Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

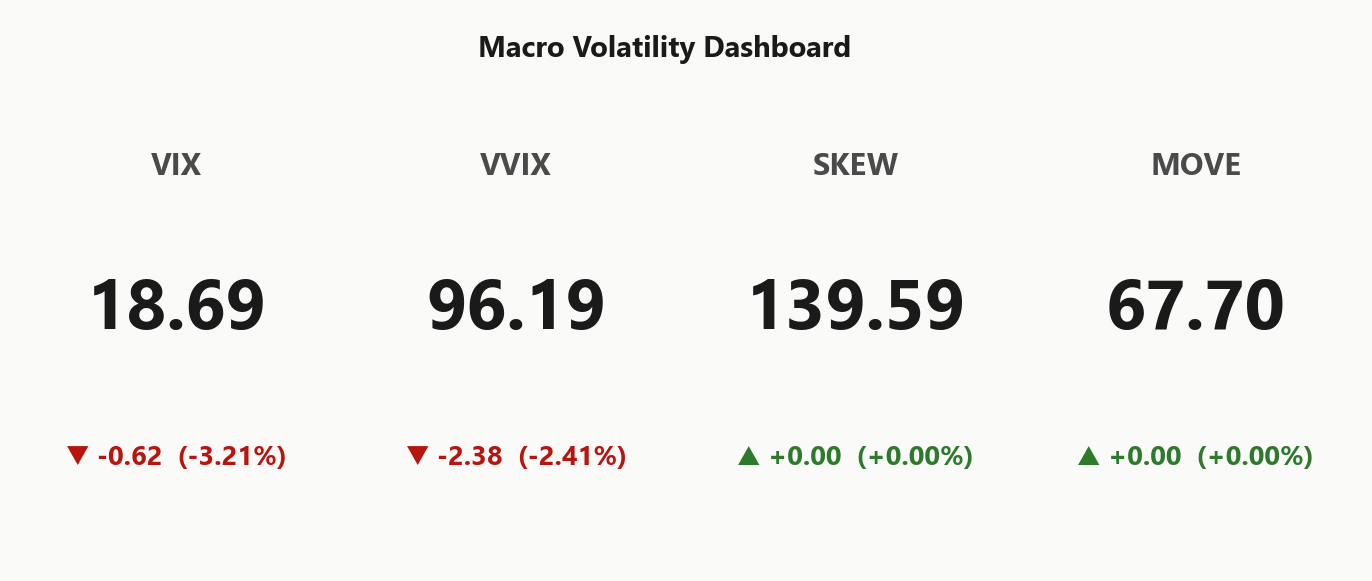

SPY at 713.32 sits in Positive Gamma with net GEX of $2.79B - dealers long gamma, moves dampened. Call wall at 711.00, put wall at 710.00, gamma flip at 710.18 - spot is parked right on the pivot, neutral bias. Dealer net DEX at $111.78B with vanna -$242.72B flags downside acceleration risk if VIX spikes. VIX at 18.69 with term structure in Contango (8.29%% near slope) - vol sellers carry intact, VRP at -0.26%. VVIX at 96.19 sits in normal range - standard sizing appropriate. Fear & Greed at 67 (Greed) confirms risk-on tone despite Iran headlines. Bottom line: iron condor structures in 30-45 DTE preferred - fade strength into 711.00, defend below 710.18.

Positive gamma cushion intact with VIX at 18.69 in contango - mean-reversion regime

Index complex sits in deep positive gamma with SPY hovering just above the 711.00 call wall and 710.18 flip - dealer hedging dampens directional moves. VIX term structure in steep contango with VVIX at 96.19 confirms vol sellers retain edge despite Iran headlines. Iron condor remains the optimal structure until spot breaches the flip or VVIX accelerates.

Regime Assessment

Regime reads Elevated / Watchful with VIX anchoring at 18.69 - the transition matrix says this state is sticky, half-life of 15 sessions. Translation: don't fade the regime, fade the extremes within it.

Near-term panic transition probability over five sessions sits at 0.05 - structurally low. The asymmetric read is the ten-session drift to low at 0.45, materially higher. Base case is vol grind lower, not panic up. Positive gamma cushion across SPY, QQQ, IWM with VIX term structure in Contango reinforces the drift lower, not the spike.

Actionable: position for mean reversion with standard sizing, keep powder for a VVIX breakout that would invalidate the Elevated read. Until then, sell strength into walls, buy weakness into flips - regime geometry does the work.

What it means for your trading

Regime is Elevated / Watchful and sticky - half-life 15 sessions, panic transition probability 0.05 over five sessions. Fade extremes, don't chase them; base case is vol drift lower.

Trading readVIX cooling, VVIX benign, MOVE subdued - three independent vol gauges all confirming risk-on. SKEW at 139.59 is the only mild dissent - tail still bid but not screaming.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

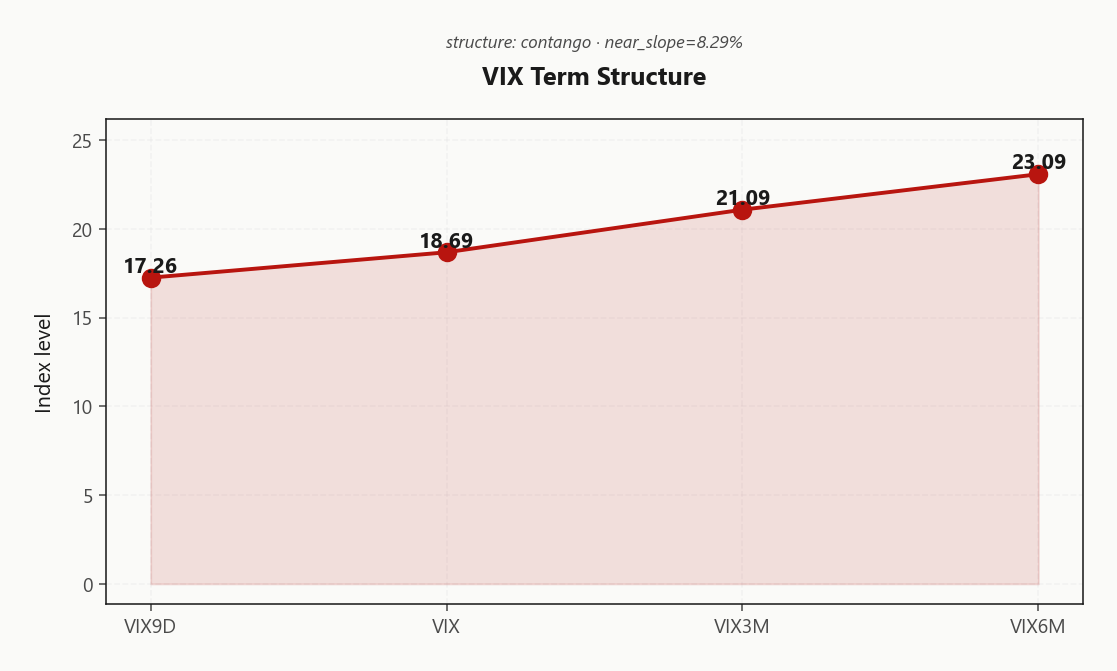

VIX term structure prints textbook Contango: VIX9D at 17.26 sits cleanly beneath spot VIX at 18.69, which in turn sits below VIX3M at 21.09 and VIX6M at 23.09. Near slope of 8.29%% is the structural carry tell - front-of-curve relaxed while long-dated stays bid. Backwardation watch is off.

Forward 30-60 vol computes to 22.1928839947 versus forward 60-90 at 24.9300641796, keeping the belly the steepest point on the curve. Regime reads Steep contango - vol sellers favored - sweet spot is short front, long back. Calendars print if spot stays pinned; naked front-month premium sales harvest the richest slope per unit of gamma risk.

Playbook: lean into Iron Condor in 30-45 DTE where forward decay is maximized, and layer in long-back/short-front calendars against the VIX3M-to-VIX6M ramp. Only a collapse of the VIX9D-to-VIX3M spread invalidates the carry thesis.

What it means for your trading

Steep Contango with near slope of 8.29%% and forward 30-60 at 22.1928839947 keeps vol sellers structurally favored in the front belly. Calendar spreads long-back/short-front and 30-45 DTE iron condors capture the richest decay geometry.

SPY ATM IV at 16.16% prints below HV20 of 16.42, dragging index VRP to -0.26% - options are cheap to recent realized. With HV60 at 15.45 sitting above HV20, realized has been decelerating; the tape is quieting faster than implied can reprice, and short index vol has lost its structural edge here.

The complex tells a different story name by name. QQQ VRP at 1.69% stays meaningfully positive, and IWM VRP at 2.34% anchors the richest corner of the board - small-cap premium is the cleanest harvest. Dispersion read is unambiguous: single-name and satellite-index vol pays, index vol does not.

Trade construction: long SPY vol versus short IWM vol captures the VRP gap directly; iron condors belong in IWM, not SPY. Fade any reflex to sell index straddles - wait for VRP to re-inflate or for realized to roll over further before re-engaging the SPY premium line.

What it means for your trading

Index VRP at -0.26% has gone cheap while 2.34% and 1.69% stay rich - harvest satellite vol, don't press SPY shorts. The long-SPY-vol / short-IWM-vol pair is the structurally cleanest expression today.

Skew Convexity

The put wing is still paying up across the complex even as VIX cools. SPY quarter-delta skew prints 3.35% with a smile ratio of 1.31% - downside conviction remains priced in, with put 14.05% IV sitting materially above call 10.7% IV around an ATM of 11.91%. Call skew flat-to-inverted says no one is chasing upside - the bid is defensive, not directional.

QQQ skew runs steeper at 3.89% - tech downside pays the richest premium in the complex, consistent with mega-cap concentration risk. IWM at 2.64% is the flatter leg; small-caps are structurally less hedged, which is its own fragility tell if the tape breaks.

Trade the asymmetry. Spread put protection rather than buying naked wings - convexity is modestly bid and you're paying for it. Sell upside calls into the 711.00 wall where skew is flat; fund downside via put spreads rather than outright longs. QQQ is the cleaner short-call target; IWM the cleaner long-gamma-on-the-downside candidate.

What it means for your trading

Put wing elevation with flat call skew means the market is hedged, not fearful - use put spreads into call-wall fades and avoid paying rich naked convexity at 1.31% smile ratio.

Vol-of-Vol Structure

VVIX at 96.19 sits squarely in the Normal band against VIX at 18.69, leaving the VVIX/VIX ratio at 5.15 - no jump premium embedded, no bimodal pricing in the tails. This is a single-mode mean-reverting regime, and the vol-of-vol tape is telling you the short-premium carry is structurally clean.

Sizing guidance prints Standard Size - no reason to dial back risk when the second derivative of vol isn't flinching. VVIX change on the session at -2.38 reinforces the read: dealers aren't paying up for convexity on VIX itself, which means the market isn't hedging a vol spike into existence.

The line in the sand is a VVIX print through the 110-handle - that's where the regime breaks and half-size becomes mandatory. Until then, treat vol-of-vol as a green light for iron condor and short-strangle structures, and let the carry compound. Fade any intraday VVIX pop that doesn't extend; chase none of them.

What it means for your trading

Vol-of-vol sits in Normal territory with VVIX/VIX ratio at 5.15, validating Standard Size on premium-selling structures. Regime breaks only on a VVIX print above the 110-handle - until then, short-vol carry remains clean.

Dispersion Spread

Index vol sits moderate with SPY ATM IV at 16.16% against QQQ at 21.85% - the tech premium is intact and the chip-driven tape is doing the heavy lifting. Top mover NVDA leads the positive GEX accumulation, with AMZN, AAPL, META and MSFT stacking the same direction. When the move is this concentrated in mega-caps, index hedges bleed carry while single-name vol overprices the actual path.

The dispersion read favors single-name vol harvest over index vol selling on a unit-of-edge basis. Short strangles in the mover complex capture the idiosyncratic premium; index iron condors remain attractive but only when paired with name-level shorts to neutralize the correlation drag. Cross-asset tone reads Unknown - aligned regime, no divergence signal to lean against.

Trade the dispersion, not the index in isolation. Fade mega-cap strangles into the chip momentum, layer the index condor on top as ballast.

What it means for your trading

SPY ATM IV at 16.16% vs QQQ at 21.85% keeps the tech premium intact while NVDA anchors the GEX build - single-name vol selling carries the edge, index condors play support.

Liquidity & Microstructure

The book is stacked in a tight band: 711.00 call wall sits directly overhead, 710.00 put wall one tick below, and the gamma flip at 710.18 threaded between them. The dominant GEX strike at 711.00 carries $4.09B of net exposure - that single pin is doing the work, and it sits right on top of spot.

Highest OI at 600 is the long-dated structural anchor, but the tactical line is 710.18. Above it, dealers buy dips and sell rallies - the classic positive_gamma pinning regime that has kept realized suppressed. A clean break below flips the hedging sign and the same flow accelerates downside rather than absorbing it.

Trade the band, not the tape: fade strength into 711.00, lean on 710.00 for support, and treat 710.18 as the kill-switch for any short-premium structure.

What it means for your trading

Walls compressed around spot with the dominant GEX at 711.00 keep the complex pinned while price holds above 710.18; a breach inverts dealer flow from supportive to amplifying.

Trading readMassive positive gamma stacked between 710.00 and 711.00 means dealers absorb both directions inside the band - fade strength into the call wall, expect support into the put wall, only get directional on a clean break of 710.18.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

The line in the sand is 711, a Call Wall pivot currently sitting at -0.3245410513 from spot with bias Neutral. Above it, charm bleeds dealer support into the close but the gamma wall still pins. Below it, vanna takes the wheel - hedging flips from dampener to accelerant and selling cascades through the 710.18 flip.

Trade the cushion, respect the trapdoor. Stay short premium while spot holds above 711; cut size immediately on a breach and do not sell naked downside into a VVIX acceleration - the vanna bid evaporates precisely when you need it.

What it means for your trading

Positive gamma is cushioning the tape, but negative VEX and CHEX mean the cushion is conditional on vol staying contained - a break below 711 or a VVIX surge converts dealers from shock absorber to accelerant.

Cross-Asset Confirmation

Cross-asset tape refuses to confirm the Iran headline panic. MOVE at 67.70 sits becalmed - bond vol is not propagating the geopolitical premium, and without a credit channel the equity tape has no mechanical reason to reprice. Fear & Greed prints 67 (Greed), a risk-on reading that squares with the Aligned regime stance across the index complex.

QQQ holds 663.00 and IWM 277.38, both parked above their respective flips - the broad complex is aligned in positive gamma and small-caps, normally the first to crack, are not dissenting. Cross-asset tone reads Unknown, but the absence of a MOVE-led rates signal is itself the signal.

Playbook: treat Iran tape as mean-reverting noise until bond vol, VVIX, or the IWM flip actually break. Fade vol spikes, do not chase them - the cross-asset confirmation required for a sustained risk-off leg is simply not there.

What it means for your trading

Credit and rates vol are not validating the equity-vol anxiety; with MOVE at 67.70 and Fear & Greed at Greed, sell the vol pop rather than buying protection into it.

Scenario EV

The book scores Iron Condor at 51 as the top structure, with the put spread alternative trailing at 40. VRP reads Unknown, but the combination of Positive Gamma dealer positioning and a Normal vol-of-vol print gives premium sellers the structural edge regardless.

Park the trade in 30-45 DTE - that window captures the steepest forward vol decay without fighting the flat front belly. Sizing guidance is Standard Size; no haircut required while VVIX sits at 96.19 and the VVIX/VIX ratio holds at 5.15.

Skip calendars here - VIX9D at 17.26 versus VIX3M at 21.09 leaves the near curve too flat to print. Condor the wings, respect 711 as the cut-size trigger, and let theta work.

What it means for your trading

Recommended trade is Iron Condor in 30-45 DTE at Standard Size, with the put spread (40) as the defensive alternative if spot loses 711.

Actionable Summary

Bottom line: the trade is an Iron Condor in the 30-45 DTE belt, where forward vol decay bites hardest and the dealer gamma cushion between 710.00 and 711.00 does the structural work for you. Regime reads Elevated / Watchful with a half-life of 15 sessions - sticky, mean-reverting, fade extremes rather than chase them.

Pivot discipline is non-negotiable: 711 is the line that flips dealer behavior from dampening to amplifying. Above it, stay short premium and let vanna-charm decay carry the book; below it, cut size immediately and respect that net VEX at -$242.72B turns hostile the moment VIX wakes up. Skew is rich on the put wing (3.35%) - spread your downside, never buy naked, and skip front-week calendars since the near curve is too flat to pay.

Sizing: Standard Size. VVIX at 96.19 prints benign, no jump premium bid, no reason to halve. Trigger to downshift is a VVIX breakout or a clean break of the flip at 710.18.

S&P and Nasdaq grinding higher on US-Iran talk hopes confirms the geopolitical-noise read - risk assets fading the war premium even as headlines persist.

Polish PM questioning US loyalty under a Russian attack scenario is the kind of NATO-cohesion crack that compounds tail risk - equities ignore it today, but it's the slow-burn story.

Pentagon framing Iran blockade as 'going global' raises the ceiling on energy/shipping disruption - watch crude proxies and MOVE for the first signal of credit propagation.

Strait of Hormuz traffic collapsing to five ships in 24 hours is the hard-data version of the war headlines - if sustained, this is the channel through which equities finally repricing.

Pentagon floating NATO suspension over Iran rift is a tail risk to alliance cohesion - equity-relevant only if it accelerates into Europe-led risk-off, which today's MOVE doesn't confirm.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.77 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 710.18 against a spot of 713.32. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.16% with a volatility risk premium of -0.26%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.69. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime