Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

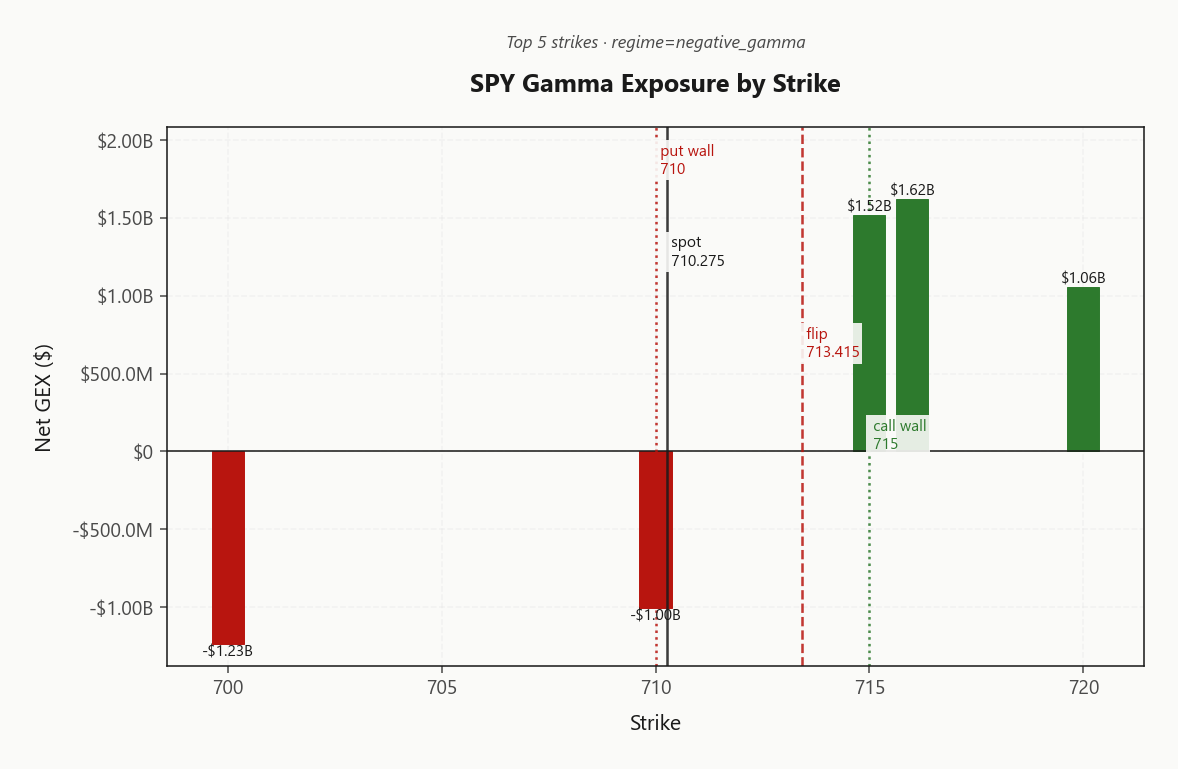

SPY at 710.28 sitting right on the put wall 710.00 with net GEX at -$2.02B - dealers short gamma, every tick gets amplified into the close. Gamma flip 713.41 is overhead at the call wall 715.00 corridor, so you're trading inside a 710.00 - 715.00 amplification box with the bias slightly negative. Vanna at -$187.82B and charm at -$986.6M are both pulling dealers to sell into weakness - vol-up = more selling, time decay = more selling, that's a hostile combo into the bell. VIX at 18.50 with VIX3M at 20.96 keeps term structure in Contango and VRP at 1.58% stays positive - so options on duration are still rich to realized. VVIX at 94.55 is normal: this is local 0DTE turbulence, not a vol-of-vol regime shift. Bottom line: do not press the 0DTE - fade extremes toward 713.41, sell premium via Iron Condor in the 30-45 window, hard stop on a clean break of 710.00.

Negative gamma into 0DTE pin with VIX contango - amplified moves, but vol sellers still favored on duration

SPY at 710.28 is pinned at the put wall 710.00 with dealers short gamma - every move gets amplified into the close. But VIX term structure stays in contango at Steep contango - vol sellers favored and VVIX is normal at 94.55, telling you the dislocation is local to 0DTE, not regime-wide. Trade the chop with iron condors out at 30-45, not the 0DTE knife fight.

Regime Assessment

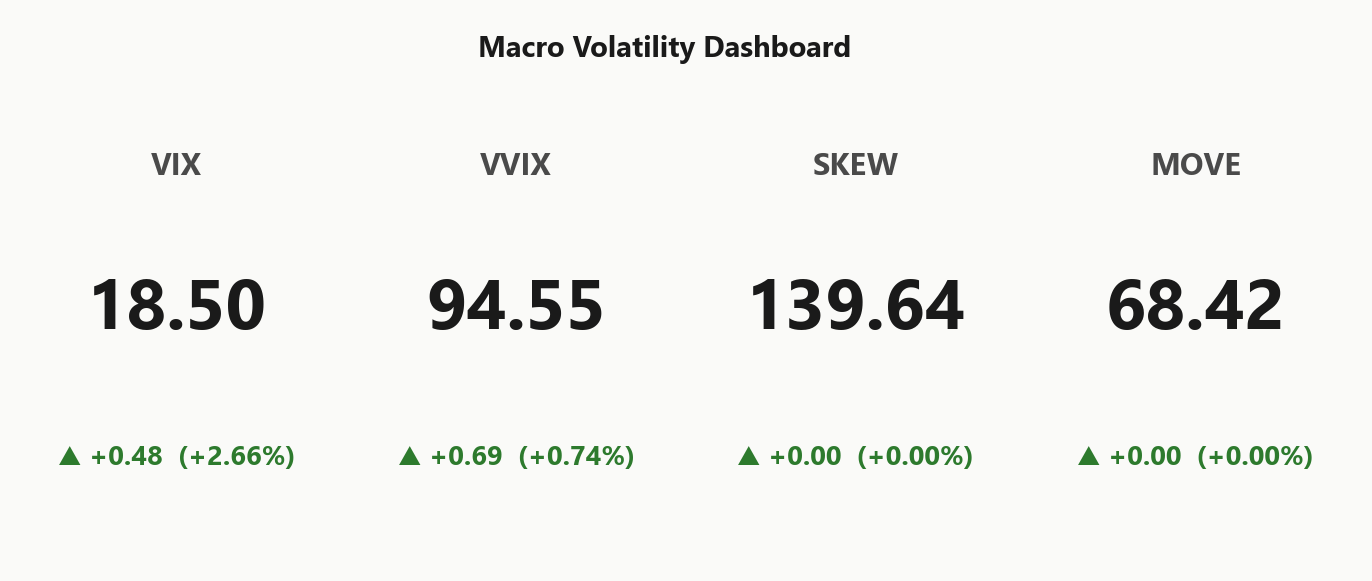

Regime reads Elevated / Watchful with VIX anchored at 18.50 - the transition matrix puts panic risk over the next five sessions at just 0.05, while the path back to a low-vol state over ten sessions sits at 0.45. This is the watchful middle, not the cliff edge.

Half-life of 15 sessions tells you the regime is sticky - it does not collapse on a single tape, and it does not resolve on a single calm close. Plan accordingly: duration trades dominate scalps when the persistence is this high, and the VRP carry sitting on top of Contango rewards holding the structure rather than flipping it intraday.

Bottom line: the Elevated regime is your operating environment for weeks, not days. Size standard per Standard Size, lean into Iron Condor in the 30-45 DTE window, and stop hunting for a regime change that the math says is unlikely to arrive this week.

What it means for your trading

Regime is Elevated / Watchful with low panic odds (0.05) and a sticky 15-session half-life - trade duration via Iron Condor, not regime-flip scalps.

Trading readVIX up modestly, VVIX up modestly, MOVE flat, SKEW elevated - partial confirmation. SKEW divergence vs MOVE is the watch item; equity tail bid without rates tail bid usually mean-reverts.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

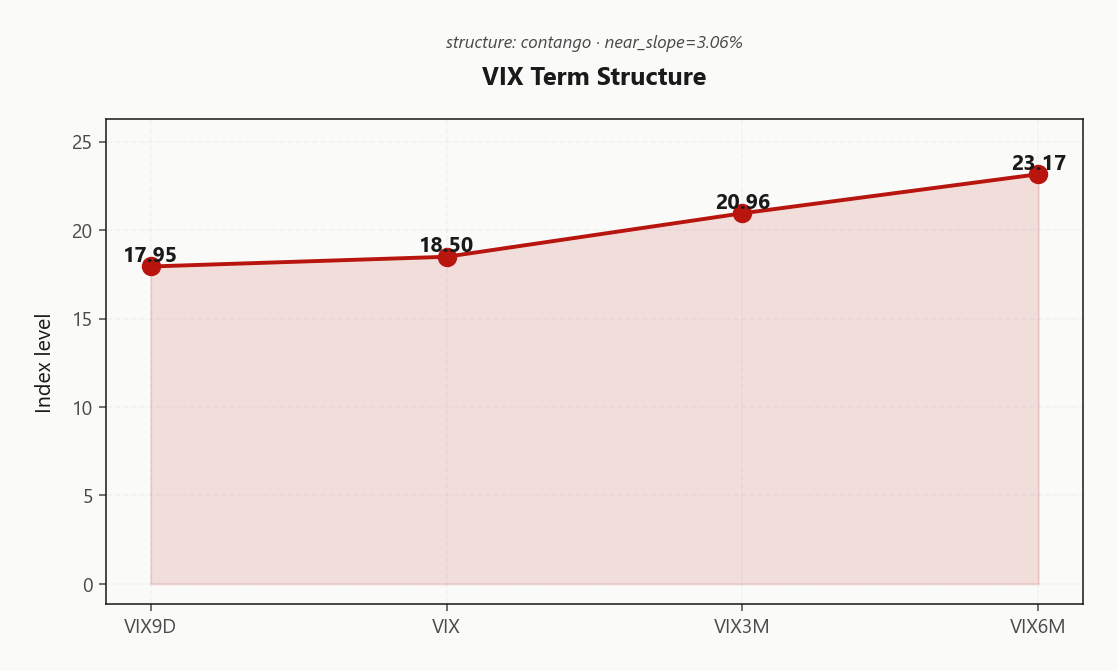

Term structure is doing the work the spot tape can't. VIX9D 17.95 printing under VIX 18.50 tells you the front-belly compression is local 0DTE noise, not a forward stress signal - near-term complacency persists despite the dealer-short-gamma pin. The back end is where the carry lives.

VIX3M 20.96 stacked over VIX6M 23.17 in Contango sequence pays calendar sellers cleanly, and forward 30-60 at 22.0874941992 embeds positive roll-down before you even pick a strike. Structure label reads Steep contango - vol sellers favored - a green light for duration shorts.

Monetize the slope, don't fight the pin. The 30-45 DTE pocket is the sweet spot: far enough out to harvest the contango, well clear of the 0DTE knife fight where vanna and charm are forcing dealers to sell into every spike. Front-month carry is asymmetric to back-month - sell the latter, leave the former to the day-trade flow.

What it means for your trading

Steep contango from VIX9D through VIX6M validates short-vol on duration with the forward 30-60 structure paying positive carry; deploy the Iron Condor in the 30-45 DTE window and skip the front-end pin chaos.

Trading readSteep contango from VIX9D to VIX6M = textbook short-vol carry on duration. Market is NOT pricing forward stress; the front-end chop is local. Calendar-spread sellers get paid here.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 16.2% is printing meaningfully above HV20 14.62 and HV60 15.51 - VRP runs 1.58% and stays firmly positive. Translation: the tape has not delivered what the strip is charging, and premium sellers are getting paid the spread. With HV60 sitting above HV20, realized is decelerating into a still-rich implied bid - the classic carry window for short-vol on the curve.

The catch is path. Dealers are short gamma, so even with VRP intact the trip from print to expiry can chop hard before realized catches implied. That makes the front contract a knife fight: 0DTE skews can spasm wider on any tick without invalidating the duration thesis. Sell vol where the curve does the work - 30-45 DTE - not where gamma does the damage.

Bottom line: VRP is the edge, gamma is the tax. Harvest Iron Condor on duration; do not press the front.

What it means for your trading

VRP at 1.58% with implied 16.2% over realized 14.62 keeps premium sellers paid on the curve, but negative gamma means execute the trade at 30-45 DTE, not at the front.

Skew Convexity

Quarter-delta put IV at 20.39% trades a clean premium over ATM 18.65%, while the call wing sits pinned flat at 16.95% - left tail bid, right tail abandoned. Skew at 3.44% is steep but reads as ordered hedging, not capitulation; smile ratio 1.2% confirms the shape is convex-balanced rather than panic-skewed.

The flat call wing is the tell: nobody is paying for upside convexity, so any rally back through the call wall 715.00 finds zero vega support and gets sold mechanically. Downside, by contrast, is paid for - but it's spread demand, not naked tail. SKEW index at 139.64 sits elevated without MOVE confirmation at 68.42, so the bid is equity-local, not cross-asset stress.

Trade implication: put spreads beat naked puts on a cost-adjusted basis, and the flat call wing makes ratio call spreads or covered-call overwrites cheap to finance hedges. Watch ten-delta wings for steepening - that's where panic prints first, and skew at 3.44% hasn't tipped there yet.

What it means for your trading

Skew shape at 3.44% with smile ratio 1.2% signals ordered downside hedging, not panic - finance protection with put spreads or call-wing overwrites rather than paying full freight on naked puts.

Vol-of-Vol Structure

VVIX prints 94.55 against VIX 18.50, putting the ratio at 5.11 - squarely in Normal territory. The vol-of-vol tape is not pricing a bimodal outcome, which means the 0DTE chop dominating spot is a mechanical artifact of dealer positioning, not the market reaching for a jump premium.

That distinction matters for sizing. With VVIX below the jump-risk threshold and term structure holding Contango, the recommended posture is Standard Size - no convexity tax, no mandatory tail overlay. Pay up for wings only if VVIX starts to lead VIX higher; until then, Iron Condor structures in the 30-45 DTE pocket carry their own protection via the contango slope.

Watch the ratio, not the absolute. A break of vol-of-vol normalcy - VVIX accelerating while VIX stays anchored - is the signal that mechanical chop is morphing into regime stress and that tail hedges flip from optional to mandatory.

What it means for your trading

Vol-of-vol at Normal with ratio 5.11 green-lights Standard Size on duration short-vol; tail hedges remain optional unless VVIX decouples higher from VIX 18.50.

Dispersion Spread

QQQ ATM IV at 23.27% sits well clear of SPY at 16.2% - a clean dispersion premium telegraphing that single-name idiosyncratic vol is doing the work index hedges keep missing. Cross-strike dispersion at 68.66 with cross-expiry at 1.8 reinforces the read: the richness lives inside the tape, not on the surface.

IWM ATM IV at 22.29% carries the small-cap fragility tax on top, rounding out a complex where every layer below the index is paying more than the index itself. That's the dispersion trade screaming - sell the index, leave the names alone. SPX/SPY iron condors in the 30-45 DTE pocket harvest the aggregated premium without taking on single-name headline risk.

Single-name VRP looks juicy on screen, but every megacap mover - NVDA, MSFT, META - is carrying its own event tape. Index-level expression strips that idiosyncratic event premium out and leaves you with the cleaner carry. Trade the basket, not the constituents.

What it means for your trading

Index-vs-single-name dispersion is the cleanest edge in the complex - sell SPX/SPY vol via Iron Condor structures in the 30-45 window rather than chasing the richer QQQ/IWM premium where idiosyncratic event risk eats the carry.

Liquidity & Microstructure

The headline open interest cluster at 600 is a red herring - that's legacy LEAPS sediment, not where the live battle sits. The active corridor is 710.00 to 715.00, and with spot at 710.28 pinned tight to the put wall, dealers are pressed into the maximum-amplification zone of the book.

Gamma flip 713.41 is THE level to watch - clear it and dealer flow inverts to supportive, lose the put wall and the negative-gamma machinery accelerates the tape lower. The top strike at 716.00 carries net GEX of $1.62B, anchoring the upper boundary and capping any reflex rally squarely into the call wall.

Trade the boundaries, not the middle. Fade extremes back toward 713.41, respect 715.00 as the rally cap, and treat a clean break of 710.00 as the hard-stop trigger that flips the regime.

What it means for your trading

The 710.00 - 715.00 corridor is the live battle with spot pinned to the put wall and dealers short gamma; 713.41 is the binary line that decides whether dealer flow turns supportive or amplifies a leg lower.

Trading readNegative gamma at 710.00 with positive gamma stacked above 715.00 sets up a ping-pong corridor - moves into the put wall get amplified down, rallies toward the call wall get capped. Trade the boundaries, not the middle.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX at -$187.82B is the dominant tell - deeply negative vanna means any uptick in IV forces dealers to sell delta, not buy it. That flips the usual vol-spike-as-relief script: a vol jolt here is an accelerant on the way down, not a brake.

Charm compounds the problem. Net CHEX at -$986.6M means time decay itself is pushing dealer flow toward selling into the bell - every hour closer to expiry, the hedge ratio bleeds the same direction as a spot drop. Vol-up sells, time-forward sells, spot-down sells: triple-confluence hostile.

The line in the sand is the Put Wall pivot at 710, with current bias Neutral at distance -0.0387173982. Above it, dealer flow flips supportive and the vanna/charm tax reverses; below it, the accelerants engage. Trade the pivot - don't fade the trigger.

What it means for your trading

Vanna and charm are aligned hostile with net VEX at -$187.82B and net CHEX at -$986.6M - a clean break of the Put Wall at 710 is the trigger that converts mechanical chop into directional dealer selling.

Cross-Asset Confirmation

Cross-asset tape is not confirming an equity stress event. MOVE at 68.42 is subdued - the rates complex sees no credit shock, no funding squeeze, no signal that today's negative-gamma chop is anything beyond an equity-mechanical event. Fear & Greed prints Greed at 67, the greed regime intact even as 0DTE flow dominates the index book.

QQQ at 655.19 and IWM at 273.53 sit in the same negative-gamma posture as SPY - regimes Aligned, no sibling index leading off in either direction. With cross-asset tone reading Unknown and bonds quiet, this is a synchronized index-complex repositioning, not macro contagion.

Trade implication: do not size for tail-risk pricing the bond market refuses to confirm. Harvest 1.58% on duration via Iron Condor; the 30-45 DTE pocket is where carry exists without paying the 0DTE pin tax.

What it means for your trading

MOVE at 68.42 subdued and Fear & Greed at 67 rejects the equity-stress narrative - this is a mechanical 0DTE event, not contagion. With QQQ and IWM regimes Aligned to SPY, sell duration vol rather than chase tail hedges.

Scenario EV

The book screens Iron Condor with a composite score of 42, comfortably ahead of the put spread alternative at 31. Positive VRP at 1.58%, Steep contango - vol sellers favored term structure, and VVIX parked at 94.55 in the normal band stack the carry case - three independent inputs all green-lighting premium harvest on duration.

Sweet spot is 30-45 DTE: far enough out to monetize the contango slope from VIX9D 17.95 through VIX3M 20.96, but well clear of the 0DTE pin where net GEX -$2.15B is doing the amplifying. Pitch the wings outside the 710.00 - 715.00 corridor so dealer flow does the boundary enforcement for you.

Sizing reads Standard Size - vol-of-vol isn't pricing a bimodal tail, so no tail-hedge tax required. Hard stop on a clean break of the charm pivot 710; below that, dealer flow flips and the carry trade becomes the wrong side of the tape.

What it means for your trading

Score gap of 42 versus 31 ranks Iron Condor in the 30-45 DTE pocket as the cleanest VRP harvest - sized standard, wings outside the wall corridor, kill-switch on a break of 710.

Actionable Summary

Bottom line: harvest VRP on duration, fade the 0DTE pin trap. SPY at 710.28 sits glued to the put wall 710.00 with net GEX -$2.02B negative - every tick into the bell gets amplified, and net VEX -$187.82B with net CHEX -$986.6M stack the dealer flow hostile. Pivot 710 is the line.

Do sell Iron Condor in the 30-45 DTE window outside the 710.00 - 715.00 corridor - VRP at 1.58% stays positive, term structure holds Contango, and VVIX 94.55 sits normal so standard sizing applies. Fade extremes toward gamma flip 713.41, fade rallies into the call wall 715.00.

Avoid naked 0DTE shorts - front-day GEX at -$2.15B is the whipsaw engine - and don't chase breakdowns through 710.00 without MOVE 68.42 confirming. Watch: a clean break of 710 flips dealer flow and is your hard stop. Regime Elevated / Watchful is sticky at half-life 15 sessions - plan duration, not scalps.

What it means for your trading

Sell Iron Condor in 30-45 DTE outside the 710.00 - 715.00 corridor; pivot 710 is the hard-stop trigger and a clean break flips dealer flow. Regime Elevated / Watchful stays sticky - harvest carry on duration, do not press the 0DTE.

UAE exit from OPEC is a structural energy-market shock - disrupts supply discipline, feeds energy-equity dispersion and could pressure broad inflation prints that the rate complex is already nervous about.

Dimon's bond crisis warning from JPM matters because it's the largest-bank CEO publicly flagging credit fragility - adds to MOVE-watch even as today's MOVE print stays subdued.

Trump-Iran-Hormuz headline keeps the geopolitical premium live in the energy and defensive complex - direct catalyst for crude vol, indirect for equity skew demand.

Treasury yields rising on stalled US-Iran peace talks is the cleanest tape link - rates moving on geopolitics is exactly what feeds cross-asset MOVE/VIX coupling.

ECB credit-tightening survey is the credit-channel data point Dimon was warning about - tangible evidence the Iran-war shock is reaching bank lending.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.50 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.41 against a spot of 710.28. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.2% with a volatility risk premium of 1.58%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.50. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime