Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

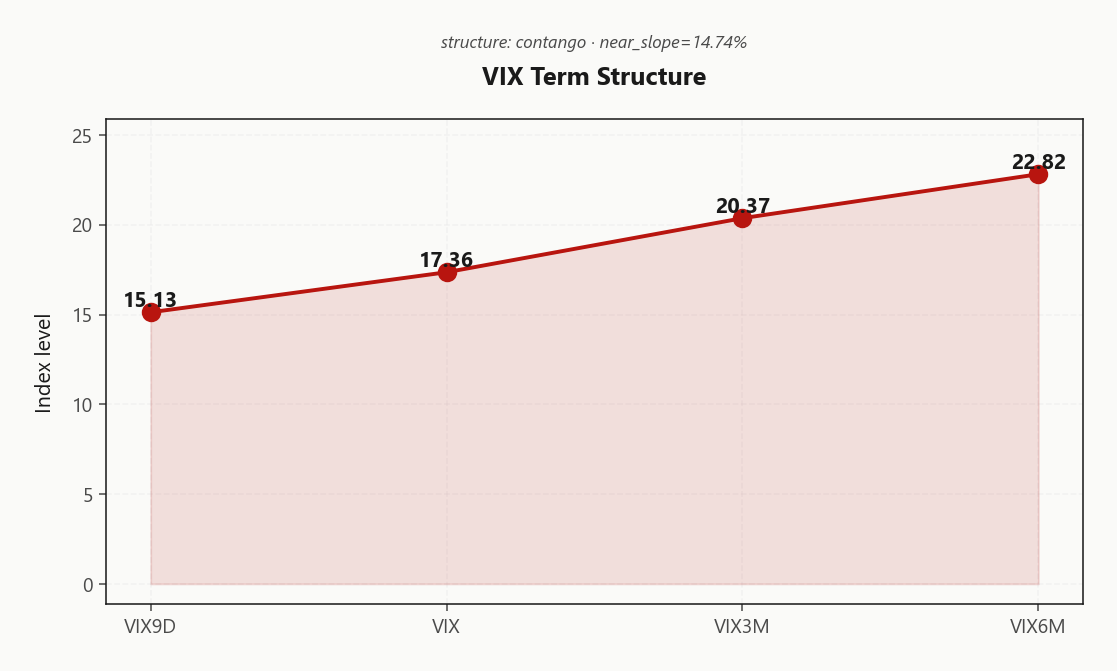

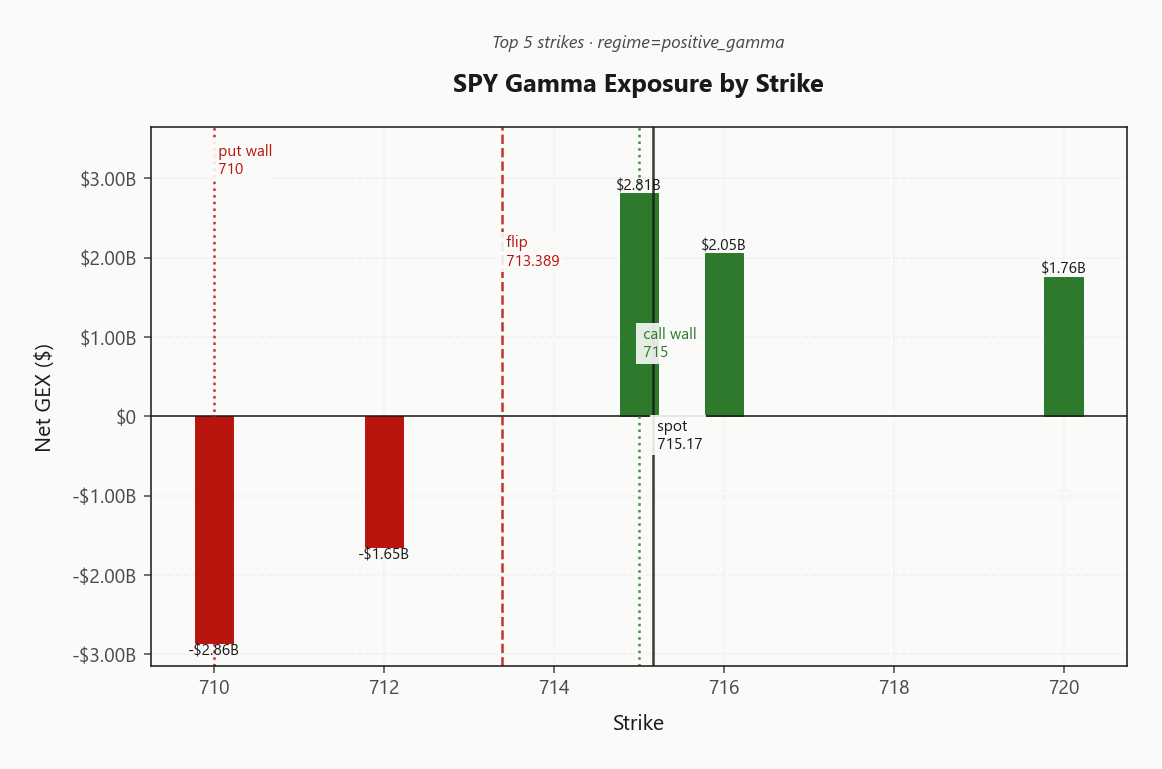

SPY at 715.17 sitting essentially on the 715.00 call wall with net GEX at $750.6M - deeply positive gamma regime, dealers long, mean-reversion tape. Gamma flip sits at 713.39, put wall at 710.00, max pain at 700.00 - spot pinned right at the upper edge of the dampening zone. Dealer net VEX at -$226.3B and net CHEX at -$1.14B mean vanna is hostile if vol spikes (dealers sell delta into a tape down) but charm is grinding into close. VIX at 17.36 (down -7.71%%), VIX9D at 15.13 versus 3M at 20.37 - steep contango, slope 14.74%%, VRP at 1.47% keeps premium sellers paid. VVIX at 94.35 is benign, no jump risk priced. Bottom line: fade strength into 715.00, lean iron condors 30-45 DTE; only flip bearish if SPY breaches the 713.39 flip.

Positive gamma cushion across index complex with VIX cooling into 17.36 and steep contango

Index complex sits deep in positive-gamma territory with SPY pinned at the 715.00 call wall and dealers long gamma across SPY/QQQ/IWM. VIX term structure is in steep contango (Contango) with VVIX at 94.35 signaling normal vol-of-vol - sellers' carry is intact. Iran-war headlines remain background noise as the market shrugs and harvests premium.

Regime Assessment

Current regime tags Elevated - labeled Elevated / Watchful - with VIX parked at 17.36. That puts us in the watchful zone, not the panic zone: transition probability to panic over the next handful of sessions reads 0.05, while drift back toward calm carries 0.45 over a longer window. The asymmetry favors mean-reversion books, not crash-hedge stacking.

Half-life of 15 sessions makes this regime sticky - no need to rotate vol stance daily, no reason to chase every headline tick. Signal color reads Yellow, which lines up cleanly with the steep Contango stack and benign 94.35 vol-of-vol - three independent reads pointing at the same harvest setup.

Lean into the persistence. Run the iron condor at 30-45 DTE, watch for VVIX divergence as the early break cue, and let the 15-session half-life do the carrying.

What it means for your trading

Regime is Elevated / Watchful with low panic-transition odds and a sticky 15-session half-life - this is a harvest tape, not a hedge tape, until the signal flips.

Trading readVIX cooling, VVIX benign, MOVE flat, SKEW steady - every macro vol gauge confirms the same story, no divergence to flag the next regime shift yet.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX9D→VIX→VIX3M→VIX6M ramp is textbook Steep Contango, with 15.13 printing well below 17.36 and the 3M anchor at 20.37. Near-slope of 14.74% confirms the structure is Contango, not flirting with backwardation - vol carry is fully intact and short-dated premium sellers collect structural roll-down on every session that holds.

Forward 30-to-60 vol prints at 21.7191286658, with the 60-to-90 forward at 25.0313383581 - the term-premium pocket lives squarely at the 30-45 DTE bend. That is the clean window: enough roll to monetize, not so far out that the forward curve flattens and edge evaporates.

Crucially, no backwardation is priced despite the Iran tape - the market is discounting the tail, not bidding it. Lean into the carry; do not pay for protection the curve refuses to price.

What it means for your trading

Term structure is in clean Steep Contango with 15.13 anchoring the front and 20.37 the belly - sellers' carry is paid, sweet spot at 30-45 DTE.

Trading readClean contango with 14.74%% near-slope says vol carry trade is alive and well - no event premium baked in, sellers' regime confirmed.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 13.19% sits comfortably above HV20 at 11.72, leaving a 1.47%-point cushion of risk premium for short-vol books. RV5 at 7.72 running well below the 20-day window confirms the tape has decelerated meaningfully into the print - sellers are being paid for calm that has already arrived, not calm they have to forecast.

The IV-RV spread reads Thin Premium, but the structural setup remains intact: HV60 at 15.37 printing above HV20 at 11.72 says the realized-vol curve is rolling lower, with the recent tape quieter than the broader window. That decay path is the engine that keeps premium harvest priced through the front weeks.

Cross-index, the richer carry sits outside SPY - QQQ VRP at 3.42% and IWM at 3.94% dominate the SPY edge on a per-vega basis. Rotate the harvest into single-index condors on QQQ and IWM rather than forcing size in SPY where the premium is thinnest.

What it means for your trading

VRP active with ATM IV at 13.19% above realized - short-vol structures retain edge, with QQQ at 3.42% and IWM at 3.94% the cleaner harvests.

Skew Convexity

Quarter-delta put skew prints 2.4% with a smile ratio of 1.17% - moderately steep but ordered, not panic-bid. Put 25d IV at 16.63% sits clearly above ATM at 15.76%, while call 25d IV at 14.23% rounds out a flat upside wing. The chain is paying for left-tail insurance in measured size - no fire-alarm bid in the wings.

With smile geometry this orderly, spread protection beats naked puts on cost - put spreads harvest the steepness instead of paying for it outright. Flat call skew confirms zero upside conviction in the chain, which lets premium sellers lean directly into the 715.00 call wall without paying up for convexity that isn't bid. Section signal sits steep but ordered - a watchful yellow, not a defensive red.

What it means for your trading

Skew at 2.4% with smile ratio 1.17% reflects ordered downside premium, not stress - favor put spreads over naked puts and sell calls into the flat upside wing.

Vol-of-Vol Structure

VVIX prints 94.35 against VIX at 17.36, a ratio of 5.43 that plants vol-of-vol firmly in Normal territory. No binary is being priced into the wings of the VIX chain - the jump-risk premium that would tag a VVIX bid above the panic threshold is absent, and the chain is not paying up for convexity on convexity.

Translation for the book: derived sizing reads Standard Size, so short-vol structures get full clip rather than the half-size haircut a stressed VVIX would force. The Iron Condor at 30-45 DTE carries cleanly here - vega risk is dampened, gamma-of-vega is benign.

Watch the divergence: if VIX presses to a fresh low and VVIX refuses to follow, that is the early jump-risk tell - the chain quietly bidding tail convexity while spot vol compresses. Until then, the green light on vol-of-vol is the cleanest standalone signal in the complex; size to plan, not to fear.

What it means for your trading

Vol-of-vol at 94.35 confirms Normal - full-size short-vol structures are sanctioned, with VVIX/VIX divergence the only trigger to defensively rescale.

Dispersion Spread

Index vol is priced consistently across the complex - SPY ATM IV at 13.19% sits in line with QQQ at 18.82%, while cross-strike dispersion of 77.49 against cross-expiry of 2.37 tells you the chain is repricing skew, not term. Index hedges are cheap relative to the single-name bid, and that gap is the trade.

The mover board is concentrated where it always concentrates when dispersion widens: NVDA, AAPL, AMZN and GOOGL are stacked one through four on absolute GEX change with positive direction, MSFT rounds out the top five. Mega-cap dealer rebuild is doing the heavy lifting in QQQ - idiosyncratic vol is being paid, but it doesn't translate one-for-one into index realized when correlation stays suppressed. Selling SPX/SPY premium against this backdrop captures the index-level VRP without paying up for the single-name tail.

Preferred expression: Iron Condor on the index, 30-45 DTE, not single-name strangles. The risk to this stance is a correlation jump - if Iran headlines re-accelerate and dispersion compresses, index vol catches up to the single-name complex fast and the dispersion edge collapses into a directional vol bid.

What it means for your trading

Dispersion is wide and ordered: index ATM IV at 13.19% is priced consistently with QQQ at 18.82% while mega-cap idiosyncratic flow stays concentrated - sell index premium, leave the single-name strangles alone unless correlation re-bids.

Liquidity & Microstructure

The book anchors at 700, a put-heavy OI cluster that pins the downside, while the gamma flip sits just beneath spot at 713.39. Holding above that line is the entire ballgame - dealer hedging absorbs both directions inside the dampening zone, buying weakness and selling strength. Lose it and the regime inverts.

The single largest dealer node lives at 710.00 with net GEX of -$2.86B, stacking the chain's heaviest hedging obligation right at the upper rail. The 715.00 call wall is THE level - flow flips from absorbing to amplifying on a clean break above, and into expiry it acts as a ceiling magnet. The 710.00 put wall mirrors that on the downside.

Translation: fade extensions toward the wall, lean against the put wall, do not chase a breakout unless spot exits the dampening band. Liquidity is deep while the regime holds.

What it means for your trading

Spot above the 713.39 flip keeps dealers absorbing both tails into the 710.00 - 715.00 dampening band; the 710.00 node is the flow-inversion trigger to watch.

Trading readMassive positive gamma stack right around spot says dealers absorb both directions - fade extensions toward 715.00 and lean against the 710.00 put wall, don't chase breakouts unless spot leaves the dampening zone.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX at -$226.3B sits deeply negative - the textbook vanna accelerant. Any vol uptick forces dealers to shed delta into weakness, converting a routine wobble into a directional cascade. This is the hidden trapdoor under the positive-gamma cushion: gamma absorbs, vanna amplifies, and the two only coexist peacefully while VIX stays bid-cooled.

Charm meanwhile is doing the opposite work. Net CHEX at -$1.14B grinds dealers progressively shorter into the bell as time decay leans the book long delta - the classic afternoon pin engine. The pivot to mark is 715, a Call Wall with current bias Neutral; spot sits essentially on the line at -0.023770572.

Trade the asymmetry: lean with charm into close while gamma holds, but treat 715 as the kill-switch. A breach flips dealer flow from absorbing to amplifying, and the negative VEX does the rest.

What it means for your trading

Vanna is hostile, charm is constructive, and they meet at 715 - harvest the pin above, abandon the playbook below.

Cross-Asset Confirmation

Cross-asset signal is Aligned and that is the load-bearing fact of the session. MOVE printing 74.33 tells you bond vol is asleep - there is no credit stress bleeding into the equity chain, no funding tantrum lurking behind the Iran headline tape. When MOVE refuses to bid, the canonical macro shock script does not run, and equity vol sellers can keep collecting without the rates-vol overlay that usually forces a defensive crouch.

QQQ at 663.67 and IWM at 276.26 are tracking SPY tick-for-tick, with all three indices sitting in positive_gamma while VIX lives in its own negative-gamma world - textbook risk-on geometry, no leader rotating against the tape. Without dispersion between large-cap, tech-heavy and small-cap complexes, there is no single asset class lighting the fuse for a regime flip.

Fear & Greed at 65 in Greed is the one yellow flag - sentiment is leaning, not extreme, but a further climb tilts the contrarian setup. Treat Iran as headline noise until MOVE bids or IWM breaks alignment.

What it means for your trading

Aligned cross-asset tape with calm bond vol at 74.33 and Greed sentiment confirms this is a premium-harvest regime, not a credit shock. Watch for IWM divergence or a MOVE bid as the first crack in the alignment thesis.

Scenario EV

The scoreboard converges on a single trade: Iron Condor tops the EV stack at 56, ahead of the put spread at 44. With VRP active, VVIX printing 94.35 in the normal pocket, and net GEX of $750.6M anchoring the dampening regime, every input pulls toward premium collection rather than directional convexity.

Sweet spot is 30-45 DTE - far enough out that theta carry compounds against the steep Contango roll-down, close enough that gamma stays manageable as spot grinds against the 715.00 ceiling. Place the call wing outside 715.00 and the put wing outside 710.00 to ride the max-pain magnet at 700.00.

Sizing follows Standard Size - no defensive scaling needed while VVIX/VIX prints 5.43. Only flip the playbook if spot breaches the 713.39 flip; until then, harvest.

What it means for your trading

Iron condor scores cleanest at 56 with 30-45 DTE wings outside 715.00/710.00; standard sizing, no jump-risk haircut while VVIX stays benign.

Actionable Summary

Trade: deploy Iron Condor at 30-45 DTE with wings placed outside the 715.00 call wall and 710.00 put wall. VRP stays active, VVIX prints Normal, and net GEX at $750.6M hands sellers the carry - standard sizing per Standard Size, no defensive scaling required.

Watch the 715 charm pivot as the intraday line; current bias reads Neutral and a break below flips dealer flow from absorbing to amplifying. Avoid naked short calls above 715.00 - the max-pain magnet at 700.00 works on the put side but turns hostile through the wall - and avoid chasing strength into that ceiling; fade with credit spreads instead.

Bias:Elevated / Watchful regime stacked on Unknown VRP, contango term structure (VIX9D 15.13 versus 3M 20.37), and Aligned cross-asset tape - mean-reversion playbook, not breakout. Only flip bearish on a clean breach of the 713.39 flip.

What it means for your trading

Harvest premium via Iron Condor structures inside the 710.00 - 715.00 dampening zone while the Elevated / Watchful regime and contango carry hold. Lose the playbook only on a decisive break of the 715 pivot or the 713.39 gamma flip.

Iran threatening 'painful response' to potential US escalation is the single biggest macro tail-risk variable in the chain right now - explains why VIX9D refuses to compress further despite calm tape.

Oil retreating from a four-year high after escalation jitters tells you the market is treating this as headline noise, not a sustained supply shock - risk-on tape persistence depends on this fade holding.

Bank of England flagging Iran-war inflation risks while holding rates is the central bank tell - DM rate-setters now explicitly link geopolitics to policy paralysis, shifting macro vol regime toward stagflation tail.

Khamenei's 'new management of Strait of Hormuz' framing is the ambiguous-de-escalation signal that lets equity vol price out near-term tail risk - direct read-through to today's VIX cooling.

Stagflation framing entering the third month means the regime narrative is shifting from acute shock to chronic drag - this is the slow-burn macro story that flattens VIX term structure if it sticks.

US military commanders briefing Trump on options against Iran is the binary headline that could re-bid VVIX in a single tick - keeps tail hedges relevant even with sleepy spot vol.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.43 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.39 against a spot of 715.17. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 13.19% with a volatility risk premium of 1.47%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.36. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime