Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

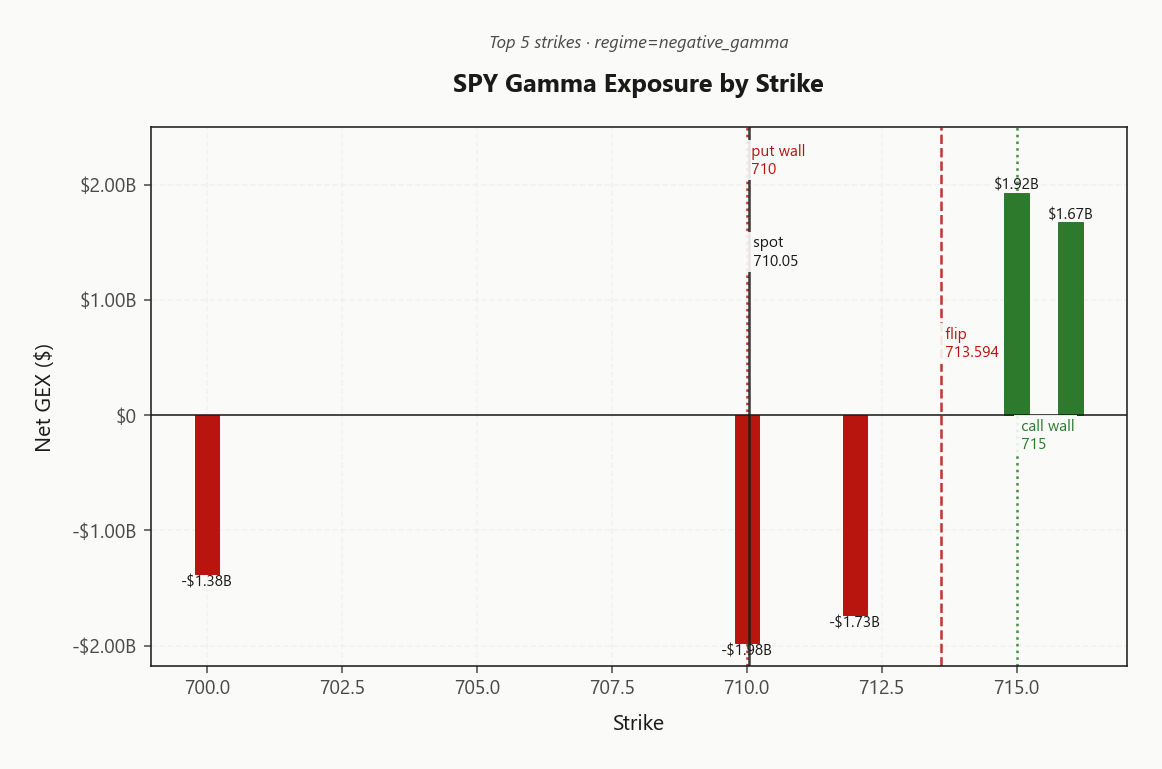

SPY at 710.05 in Negative Gamma regime with net GEX -$4.11B - dealers short gamma, moves get amplified into Fed/earnings tape. Key levels: gamma flip 713.59 sits as resistance, call wall 715.00 caps upside, put wall 710.00 is exactly where spot sits - pinned at the breakdown line. Dealer vanna -$175.56B and charm -$908.1M are both negative - vol up = more selling, time decay pressures dealers to lean offered into close. VIX at 18.17 with term structure Contango (VIX9D 16.69 < VIX3M 20.49), VRP 4.3% keeps options rich to 11.91 HV20. Bottom line: above 713.59 we mean-revert toward call wall; below 710.00 dealer selling accelerates toward 699.00 - trade the break, don't pre-position into FOMC.

SPY pinned at put wall 710.00 in negative gamma - dealers amplify, Iran/Fed/mag7 tape risk live

Index complex sits in unanimous negative gamma with SPY hugging its put wall at 710.00 and gamma flip just overhead at 713.59 - any break opens accelerant flow into a Fed decision and four mag-7 prints tonight. VIX term structure remains in steep contango with VVIX/VIX ratio at 5.01, telling us vol sellers still get paid but the tape is fragile around catalysts. Iron condor is the EV-recommended structure but size half until VVIX confirms the calm.

Regime Assessment

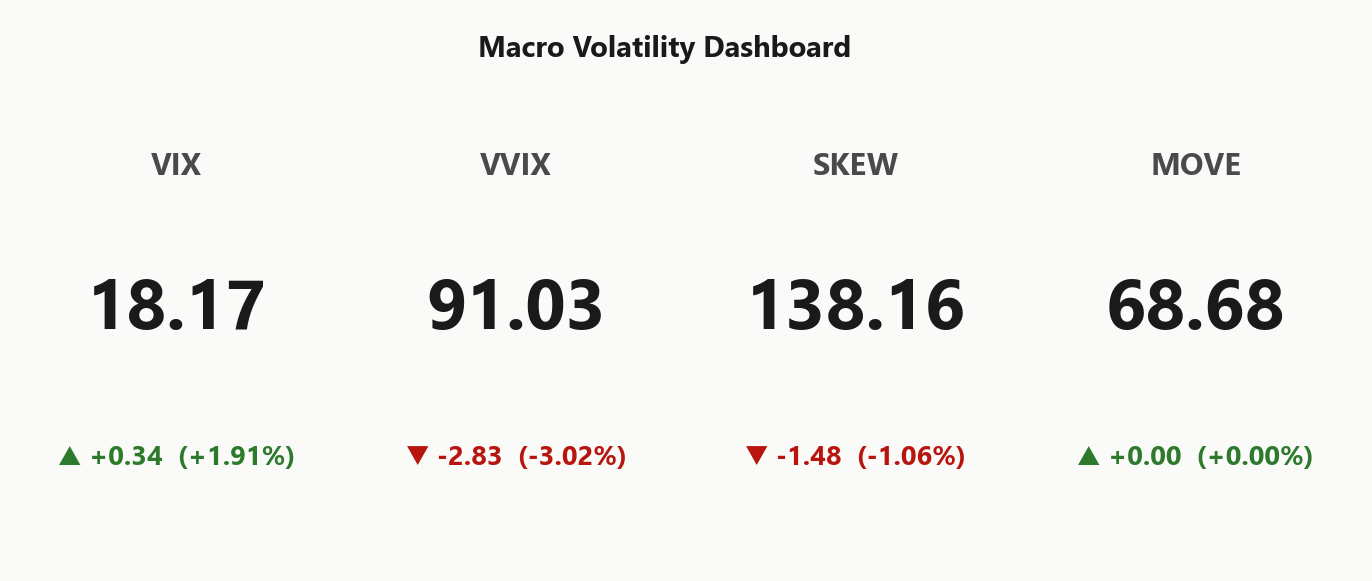

Volatility regime reads Elevated / Watchful - VIX at 18.17 sits squarely mid-range, neither the complacent floor nor the panic shoulder. This is the Elevated bucket: bid enough to pay vol sellers, calm enough that tail hedges still print as insurance rather than performance.

Half-life of 15 sessions tells us the regime is sticky - extremes get faded, mean reversion in vol space is the base case. But the transition matrix is honest about the catalyst: probability of slipping to panic inside five sessions is 0.05 - small, manageable, but non-zero ahead of a binary Fed-plus-mag7 night. The dovish-Fed counterfactual is the bigger tail: probability of drifting to low inside ten sessions sits at 0.45, the cleanest unwind path if the catalyst stack resolves benign.

Plan trades for the regime that exists, not the one you wish it was. Elevated-but-stable means iron condors get paid, fade vol spikes that don't have catalyst behind them, and keep tail hedges sized for the panic transition rather than the modal path.

What it means for your trading

Regime is Elevated / Watchful with VIX at 18.17 and a 15-session half-life - sticky enough to fade extremes, but the 0.05 five-session panic probability says respect the Fed/earnings tape.

Trading readVIX bid, VVIX subdued, SKEW elevated, MOVE flat - equity tail premium without rates panic. This says equity-specific event risk, not macro contagion. Confirmation across the panel, not divergence.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

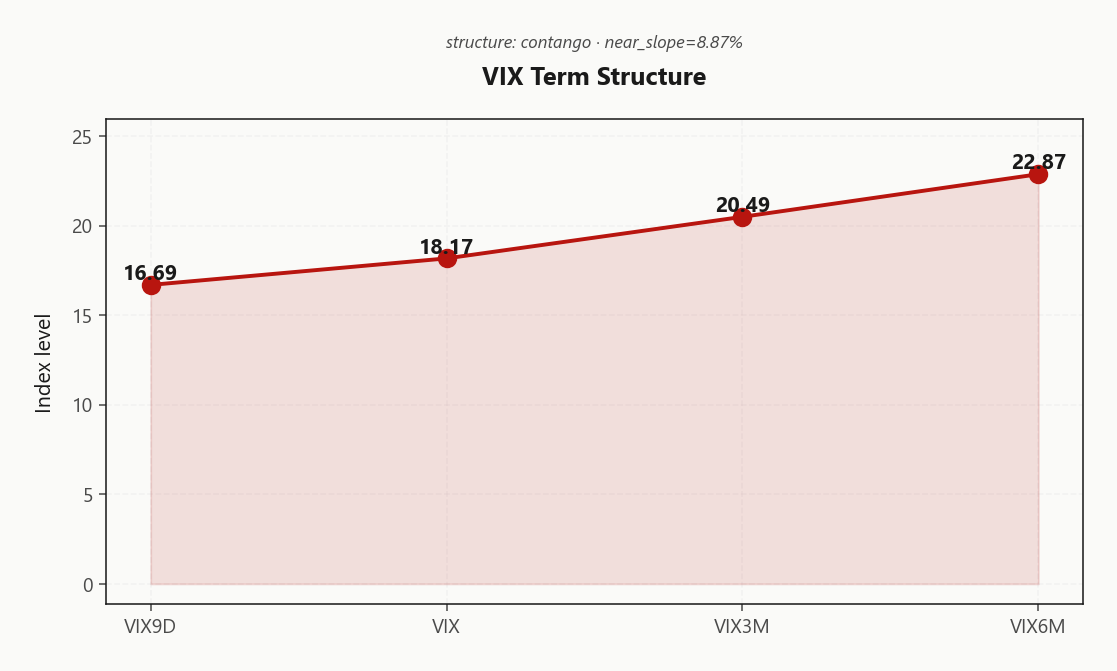

The VIX curve prints textbook Contango with VIX9D at 16.69 sitting under spot VIX 18.17, then stepping up through VIX3M 20.49 to VIX6M 22.87 - near slope 8.87%% confirms the curve hasn't been flattened by tonight's catalyst stack. Forward vol regime tags Steep Contango: vol sellers' carry is structurally green and the roll-down compounds.

Front-month VIX future basis at 12.77%% keeps futures sellers paid, but the forward 30-60 to 60-90 step from 21.5565697642 to 25.0246618359 is the visible event hump - Fed plus four mag-7 prints already priced into the front. The cleanest carry sits in the 30-45 DTE bucket, far enough from tonight's binary to dodge gap risk while still riding the contango decay.

Trading readContango stays intact with VIX9D below VIX below VIX3M - the carry trade is alive, but the front is paying for tonight; sell vol in the 30-45 DTE bucket, not the front week.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 16.21% sits comfortably above HV20 of 11.91 and HV60 of 15.46 - options are rich to recent realized, and VRP at 4.3% keeps premium sellers structurally paid. But the gap between IV and HV60 is tighter than the IV/HV20 spread, which tells you realized has been quietly catching up over the longer window even as the front end stays bid for tonight's binary tape.

The premium here is not a free lunch - it is compensation for the Fed plus four mega-cap prints stacked into a single session. Front-week IV is paying for gap risk, not carry. Selling that wing naked is paying you to absorb someone else's hedge cost into a binary outcome.

The structural edge sits on the back end, where realized lags the implied curve and the catalyst premium does not dominate the print. 30-45 DTE is where VRP harvest works without owning tonight's gap - and the EV engine concurs with a Iron Condor tilt at score 52. Avoid front-week short vol; let the catalyst clear, then sell into the post-event IV crush.

What it means for your trading

IV at 16.21% vs HV20 11.91 says vol sellers are paid, but VRP of 4.3% is compensation for tonight's gap risk - harvest the back end at 30-45 DTE, not the front.

Skew Convexity

The quarter-delta skew is screaming hedge demand into the binary night: put IV at 26.03% trades a clean premium to ATM 24.07% while the call wing prints 21.82% - flat, uninspired, and telling you nobody is paying up for upside even with four mega-cap tapes tonight. Skew differential at 4.21% on the front expiry concentrates the entire event premium into the downside wing.

Smile ratio at 1.19% sits comfortably above one - this is ordered protection-buying, not capitulation. SKEW index 138.16 confirms the tail bid is structural, not a one-print anomaly. Traders are paying for the left tail; nobody is reaching for the right.

The trade write itself: with the put wing this rich, naked short puts are a tax. Sell the skew through put spreads - finance the long leg with the over-bid wing, cap the convexity, and let the smile compress post-Fed do the work.

What it means for your trading

Front-expiry skew differential 4.21% with smile ratio 1.19% and SKEW 138.16 confirms ordered downside hedging - sell the put wing via spreads, never naked, into FOMC plus mag-7 prints.

Vol-of-Vol Structure

VVIX prints 91.03 against VIX at 18.17 - vol-of-vol sits in the Normal zone with the ratio at 5.01. Translation: the options market is not pricing a bimodal jump outcome into the Fed plus four mag-7 prints. If panic were genuinely loaded, VVIX would be testing triple digits with the ratio blowing out - instead it's quiet under the catalyst stack.

That's the contrarian tell. With skew steep but vol-of-vol calm, this is ordered hedging, not chaos - sizing guidance reads Standard Size, meaning premium sellers carry full clip on iron condors rather than the half-size derate you'd run if the jump component were lit. Calm VVIX with bid skew is the cleanest green light the vol-seller gets ahead of binary tape.

The watch level is post-Fed VVIX. A break through the triple-digit handle flips the regime read - at that point cut size, layer tail protection, and respect that the jump distribution just repriced. Until then, trade what's printed: Normal vol-of-vol means the catalyst is priced as a move, not a shock.

What it means for your trading

VVIX/VIX at 5.01 in the Normal zone says no jump panic is priced - run Standard Size on premium structures, but flip defensive if VVIX breaks the triple-digit handle post-Fed.

Dispersion Spread

Dispersion sits fat into tonight's quad-print. SPY ATM IV at 16.21% looks tame next to the single-name event vols stacked in NVDA/MSFT/META/AMZN - index hedges are structurally underpricing the idiosyncratic earnings dispersion the tape is about to absorb. Cross-strike IV dispersion at 73.97 captures the skew-driven spread; cross-expiry at 2.16 confirms the front carries the event hump.

The trade is sell index vol, leave single-names alone. Short SPY/QQQ premium harvests the correlation collapse that mechanically follows when four mega-caps print idiosyncratic gaps - index realized compresses while names diverge. Naked short straddles on the reporters tonight is the inverse trade: you're short the dispersion you should be harvesting passively through the index.

Timing is the discipline. Dispersion harvest works after the catalyst, not before - sell the index vol crush in the post-print session, not into it. Cross-asset regime reads Aligned, which means the complex moves together until the names diverge tomorrow morning.

What it means for your trading

Index vol at 16.21% trades cheap to the single-name event premium loaded into tonight's mag-7 prints - sell SPY/QQQ vol post-catalyst as correlation compresses, not single-name straddles into the print.

Liquidity & Microstructure

The book is a single-level binary today: spot is camped on the put wall at 710.00, with the gamma flip just overhead at 713.59 and the call wall stacked at 715.00. Top GEX strike 710.00 prints net -$1.98B - that's the pin, and it sits exactly where price is trading.

Highest OI strike 700 sits below as a gravity well: lose the wall and dealer hedging compounds toward it. Reclaim the flip and the regime inverts - short-gamma amplification flips to supportive flow, capping any rip into the call wall on a dovish Fed surprise. Until one side breaks, expect chop into resolution.

Microstructure caveat: 0DTE accounts for 47% of total gamma - intraday whip risk dominates, and the post-2pm tape rewrites the surface. Trade the breach of 713.59 or 710.00, don't fade either side pre-print.

What it means for your trading

Spot pinned at 710.00 with the flip overhead at 713.59 - single-level binary tape where break direction dictates whether dealers dampen or amplify.

Trading readSpot is camped at the put wall with the call wall just overhead - dealers amplify any directional break, so trade the breach not the chop. Above gamma flip, mean-reversion wins; below put wall, cascade activates.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order Greeks are stacked hostile into the catalyst tape. Net VEX prints -$175.56B - deeply negative - meaning any vol spike forces the desk to dump delta, not absorb it. CHEX at -$908.1M compounds the problem: charm bleeds dealers offered into the cash close, so late-day flow leans seller mechanically, regardless of fundamental tape.

The pivot sits at 710 - the put wall doubling as the dealer-flow flip point. Current bias reads Neutral despite spot camped at the wall, distance -0.0070417576. That is a knife-edge, not a stable equilibrium. Above the pivot, vanna and charm pressure ease and dealers drift toward the call wall at 715.00; below it, the same Greeks weaponize against spot.

The trip-wire is straightforward: VIX breaking 18.17's shelf with spot under 710 activates the cascade - vol-up forces vanna selling, charm extends it into close. Trade the break of the pivot; do not pre-position into a hostile second-order book.

What it means for your trading

Vanna and charm both lean against dealers - VEX -$175.56B and CHEX -$908.1M turn any vol bid or time decay into mechanical selling. The 710 pivot is THE line; bias flips and so does dealer flow direction.

Cross-Asset Confirmation

Cross-asset tape reads Unknown - confirmation, not divergence. MOVE at 68.68 sits flat while VIX prints 18.17 bid: rates desks aren't pricing crisis, equity desks are paying up for tonight's binary. That bifurcation is the tell - this is an isolated equity event setup around Fed plus four mag-7 prints, not a macro cascade bleeding from credit or duration.

QQQ at 657.98 and IWM at 272.95 both sit in negative gamma alongside SPY - index complex regime is Aligned, no rotation hedge available. When fragility synchronizes this cleanly into a catalyst, the eventual break trends rather than chops. Layer on Iran/Hormuz keeping crude bid and you get an oil-up tax on multiples stacked over the rates decision.

Sentiment delivers the contrarian capstone: Fear & Greed reads 63 - Greed - with spot pinned at the put wall. Complacency into a binary night means downside surprise carries more juice than the upside.

What it means for your trading

Cross-asset panel confirms equity-specific event premium without macro contagion: MOVE flat, VIX bid, index complex Aligned in negative gamma, sentiment at Greed. Trade the equity catalyst, not a cross-asset rotation.

Scenario EV

Derived EV ranks Iron Condor top of the book at score 52, with the put spread trailing at 46 as the directional kicker. The setup is textbook premium-harvest: VRP 4.3% versus HV20 11.91, term structure in Contango, and VVIX/VIX ratio 5.01 sitting in the normal band - sizing guidance reads Standard Size, no half-size derate.

Optimal expiry sits in 30-45 DTE - far enough out to dodge tonight's binary gap, close enough to compound roll-down before the event hump in forward vol decays. Strangle wings work cleanly inside call wall 715.00 and put wall 710.00; the front week is a no-fly zone with skew 4.21% bidding the put wing into the print stack.

If you must lean directional, put spreads at score 46 exploit steep skew without naked vanna exposure - debit cheap relative to outright puts, defined risk into Elevated / Watchful. VRP read Unknown, but contango carry plus normal vol-of-vol does the heavy lifting either way.

What it means for your trading

Iron condor in 30-45 DTE is the EV-recommended trade - sell wings inside 715.00 and 710.00 at standard size; put spread at score 46 is the runner-up tactical lean.

Actionable Summary

Trade structure: derived EV scores Iron Condor as the optimal vehicle in 30-45 DTE - sell strangles inside the call wall at 715.00 and put wall at 710.00, harvesting contango carry while sidestepping tonight's catalyst gap. Layer a long put spread as tactical hedge: skew is steep enough that debit financing beats outright puts.

Avoid: naked short puts into FOMC plus four mega-cap prints - net VEX at -$175.56B means vanna amplifies any vol spike against you. Equally, do not pre-position above 715.00; call skew is flat, the tape is not pricing upside conviction even with mag-7 reporting.

Watch the lines: gamma flip 713.59 is the dealer-flow pivot - break above and fade strength as dealers turn supportive into the wall. Put wall 710.00 is the cascade trigger with pivot at 710 - break below and dealer selling compounds toward 699.00. Regime reads Elevated / Watchful: trade the break, do not catch the knife.

Iran/blockade headlines keep oil bid, layering an inflation/multiples tax on top of tonight's Fed decision - geopolitical premium plus rates uncertainty is exactly why front-week skew stays steep.

Mag-7 prints (Alphabet/Amazon/Meta/Microsoft) plus Fed - single biggest event-cluster of the quarter for index dealer flow, four idiosyncratic vol crushes around one macro catalyst.

US sanctions escalation against China-based oil shipper signals the Iran crackdown is spilling into US-China trade vector - second-order risk for QQQ semiconductor names.

Gold extending decline into Fed meeting tells us the rates market is pricing 'higher for longer' more than 'cuts coming' - bearish duration tilt for growth multiples.

Hormuz disruption outweighing OPEC supply news in oil pricing - confirms the geopolitical premium is the dominant macro driver, not supply/demand.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.36 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.59 against a spot of 710.05. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.21% with a volatility risk premium of 4.3%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.17. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime