Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

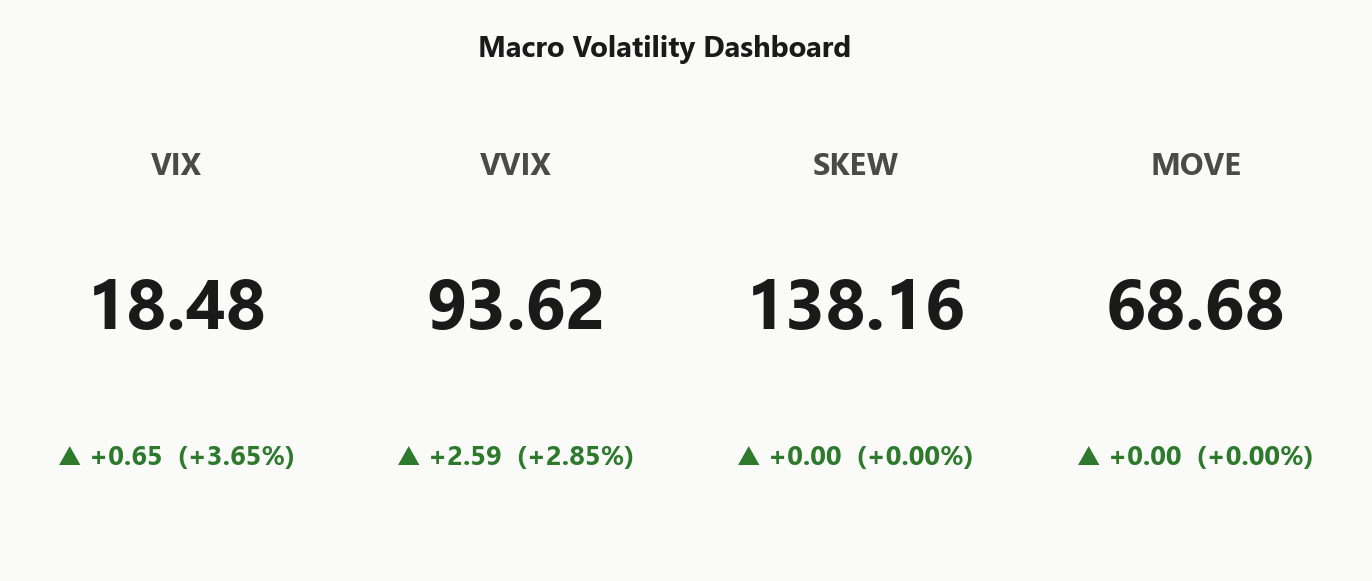

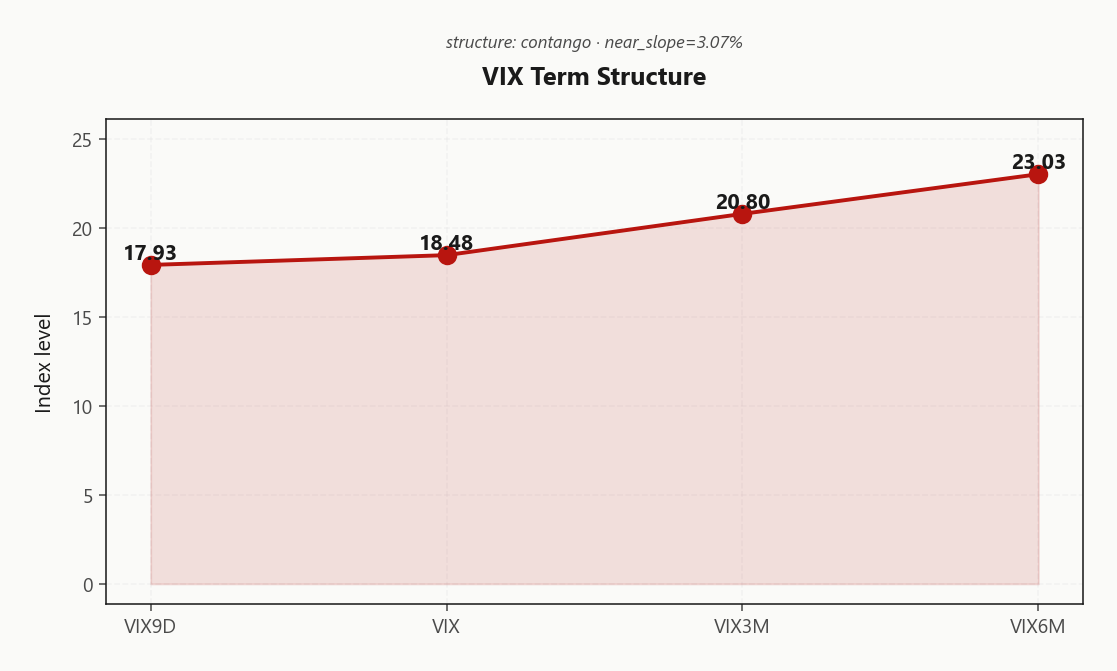

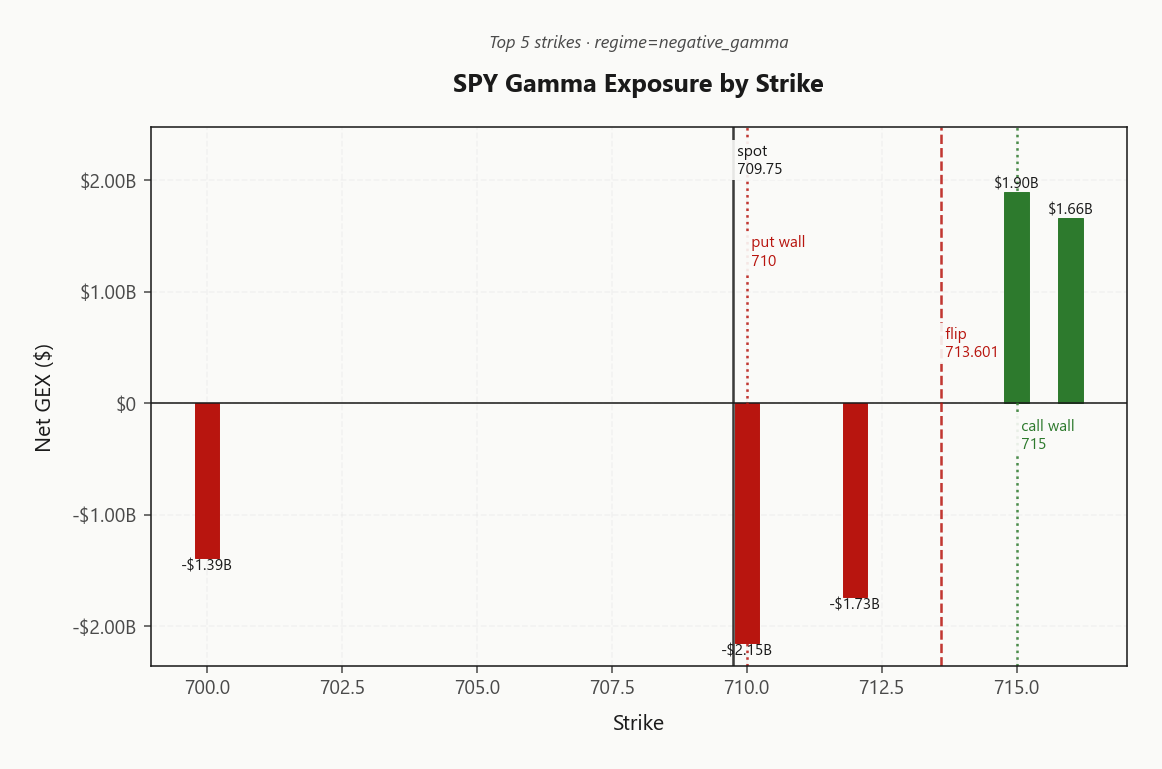

SPY at 709.75, regime is Negative Gamma with net GEX at -$4.68B - dealers short, moves amplified rather than dampened. Key levels: call wall 715.00, put wall 710.00, gamma flip 713.60; spot is sitting just under the flip, which means a downside break gets reinforced by dealer selling. Dealer positioning is hostile - net VEX at -$172.38B means a vol pop forces more delta selling, charm at -$907.9M adds late-day pressure. Vol read: VIX 18.48 (3.65%% on the day), term structure in Contango with VIX9D 17.93 under VIX3M 20.80, VRP at 4.8% so options remain rich to 20d realized of 11.95. VVIX at 93.62 is normal - no extreme jump pricing, but it's lifting alongside vol. 0DTE accounts for 48.3%% of SPY's gamma so intraday whipsaw risk is heavy through the FOMC window. Bottom line: respect 710.00 as the trigger - above it, fade strength to 715.00; below it, dealer flow accelerates the move and you stand aside until VIX prints back inside its term curve.

Negative gamma across index complex with VIX at 18.48, dealers short - moves amplified into tech earnings and FOMC

SPY at 709.75 sits below gamma flip 713.60 with dealers short gamma - moves get amplified, not dampened, into tonight's Mag7 earnings cluster and the FOMC decision. VIX term structure remains in contango at 3.07%% slope, VVIX normal at 93.62, so the carry trade still works but tail risk is rising on the Iran/oil overhang. Cross-asset alignment intact (Unknown); the single tape level that flips dealer flow is the 710.00 put wall.

Regime Assessment

Regime classification reads Elevated / Watchful with VIX anchored at 18.48 - not stress, but a level where protection premium is justified rather than wasted. The transition matrix puts probability of escalation to panic over five sessions at 0.05: low in absolute terms, but non-trivial with FOMC and the Mag7 cluster stacked on the same tape.

Half-life of 15 sessions tells you this print is stickier than recent bouts - don't expect instant mean-reversion off a single benign data point. Probability of decay back to low over ten sessions sits at 0.45, so the base case remains drift lower in vol, not escalation. That asymmetry is what keeps the carry trade viable while the regime is yellow.

FOMC tonight is the binary that resolves the path. A calm read collapses front-end IV onto the contango curve and accelerates the decay timeline; a hawkish surprise spikes the panic-transition probability and re-prices the half-life shorter. Trade the regime you have - Elevated / Watchful, sticky, defined-risk - not the one you fear.

What it means for your trading

Regime is Elevated / Watchful at VIX 18.48 with a 15-session half-life - sticky but decay-biased, with FOMC the binary that resolves direction.

Trading readVIX up, VVIX up, MOVE flat, SKEW elevated - equity vol is rising on its own without rates contagion. That's an isolated equity event, not a credit/macro shock; mean-reversion-friendly setup if FOMC is benign.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve sits in Contango with VIX9D at 17.93 printing under VIX 18.48 and VIX3M at 20.80 - a clean, ordered term structure that says the tape isn't pricing a near-term event spike despite FOMC tonight. The derived label reads Steep Contango, which keeps the short-vol carry trade firmly in the favored column.

Forward vol from 21.8678942745 through 25.062358229 implies the curve is pricing a post-FOMC drift, not a shock - the back-end isn't pulling the front, the front is decaying into the back. That's the textbook roll-down setup, and it's where the edge lives.

Trade the geometry where it pays: 30-45 DTE captures real roll-down past the FOMC and Mag7 prints without paying the gamma tax of front-week paper. Avoid 0-7 DTE shorts outright - with spot sub-flip at 713.60, gamma cost is punitive and the curve isn't compensating you for it.

What it means for your trading

Term structure is Steep Contango with VIX9D 17.93 under VIX3M 20.80, so short-vol carry stays favored - but harvest it at 30-45 DTE, not the front week.

Trading readContango with shallow front-end slope says the market expects vol to drift back down post-FOMC, not spike. That's the carry signal - but the slope is shallow enough that one bad print flips it to backwardation fast.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 16.75% sits well clear of 20-day realized at 11.96, and the 5-day print at 8.31 shows tape behavior is cooling, not accelerating. VRP at 4.8% is firmly active - the IV-RV spread carries a Moderate Premium assessment, which is the cleanest read we get on options being genuinely rich versus what the underlying is actually delivering.

Hedgers are paying up for protection into the FOMC and the Mag7 cluster, but the realized leg hasn't caught up. That's the short-vol thesis in one line: you're being paid handsomely to take the other side, and the decay window past tonight's binaries is exactly where premium harvest lives. Don't conflate a FOMC-day IV pop with sustained realized - fade the spike if the print is benign and let mean-reversion do the work.

What it means for your trading

VRP at 4.8% with realized cooling toward 8.31 keeps the short-vol carry intact through the event window. Treat any IV expansion tonight as harvestable, not a regime break, until realized actually accelerates.

Skew Convexity

Quarter-delta skew prints 3.86% on the front expiry with put-25d IV at 26.61% bid heavy against ATM 24.86%, while call-25d sits at 22.75% - flat-to-inverted versus the body. This is ordered event hedging into the FOMC + Mag7 cluster, not capitulation: the wing is paying for itself, but it's paying.

Smile ratio at 1.17% sits firmly above unity, confirming downside is the only side carrying real premium. The flat call wing tells you there's no upside conviction in the tape - fade rallies into 715.00 by selling calls outright; on the protection side, structure put spreads rather than naked puts since you're financing the long leg with a wing the market is already overpaying for.

Trigger to watch: left-tail steepening accelerating through the FOMC window. If put-25d pulls further away from 24.86% while calls stay pinned, that's the panic-mode flip - exit short premium and reassess.

What it means for your trading

Skew is steep but ordered - sell calls into strength, buy put spreads not naked puts, and watch for left-tail acceleration past 3.86% as the panic trigger.

Vol-of-Vol Structure

VVIX prints 93.62 against VIX 18.48, a ratio of 5.07 that sits squarely inside the standard band. The level reads Normal - no bimodal jump premium baked into vol-of-vol, no fat tail being repriced ahead of the FOMC binary. Sizing guidance comes back Standard Size, which means full clip on iron condors rather than the half-size discipline a stressed VVIX would force.

That said, VVIX lifting 2.85% on the session alongside VIX 3.65% tells you nerves are building underneath the calm headline read - the cushion is intact but thinning into Mag7 prints and the Fed. The trade is to deploy now while the vol-of-vol surface is still pricing orderly, not panicked, distributions.

Re-check post-FOMC: a VVIX break through 110 flips the regime, kills standard sizing, and forces condors down to half-clip or out entirely. Until then, vol-of-vol is a green light, not a red one.

What it means for your trading

Vol-of-vol reads Normal with VVIX 93.62 and a VVIX/VIX ratio of 5.07 - full-size iron condors are sanctioned, but a post-FOMC VVIX breach of 110 invalidates the call.

Dispersion Spread

Index vol is trading cheap to the components: SPY ATM IV at 16.75% sits well under QQQ at 23.57% and IWM at 23.79%. That's a textbook earnings-week dispersion footprint - single-name premium is bid harder than the basket because Mag7 idiosyncratic risk doesn't net out at the index level.

Cross-expiry dispersion of 2.22 concentrates the event premium in the Apr 30 / May 01 tenors, while cross-strike dispersion of 66.61 confirms the bid is idiosyncratic, not systemic. The SPY-QQQ vol spread is wide enough to favor the SPY iron condor over QQQ - same regime read, cleaner premium decay, less single-name tail.

Trade implication: sell the index, not the names. Avoid naked short premium on NVDA, META, AMZN, GOOGL into print - the wing is paying for a reason. SPY hedges won't fully cover Mag7 idio gaps; if you must short single-name vol, define it.

What it means for your trading

SPY ATM IV at 16.75% trading well below QQQ 23.57% and IWM 23.79% says the premium is in the components, not the index - sell the SPY condor, leave the single names alone.

Liquidity & Microstructure

Open interest stacks hard at 700 with the heaviest single-strike net GEX print of -$2.15B sitting at 710.00 - a put-heavy magnet that pulls flow on any test. Spot is trading below the gamma flip at 713.60, which is the line that flips dealer behavior from supportive to amplifying. Above it, hedging buys dips; below it, hedging sells them.

The book is bracketed by the call wall at 715.00 capping rallies and the put wall at 710.00 functioning as the trapdoor - a clean break of the put wall hands control to dealer sell programs and accelerates the move. P/C OI ratio at 2.193 confirms the hedger lean is protective and skewed downside, not directional chase.

Trade the levels, not the narrative: fade strength into 715.00, respect 710.00 as the bias trigger, and stand aside on a clean break.

What it means for your trading

Spot below 713.60 with concentrated put-heavy OI at 700 means dealer flow is the dominant variable - 710.00 is the single level that inverts the regime.

Trading readNegative gamma below 713.60 means dealers sell into weakness - the put wall 710.00 is the trapdoor, and the cluster at 700 is where flow accelerates if breached. Above the flip, the call wall 715.00 caps rallies.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$172.38B - deeply negative - which means any vol pop forces dealers to sell more delta, not buy it. Vanna stops being a damper and starts being an accelerant: VIX up, dealer delta down, spot down, repeat. Into a binary FOMC plus the Mag7 quad-print, that's the feedback loop traders need to respect.

Charm reinforces the same direction. Net CHEX at -$907.9M means time-decay flow leans dealers shorter into the bell - afternoon weakness gets amplified rather than pinned. The charm pivot sits at 710 with current bias Neutral; reclaim it and the late-day drag eases, lose it and the close gets ugly.

Asymmetry is the trade. A calm Powell + in-line Mag7 = vanna unwind = relief rally that runs further than fundamentals justify. A hawkish surprise or one bad capex print = waterfall, because there's no positive greek anywhere in the book to lean against. Stay defined-risk through the binary.

What it means for your trading

Vanna and charm are aligned negative - dealers are positioned to amplify whichever way the FOMC/Mag7 binary breaks, with 710 as the line that flips intraday bias.

Cross-Asset Confirmation

MOVE at 68.68 sits subdued - this is not a credit or rates shock bleeding into equities. The selloff is contained to the equity-tech complex around tonight's Mag7 cluster and the FOMC, with no rates contagion to amplify it. Fear & Greed printing 64 (Greed) confirms there is no panic underneath the tape - sentiment hasn't priced disappointment, which leaves room to drop if guidance or the dot plot disappoints.

Across the index complex, QQQ at 658.46 and IWM at 271.27 both sit in negative-gamma regime alongside SPY - no divergence to exploit (Aligned, regime-diverged: False). When all three move together, dealer flow becomes the dominant variable, not relative value. Trade the index as a single coordinated book; cross-hedges between SPY/QQQ/IWM offer no edge here.

What it means for your trading

Subdued 68.68 MOVE plus aligned negative-gamma across SPY/QQQ/IWM (Aligned) confirms an isolated equity-event setup - Greed at 64 means downside asymmetry is real if the binary disappoints.

Scenario EV

The scenario engine flags Iron Condor as the preferred structure at score 57, with the optimal tenor parked in the 30-45 DTE band. That window threads the needle: it sits past tonight's FOMC and the Mag7 vol crush, harvesting roll-down without inheriting front-week gamma risk while spot trades sub-flip at 713.60.

Defined-risk wins over strangles here - VVIX at 93.62 is lifting on the day and the iron condor caps the tail if vanna feedback compounds a hawkish surprise. VRP read of Unknown against ATM IV at 16.75% versus 20-day realized of 11.95 still supports premium sale, and VVIX flagged Normal keeps sizing at Standard Size.

Structure the wings off the dealer map: short call into the 715.00 cap, short put adjacent to the 710.00 trapdoor. Pull the trade if VVIX breaches its event threshold or VIX9D inverts above VIX3M - that flips the regime and kills the carry.

Bottom line: stay defined-risk, fade vol pops, and respect 710.00 as the bias trigger. With SPY at 709.75 sitting under the 713.60 flip and net GEX at -$4.68B, dealers are short and downside breaks compound rather than dampen into tonight's Mag7 quad-print and FOMC.

The trade is Iron Condor at 30-45 DTE, wings pinned to the 715.00 call wall and just inside the put wall - VRP at 4.8% versus 20d realized of 11.95 says options stay rich, and VVIX at 93.62 keeps sizing standard. Watch 710 as the line; below it, stand aside and let dealer flow finish the move.

Avoid front-week premium sale, naked Mag7 short vol, and outright puts - the wing is paid, use spreads. Regime reads Elevated / Watchful: sticky, not panic, carry intact. Exit triggers are clean - VVIX through the jump-pricing threshold or VIX9D crossing above VIX3M flips the curve and the regime with it.

What it means for your trading

Sell defined-risk index premium at 30-45 DTE while VRP at 4.8% pays and VVIX at 93.62 holds normal; 710 is the stand-aside line and a flip to backwardation is the regime-break exit.

Mag7 quad-earnings cluster tonight (GOOGL/AMZN/META/MSFT) plus FOMC is THE binary event for the index complex - explains the negative-gamma pin and bid skew.

Fresh sanctions on 35 entities aiding Iran sanctions evasion = continued geopolitical premium in vol; tail-hedge demand stays bid.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.67 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.60 against a spot of 709.75. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.75% with a volatility risk premium of 4.8%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.48. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime