Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

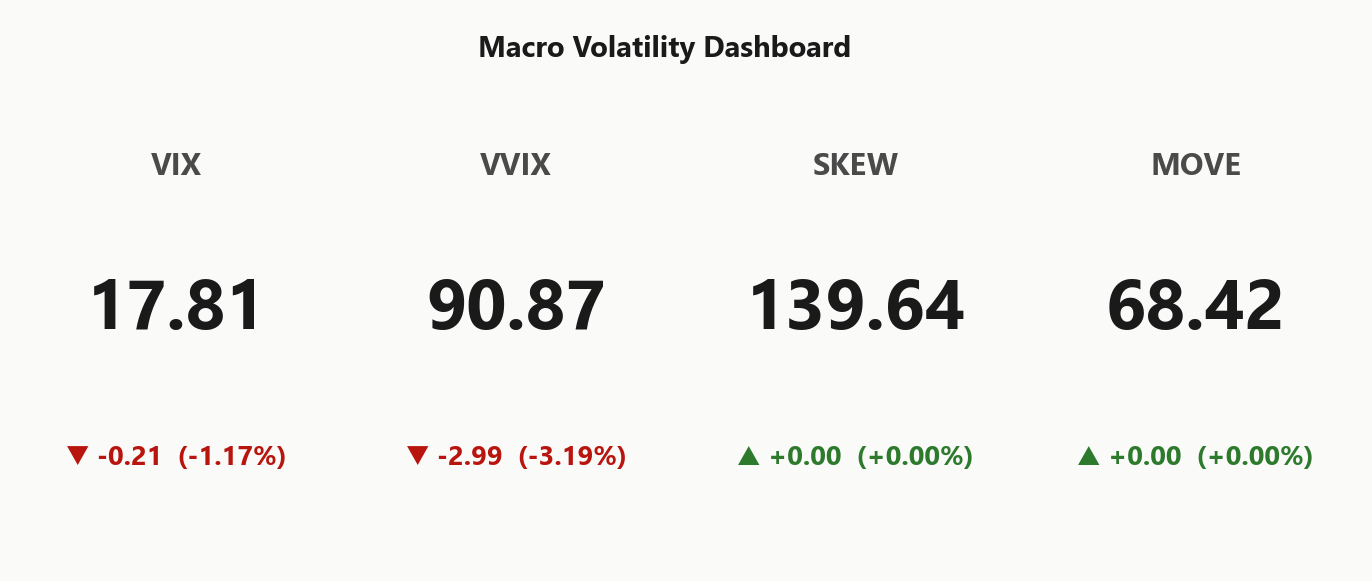

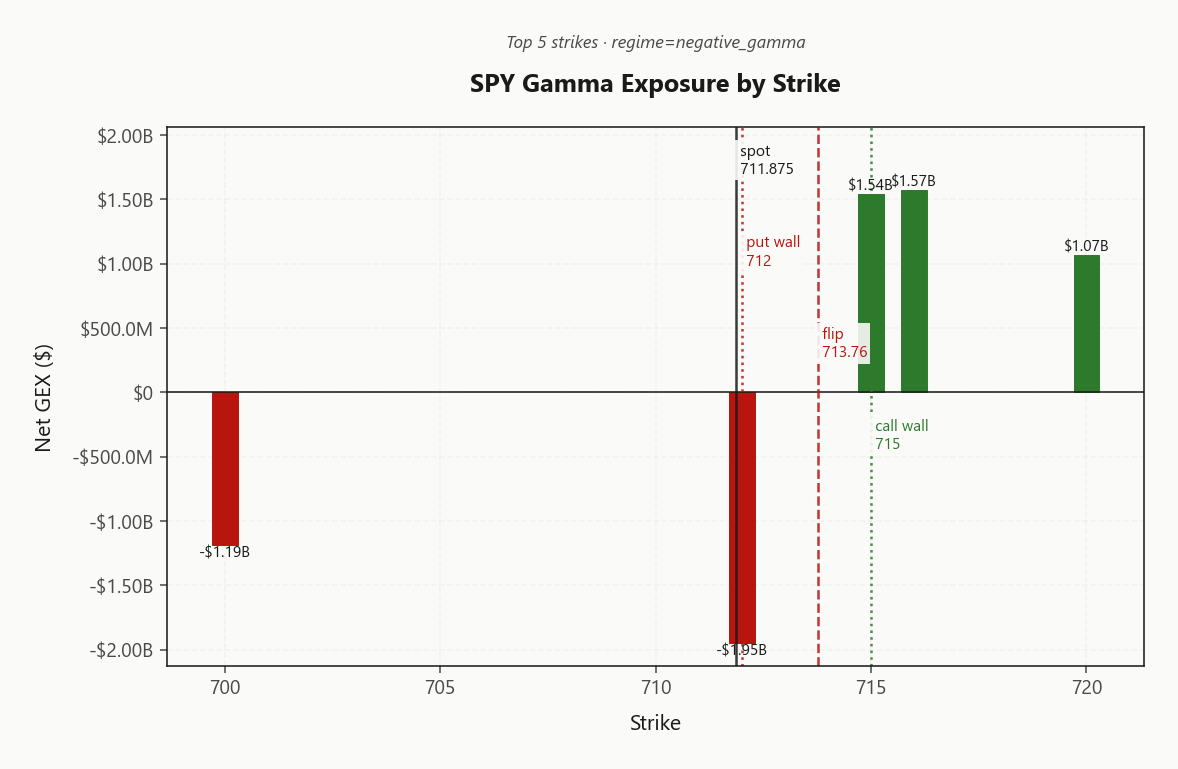

SPY closed at 711.88 sitting fractionally below the 713.76 gamma flip - net GEX at -$2.33B confirms a Negative Gamma regime where dealers amplify rather than dampen. Key levels: call wall 715.00, put wall 712.00 (spot is pinned right on it), max pain 695.00 sits well below - gravity is downside if the put wall breaks. Dealer positioning is hostile: net VEX -$206.55B means a vol uptick forces dealers to sell delta, and net CHEX -$908M adds time-decay selling pressure into close. Vol read: VIX 17.81 with VIX9D 16.61 below VIX3M 20.51 keeps the curve in contango and VRP at 0.68% - vol carry intact but thin. VVIX at 90.87 rules out jump-risk panic. Bottom line: trade Iron Condor structures in the 30-45 DTE window, but a confirmed break of 712.00 flips dealers to amplifier-sell mode toward 695.00.

Negative gamma across SPY/QQQ/IWM with spot pinned at 712.00 - moves amplify in either direction

Index complex sits in Negative Gamma with spot fractionally below the 713.76 flip - dealers amplify direction, not dampen it. VIX term structure stays in Contango and VVIX at 90.87 keeps vol-of-vol benign, so the carry trade isn't broken - but Iran-war headlines and the 154.6%% 0DTE concentration mean intraday tape can whip violently around 712.00.

Regime Assessment

Tape sits in Elevated territory - Elevated / Watchful - with VIX at 17.81 parked squarely in the watchful band. Not panic, not complacent; the kind of read where you size for persistence but keep the tail-hedge phone number on speed dial.

Transition math says base case is mean-reversion: to-low probability over ten sessions runs 0.45 while the slip-to-panic tail across five sessions sits at 0.05 - small, not zero, and Iran headlines plus Negative Gamma fragility keep that tail live. Half-life of 15 sessions confirms the regime is sticky, not transient - fade the noise, respect the level.

Translation for the book: pay attention, don't flatten. Iron Condor structures still earn their carry while VVIX at 90.87 stays in Normal - the green light hasn't flipped, but the charm pivot at 712 is the line where watchful becomes urgent.

What it means for your trading

Regime registers Elevated / Watchful with a sticky 15-session half-life - base case mean-reversion, but the path to panic is non-trivial while spot pins the put wall.

Trading readVIX up modestly, VVIX calm, MOVE flat, SKEW elevated - equity surfaces price tail risk but rates and vol-of-vol don't confirm. Divergence usually means one side gives; watch VVIX for the tell.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

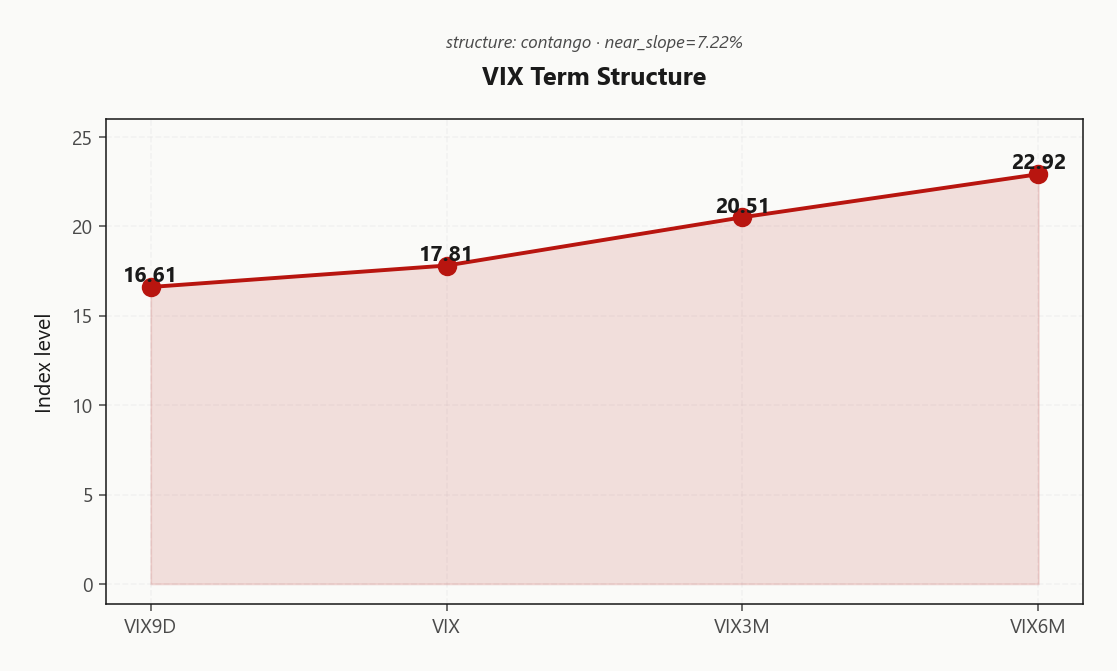

The VIX curve stacks cleanly: 16.61 on the front, 17.81 spot, 20.51 at three months, 22.92 at six - textbook Contango. Near-term slope of 7.22%% says no event premium is piling into the front month despite the Iran headline tape. This is the Steep contango - vol sellers favored regime, and it is the single most important confirmation that vol carry remains intact even with the index complex pinned in negative gamma.

Forward implieds price the back of the curve rich: 21.7345830418 across the 30 - 60 window, 25.0996553761 further out. That geometry hands the edge to sellers in the 30-45 bucket, where forward vol is richest and 0DTE noise is sidestepped. Front-month decay is shallow, back-month carry is fat - calendarize accordingly.

What it means for your trading

Contango from 16.61 through 22.92 with no front-end event bid keeps the carry trade open; harvest forward vol in the 30-45 window where the curve pays best.

Trading readHealthy contango with VIX9D well below VIX3M says the carry trade is alive and the market does not expect imminent stress - but that's exactly when complacency snaps if Iran headlines escalate.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV carries a Thin Premium over recent realized: SPY HV20 at 14.43 against ATM IV 15.11% prints VRP at 0.68% - a cushion, not a windfall. Five-day realized at 10.73 sits well below HV20, and HV60 15.48 running above HV20 confirms realized has decelerated into the print. Options aren't expensive versus what tape is actually delivering - the short-vol case is alive but thin, and the regime can only support structures that cap the tail.

The cross-section tells a sharper story: 4.18% on QQQ dwarfs the SPY cushion, with tech-heavy realized cooling into a still-bid implied surface. That dispersion is where the harvest sits - index VRP is positive but slim, single-asset VRP in the Nasdaq complex is doing real work. Iron condor scoring at 33 reflects the thin-but-positive edge: defined-risk theta clears the bar, naked strangles do not.

Trade structures that limit tails - Iron Condor in the 30-45 window favors QQQ as the venue, SPY as the lighter-weight expression.

What it means for your trading

VRP is active but slim on SPY at 0.68% - the Thin Premium read keeps short-vol harvesting positive-EV only via tail-capped structures, with QQQ's richer 4.18% the standout venue.

Skew Convexity

SPY's quarter-delta put prints 18.7% against ATM at 16.56% and the call wing at 15.38% - downside is paying up, upside is going begging. Skew sits at 3.32% with smile ratio 1.22%: elevated, as the Negative Gamma regime demands, but ordered. The curve is pricing protection, not catastrophe.

The flat-to-ATM call wing is the tell - no one's reaching for upside convexity, which is consistent with spot pinned at the put wall and dealers amplifying directional breaks rather than dampening them. With VVIX at 90.87 in the Normal band, the surface isn't bimodal and tail premium isn't bid for a jump.

Trade implication: put spreads dominate outright puts here - you're funding the long leg with a wing that's already paying a premium, and the ordered curve says naked tail convexity is overpriced relative to the realized risk. Reserve outright tail buys for a confirmed VVIX expansion; until then, finance the hedge.

What it means for your trading

Quarter-delta put skew at 3.32% with smile ratio 1.22% signals elevated-but-ordered downside pricing - favor put spreads over naked puts and chase tail convexity only on a VVIX break.

Vol-of-Vol Structure

VVIX at 90.87 sits squarely in the Normal band - no panic premium on vol itself, no bimodal pricing creeping into the surface. The VVIX/VIX ratio at 5.10 registers as Normal, which is the cleanest tell that the market is not paying up for jump risk despite the headline tape. Vol-of-vol is the discipline check on every other signal in this book, and right now it isn't flashing.

Sizing follows directly: Standard Size - no haircut, no half-size defensive crouch. Iran-war headlines have flowed across screens for sessions without bidding VVIX off its anchor; the surface treats the geopolitical overlay as priced-in rather than as a binary waiting to detonate. With VIX at 17.81 and the convexity bid quiet, short-vol structures don't need to compensate for a fat-tail premium that isn't actually being charged.

This is the green light beside a yellow gamma backdrop - trade Iron Condor at standard clip, but stay alert: the moment VVIX expands while spot sits below the 712 pivot, the green flips and the carry breaks fast.

What it means for your trading

VVIX at 90.87 in Normal regime green-lights Standard Size on defined-risk vol carry - but the signal inverts the instant vol-of-vol expands while spot trades below the charm pivot.

Dispersion Spread

Index IV reads 15.11% against QQQ at 22.29% - the spread says tech is carrying the idiosyncratic load while the index surface stays comparatively well-behaved. Cross-strike dispersion at 63.29 versus cross-expiry at 2.16 reinforces the read: it's the smile, not the term structure, doing the work. Corning-style earnings noise and the parabolic-stock pullback are repricing single names, not the system.

IWM at 21.29% slots between SPY and QQQ - small-cap realized has caught up enough that the index is no longer the cheap-vol outlier, confirming the dispersion is concentrated in megacap tech rather than broad risk repricing. Cross-asset regime stays Aligned, so this is dispersion within a coherent tape, not a regime fracture.

Trade implication: harvest VRP via single-name vol sales in tech megacaps where premium is genuinely rich; keep index exposure in defined-risk iron condors anchored at 715.00 / 712.00. Naked single-stock structures into earnings-noise season are the wrong tail to short.

What it means for your trading

Dispersion sits in megacap tech, not the index - sell single-name vol where QQQ's 22.29% premium pays, keep index trades defined-risk.

Liquidity & Microstructure

The chain's center of gravity and its combat zone aren't the same place. 600 carries the highest open interest - long-dated put hedges anchored well below spot - but the active gamma battlefield sits between the put wall at 712.00 and the call wall at 715.00. That's where dealer flow lives today, and spot is pinned right on the floor.

The top strike 712.00 carries net GEX -$1.95B - the put wall is the pivot, not a level near it. The gamma flip at 713.76 sits a hair above spot; every uptick toward it shifts dealer flow from amplifier-sell to amplifier-buy. Below the put wall, dealers sell into weakness toward 695.00; above the flip, they buy strength into 715.00.

Trade the levels - don't fade them. Anchor structures at the walls, treat 712.00 as a trapdoor on confirmed break, and respect that 154.6% of total GEX in 0DTE means intraday whip dominates multi-day positioning.

What it means for your trading

OI sits at 600 but the day's combat zone is 712.00 - 715.00, with spot pinned exactly on the put wall. A confirmed break flips dealers to amplifier-sell mode toward 695.00; a reclaim of 713.76 inverts the flow.

Trading readShort-gamma profile with the put wall at 712.00 acting as a trapdoor and call wall at 715.00 acting as a magnet - dealers amplify any directional break, so trade the levels, don't fade them naively.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order Greeks line up against the tape. Net VEX at -$206.55B means any uptick in 17.81 forces dealers to sell delta into weakness, while net CHEX at -$908M layers charm-driven supply into the close. Vanna and charm point the same way - the worst possible combination if vol expands from here.

The charm pivot sits at 712, a Put Wall with current bias Neutral. Distance to pivot is only 0.0175592625 - knife-edge. Spot is fractionally below, so dealers already lean short delta; a confirmed break activates the accelerant.

Watch 90.87 as the trigger. If VVIX expands while spot trades under the pivot, vanna selling and charm selling compound into a self-reinforcing downside cascade toward 695.00. The single level that matters tomorrow is 712.

What it means for your trading

Vanna and charm both hostile with the pivot at 712 only 0.0175592625 away - a VVIX expansion under that level converts dealer flow into an accelerant, not a stabilizer.

Cross-Asset Confirmation

Cross-asset tape refuses to confirm the equity fragility. MOVE at 68.42 sits benign - the bond surface is unbothered by Iran headlines, and credit is not pricing a macro shock. Fear & Greed clocks 64 in Greed territory, the opposite of panic positioning. VIX term structure holds Contango, so the carry geometry is intact and the rates/vol channel agrees with the bond read.

Inside the equity complex, QQQ at 657.99 and IWM at 274.14 sit in an Aligned regime alongside SPY - every index short gamma at once, no diversification across the book. Tone reads Unknown: equity-specific gamma fragility meeting risk-on positioning at the margin, not a compounding credit cascade.

Trade implication: Iran-driven dislocations are mean-reversion candidates while MOVE stays flat and VVIX at 90.87 holds normal. The tell that flips this thesis is MOVE waking up - until then, headline drawdowns are buyable inside the equity book, not hedged across asset classes.

What it means for your trading

Cross-asset signals stay Aligned with MOVE at 68.42 and Fear & Greed in Greed - equity gamma fragility is isolated, not systemic, so fade headline shocks inside the index complex until the bond surface confirms.

Scenario EV

The EV stack tilts decisively to Iron Condor structures - the model prints a best score of 33 against a put-spread alternative at 22. Steep contango from 16.61 through 20.51, a Normal VVIX at 90.87, and a thin-but-positive VRP at 0.68% all reward defined-risk theta - this is exactly the regime where four-legged, capped-tail structures monetize carry without paying for the privilege.

Sweet spot is the 30-45 DTE window where forward vol prints richest - 21.7345830418 on the 30-to-60 segment - far enough out to dodge the 0DTE noise concentrated at 154.6% of total GEX, close enough that theta carries. Anchor the wings at the 715.00 call wall and 712.00 put wall - natural dealer pivots, not arbitrary deltas. Size Standard Size; VVIX in Normal regime rules out a jump-risk haircut.

Hard pass on naked strangles. With spot pinned below the 713.76 flip in a Negative Gamma regime, dealers amplify on a break - uncapped tails aren't theoretical. Put spread at 22 stays viable only if you want the directional bias.

What it means for your trading

Trade Iron Condor in the 30-45 window, wings anchored at 715.00 / 712.00, sized Standard Size. Avoid naked strangles - negative gamma below the flip turns capped-risk theta into the only defensible vol-seller geometry.

Actionable Summary

Trade Iron Condor structures in the 30-45 DTE window, anchored at the 715.00 call wall and 712.00 put wall, sized standard. The regime is Elevated / Watchful: Negative Gamma with spot pinned fractionally below the 713.76 flip, but Contango term structure and VVIX at 90.87 keep the carry trade alive. Iron condor scoring at 33 beats the put spread alternative at 22 - defined-risk theta wins when VRP at 0.68% is thin but positive.

Watch the 712Put Wall like a hawk. Distance to pivot at 0.0175592625% is knife-edge - a confirmed break flips dealers from amplifier-neutral to amplifier-sell with net VEX -$206.55B and net CHEX -$908M converting any vol uptick into self-reinforcing supply toward 695.00.

Avoid naked strangles, naked single-name tech vol sales, and 0DTE-heavy longs - 154.6%% 0DTE concentration plus Iran tail makes undefined risk uneconomic. Hedge tail via VIX call spreads if VVIX breaks higher; the current Normal regime is the green light, not the all-clear.

What it means for your trading

Sell defined-risk vol in 30-45 DTE at the 715.00/712.00 walls while Contango and Normal VVIX persist. A confirmed break of the 712 pivot flips bias and demands tail hedges via VIX call spreads.

Trump approval at new low with Iran-war cost-of-living concerns is the political-economy backdrop pressuring consumer-discretionary multiples and feeding the persistent skew bid.

US pump prices near 4-year high directly threatens the consumer-spending tail that the index complex has been leaning on - energy passthrough into core CPI watch.

UAE leaving OPEC is a structural energy-market shock; could force oil to re-price and reactivate the inflation/rates channel that MOVE has so far ignored.

Jamie Dimon's bond-crisis warning is a tail-risk reminder; if it gains traction, MOVE wakes up and the cross-asset 'aligned' regime breaks first in rates.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.83 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.76 against a spot of 711.88. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 15.11% with a volatility risk premium of 0.68%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.81. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime