Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY closes at 708.21 sitting above its gamma flip at 684.07 - net GEX -$5.85B keeps the index in Positive Gamma territory and dampens close-to-close range. Call wall 715.00 caps strength while put wall 710.00 is the proximate magnet - pin risk into Friday is real with the charm pivot at 710. Dealer vanna sits at -$161.51B - a vol uptick translates into delta selling, so the cushion is conditional on VIX not breaking out. VIX at 18.78 with the term structure Contango (6.81%% near slope) and VVIX/VIX ratio at 5.20 flags carry-rich but not complacent. VRP at 4.36% keeps short premium structurally paid, and Iron Condor scores best at the 30-45 bucket. QQQ and IWM both sit Negative Gamma below their flips - that's where the day's break would come from if it comes, not from SPY. Bottom line: sell premium in SPX/SPY iron condors around the call/put walls, but size with VVIX in mind and avoid naked QQQ/IWM upside chase.

SPY positive gamma cushion vs QQQ/IWM short-gamma fragility - index complex split

SPY closes above its gamma flip in Positive Gamma territory while QQQ and IWM remain Negative Gamma - a classic divergence where cap-weight stability masks small-cap and tech fragility. VIX term structure stays in Steep Contango with VVIX at Normal levels, leaving carry trades intact but the tail quietly bid on Iran headlines. Recommended structure scores into Iron Condor at the 30-45 sweet spot.

Regime Assessment

Regime classification lands at Elevated / Watchful with VIX printing 18.36 - sticky enough to keep premium structurally bid, not panicky enough to force defensive sizing. The Elevated bucket is where carry trades earn their keep, but the half-life of 15 sessions is the operative number: this isn't a one-day vol pop that mean-reverts by Monday, it's a moderately persistent state that demands you trade the regime, not against it.

Transition probabilities anchor the read. Move-to-panic in five sessions sits at 0.05 - small enough that paying up for crash convexity is a bad trade, large enough that naked short-vol on the wings is reckless. Move-to-low in ten sessions at 0.45 is the constructive scenario and explains why the Steep Contango term structure is paid: forward sellers are positioned for that drift lower.

Signal color Yellow - proceed, but with the regime's stickiness priced into duration. The trade is Iron Condor at 30-45 DTE, sized for Standard Size, and respect the SPY/QQQ regime split - the cushion is real on the cap-weight, fragile everywhere else.

What it means for your trading

Elevated-but-watchful regime with a 15-session half-life - premium-selling carry is structural, not opportunistic, and panic-transition odds at 0.05 keep tail hedges expensive relative to expected payoff.

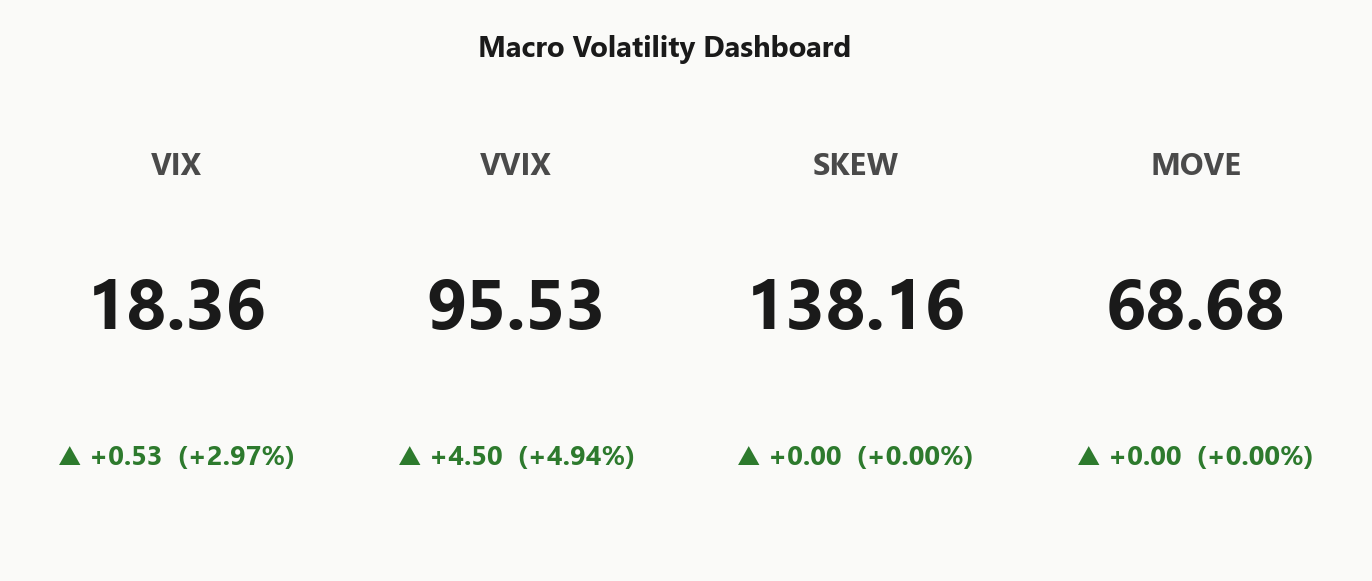

Trading readVIX up modestly, VVIX confirming the uptick, SKEW elevated, MOVE quiet - equity-vol divergence from bond-vol is consistent with a geopolitical-not-systemic read. Watch MOVE for the regime change tell.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

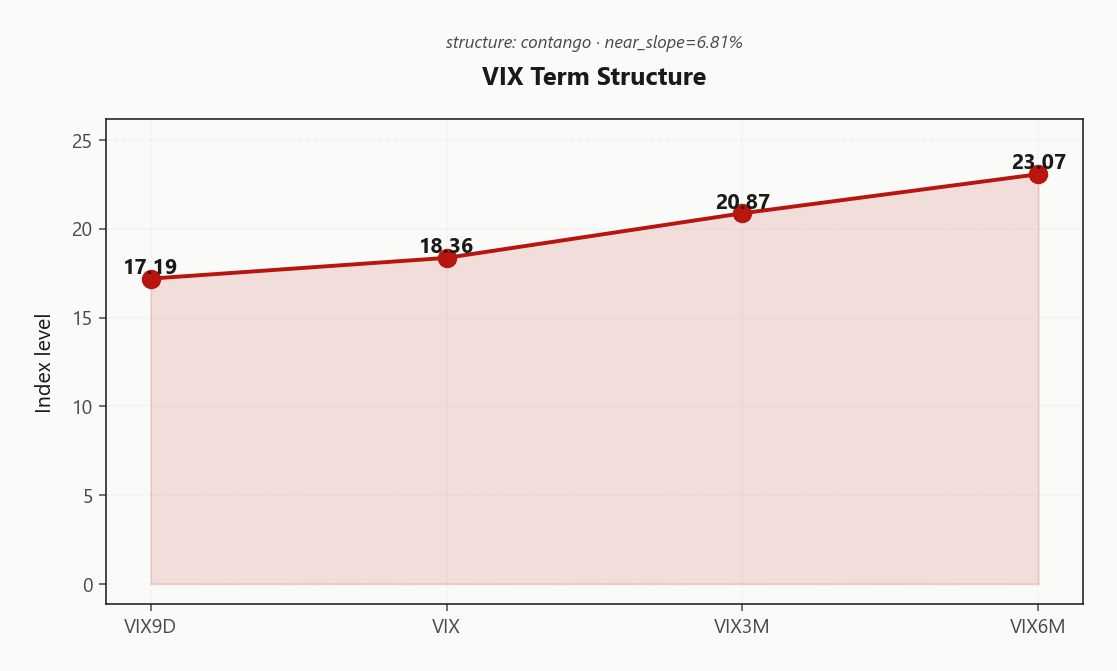

The VIX curve prints a clean Contango ladder with all four nodes stepping up: VIX9D at 17.19 sits below VIX at 18.36, both well under VIX3M at 20.87 and VIX6M at 23.07. The regime reads Steep Contango - vol sellers are paid to hold the line, but the back end is not giving the premium away.

Near slope at 6.81%% keeps structural carry alive on the front leg, while front-month VIX futures at 20.90 against spot of 18.36 price a 13.83%% basis that confirms the carry regime. Forward 30-to-60 implied at 22.0179597147 is where roll-down PnL concentrates.

Trade construction: sell the 30-60 forward, hedge with VIX9D length. The front node is too compressed to carry long, but it is the cleanest cheap convexity if Iran headlines escalate. Fade the belly, own the wing.

What it means for your trading

Steep Contango with the back end pricing real risk premium - the edge is selling the 22.0179597147 forward against cheap 17.19 length, not naked front-month shorts.

Trading readClean Contango ladder with near slope at 6.81%% - vol carry trade is paid, market does not expect imminent stress. A flattening of the 9-day-to-spot leg is the early warning sign.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 16.13% sits materially above HV20 at 11.77, leaving VRP at 4.36% structurally bid. Vol sellers are getting paid handsomely versus what spot has actually delivered - premium is rich, not fair, and the carry is the trade.

HV60 at 15.45 threads between IV and HV20, a tell that the implied bid is anchored to the memory of larger moves rather than current realized. That's a stale-fear premium - the market is paying for a regime that hasn't been delivered in a month, which is exactly when short premium edge is widest.

QQQ VRP runs wider at 7.08%, fattened by tonight's mega-cap earnings flow that hasn't yet been crushed out of the surface. IWM tops the complex at 7.33% - small caps carry the highest premium per realized point, but pair that with the negative_gamma regime in both names before sizing. The cleanest harvest sits in SPY where dealers aren't fighting you.

What it means for your trading

VRP is structurally paid across the complex with SPY at 4.36%, QQQ at 7.08%, and IWM at 7.33% - premium harvest works, but route through SPY to avoid the short-gamma penalty in tech and small caps.

Skew Convexity

The body is calm but the tail is paying up. SPY's quarter-delta put prints 23.3% against a call wing at 20.47% and ATM at 21.51% - a skew of 2.83% points with smile ratio at 1.14%. That's a one-sided hedge bid, not a smile; left wing is doing the work while the right wing barely registers.

The complex steepens as you move down the cap stack. QQQ skew at 4.69% reflects more aggressive tech downside hedging - consistent with three mega-cap prints tonight and Negative Gamma dealer positioning underneath. IWM at 4.31% is the steepest leg of the three, small-cap puts the richest relative to ATM and the cleanest read on where the marginal hedger is paying up.

Implication: skew is rich enough to fade, but selectively. Prefer put spreads over naked puts to monetize the steepness rather than fight it; the call wing's cheapness rewards condor structures around the SPY walls more than directional shorts.

What it means for your trading

Quarter-delta put skew is structurally bid across the complex - 2.83% in SPY widening to 4.31% in IWM - a classic late-cycle pattern where the body trades calm and the tail pays up. Sell the steepness via put spreads and condors, don't buy it naked.

Vol-of-Vol Structure

Vol-of-vol sits in the Normal range - VVIX at 95.53 against VIX at 18.36 prints a ratio of 5.20, a Green read with no panic premium bleeding into the VIX call wing. Carry trades stay intact and sizing reverts to Standard Size.

The genuine tail premium isn't in VVIX absolute level - it's in VIX upside convexity. VIX call-25d marks at 148.46%, materially richer than what the VVIX/VIX ratio implies and consistent with a headline-driven bid rather than a systemic one. That's the asymmetry to respect: the body of vol-of-vol is calm, the right wing is paying up.

Operationally, run book size on Iron Condor structures and don't haircut for vol-of-vol. The trigger to cut is a VVIX/VIX uptick on Iran escalation - until then, Normal means standard, not stressed.

What it means for your trading

Vol-of-vol at Normal levels with a Green signal - size short premium normally, but the rich VIX call-25d at 148.46% is the live tripwire if headlines escalate.

Dispersion Spread

Index VRP screens attractive, but the regime split does the work here: SPY ATM IV at 16.13% versus QQQ at 22.57% opens a meaningful gap, with IWM at 22.99% marking the high-vol leg of the complex. Cross-asset tone reads Unknown with divergence direction Spy Heavier - small caps and tech are paying up for a reason while large-cap stays anchored.

The implication is operational: index dispersion is not neutralizing single-name earnings risk tonight. Selling QQQ vol means absorbing the GOOGL/MSFT/AMZN event leg through a Negative Gamma underlying; selling IWM vol stacks the richest premium against the most fragile regime. SPY, sitting Positive Gamma above its flip, is the only leg where dealer hedging and VRP push the same direction.

Stick to SPX/SPY for the premium harvest. The dispersion trade - long single-name vol, short index vol - is structurally underpriced into tonight's prints, but that's a book-level expression, not a substitute for clean SPY-only condors at the walls.

What it means for your trading

The IV gap between SPY at 16.13% and QQQ/IWM at 22.57%/22.99% is real premium, but with divergence direction Spy Heavier it's compensation for regime risk you don't want. Harvest the SPY leg only.

Liquidity & Microstructure

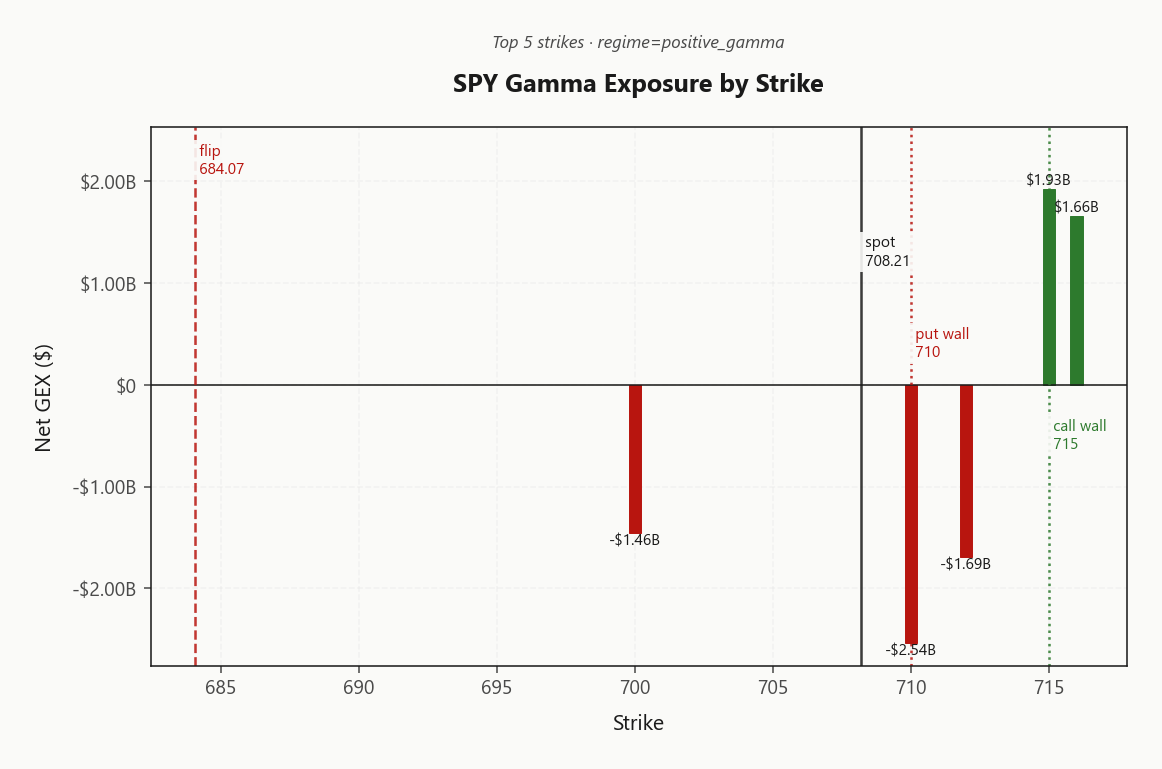

SPY's open interest stacks tightly between the 710.00 put wall and the 715.00 call wall, with spot at 708.21 pinned just above the proximate magnet. The top-strike concentration sits at 710.00 carrying net GEX of -$2.54B - that's the gravitational center of the book into the close.

The gamma flip at 684.07 against spot at 708.21 leaves a real but thin cushion; the highest OI cluster at 700 is an older support node that no longer dominates the dealer-hedging math. Below the flip, positive_gamma inverts to negative_gamma and the damping zone gives way to amplification - small breaches get faded, conviction breaches accelerate.

Zero-DTE carries 39.8% of total gamma, which means intraday flow drives a meaningful share of close-to-close behavior. Expect chop within the wall corridor and a fast regime shift outside it.

What it means for your trading

Spot trapped between 710.00 and 715.00 with the flip at 684.07 just below - fade strength into the call wall, but treat any breach of the put wall toward the flip as the regime-change trigger.

Trading readSPY's positive-gamma cluster between 710.00 and 715.00 traps spot in a damping zone - fade strength into the call wall, expect dealer support if spot breaches the put wall toward the flip. Below the flip the regime inverts hard.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX is the trade today. SPY carries -$161.51B of dealer vanna against -$1.13B of charm - the gamma cushion is real but conditional, and any uptick in 18.36 translates one-for-one into dealer delta selling. That's the accelerant condition: positive gamma damps until vol moves, then vanna takes the wheel.

QQQ compounds the asymmetry with -$105.06B of negative vanna stacked on top of an already Negative Gamma book. Same mechanism, worse starting point - a vol uptick there doesn't flip a regime, it deepens one. The charm pivot sits at 710, only 0.2527498906 from spot, with bias reading Neutral; that's the operative level for late-day flow into the close.

Practical read: vanna is the single largest unhedged exposure on the tape. Size short premium with VVIX/VIX at 5.20 in mind, and treat any break of the charm pivot or a tick higher in the front VIX node as a cue to lighten - not because the cushion is gone, but because it stops being a cushion the moment vol bids.

What it means for your trading

Dealer vanna is deeply negative across SPY and QQQ - the positive-gamma read is contingent on 18.36 staying contained, and the charm pivot at 710 is the operative trigger for late-day flow.

Cross-Asset Confirmation

The cross-asset tape isn't confirming a systemic risk-off - it's confirming geopolitics. MOVE sits at 68.68, nowhere near a level that would validate the equity vol bid as credit-driven, while Fear & Greed prints 63 in Greed territory. Bonds are calm, sentiment is still risk-on, and the tail premium is concentrated in the equity options surface - that's a headline trade, not a macro shock.

Underneath the index complex, the divergence is doing the heavy lifting. SPY-QQQ regime split flags True with direction Spy Heavier - large-cap stability anchored above the flip while QQQ at 656.64 and IWM at 271.22 sit below theirs as the fragile legs. The break, if it comes, originates in small caps and tech, not SPX.

The tell to watch is MOVE. A break higher in bond vol is what converts this from headline-driven to systemic; until then, fade vol spikes on Iran-tape escalations and stay paid on premium against the SPY walls.

What it means for your trading

Equity-vol bid is geopolitical, not credit - MOVE at 68.68 and F&G in Greed argue for mean reversion if Iran headlines fade, with the QQQ/IWM short-gamma legs as the asymmetric break risk.

Scenario EV

Structure selection lands on Iron Condor with a top score of 43 versus the put spread alternative at 34 - defined-risk premium sale wins on a clean margin. The setup is paid by three independent legs: Steep Contango in the VIX curve feeds both wings via roll-down, the SPY 715.00 call wall and 710.00 put wall anchor the strike geometry, and VRP at 4.36% keeps the short premium structurally rich versus what spot has actually delivered.

Sweet spot is the 30-45 DTE bucket - long enough to harvest term carry from 22.0179597147 forward implieds, short enough that vanna decay stays bounded against the deeply negative -$161.51B dealer book. Sizing per VVIX guidance: Standard Size - VVIX/VIX at 5.20 sits in the Normal range, no panic premium to discount for.

Underlying is Positive Gamma with spot 708.21 above the flip at 684.07, so dealers don't fight the structure. Keep the trade SPY/SPX-only - QQQ and IWM sit Negative Gamma below their flips and don't earn the same dealer cushion.

What it means for your trading

Iron Condor at 30-45 DTE around the 715.00/710.00 corridor is the cleanest carry expression - Standard Size sizing applies, SPY-only, avoid extending the structure into negative-gamma QQQ/IWM.

Actionable Summary

Sell premium via Iron Condor structures on SPX/SPY at the 30-45 DTE bucket, framed around the 715.00 call wall and 710.00 put wall. Spot sits in Positive Gamma territory above the flip at 684.07 - dealers fade strength into the upper wall and cushion weakness toward the lower one. Contango is Steep Contango, VVIX/VIX prints Normal, and VRP at 4.36% keeps the carry structurally paid. Sizing per Standard Size.

Avoid naked QQQ and IWM upside chase - both indices print Negative Gamma below their flips, and the regime divergence is flagged Spy Heavier. Avoid shorting VIX call wings: the rich call-25d at 148.46% is paying for headline tail, not noise. Watch the charm pivot at 710 where bias reads Neutral, and the VVIX/VIX ratio at 5.20 for any uptick that flags tail-bid escalation. MOVE at 68.68 stays the credit-market tell - until it breaks higher, this remains geopolitical, not systemic.

What it means for your trading

Trade structure is Iron Condor around the SPY walls at 30-45 DTE while the regime stays Elevated / Watchful; the unhedged risk is a VVIX uptick flipping the -$161.51B vanna cushion on Iran-headline escalation.

Iran blockade headlines are the proximate driver of the elevated VIX call skew and steeper put-25d across the index complex - geopolitics is paying up, not credit.

Three mega-cap earnings tonight (GOOGL, MSFT, AMZN) plus Fed meeting - explains the steep QQQ skew and the meaningful event premium baked into 1-2 day IVs.

OPEC instability layered on top of Iran blockade is the macro backdrop pushing forward vol up despite stable spot equity - watch energy as the transmission mechanism.

UBS profit beat from Iran-driven trading volatility is a real-world confirmation that the vol bid is sticky enough to feed dealer P&L, which means it won't unwind quickly.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.78 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Spy Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 684.07 against a spot of 708.21. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.13% with a volatility risk premium of 4.36%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.36. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime