Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

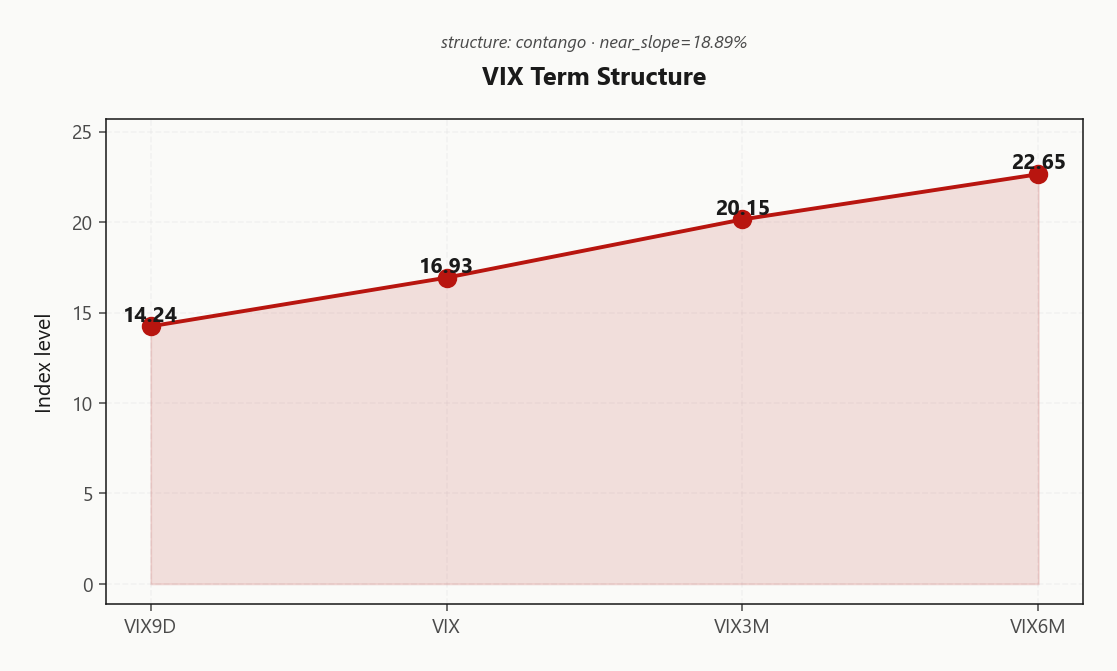

SPY at 719.06 closes in deep positive gamma with net GEX at $5.91B - dealers long gamma, mean-reversion regime intact. Call wall at 720.00 capped today's tape; put wall at 710.00 is the cushion; gamma flip at 713.53 sits well below spot, so the cushion is fat. Net VEX at -$244.7B means a vol pop forces dealers to sell delta - vanna is the asymmetric risk, not gamma. VIX collapsed to 16.93 (-9.99%%) and the term curve is Contango with VIX9D at 14.24 and 3M at 20.15 - vol sellers' carry is real. VRP at 0.96% confirms options modestly rich to realized. VVIX at 93.88 is normal, sizing stays standard. 0DTE is 85.4%% of total gamma - intraday will pin without a catalyst. Bottom line: sell Iron Condor structures in the 30-45 window between the walls; lose the bias only if spot breaks 713.53.

Positive gamma cushion holds across index complex with VIX easing into 16.93

SPY closes pinned just under the 720.00 call wall with dealers deeply long gamma and VIX collapsing to 16.93 on easing geopolitical premium. The forward curve is in steep contango with Steep contango - vol sellers favored, telling vol sellers their carry is paid - but VVIX/VIX ratio and a still-bid skew say the tail is not free. Trade the chop, harvest premium in the 30-45 window, and respect the 713.53 flip as the line where the regime breaks.

Regime Assessment

Regime classification prints Elevated / Watchful with VIX anchored at 16.93 - above the structural floor but with the term curve in Contango telling you the mean-revert path is the favored one. The transition matrix says probability of escalating to panic over the next handful of sessions sits at 0.05, while the path back to a low-vol regime over a two-week horizon runs 0.45 - asymmetric in favor of the carry trade.

Half-life is 15 sessions, roughly three trading weeks - sticky enough to plan structures around without flinching at every tape print. Cross-asset confirms: indices Aligned in positive gamma, MOVE at 74.33 quiet, Fear & Greed recovered to Greed. This is an equity-led relief, not a credit-led unwind.

The fragility is geopolitical, not technical. A Strait of Hormuz headline collapses the half-life to a single tape - keep spread protection on, lift hedges only if VIX bleeds below 14.24 without VVIX confirming.

What it means for your trading

Regime is Elevated with a half-life of 15 sessions - plan around the carry, but the gamma flip at 713.53 is the line where this thesis breaks.

Trading readVIX collapsing while VVIX holds and SKEW stays bid = the surface is telling you spot vol is gone but the vol-of-vol channel still embeds jump risk. Headline alignment, surface divergence - typical post-event pattern.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve is in Contango with VIX9D at 14.24 printing well below spot VIX at 16.93 - the ultra-near horizon has already bled its event premium and the front of the curve is openly discounting calm. Carry the read into the belly: VIX3M at 20.15 against VIX6M at 22.65 keeps the slope structurally steep, classified Steep Contango (Steep contango - vol sellers favored).

The implied forward sits at 21.5805769154, richer than spot - that is where the term-slope kink concentrates and where calendar sellers get paid for taking the roll-down. Sweet spot for premium harvest is the 30-45 window: short the front against longer-dated hedges, let theta and contango do the work.

Signal: Green. Carry is real and the curve says event premium has been extracted; the discipline is to sell the front the curve is giving away, not to chase the back.

What it means for your trading

Steep contango from 14.24 through 20.15 confirms the Steep Contango regime - front-month vol is the cheapest leg on the curve, and forward 21.5805769154 is the structural carry trade. Sell front, hedge belly.

Trading readSteep contango with front-month kink low - vol carry trade is paid both ways: short front, long belly. The slope says the market is no longer pricing imminent stress, but the long end staying elevated means term premium for tail risk is intact.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 12.84% sits modestly above HV20 at 11.88, leaving VRP at 0.96% - options are paid for risk, not gouging. The premium is real but not extreme; sellers get carry without the comfort of a fat cushion.

HV60 at 15.46 sits well above HV20 - realized has been decelerating, and the curve still embeds memory of last quarter's chop. That asymmetry is why naked short-vol structures remain mispriced for risk: the surface looks calm, the lookback does not.

Cross-section, QQQ VRP at 3.07% runs richer than SPY - single-name beta drag is the catch for harvesting it. IWM ATM IV at 20.33% with VRP at 3.58% is the cleanest harvest if the positive-gamma regime sticks; small-cap put skew makes defined-risk condors the right vehicle, not naked strangles.

What it means for your trading

VRP is alive across the index complex - modest in SPY at 0.96%, richer in QQQ at 3.07%, richest in IWM at 3.58% - but HV60 at 15.46 above HV20 at 11.88 says the curve still respects last quarter's tape. Sell premium with defined risk, lean into IWM for the cleanest harvest if the regime holds.

Skew Convexity

Front-week quarter-delta skew stays positively sloped: put 25d prints 13.8% bid over call 25d at 11.96%, with ATM anchored at 12.02%. Skew_25d at 1.84% and a smile ratio of 1.15% describe an ordered surface - protection bid, not panic-bid. The relief tape into the 720.00 call wall has not pulled the put wing in.

The call skew is inverted - call 25d trades under ATM, so no FOMO premium is priced for an upside breakout. That asymmetry matters: dealers long gamma cap rallies, and the surface refuses to pay you for a chase. Meanwhile SKEW at 141.88 says the tail is not cheap; with VVIX at 93.88 still bid against a collapsing 16.93 print, naked tail shorts are mispriced risk.

Trade the convexity, do not fade it: spread the put protection rather than ditch it, and finance call wings against the inverted upside. Iron condors clear the bid/offer cleanly between the 710.00 and 720.00; lift hedges only on a clean break of 713.53.

What it means for your trading

Skew at 1.84% with put 25d bid over call 25d says downside is paid for despite the rally - spread the hedge, do not sell it. SKEW index at 141.88 confirms the tail is structurally bid, so favor defined-risk condors over naked strangles.

Vol-of-Vol Structure

VVIX prints 93.88 against VIX at 16.93, putting the ratio at 5.55 - optically elevated, but that's the denominator collapsing, not the numerator screaming. The vol-of-vol channel reads Normal, signal Green, and that's the entire story: spot vol got crushed faster than jump-risk repriced, so the ratio drifts higher mechanically while the absolute VVIX print sits in its structural band.

Sizing guidance: Standard Size. No reason to flinch on the premium-sell book, no reason to lever it either - the surface is not telling you the tail is gone, it's telling you spot stress evaporated. Treat VVIX as the unconfirmed witness while VIX does the talking.

The tell to watch is divergence: if VIX bleeds below VIX9D at 14.24 without VVIX following lower, that's the green light to lift residual hedges and lean into the carry. VVIX rolling higher while VIX keeps grinding down is the opposite signal - jump-risk repricing under a calm tape, the cue to size down before the next headline finds the surface.

What it means for your trading

VVIX in the Normal band keeps sizing at Standard Size - the elevated VVIX/VIX ratio is a denominator artifact of VIX collapsing to 16.93, not a jump-risk warning. Watch for VVIX divergence as VIX probes below VIX9D at 14.24: confirmation lifts hedges, divergence is the cue to trim.

Dispersion Spread

Index VRP runs modest with SPY ATM IV at 12.84% while the tech basket carries the vol load - QQQ ATM IV at 18.45% and IWM at 20.33%. Correlation is moderate, not crashing, which means the dispersion premium between index and constituents is real but not extreme. The right harvest is selling index vol against held single-name exposure, not naked short vol on the components where idiosyncratic tails are still bid.

Cross-strike dispersion confirms the read: SPY skew is ordered at 1.84%, QQQ steeper at 2.83%, and IWM steepest at 2.94% - small-cap put protection remains the most bid wing in the complex. With QQQ VRP at 3.07% and IWM VRP at 3.58% running richer than SPY at 0.96%, the cleanest expression is SPX/SPY premium-selling - index carry pays without forcing single-name correlation risk into the book.

Preferred: sell index vol, lean long single-name gamma where idiosyncratic prints sit in window. Avoid naked short single-name strangles while constituent skew stays this firm.

What it means for your trading

Dispersion is moderate - single-name VRP runs richer than index VRP with IWM skew steepest, so harvest the spread by shorting index vol against long constituent exposure rather than fading single-name premium directly.

Liquidity & Microstructure

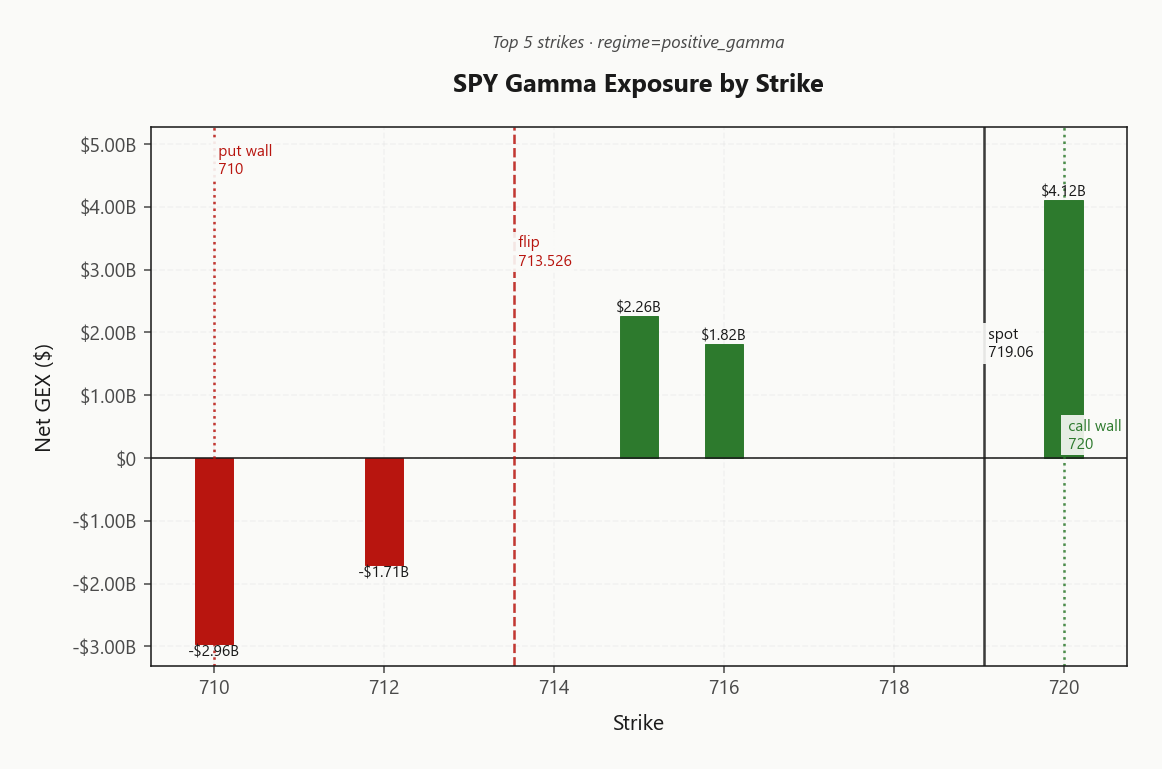

The book is stacked: dealer OI clusters at the 720.00 call wall - top-strike net GEX of $4.12B at 720.00 acts as a magnetic ceiling - with the 710.00 put wall framing the downside cushion. Spot at 719.06 sits comfortably above the gamma flip at 713.53, so dealer hedging vector is buy weakness, sell strength - the textbook mean-reversion fuel between the walls.

Highest OI parks at 700, exerting a max-pain pull lower if a pin develops late tape. With 0DTE absorbing 85.4% of total gamma, intraday is governed by hedging mechanics, not multi-day positioning - pin behavior dominates absent a fresh catalyst.

The flip at 713.53 is the regime line. Above it, dealer flow is your friend; through it, the vector inverts and amplification replaces dampening. Trade the chop between the walls; the only setup that breaks the structural carry is a flip break.

What it means for your trading

Dealers pinned long gamma between 710.00 and 720.00 with spot anchored well above the 713.53 flip - fade extremes, respect the flip as the line that flips the regime.

Trading readMassive call-wall concentration at 720.00 with the put-wall cushion at 710.00 = dealers dampen rallies and absorb dips between the walls. Trade the chop, fade extremes; only respect a break of the gamma flip as a regime change.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints at -$244.7B - deeply negative and the asymmetric tell of this regime. Gamma is the cushion, but vanna is the trapdoor: any vol pop forces dealers to sell delta into the move, accelerating rather than absorbing. The calm tape masks this; the surface does not.

Charm exposure at -$1.71B compounds the picture, pulling dealers to sell into expiry as time decay bleeds long-dated hedges. The pivot sits at 720 (Call Wall), with current bias Neutral and spot inside the friction zone at 0.1307262259 from the line.

Trade implication: the call wall is not just resistance, it is the inflection where dealer flow turns hostile. Stay short premium between the walls while spot holds below 720.00; above it, vanna and charm both cut against the long-gamma cushion and the mean-reversion edge evaporates fast.

What it means for your trading

Vanna is the asymmetric risk, not gamma - a vol shock at -$244.7B VEX forces dealer delta-selling that overwhelms the long-gamma cushion. Respect 720 as the line where charm and vanna flip from tailwind to accelerant.

Cross-Asset Confirmation

The index complex sits Aligned in positive gamma - SPY, QQQ at 667.82, and IWM at 278.30 all parked above their respective flips, with VIX in its own negative-gamma regime. That asymmetry is the cleanest tell available: equity dealers cushion, vol dealers accelerate. No regime divergence to lead a stress story, just one-sided relief.

MOVE at 74.33 seals the read - rates are quiet, no credit echo, no cross-asset confirmation of fragility. This is an equity-led relief tape, not a credit-led unwind. Fear & Greed has rotated to Greed at 67, the contrarian counter to a vol crush that already priced the de-escalation.

The fat-tailed catalyst is exogenous: a Hormuz headline is the only vector that flips the cross-asset alignment in one tape. Until then, trade the alignment, not against it - fade extremes between the walls and respect that VIX's negative-gamma posture means any upside surprise in spot vol gets amplified, not dampened.

What it means for your trading

Cross-asset alignment is clean and equity-led: indices in positive gamma, MOVE at 74.33 calm, sentiment recovered to Greed. The only break-the-regime catalyst is a geopolitical tape; structural carry pays until then.

Scenario EV

The scoreboard prints Iron Condor at 45, leading the put spread alternative at 33 - a clean win for two-sided premium harvest over directional structures. Moderate VRP at 0.96%, Contango term curve, and dealers parked deep in Positive Gamma with net GEX at $5.91B stack the carry the same direction. VRP read: Unknown; sizing per the vol-of-vol desk stays Standard Size.

Sweet spot is the 30-45 window - far enough out to skip 0DTE pin roulette, near enough to ride the term-curve kink between 14.24 front and 20.15 belly. Center the body between the 710.00 put wall and 720.00 call wall; let the dealer cushion do the work.

Kill switch is the gamma flip at 713.53 - break it and the carry trade flips to a momentum trade in one tape.

What it means for your trading

Iron condor is the scored winner at 45 on 30-45 DTE, structured between the walls with Standard Size. Lose the bias only on a clean break of 713.53.

Actionable Summary

Trade plan: sell premium between the walls. Put on Iron Condor structures centered between 710.00 and 720.00, sized in the 30-45 DTE window where the term-curve kink concentrates VRP harvest. Calendar bias engages while VIX9D at 14.24 stays pinned below spot VIX at 16.93 - short the front, hedge with the belly.

Risk discipline: avoid naked short strangles. VVIX at 93.88 remains bid relative to the VIX collapse, and skew_25d at 1.84% says the tail is not free - spread the protection rather than naked short the wing. Keep sizing at Standard Size.

Lines that matter: the gamma flip at 720 is where the regime breaks - lose the mean-reversion bias on a clean break. The Iran/Hormuz tape is the only catalyst that snaps the structural carry; current regime stamps as Elevated / Watchful.

Oil pulling back from a four-year high with US-Iran de-escalation chatter is the single biggest driver of today's vol crush - energy-led inflation tail premium is bleeding out of the curve.

Iran threatening retaliation if the US renews attacks keeps the geopolitical tail alive even as VIX collapses - the reason naked short vol still has asymmetric downside.

A pivotal US-Iran war deadline with no resolution is exactly the kind of binary catalyst that argues for keeping spread protection on instead of letting hedges roll off into the calm tape.

A US naval blockade on Iranian oil exports forcing crude into floating storage means physical disruption risk is real even with paper prices easing - energy vol stays bid in single names.

ECB on hold while explicitly flagging Iran-war inflation risk says central banks are not yet declaring victory - rate-vol (MOVE at 74.33) is calm but path-dependent.

Bank of England flagging Iran-war inflation risk in its hold decision corroborates the ECB tone - global rate path is hostage to Hormuz, which in turn keeps long-dated equity vol structurally bid.

Forecasters lifting prolonged-disruption oil price targets is the slow-burn supply-side risk that the curve has not fully priced - a future regime shift catalyst worth watching.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 16.89 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.53 against a spot of 719.06. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.84% with a volatility risk premium of 0.96%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 16.93. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime