Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

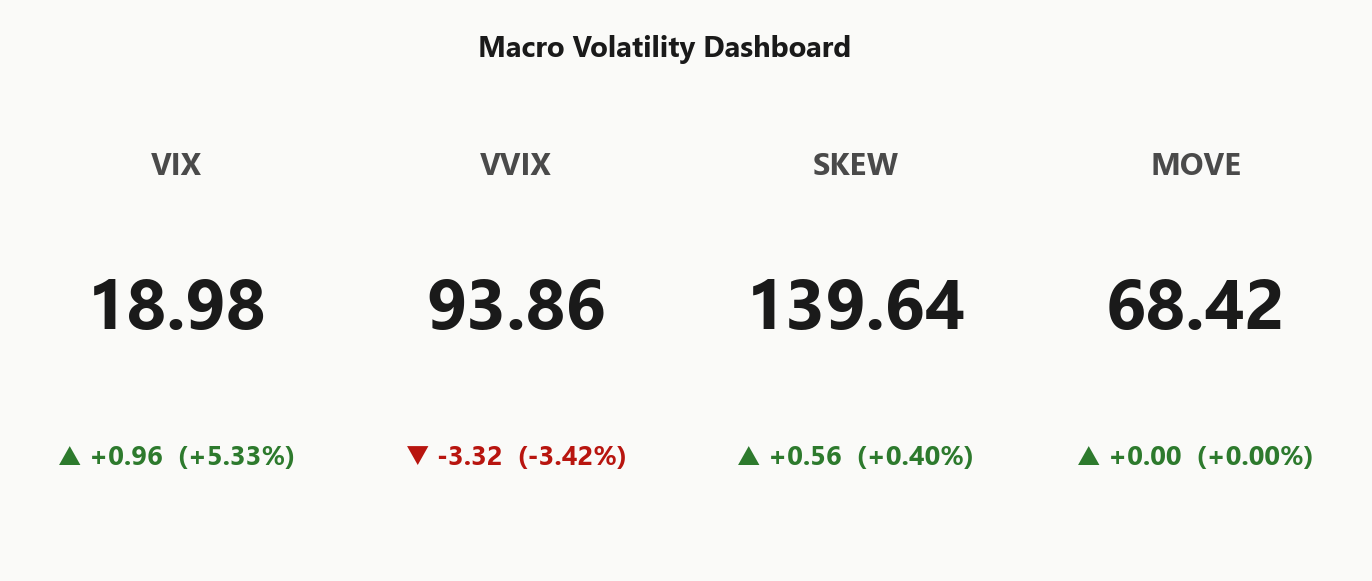

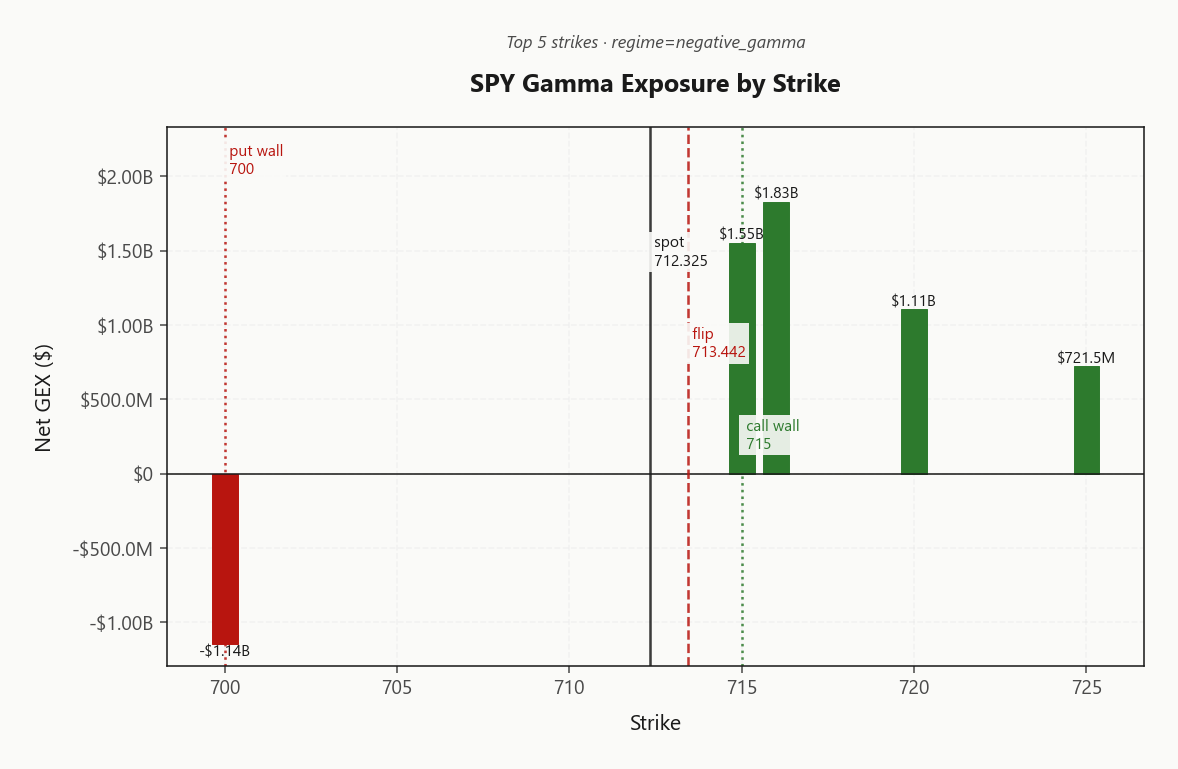

SPY at 712.33 sits just under its gamma flip at 713.44, putting dealers in Negative Gamma with net GEX of $348.1M - moves get amplified, not dampened. Call wall at 715.00 caps the rally, put wall at 700.00 is the next gravity well if 713.44 fails. Dealers carry net VEX of -$204.55B and net CHEX of -$989.5M - vanna and charm both push delta lower as vol rises and time decays, hostile into the close. VIX at 18.98 (+5.33%%) with VVIX at 93.86 confirms a watchful regime; term structure is Contango with near-slope 13.72%% - front-week stress, back months still calm. VRP of 1.88% is positive but compressed, and 0DTE gamma is -322.8%% of total - intraday whip risk is the dominant feature. IWM holds Positive Gamma above 273.38 - divergence says small-caps are the stable leg today. Bottom line: treat 713.44 as the line in the sand - below it, fade rallies into 715.00 and respect downside extension toward 700.00; above it, dealers re-cushion and mean-reversion returns.

Negative gamma below 713.44 with VIX bid on Iran tape - amplifier regime, contango still paying carry

SPY opens just under 713.44 in negative-gamma territory while VIX pops on Iran impasse and crude at 68.42-adjacent stress. The term structure stays in Contango with VVIX at 93.86 - vol sellers still get paid out the curve, but front-week 0DTE gamma is destabilizing into a charm-hostile pivot. IWM diverges positive-gamma while SPY/QQQ flip dealers short - small-caps are the stable leg, mega-cap index is the fragile one.

Regime Assessment

Regime print is Elevated / Watchful with VIX at 18.98 - squarely in the elevated band but well clear of panic. The transition matrix is the tell: probability of escalating to panic over the next handful of sessions sits at 0.05, while the probability of normalizing back to low over a two-week window runs materially higher at 0.45. Base case is mean-reversion, not escalation.

Half-life is 15 sessions - sticky but not stuck. Plan for roughly two weeks of similar conditions: contango carry intact, VVIX normal, walls well-defined, but spot pinned sub-flip with vanna and charm pulling delta lower into closes. The regime won't snap on a single headline; it will grind.

Trade the band, not the tail. With cross-asset tape Aligned and IWM still holding Positive Gamma, the canary is fine. Size standard, lean defined-risk neutral structures, and treat any VIX pop toward the panic threshold as the fade - not the entry.

What it means for your trading

Elevated but mean-reverting: panic-transition odds of 0.05 versus normalization odds of 0.45 over ten sessions argues for fading vol pops, not chasing them. Half-life 15 sessions - plan two weeks of Elevated / Watchful conditions and watch IWM as the broadening tell.

Trading readVIX bid, VVIX softer, SKEW elevated, MOVE flat - the dashboard is mixed. SKEW says tail is being bid; MOVE says credit isn't worried; VVIX says the spot vol move is digestible. This is an equity event, not a system event - until MOVE moves.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

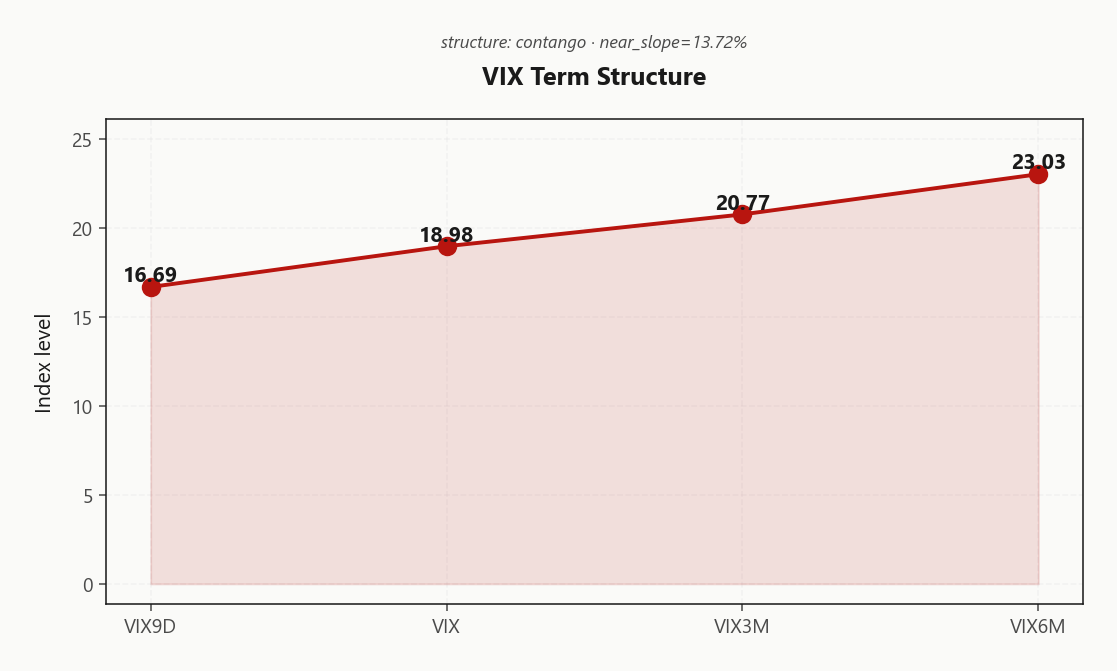

The curve prints clean upward-sloping Contango with near-slope at 13.72% - structural carry is intact and the back end is pricing normalization, not contagion. 16.69 on VIX9D printing under spot VIX at 18.98 is the tell: front-week stress from the Iran tape is concentrated at the kink, not bleeding into the very near term. VIX3M at 20.77 and VIX6M at 23.03 anchor the back of the curve.

Forward 30-to-60 vol resolves to 21.6094689893 - that is the cleanest expression of the carry, and where short-vol structures deserve their capital. Selling the kink eats the headline tail; selling the belly collects theta on the flattest, richest segment of the surface.

Regime read: Contango - structural carry available. Green light for short-vol carry, but size for the Iran tail - DTE sweet spot is the 30-45 bucket, past the front-week event premium and ahead of back-month decay erosion.

What it means for your trading

Term structure is Contango with the front kink absorbing the geopolitical bid while the back end normalizes - sell vol at the 30-45 belly where forward vol resolves to 21.6094689893, not at the kink.

Trading readVIX9D under VIX under VIX3M under VIX6M = Contango with slope 13.72%% - vol-carry trade is alive, the back end is pricing normalization, the front kink absorbs the Iran headline.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 16.19% still trades rich to HV20 at 14.31, leaving a positive VRP cushion of 1.88%. HV60 at 15.47 prints above HV20 - recent tape is calmer than the three-month baseline, so options are doubly rich to what's actually been delivered. Realized has not accelerated into the Iran headlines; the vol bid is in the screen, not on the tape.

The premium isn't evenly distributed. QQQ VRP at 4.64% and IWM VRP at 5.3% dwarf the index expression - single-name dispersion is where the richest carry sits, and IWM in particular pays meaningfully more per unit of DTE.

Bottom line: options are rich to realized across the complex, but the SPY VRP cushion has thinned. Favor defined-risk short-premium structures - condors, strangles - over outright long vol hedges; lean the size into QQQ and IWM where the cushion is fattest.

What it means for your trading

ATM IV at 16.19% versus HV20 at 14.31 keeps VRP positive at 1.88%, but the richest carry is in QQQ at 4.64% and IWM at 5.3% - short-premium, not long vol.

Skew Convexity

The front-week smile is decisively asymmetric: put 25d prints 22.7% against ATM at 20.12% and call 25d at 17.92%. Skew of 4.78% vol points with a smile ratio of 1.27% tells the story - downside is bid, upside is unloved. SKEW at 139.64 independently confirms the tail is paying up.

The call wing trading at a discount to ATM is the tell: there is no upside conviction priced in, fully consistent with the negative-gamma cap dealers are defending at 715.00. The wing premium is concentrated entirely on the put side, which changes the hedging math.

Trade implication: prefer put spreads over naked puts here. The expensive put wing funds the structure on the short leg, cheapening the protection materially versus an outright. Naked downside is overpaying the asymmetry the market has already priced.

What it means for your trading

Skew is steep and one-sided - put 25d at 22.7% versus call 25d at 17.92% with SKEW at 139.64 means the tail is bid and the upside is discounted. Put spreads, not naked puts, are the efficient expression.

Vol-of-Vol Structure

The single most important comfort signal on the page: VVIX prints 93.86 and is actually down -3.42%% on the day even as VIX at 18.98 trades bid on the Iran tape. That divergence is the tell - vol-of-vol is explicitly disagreeing with the spot vol move. The market is pricing this as a digestible headline pop, not the front edge of a bimodal regime shift.

The VVIX/VIX ratio at 4.95 sits squarely in Normal territory, hugging the long-run mean. No jump-risk premium is being layered into VIX options; dealers are not paying up for convexity on vol itself. Translation: the geopolitical tail is being treated as priced-in, not as an open-ended fat-tail catalyst.

Sizing guidance follows directly - Standard Size. This is not a half-size regime. Full-size vol-selling structures are appropriate against the contango carry; the dealer-positioning hostility (negative VEX, negative CHEX) belongs in strike selection and the gamma flip line, not in clip-size haircuts.

What it means for your trading

VVIX softer while VIX is bid, ratio at 4.95 in Normal territory - vol-of-vol refuses to confirm a bimodal break, so Standard Size is the green light for full-clip short-vol structures. Manage the regime through strike selection around the gamma flip, not through reduced size.

Dispersion Spread

Dispersion is bid and the index/single-name spread is the cleanest expression on the page. SPY ATM IV at 16.19% sits well inside QQQ at 22.51% and IWM at 22.63% - index hedges are underpricing the idiosyncratic earnings tape, and the small-cap premium says correlation crush is real, not statistical noise.

Mover GEX is confirming the rotation: META leads with a Positive dealer repositioning, with AMZN and AAPL stacking behind it - capital is moving name-by-name, not index-wide. That is the signature of a dispersion regime, and it argues against treating the SPX complex as a proxy for the underlying book.

Trade expression: short index vol against long single-name vol, sized into the dispersion premium rather than the headline. Avoid naked short premium into single-name earnings prints - the wing on those names is paying up for a reason. Index condors collect the carry; single-name shorts give it back on the first gap.

What it means for your trading

Single-name IV running rich to SPY at 16.19% with QQQ at 22.51% and IWM at 22.63% - fund index short-vol with single-name long-vol and let META-led dispersion do the work.

Liquidity & Microstructure

The book's gravity is unambiguous: deepest open interest sits at 600, well below spot - legacy hedges still anchoring the tape - while the active battle plays out between the put wall at 700.00 and the call wall at 715.00. The single number that matters is 713.44: the regime switch. Spot prints sub-flip, which puts dealers in Negative Gamma and turns every tick into an amplifier rather than a cushion.

Above the flip, dealer hedging mean-reverts moves; below it, dealers chase. Top GEX strike at 716.00 carries net GEX of $1.83B, stacking call-side gravity just overhead and reinforcing 715.00 as the hard cap on any reflex rally. If 713.44 fails to reclaim, the magnet is the put wall at 700.00 - the next structural floor where dealer flow re-anchors.

Trade the line, not the noise: reclaim of 713.44 re-cushions; rejection extends toward 700.00.

What it means for your trading

Sub-flip negative gamma between 700.00 and 715.00 makes 713.44 the only level that matters - reclaim cushions, rejection amplifies into the put wall.

Trading readCall wall at 715.00 caps rallies and put wall at 700.00 is the magnet on weakness - between them is whip territory because spot trades just under 713.44, the dealer regime switch.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order Greeks are stacking against the tape. Net VEX prints at -$204.55B - deeply negative - which means every uptick in vol forces the book to sell delta, the textbook vanna accelerant. Net CHEX at -$989.5M compounds it: charm bleed pushes the same hedges lower as the clock runs, loading pressure into the close rather than relieving it.

The charm pivot sits at 713.4423528334, a hair above spot at 0.1568599773% distance, and the current bias reads Destabilizing. Both vanna and charm are pulling in the same direction - there is no offsetting flow buried in the book to lean on. Combine that with sub-flip negative gamma and you have three force vectors aligned south.

Trade implication: any vol pop down here gets force-sold lower by dealer hedges. Do not reflexively fade weakness - the mechanical seller is still in front of you. Wait for spot to reclaim 713.44 before the cushion returns, or for an overshoot into 700.00 where the magnet bites.

What it means for your trading

Vanna and charm are aligned hostile with the pivot at 713.4423528334 and bias Destabilizing - dealer hedges amplify weakness rather than dampen it, so reclaiming 713.44 is the prerequisite for any mean-reversion trade.

Cross-Asset Confirmation

Bond vol is the tell: MOVE at 68.42 sits flat while equity vol bids on the Iran tape - credit is unbothered, which keeps this an isolated equity/geopolitical event rather than a system-wide repricing. Until MOVE moves, the mean-reversion playbook stays live and the spot vol pop is fade-able further out the curve.

Sentiment cuts the other way. Fear & Greed at 67 still rates Greed - contrarian-bearish at the margin, the classic late-cycle pairing of greed sentiment with sub-flip negative gamma that punishes reflexive dip-buyers. Cross-asset tone reads Unknown with regime divergence Aligned.

Within equities, dispersion is the cleanest signal. QQQ at 658.76 mirrors SPY in negative gamma, but IWM at 276.47 holds positive gamma above its flip - small-caps are today's stable leg, mega-cap and the AI complex are the fragile ones. Watch IWM as the canary; if it flips sub-flip too, the regime broadens and the credit-event tail starts pricing in.

What it means for your trading

MOVE flat at 68.42 and F&G Greed at 67 say this is an equity-only event - fade the vol pop out the curve until IWM rolls or MOVE bids.

Scenario EV

Synthesis says Iron Condor is the trade - score 45 versus the put-spread alternative at 37. Contango carry is alive, VVIX sits in the normal zone, VRP is positive, and the walls are clean: 715.00 caps the rally, 700.00 is the magnet on weakness. Defined-risk neutral structure is what this regime pays for.

DTE sweet spot is 30-45 - past the front-week kink where the Iran tape concentrates event premium, before the back-month theta drag slows. Anchor the body inside the wall pair and let the contango do the work. Sizing stays Standard Size - VVIX is not pricing a bimodal outcome, so this is full-size territory, not half-size.

Avoid front-week naked vol selling and calendars that straddle the Iran catalyst window - the front kink is where the headline risk lives. Respect 713.44 as the regime line, but the trade itself is the condor between the walls.

What it means for your trading

Defined-risk neutral via Iron Condor in the 30-45 DTE bucket, anchored between 700.00 and 715.00, sized Standard Size. Front-week vol selling and calendars through the Iran window are the trades to skip.

Actionable Summary

SPY trades just under 713.44 in Negative Gamma territory, with dealers carrying net VEX of -$204.55B and net CHEX of -$989.5M - vanna and charm both push delta lower as vol rises and time decays. The pivot at 713.4423528334 is the line in the sand: above it, dealer cushion returns; below it, weakness gets force-sold into the close. Bias reads Destabilizing.

The trade is Iron Condor in the 30-45 DTE bucket, struck between 700.00 and 715.00. Hedge with put spreads - the wing premium funds the structure. Avoid front-week naked vol selling and chasing weakness while VEX is this negative. Watch IWM as the canary; if it flips, the regime broadens.

What it means for your trading

Structural contango carry plus normal vol-of-vol plus clean walls makes Iron Condor the highest-EV expression, but 713.44 is the regime switch that gates the entire playbook. Plan for Elevated / Watchful conditions to persist roughly 15 sessions.

Gulf summit on Iranian strikes is the geopolitical anchor for today's vol bid - every Mideast escalation headline this week is going to flow straight into front-week IV, which is why VIX9D underperforms VIX.

Hormuz subsea-cable risk is the asymmetric-tail story behind oil and tech vol - if cables go, energy AND comms are simultaneously hit, and that's a credit-event-shape distribution, not a normal one.

European political pressure on the US over Iran raises the probability of policy mistakes and discontinuous moves - exactly the kind of regime-shift catalyst that compresses VVIX/VIX ratio if it actually fires.

Treasury yields rising on stalled peace talks is the cleanest cross-asset confirmation that the market is pricing event risk - 10Y at 4.356% means TLT is NOT bid as flight-to-safety, which keeps the equity move idiosyncratic.

ECB credit tightening from the Iran war is the slow-burn macro story - banks rationing credit is how a geopolitical shock turns into a credit shock, and that's the regime change that breaks contango.

Trump rejecting the latest Iran proposal directly extends the conflict timeline and is the proximate cause of today's VIX bid - every refresh of this headline is a vol catalyst.

Crude at $110 alongside the Iran impasse is the inflation-and-growth double-hit that breaks the soft-landing narrative - energy spike plus AI capex concern is the setup for a regime widening if it persists.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.59 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.44 against a spot of 712.33. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.19% with a volatility risk premium of 1.88%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.98. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime