Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

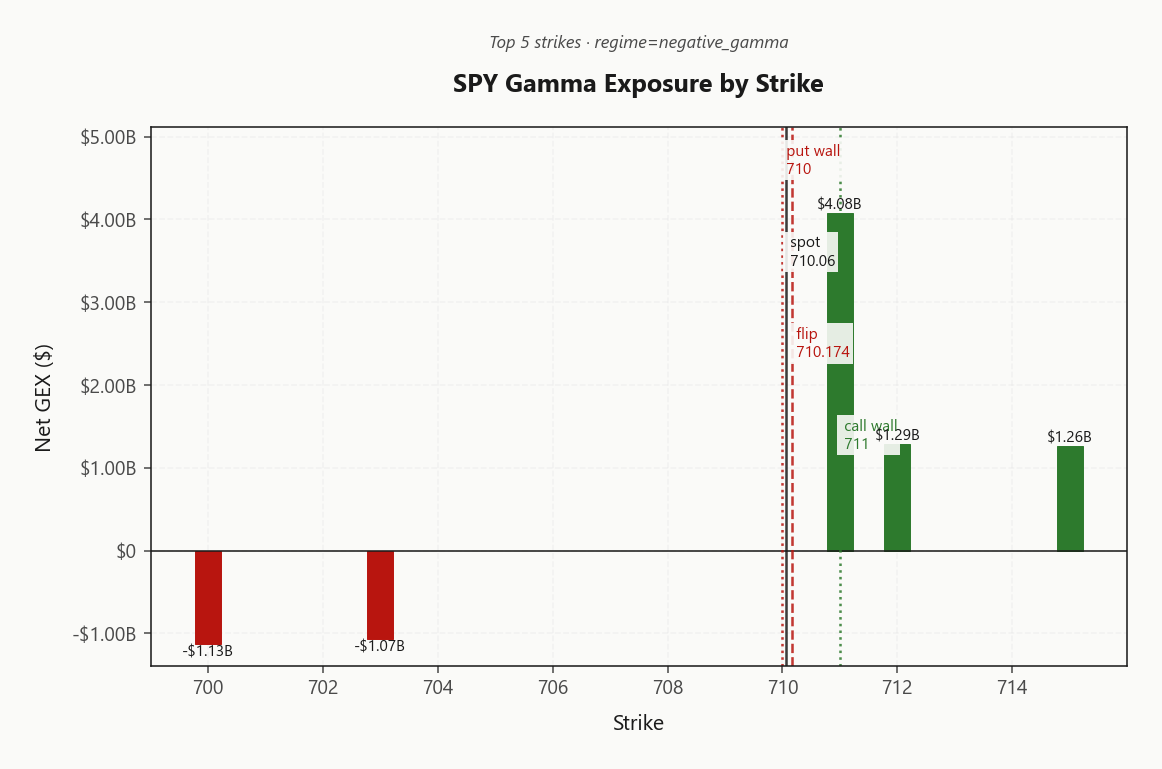

SPY at 710.06 sitting right on the gamma flip at 710.17 with net GEX at -$2.17B - dealers are short gamma here, so any break amplifies. Call wall 711.00, put wall 710.00, and the flip all cluster within a handful of handles - this is a pin-or-break setup, not a trend day. QQQ is the cushion: net GEX $3.15B with spot well above flip 644.80 (Positive Gamma), so tech mean-reverts while SPY whips. IWM remains fragile at -$1.2B - Negative Gamma with put wall 275.00 defining the fail line. Vanna is a hostile -$218.28B - any vol pop sells dealer delta and feeds downside; charm pressure (-$741.2M) tilts the same way into Friday close. Vol read: VIX 19.14, VIX9D 18.04 under VIX3M 21.48 - Steep Contango, VRP still active (0.11% for SPY, 2.14% for QQQ). VVIX 98.57 is benign (Normal), so Standard Size. Bottom line: fade extremes into the 711.00/710.00 walls with Iron Condor structures in the 30-45 DTE pocket; abandon the mean-reversion thesis if SPY closes decisively below 710.00.

SPY pinned at gamma flip in steep contango; QQQ cushion holds while IWM stays fragile - Elevated / Watchful

SPY trades directly on its gamma flip at 710.17 with dealers short gamma, while QQQ sits well above its flip in positive-gamma territory - a classic Qqq Heavier divergence. Steep contango (Steep contango - vol sellers favored) and normal vol-of-vol (Normal) favor premium sellers, but IWM's negative-gamma fragility and Iran-war headlines keep tail hedges relevant. Bottom line: carry is there, but size through the SPY flip line.

Regime Assessment

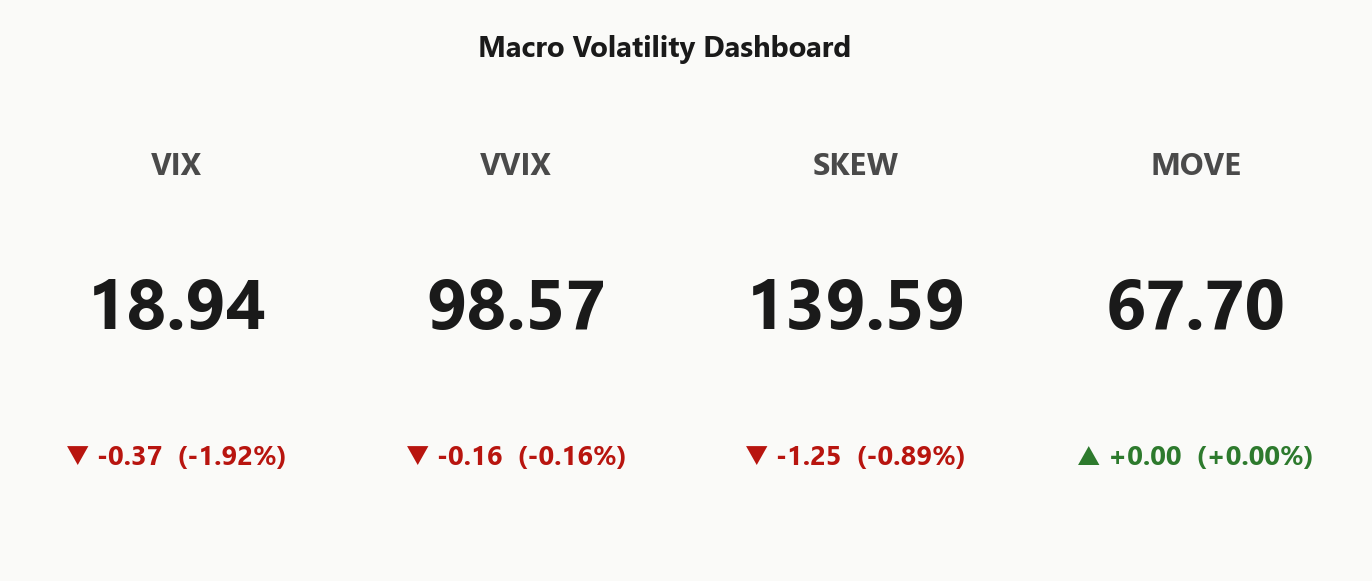

The tape is parked squarely in an Elevated / Watchful regime - VIX at 18.94 is neither the lullaby of a compressed-vol grind nor the scream of a panic print. This is the middle band where dealers still hedge meaningfully, skew stays bid, and headline tape makes the path jumpy without actually breaking the structure.

The transition math backs the sit: probability of rolling into panic over the next five sessions is only 0.05, while the drift toward a lower-vol regime over ten sessions runs 0.45 - the asymmetry says the next leg is more likely down-in-vol than up-in-vol, barring a fresh Iran-war escalation. Half-life of 15 sessions confirms it: Elevated is sticky, not a waystation.

Trade the regime, don't fight it. Premium-selling structures get paid, tail hedges stay on the book cheap, and sizing stays standard until VVIX or MOVE tells you the backdrop has changed.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - panic transition odds of 0.05 are low, so plan for weeks of this tape, not days. Harvest the carry, keep the hedge, don't chase a regime break that the transition matrix says is unlikely.

Trading readVIX fading, VVIX flat, SKEW elevated but not extreme, MOVE unchanged - the macro dashboard is CONFIRMING a structural-greed regime, not warning of an imminent break; the Iran headlines are being treated as noise by the vol complex.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

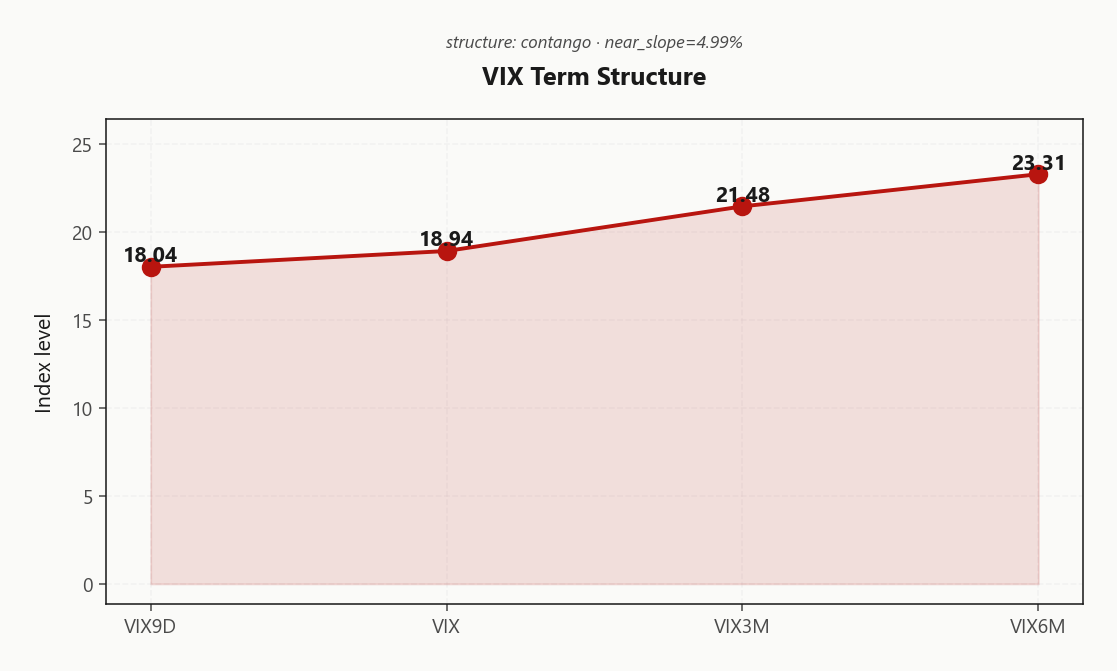

Term structure is in Contango with VIX9D at 18.04 printing below spot VIX at 18.94 - the curve is flatly refusing to price near-term event premium despite the Iran headline overhang. VIX3M at 21.48 and VIX6M at 23.31 stack well above the front, locking in Steep contango - vol sellers favored.

The forward 30-to-60 roll prints 22.6434052209 and the 60-to-90 extends to 25.0064351718 - the slope still pays to own, so the carry trade is structurally intact. SPY's own term walks from a cheap front-week print at 13.1 up into the belly, making 30-45 DTE the harvest pocket where the curve rewards the roll without front-week gamma noise.

Read: sell the belly, respect the front. Front-weeks still carry headline residue and pin-zone gamma; the Steep Contango print is a green light for Iron Condor size in the belly, not in the wings.

What it means for your trading

Curve shape is unambiguously Steep Contango - vol sellers are paid to sit in the 30-45 DTE pocket while leaving front-week Iran-headline premium alone. Structural carry, not event pricing.

Trading read4.99%% near-slope with VIX3M well over VIX confirms the vol-seller carry trade; market does NOT expect stress to materialize in the next quarter.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

Realized is quiet and index implied barely pays for it: SPY ATM IV at 16.54% sits a whisker above HV20 16.43 with HV60 15.39 beneath - a SPY VRP of 0.11% is effectively fair value, not a harvest. The realized tape is not accelerating; HV20 over HV60 is a mild drift, not a regime break.

The premium has migrated to the single-index ETFs. QQQ VRP prints 2.14% and IWM VRP 3.32% - both multiples of SPY's carry and the actual payer for short-vol structures. With ATM IV richer at 21.99% and 23.92%, the dispersion is ordered: index-fair, satellites-rich.

Actionable: sell QQQ and IWM vol against SPY, not alongside it. Use SPY as the hedge leg where index IV is cheap relative to realized, and harvest the satellite VRP where realized has clearly not caught up. Abandon the premium-sell thesis only if HV20 starts tracking above ATM IV into the close.

What it means for your trading

Index VRP at 0.11% is skinny against HV20 16.43; real carry lives in QQQ 2.14% and IWM 3.32%, so sell the satellites and keep SPY as the hedge.

Skew Convexity

Quarter-delta put IV sits over call IV by 3.82% points with the smile ratio printing 1.33% - ordered downside bid, not panic. Put wing at 15.42% pays the convexity premium while the call wing at 11.6% trades essentially flat to ATM 12.94% - zero upside conviction priced into the surface.

SKEW at 139.59 corroborates: the left tail is bid but nowhere near blow-out territory, consistent with the Skew Steep read and the broader Elevated / Watchful backdrop. With vol-of-vol benign at Normal, the market is paying for ordered protection, not jump insurance.

Trade implication: overpaying for naked puts when the wing is this rich is a tax - prefer put spreads to finance the protection, and let the flat call skew fund call-side wings in Iron Condor structures across the 30-45 DTE belly where the surface geometry actually pays.

What it means for your trading

Skew is steep but orderly - puts bid, calls flat, SKEW at 139.59 confirming tail is priced without panic. Sell the wing via spreads; don't buy it naked.

Vol-of-Vol Structure

VVIX prints 98.57 against a VIX of 18.94 - squarely in Normal territory. The VVIX/VIX ratio at 5.20 is consistent with a non-event backdrop: no bimodal tail is being quietly priced, no jump premium layered into the surface. The vol-of-vol complex is not corroborating the geopolitical headline tape.

That greenlights Standard Size on the premium-selling book - no need to halve clips, no need to pay up for wings on a binary-outcome thesis. Pair it with steep contango (Steep contango - vol sellers favored) and the carry trade is mechanically clean: the market is telling you to harvest, not hedge convexity.

The caveat is asymmetric. VVIX can rip fast on an Iran headline, and with SPY vanna hostile at -$218.28B the feedback loop bites hard if it does. Recheck pre-close; a break through 130-handle VVIX is the sizing-halving trigger - until then, standard-clip iron condors in the 30-45 DTE pocket.

What it means for your trading

VVIX at 98.57 with a 5.20 ratio says the tail isn't being priced - standard sizing is validated. Monitor for a VVIX spike on headline risk as the only regime-flip trigger.

Dispersion Spread

Index vol is the cheap leg of the complex: SPY ATM IV at 16.54% sits well under QQQ at 21.99% and IWM at 23.92%, and the VRP print tells the same story - SPY carries a razor-thin 0.11% while QQQ pays a full 2.14% and IWM 3.32% over realized. Selling index vol and sitting flat on single-ETF names is the wrong trade here; the harvest lives one layer out.

Play the dispersion as designed: carry in the single-ETF wings, hedge at the index. QQQ is the cleanest premium seat given its Positive Gamma cushion, while IWM's richer VRP comes with a Negative Gamma tail that argues for defined-risk over strangles. Use SPY - cheap, liquid, aligned with the Qqq Heavier divergence - as the hedge leg rather than the premium source.

Correlation regime is moderate, not crisis-bid, so index hedges bleed more basis than in a stress tape - size the SPY protection accordingly and keep the QQQ/IWM premium book as the earner.

What it means for your trading

Harvest the rich single-ETF VRPs (2.14%, 3.32%) while using SPY's thin 0.11% as the hedge leg - the dispersion trade is carry in the names, protection at the index.

Liquidity & Microstructure

SPY's book is a vice: the gamma flip at 710.17, put wall at 710.00, and call wall at 711.00 cluster inside a handful of handles. That's a pin corridor, not a trend setup - dealers damp above the flip, amplify below it.

The top positive GEX strike at 711.00 prints $4.08B of concentrated dealer long gamma, capping rallies into the wall. Max pain at 695.00 acts as the expiry magnet beneath. Meanwhile the highest total OI sits far below spot at 600 - that's legacy protection stacked in the book, not fresh directional bets, so don't read it as conviction.

Action: the flip line is the coin-flip. Above it, fade extremes into the wall and harvest premium. Below it, dealers sell rips and the put wall becomes the last defensible pin - a decisive break there abandons the mean-reversion thesis and opens air to the OI shelf.

What it means for your trading

SPY's gamma flip at 710.17 is the single actionable line - pin-zone behavior holds above, amplification kicks in below. Trade the 710.00/711.00 corridor, not direction.

Trading readSPY's positive gamma stacks tightly at the call wall and fades just below spot - dealers dampen above the flip and amplify below it, so the 710.17 line is the single coin-flip level for the day.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Vanna is the hostile greek on the board: SPY net VEX sits at -$218.28B, meaning any uptick in implied sells dealer delta into the tape and accelerates downside. Charm compounds the problem - net CHEX at -$741.2M bleeds the same direction as the clock runs down, making the last two hours asymmetric to the short side.

The only place this flips constructive is above the charm pivot at 710 (Put Wall), where current bias reads Neutral. Reclaim and hold, and the vanna drag inverts; fail it, and dealer hedging becomes the procyclical engine rather than a brake.

QQQ is the release valve: net VEX at -$144.46B is materially less hostile, and with spot parked above its flip the tech book absorbs vol pops rather than amplifying them. Trade structure follows: harvest premium in QQQ, respect the SPY pivot, keep a wing on for the headline tail.

What it means for your trading

Hostile vanna and negative charm stack the close against longs unless SPY reclaims 710; QQQ's softer -$144.46B is where the premium-seller edge lives.

Cross-Asset Confirmation

Cross-asset tape is not confirming equity stress. MOVE prints 67.70 and hasn't budged - rates vol is dead flat, which rules out a credit-driven tape. Fear & Greed sits at 67 (Greed), so sentiment is still warm despite the Iran headline overhang. What you're looking at is an equity-level structural pin with a geopolitical hood, not a systemic shock.

The divergence is the tell: QQQ at 658.63 sits above its flip in Positive Gamma territory, while SPY and IWM at 275.68 remain below theirs in Negative Gamma. Call it Qqq Heavier - tech carries the cushion, broad-market and small-cap carry the fragility.

Bottom line: with no credit compounding, headline shocks should mean-revert rather than cascade. Stay a premium seller, but size through the SPY flip line - credit isn't giving you cover if breadth cracks.

What it means for your trading

MOVE at 67.70 and Fear & Greed in Greed confirm this is an equity-structural pin, not a credit shock - Qqq Heavier divergence favors harvesting vol in the QQQ cushion while respecting the SPY/IWM negative-gamma tail.

Scenario EV

The scorecard prints Iron Condor as the winning structure with best score 37, and the logic is clean: Steep contango - vol sellers favored term structure, Normal VVIX at 98.57, and ordered skew converge on a premium-seller's tape. VRP carries the harvest - 2.14% on QQQ and 3.32% on IWM dwarf what SPY offers, so the richest condor fit lives in tech with the positive-gamma cushion doing the babysitting.

Sweet spot is the 30-45 DTE pocket where the curve pays richest and gamma risk stays manageable. Put spreads score 26 - a clean secondary fit for desks wanting IWM-leaning downside, preferable to naked wings given the steep put skew. With vol-of-vol benign, sizing guidance is Standard Size - no need to halve.

Avoid: front-week SPY short strangles into the pin-zone gamma at 710.17, and naked IWM short premium given the negative-gamma tail below 275.00. Harvest the belly, skip the wings.

What it means for your trading

Iron condor in the 30-45 DTE belly is the edge - lean QQQ for the cushion, use put spreads over strangles on IWM, and stay out of front-week SPY where flip-line gamma punishes premium sellers.

Actionable Summary

Primary trade: harvest the richer ETF VRP with a Iron Condor in QQQ across the 30-45 DTE pocket - QQQ sits Positive Gamma above its flip at 644.80, giving you a dealer cushion while the VRP (2.14%) still pays. SPY's own VRP (0.11%) is too skinny to be the carry leg; use SPY as the hedge, not the engine.

Watch level: the SPY flip near 710 is the coin-flip line - above, fade to the 711.00 call wall and 710.00 put wall; decisively below, abandon mean-reversion because net vanna (-$218.28B) and charm (-$741.2M) both sell dealer delta into weakness.

Avoid front-week SPY short strangles in this pin-zone gamma and naked IWM downside given the Negative Gamma tail at -$1.2B. Keep a cheap SPY put spread on for Iran headline overhang - VVIX is Normal so sizing is Standard Size. Regime:Elevated / Watchful with a 15-session half-life - plan for the sit.

What it means for your trading

Carry is there but the tape is fragile: sell QQQ premium in the 30-45 DTE belly, respect the SPY flip at 710, and keep a cheap put-spread hedge on through the Iran overhang.

US-Iran deadlock with no talks in sight keeps the geopolitical tail premium baked into index skew - this is why the left wing stays bid even as VIX fades.

Strait of Hormuz throughput collapsing to five ships in 24 hours is the single most important oil-supply signal of the week - any price spike feeds directly into inflation expectations and rate volatility.

The CNBC piece flags exactly what our data shows - VIX stuck near 20 in a geopolitical tape is unusual, and the VVIX/skew complex is the real place the hedging is happening.

EU mutual-defense blueprint signals the NATO cohesion erosion tail risk is no longer academic - a structural risk-premium re-rating story for European and defense equities.

Pentagon floating suspension of Spain from NATO over Iran rift is a credible alliance-fracture headline - monitor for cross-asset confirmation via EUR, Bunds, and European vol.

Gold weekly loss despite Iran war and inflation worries tells you the dollar is absorbing the safety bid - watch DXY as the regime-confirmation asset today.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 19.14 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 710.17 against a spot of 710.06. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.54% with a volatility risk premium of 0.11%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.94. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime