium is sticky. Stagger entries - VVIX at 96.02 says vol-of-vol is bid even as VIX cools.

What it means for your trading

VRP at 3.13% with HV20 at 11.76 cooling beneath HV60 at 15.34 is a genuinely harvestable IV-RV gap, not a trap. Short-vol carry through 30-45 DTE iron condors is the cleanest expression.

Skew Convexity

Quarter-delta skew at 3.84% with smile ratio 1.23% tells the whole story: downside is bid, but it's ordered bid - protection paid up in size, not panic chased. Put wing at 20.93% sits well clear of ATM at 18.4%, while the call wing flattens at 17.09% - no one is paying for upside convexity.

That asymmetry is the trade. With the left tail this rich and the right tail this cheap, naked puts overpay for skew that's already priced; put spreads capture the directional bias while financing the wing you're long against the wing the market is bidding. Skip the call side entirely - flat call skew on a tape parked at the gamma flip is the market telling you it doesn't believe in the breakout.

Net read: skew steep but ordered, smile ratio confirms hedging flow rather than crash repricing. Harvest the put-wing premium via spreads, fade upside vol via short calls only into the call wall, and treat any skew flattening intraday as the early tell that dealers are getting their hedges off.

What it means for your trading

Quarter-delta skew at 3.84% with smile ratio 1.23% = ordered downside bid, flat call wing at 17.09% = no upside conviction. Put spreads beat naked puts; ignore the call side.

Vol-of-Vol Structure

VVIX at 96.02 against VIX at 17.74 puts the ratio at 5.41 - squarely in Normal territory. No bimodal tail being priced, no convexity panic in the options-on-options book; the second-derivative is awake but not screaming.

The wrinkle is the direction of the move. VVIX bid 5.48% while spot VIX softened -5.69% - that's a divergence, not a confirmation. Vol-of-vol getting paid into a cooling VIX tells you the desk is bidding upside vol convexity even as front-month carry compresses. Read it as a hedge accumulation tape, not a fresh fear bid.

Sizing per the regime: Standard Size. Run the iron condor harvest at full clip, but stagger entries - the VVIX bid is the early warning that any spot VIX repricing will be reflexive, not gentle. Standard size today, twitchy stops if VVIX extends.

What it means for your trading

VVIX/VIX at 5.41 flags a Normal vol-of-vol regime - short-vol carry remains the trade, sized Standard Size. The VVIX bid into a softer VIX is the tell to watch: hedge-accumulation flow, not panic, but it raises the convexity cost of being late to cover.

Dispersion Spread

Index vol is moderate with SPY ATM IV at 14.88%, but the single-stock complex is pricing materially richer - QQQ ATM IV at 20.84% and IWM at 22.14% tell you correlation isn't pinned to one, so the dispersion premium is alive and harvestable.

Cross-strike IV dispersion at 69.5 with cross-expiry at 2.09 confirms wings are being paid up while the belly compresses - that's a classic relative-value setup, not noise. The Qqq Heavier divergence between SPY's Negative Gamma book and QQQ's Positive Gamma cushion sharpens the angle: index gamma is fragile while single-name carry is intact.

Trade structure: short index vol via SPY iron condors in the 30-45 DTE window, financed against long single-name vol in the mega-cap GEX-rebuild cohort. The inverse - long index, short single-name - is the trap given correlation isn't extreme.

What it means for your trading

Single-name IV richer than index IV with cross-strike dispersion at 69.5 keeps the dispersion trade live; harvest SPY vol against single-name longs, not the other way around.

Liquidity & Microstructure

Order book structure is barbelled: the heaviest open interest sits at 700 as the long-dated put magnet, while the call wall at 715.00 caps the upside. The day's gravitational center is the top GEX strike at 710.00, carrying net GEX of -$2.74B - that's where dealer flow concentrates and where pin pressure clusters into the close.

Spot at 712.86 sits a hair below the flip at 713.42, making the binary real-time. Above the flip, dealers buy weakness and sell strength - rallies get supported, dips get bought. Below it, the polarity inverts: selling amplifies selloffs, every tick lower forces incremental supply. The put wall at 710.00 is the next gravity well if the flip cracks.

Trade the box: fade strength into 715.00, fade weakness into 710.00, but size half on the SPY leg given the flip-line fragility. The structure is deep, not thin - liquidity isn't the problem, the regime is.

What it means for your trading

SPY's microstructure is a barbell anchored by deep-OTM put OI at 700 and the call wall at 715.00, with spot pinned a tick below the gamma flip at 713.42 - the flip is the binary that decides whether dealer flow dampens or amplifies the next move.

Trading readSPY gamma profile is barbell with the call wall at 715.00 as the upside dampener and the put wall at 710.00 as the downside accelerant; spot pinned at the flip means today is binary, not range-bound.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer book is Destabilizing: net VEX at -$206.02B is deeply negative, so any vol pop forces dealers to sell delta into the move - the classic accelerant, not a dampener. Spot sits just under the pivot at 713.4247500942, the gamma flip; until that level is reclaimed, the bias stays one-way and breaches amplify rather than fade.

Charm is the second engine. Net CHEX at -$1.14B means time decay drags dealer hedges the wrong way into the bell - programmatic selling pressure builds through the PM session regardless of tape. Pair that with a negative-VEX book and the path of least resistance into the close is lower, not flat.

Trade the level, not the narrative: above 713.4247500942 the accelerant flips to a tailwind for rallies; below it, fade strength and respect the put wall at 710.00 as the next magnet. Avoid naked 0DTE shorts - charm pressure is on your side as a structure, against you as a runner.

What it means for your trading

Dealers are Destabilizing with VEX at -$206.02B and CHEX at -$1.14B; the gamma flip at 713.4247500942 is the binary line - below it, moves amplify and charm sells into the close.

Cross-Asset Confirmation

Cross-asset tape is the reassurance trade: MOVE at 74.33 sits flat with bond vol asleep, and Fear & Greed prints 64 (Greed) - sentiment still risk-on despite a Reuters tape stuffed with Iran-war headlines. No credit-spread reaction, no rates-vol breakout. This is isolated geopolitical premium living in equity skew, not a compounding credit crisis bleeding into the funding stack.

The internal split is the lead. SPY runs Negative Gamma while QQQ at 661.99 holds Positive Gamma and IWM at 273.66 mirrors with a Positive Gamma cushion - the divergence is Qqq Heavier, with the Qs and Russell carrying the upside dampener that SPY no longer has. That makes SPY the fragile leg into any vol pop and the Qs the relative anchor.

Trade implication: lean the SPY-short / QQQ-long pair as the cleanest hedge against the gamma-flip binary, and keep MOVE on the dashboard - a breakout there is the one signal that converts isolated equity premium into systemic repricing.

What it means for your trading

Macro plumbing is intact - bond vol flat at 74.33 and sentiment at Greed confirm no credit shock - so today's risk is purely the SPY vs QQQ regime split, not a top-down deleverage. Fade the divergence via SPY/QQQ pair structures while MOVE stays asleep.

Scenario EV

Edge of the book scores cleanest as Iron Condor at 63, with the put-spread alternative trailing at 55 for traders who want directional skin. Paid VRP at 3.13%, a Contango curve from 17.61 to 21.19, and normal vol-of-vol at 96.02 stack the carry case - VRP assessment reads Unknown, but the structural signal is unambiguous.

Sweet spot is the 30-45 DTE belly - far enough out to capture the IV - RV gap with HV20 at 11.75 cooling under HV60, short enough to avoid forward-curve drift. Skip 0 - 2DTE: charm bias is Destabilizing with net CHEX at -$1.14B, and front-week IV at 19.03 is sticky on event premium.

Sizing guidance reads Standard Size - full clip, but stagger entries around the SPY flip at 713.42 and bracket the box between the put wall 710.00 and call wall 715.00.

What it means for your trading

Iron condor in the 30-45 DTE belly is the highest-scoring harvest at 63; put spreads at 55 are the directional fallback if the SPY flip at 713.42 breaks.

Actionable Summary

Trade: harvest VRP via Iron Condor in the 30-45 DTE belly, structured around SPY's call wall at 715.00 and put wall at 710.00. With VRP at 3.13% and the curve in Contango, the carry is paid; size standard per Standard Size and stagger entries.

Watch: SPY pivot at 713.4247500942 - break below flips the book to trend-amplification with net VEX at -$206.02B and net CHEX at -$1.14B dragging dealers the wrong way. Avoid naked 0DTE shorts: charm bias is Destabilizing into the close.

Iran threats with oil seesaw is the macro tape's primary driver - keeps geopolitical premium in skew but the absence of a credit-spread reaction means it's still localized.

Stagflation framing as the Iran war drags on is the slow-moving regime risk - bond vol has not responded yet, but a MOVE breakout is the trigger to watch.

Oil retreat from a 4-year high softens the immediate inflation impulse - partially explains why VIX cooled and contango persists despite the headline tape.

Fed dissent with Powell staying is the rates-vol wildcard - MOVE flat today says the market hasn't repriced, leaving room if dissent turns formal.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.97 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.42 against a spot of 712.86. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.88% with a volatility risk premium of 3.13%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.74. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime