Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

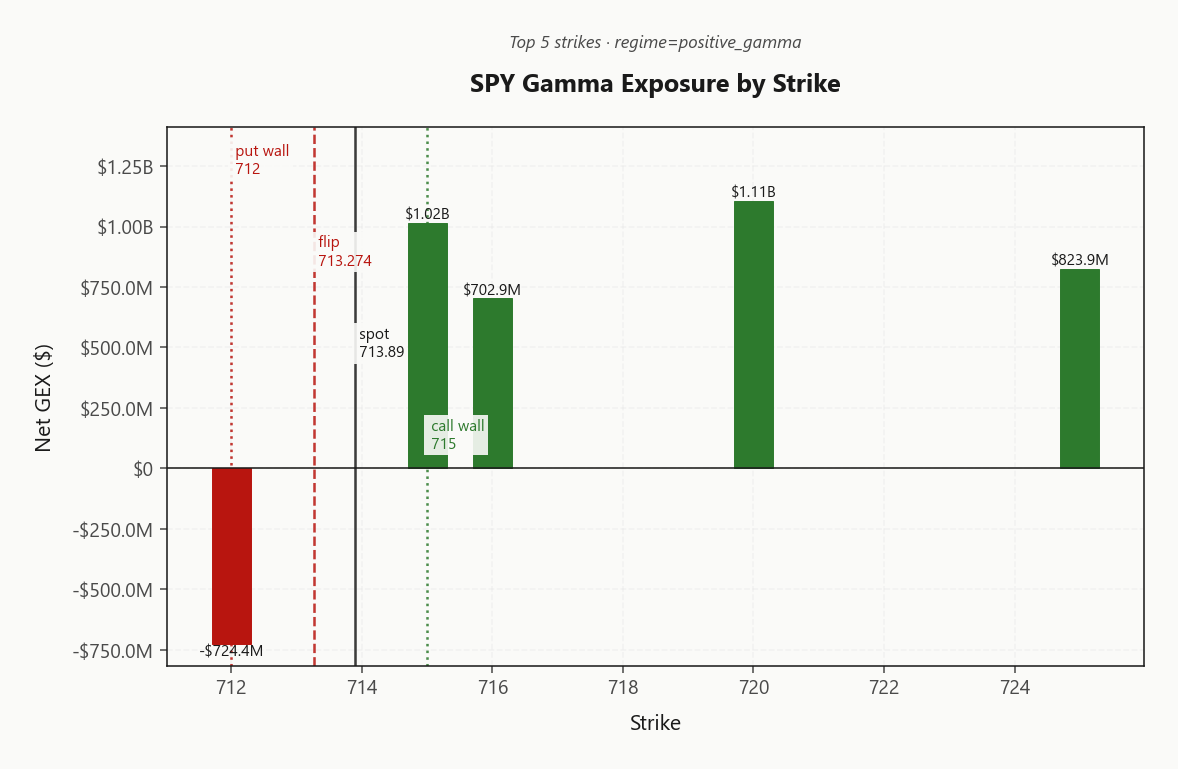

SPY at 713.89 holds the positive-gamma regime with net GEX at $1.11B and dealers leaning into mean-reversion. Call wall sits at 715.00, put wall at 712.00, and the gamma flip at 713.27 - spot is -0.0862630825 above flip, a thin cushion that keeps dealer flow supportive but punishes any breach. Vanna at -$223.34B says a vol spike flips dealers into delta-selling fast, and charm at -$10.5M pressures into the close. VIX at 18.53 with VIX9D/VIX3M structure Contango and slope 5.52%% pays carry, while VVIX at 95.84 sits in normal sizing range. VRP at 1.18% keeps options modestly rich to realized - Iron Condor in the 30-45 bucket scores best. Bottom line: fade strength into 715.00, defend below 713.27, and respect IWM's negative-GEX warning as the early break signal.

Positive gamma across index complex with VIX in contango - mean-reversion regime, vol sellers favored

SPY at 713.89 sits just above 713.27, keeping the index complex in dealer-long-gamma territory while VIX in contango at 18.53 reinforces the suppressive regime. The cushion is real but thin - only -0.0862630825 above the flip - and IWM's negative net GEX flags the small-cap tape as the fragile leg if the Iran-driven macro overlay reasserts. Mag-7 earnings week plus geopolitical premium argue against naked short vol; structured 30-45 DTE iron condors fit the VRP and vol-of-vol setup.

Regime Assessment

Regime tape reads Elevated / Watchful with the current state classified as Elevated and VIX parked at 18.53 - the elevated-but-not-stressed band where vol sellers still get paid but the cushion is no longer free. Half-life of 15 sessions argues this state is sticky; mean-reversion remains the base case and the transition matrix prices a 0.45 probability of decaying back to low over the next ten sessions.

The asymmetry sits in the tail. Conditional probability of jumping to panic over five sessions reads 0.05 - small in isolation, but the Iran overlay stacked against Mag-7 earnings week is exactly the kind of two-catalyst window that fattens the left tail beyond what the unconditional model assumes. Cross-asset tape stays Aligned, which keeps the regime hinge intact rather than already-broken.

Trade the sticky base case, respect the conditional jump. Carry the VRP, defend the flip, and treat any breach of 713.27 as the early read that the regime is migrating, not chopping.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - sticky enough to harvest, fragile enough that the 0.05 jump probability into Iran/earnings week deserves real respect.

Trading readVIX, VVIX, and MOVE all sit in normal-to-elevated zones with no divergence - the dashboard says contained risk, not crisis; F&G in greed reinforces the complacency-with-cushion read.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

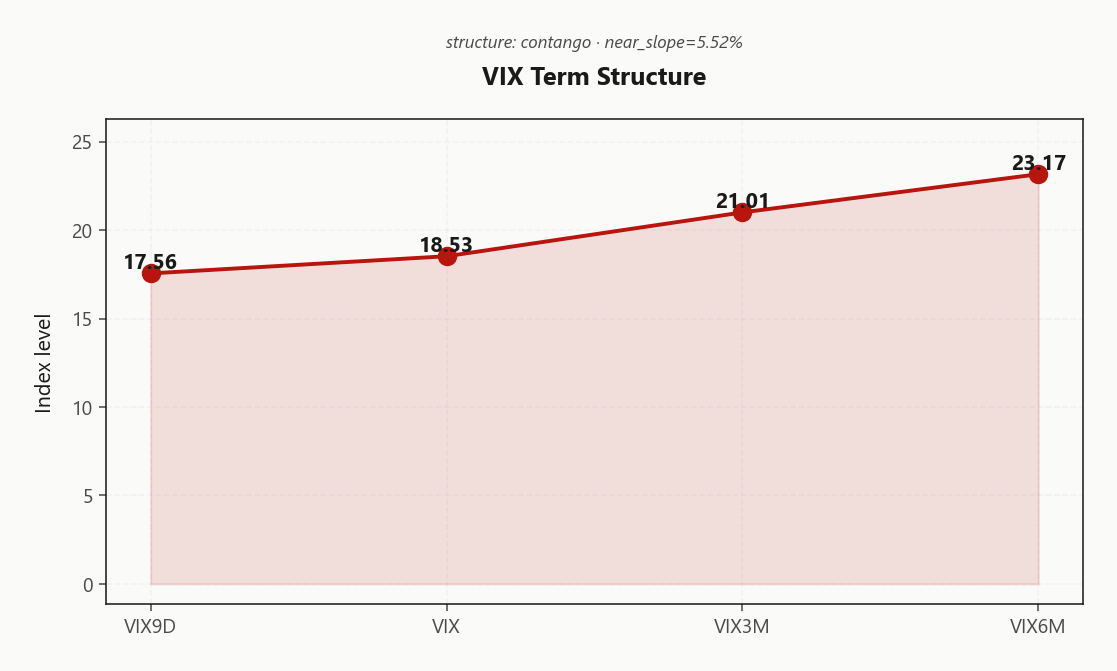

The VIX curve prints textbook Contango with VIX9D at 17.56 sitting under spot VIX at 18.53 and VIX3M anchoring the back at 21.01 - no near-term event premium baked in despite the Iran tape and Mag-7 reporters. Near-slope at 5.52%% confirms the carry trade is paid, and the regime label Steep Contango classifies the backdrop as unambiguously vol-seller-favored.

Forward 30-to-60 vol resolves at 22.1460989793, the cleanest bucket for calendar carry - long enough to dodge the 0-5 DTE event-pricing distortion, short enough to keep theta dense. Front-month VIX future at 21.01 against a spot basis of 13.38%% says roll-down still pays into the front.

Trade the curve, not the tape: sell front, own the 30-45 bucket, and respect that a single Hormuz headline can flatten the slope before the carry monetizes.

What it means for your trading

Steep contango with VIX9D under spot VIX and a positive near-slope keeps the curve paying sellers - best edge sits in the 30-45 window where forward 30-to-60 vol at 22.1460989793 prints cleanest carry without hugging the event strip.

Trading readSteep contango with VIX9D below spot VIX = no near-term event panic priced; the carry trade pays, but be aware the slope can flatten fast on a single Iran headline.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY's 14.35 HV20 sits below ATM IV at 15.53%, leaving VRP at 1.18% - options modestly rich to realized but inside normal harvest range, not extended. The IV/RV read is Thin Premium: harvestable, not generous.

RV5 at 11.47 tracking under RV20 of 14.35 says realized has been decelerating into Mag-7 prints - the setup where a stable IV print does the VRP a favor as the realized leg keeps fading. Watch for any RV re-acceleration off earnings tape; that is what flips the premium from thin to fat.

Cross-asset, 3.36% QQQ VRP carries more juice than SPY given concentrated single-name risk, while 2.64% IWM VRP splits the two. Index vol selling stays favored; reach for QQQ structures where the carry actually pays.

What it means for your trading

SPY VRP at 1.18% is positive but compressed with RV decelerating - a clean but unspectacular short-vol backdrop where QQQ at 3.36% offers the richer harvest into Mag-7 week.

Skew Convexity

The quarter-delta skew is doing the talking across the index complex: SPY put wing prints 14.85% against a call wing at 11.83% and ATM at 12.47% - a clean 3.02% vol-point premium for downside convexity with no offsetting bid in the upside wing.

Smile ratio at 1.26% sits firmly above parity but reads as ordered steepening, not panic convexity - the put bid is structural hedge demand layered onto the Iran tape, not a tail-grab. Call wing flatness corroborates: no one is paying up to chase strength into 715.00, and QQQ's richer ATM at 21.32% versus SPY's 15.53% says the convexity bid is concentrated where Mag-7 prints, not broad.

Trade expression: put debit spreads dominate naked puts on this surface - you are funded by the flat call wing and the ordered (not convex) tail. Pair against iron-condor VRP harvest in the 30-45 bucket; skew this steep punishes the unhedged short-put leg if the cushion at 713.27 breaks.

What it means for your trading

Quarter-delta skew at 3.02% vol points with smile ratio 1.26% prices downside as the concern, not upside chase - favor put debit spreads over naked puts and let the flat call wing fund the structure.

Vol-of-Vol Structure

VVIX at 95.84 against VIX at 18.53 prints a ratio of 5.17 - squarely inside the Normal band. No convexity bid, no jump premium, no second-derivative panic. The vol-of-vol surface is telling you the market is not pricing a binary outcome despite the Iran tape stacking against Mag-7 earnings week - and that, in itself, is the complacency tell worth respecting.

Sizing guidance reads Standard Size with signal color Green - green light for VRP harvest at full size on defined-risk short-vol structures. The absence of a VVIX bid means the cheap convex tail isn't there to lean on; if a headline forces the convexity repricing, it happens from a standing start and moves fast. Standard sizing, not hero sizing.

What it means for your trading

VVIX at 95.84 with the ratio at 5.17 clears full-size VRP harvest, but the Normal read into a loaded macro/earnings tape means any convexity repricing starts from zero - defined-risk only.

Dispersion Spread

Cross-sectional vol is doing the talking. QQQ ATM IV at 21.32% sits well clear of SPY at 15.53%, a gap that says the tape is pricing idiosyncratic Mag-7 dispersion, not a broad market shock. With NVDA, MSFT, META, AMZN all printing into the same window, the index is effectively a basket of single-name event premium - and the hedges sold against the basket consistently underpay for the actual realized surface that earnings deliver.

Cross-strike dispersion of 76.52 against cross-expiry of 1.83 reinforces it: the smile is wider than the term, meaning the market is pricing path-dependent strike risk over duration risk. That's a name-specific signature, not systemic stress, and dovetails with Aligned regimes across the index complex.

Trade expression follows: sell index vol, buy single-name convexity. Iron condors on SPY in the 30-45 bucket harvest the underpriced index surface; long single-name straddles or directional risk-reversals on the reporters capture the dispersion the index is suppressing. Avoid using SPY puts to hedge a Mag-7 book - the basis works against you.

What it means for your trading

QQQ ATM IV at 21.32% versus SPY at 15.53% flags single-name dispersion as the dominant risk axis this week - sell the index, own the names.

Liquidity & Microstructure

The book is anchored above spot: top strike at 720.00 carries net GEX of $1.11B, acting as a magnet and an upside dampener as dealers fade strength into the 715.00 call wall. The highest-OI strike sits at 600, far below spot - structural support, not an active line, but a reminder of where the legacy positioning still lives.

The regime line is the gamma flip at 713.27, just -0.0862630825 from spot. Above it, dealer flow is the cushion: buy dips, sell rips, mean-revert into the call wall. Below it, the same mechanics invert and amplify - the 712.00 put wall becomes the first defended line and any breach hands the tape to negative-gamma reflexivity.

Trade the band: fade pops into 715.00, defend 712.00, and treat 713.27 as the binary switch. Cushion is real but thin; respect it.

What it means for your trading

Microstructure is supportive while spot holds -0.0862630825 above the 713.27 flip, with the 720.00 OI cluster pulling as a magnet into the 715.00 call wall. A break of the flip flips the cushion to amplifier - that is the line that matters.

Trading readGamma stacked above spot through the call wall acts as a rubber band - fade rallies into 715.00, expect dealer dampening unless spot breaks 713.27, in which case the cushion flips to amplifier.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX at -$223.34B is the tell - deeply negative, which means any vol pop forces dealers to sell delta into weakness. The positive-gamma cushion holds the tape mean-reverting in calm conditions, but the vanna channel is the trapdoor: a VIX lurch and the same desks that were buying dips become the marginal sellers.

Charm at -$10.5M still pays into the close while spot holds north of the pivot. The line that matters is 713.2741764802 - current bias reads Supportive as long as we sit above it, hostile the moment we don't. Cushion to the pivot is -0.0862630825, thin enough that one Iran headline does the work.

Charm is supportive into the close while SPY holds above 713.2741764802, but vanna at -$223.34B means a vol spike flips dealer flow from dampener to accelerant - the pivot is THE level for the day.

Cross-Asset Confirmation

Cross-asset tape reads Aligned: MOVE at 66.97 sits stable, telling you the rates desk is not pricing the Iran headlines as a credit shock, while Fear & Greed prints Greed at 67 - sentiment leaning constructive, not defensive. The bond-vol-quiet, equity-bid combination is the classic positive-gamma backdrop that lets dealers absorb headline noise rather than transmit it.

QQQ at 662.61 confirms the SPY tape with regime label Positive Gamma, both indices anchored above their flips and feeding the same mean-reversion impulse. The lone fragile leg is IWM at 276.67, where net GEX prints -$679.4M - small-cap dealer flow inverts on a break and would lead any unwind. Watch IWM as the canary; SPY/QQQ are followers if the regime cracks.

Cross-asset tone Unknown, regime aligned with one fragile flag - fade strength into 715.00, defend below 713.27, treat IWM as the early break signal.

What it means for your trading

Equity tape is digesting Iran/earnings risk through a positive-gamma cushion with MOVE at 66.97 and F&G at 67 reinforcing the contained-shock read. IWM's negative net GEX at -$679.4M is the divergent tell - the first place a regime break shows up before SPY/QQQ confirm.

Scenario EV

The scoring board lands on Iron Condor as the cleanest expression at 54, decisively ahead of the put spread alternative at 43. Positive gamma across the index complex, VIX term structure in Contango, and VVIX parked in the Normal band stack the regime in favor of premium harvest without a directional lean - collect the VRP, let dealers do the dampening work.

The DTE sweet spot is 30-45, threading the needle between the 0DTE charm whip and the longer-dated event-pricing distortion. VRP assessment reads Unknown, so structure beats raw richness - defined wings around the 715.00 ceiling and the 712.00 floor frame the body. Sizing stays Standard Size; VVIX is not flashing convexity panic.

Discipline points: anchor the regime read on 713.2741764802 and respect IWM's negative-leaning microstructure as the early break tell if the macro overlay reasserts.

What it means for your trading

Iron Condor at score 54 in the 30-45 bucket is the cleanest VRP harvest given positive gamma plus contango plus normal vol-of-vol. Keep sizing Standard Size and pivot off 713.2741764802.

Actionable Summary

SPY holds above the gamma flip at 713.2741764802 with the index complex parked in Positive Gamma territory and VIX in Contango - a textbook mean-reversion backdrop, but the cushion is only -0.0862630825 deep. Lean into Iron Condor structures in the 30-45 bucket to harvest the 1.18% VRP without picking direction; Standard Size applies given VVIX at 95.84.

Fade strength into the 715.00 call wall and defend the 712.00 put wall - break of the flip flips dealer flow from dampener to amplifier, and net VEX at -$223.34B means a vol spike forces delta-selling fast. Avoid naked short vol into Mag-7 earnings plus the Iran tape; IWM's negative net GEX is the early-break signal if the macro overlay reasserts. Regime tag: Elevated / Watchful, half-life 15 sessions.

What it means for your trading

Sell Iron Condor at 30-45 DTE around current spot, fade into 715.00, and treat 713.2741764802 as the regime hinge - IWM's negative GEX is the canary.

Iran tanker blockade and sparse Hormuz traffic = direct oil/inflation transmission channel; the geopolitical premium is the single biggest non-earnings macro factor on the tape today.

Earnings-heavy week framing matters - Mag-7 prints concentrate index realized vol and explain why QQQ ATM IV is well above SPY despite aligned regimes.

Putin-Iran alignment escalates the geopolitical risk surface materially; if the tape starts pricing a wider conflict, MOVE and VVIX would be the first to crack.

Iran war's emerging-market spillover speaks to credit/contagion risk - the channel that would flip this from contained-shock to systemic-shock if it broadens.

Calls richer than puts across this week's Mag-7 reporters with GOOGL the only contrarian print = positioning is long-skewed into earnings, magnifying disappointment risk.

Gold rally resumption with Iran-conflict overlay = real-asset bid persisting; cross-asset confirmation that the geopolitical premium is structural, not one-day.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.55 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 713.27 against a spot of 713.89. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 15.53% with a volatility risk premium of 1.18%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.53. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime