Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY closed at 713.72 with dealers long gamma ($4.19B net GEX) - mean reversion regime firmly intact. Call wall at 711.00 is the ceiling, put wall at 710.00 the floor, with gamma flip directly below spot at 710.28 - we are only -0.3804039428% from the pivot, so the cushion is thin despite the positive regime label. Dealer vanna is -$731.3M (vol-up = dealers sell delta, so any VIX spike amplifies downside) and charm is pressing negative into close. VIX at 18.69 with term structure in Contango at 12.36%% slope - front-end still cheap, back-end expensive, classic carry setup. VRP at -1.59% versus 20d HV of 16.44 says realized is eating premium - options are cheap to the recent tape, so short-vol sizing needs to be disciplined. VVIX at 96.86 is benign, Fear & Greed at 66 in Greed. Bottom line: Iron Condor at 30-45 DTE is the vehicle - lean short premium around the walls, but keep a convex tail hedge on given Iran/Hormuz headline risk.

Index complex closes with dealers long gamma across SPY/QQQ/IWM while VIX term structure remains in Contango - the suppressive regime is intact. Spot sits above the gamma flip at 710.28 with the call wall capping at 711.00, and VRP turned negative (-1.59%) as realized has overshot implied. With VVIX benign and forward vol Steep Contango, the carry trade remains the path of least resistance - but Iran headlines keep tail hedges non-optional.

Regime Assessment

Regime tag reads Elevated / Watchful with VIX at 18.64 and a 15-session half-life - elevated but not stressed, and sticky enough that fading the label is the wrong trade. The transition math favors compression: probability of a panic break within five sessions sits at 0.05, while the drift-to-low-vol path over ten sessions runs at 0.45. Bleed lower is the base case, not a jump higher.

Current regime prints Elevated with signal color Yellow - watchful, not defensive. Trade the regime we have: short premium around the walls with defined risk, size standard on VVIX, and let carry do the work. But the Iran/Hormuz tape is the one headline that can invalidate the half-life assumption overnight, so a cheap convex tail is non-optional even as the base-rate math points to compression.

What it means for your trading

Regime is sticky at Elevated / Watchful with drift-to-compression the dominant path and panic transition a tail scenario - lean short vol around the walls, but hold a cheap convex hedge given geopolitical headline risk.

Trading readVIX easing, VVIX easing, SKEW flat, MOVE subdued - the macro dashboard is aligned in 'quiet' mode. The divergence to watch is SKEW staying elevated while VIX falls, which would say tail hedgers are still positioned even as front vol compresses - that's a subtle warning, not a green light.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

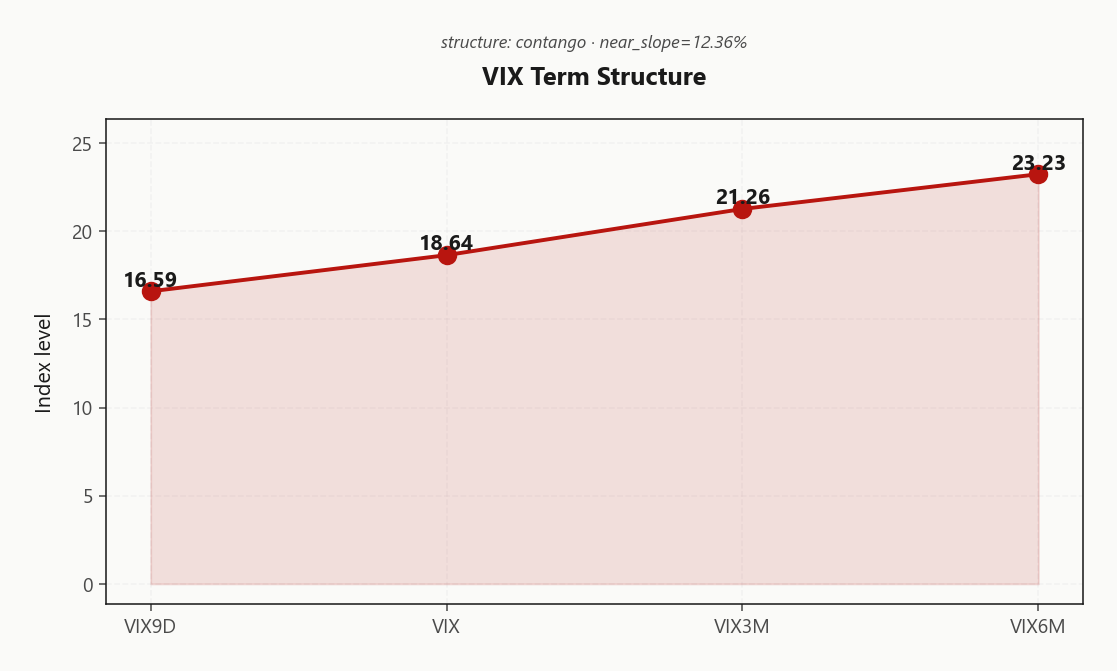

Term structure prints Contango from 16.59 through 23.23, with spot VIX at 18.64 and the 3M node at 21.26. VIX9D printing below spot VIX tells you near-term realized expectations are muted - the curve is paying vol sellers to hold the short end while the back end carries the mean-reversion premium. Front-to-3M slope at 12.36%% is the carry signature, and the regime tag Steep Contango - Steep contango - vol sellers favored - supports systematic short-vol in size.

Forward 30-60 and 60-90 both price a mean-reverting path higher; don't fight the roll. Best edge sits in the 30-45 DTE belly where the forward is richest versus realized expectations - front weeklies are too cheap to short naked, long-dated too expensive to own outright. Calendar spreads are the cleanest expression: sell front, own back, let time and roll-down do the work.

What it means for your trading

Steep Contango across the curve with a 12.36%% near-slope pays vol sellers to carry - concentrate short exposure in the 30-45 DTE belly and lean on calendars over naked short premium.

Trading readSteep contango with 14% basis between spot VIX and front-month future - classic carry setup for vol sellers. The market expects mean reversion higher, which is actually bullish for equity; backwardation would be the alarm bell.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 14.85% is printing below 20-day realized at 16.44 - VRP has compressed to -1.59%, which is a counterintuitive read in a positive-gamma tape. Options are cheap to the actual range the market is delivering, and the systematic short-premium edge that usually rides alongside a dealer-long-gamma regime is simply not there on a naked basis.

The term structure of realized adds nuance: 60-day HV at 15.46 sits below the 20-day, so recent tape has accelerated relative to the trailing baseline. That asymmetry argues either realized mean-reverts lower from here - or implied is genuinely underpricing the range. Assessment flag reads Unknown, so the premium harvest is not a screen-pass.

QQQ and IWM echo the same compression - at -0.33% and 0.31% respectively - so this is a complex-wide signature, not an SPY anomaly. The rule writes itself: defined-risk structures over naked wings, lean on skew geometry rather than vega level, and size short-vol books against the walls, not against the VIX print.

What it means for your trading

With ATM IV at 14.85% below 20-day HV at 16.44 and VRP at -1.59%, naked strangles lose their automatic edge - defined-risk structures are the only disciplined way to harvest premium here.

Skew Convexity

Quarter-delta skew remains stubbornly steep at 2.71% with smile ratio at 1.28% - puts are still bid meaningfully over calls even as VIX eases and dealers sit long gamma. The protective bid has not left the building; the crowd is hedging, not chasing.

Put wing prints 12.24% against ATM at 10.83% - a steep left wing that eats single-strike premium. The right wing is the tell: call quarter-delta at 9.53% sits below ATM, a flat-to-inverted profile that says no one is paying for upside convexity into the call wall.

Two trades fall out. Risk reversals are structurally cheap directionally - owning upside convexity is a value trade here, not a reach. And on the downside, put spreads dominate naked puts: the steep left wing punishes single-strike premium buyers, so finance the long leg by selling the fat one. Classic buy-the-dip, fade-the-rip positioning baked straight into the surface.

What it means for your trading

Skew at 2.71% with smile ratio 1.28% signals persistent downside hedging despite the positive-gamma tape - lean put spreads over naked puts, and treat upside risk reversals as a cheap directional value trade.

Vol-of-Vol Structure

VVIX at 96.86 sits squarely in the Normal band and eased on the session - no jump premium embedded, no binary-outcome kink priced into the vol-of-vol surface. The VVIX/VIX ratio of 5.20 is structurally unremarkable, well shy of the stressed prints that force a sizing haircut on short-gamma books.

Translation for the trade desk: Standard Size. Iron condors and strangles clear at full notional - the vol-of-vol tape is not demanding the defensive half-size treatment that a 18.64 VIX might otherwise imply. Jump-risk tail hedges are cheap in absolute terms but not urgent; treat them as opportunistic adds rather than mandatory overlay, and layer them on weakness in VVIX rather than chasing strength.

The signal to watch is divergence: if VVIX re-rates higher while VIX drifts sideways or lower, that is the early warning that the market is quietly re-pricing jump risk ahead of spot vol. Until that divergence prints, the vol-of-vol read stays Normal and carry trades remain the path of least resistance.

What it means for your trading

VVIX at 96.86 and a ratio of 5.20 mean no jump premium is embedded - short-vol structures clear at Standard Size. Watch for VVIX divergence above VIX as the leading tell that the regime is about to flip.

Dispersion Spread

Index vol has compressed hard while single-name implied stays sticky - 14.85% ATM sits well below 19.94% in QQQ and 20.84% in IWM. That is correlation bleeding, not a benign vol compression. When the index-to-single-name spread runs this wide, systematic index short-vol quietly underperforms single-name carry, and index hedges protect less per dollar than they did two weeks ago.

The GEX move list confirms the dispersion: NVDA, MSFT, and META headline the mega-cap GEX builds, with AMZN and GOOGL rounding it out - flow is concentrated, not broad. Lean the trade accordingly: sell index premium around the walls, own single-name convexity in the mega-cap set where implied is already paying you to be long gamma. Risk reversals and calls in the movers are where the asymmetry lives; naked index strangles are the losing side of this dispersion.

What it means for your trading

Correlation is decoupling - index vol at 14.85% is cheap to 19.94%/20.84%, favoring short index premium against long single-name convexity in the NVDA/MSFT/META complex.

Liquidity & Microstructure

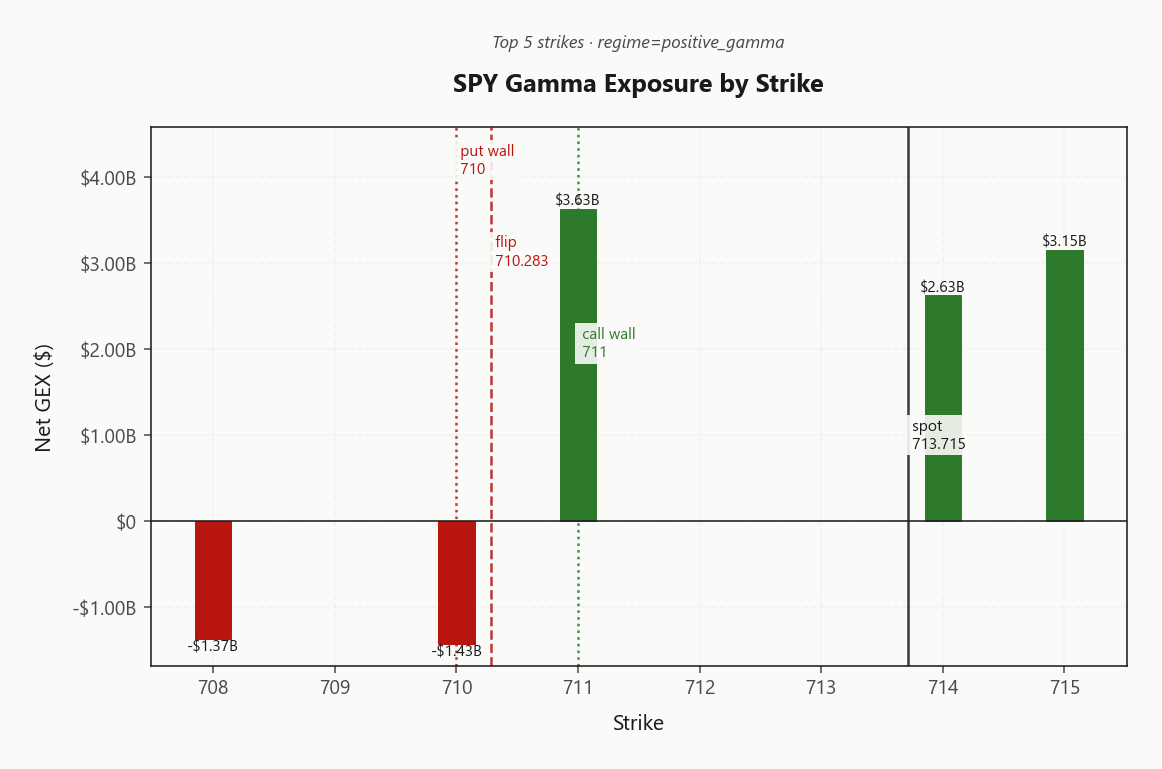

Open interest clusters are extreme around the 711.00 call wall and the gamma flip at 710.28 - that zone is the pinning magnet into weekly expiry. The top strike at 711.00 carries $3.63B of net GEX, so intraday rallies run into dealer supply exactly where the book is heaviest. Highest OI at 700 anchors the structural floor for the weekly.

Spot sits barely above the flip - the cushion is thin, not durable. Above the wall dealer selling kicks in; below the flip, support inverts into amplification and the tape turns trend-following in a single break. Trade the range, but treat the flip as the line in the sand.

0DTE share of gamma at 134.6%% is enormous - session tone is set at the 0DTE magnet, not the weekly. Expect chop pinned between the walls until charm flow tips the final hour.

What it means for your trading

Extreme OI concentration around 711.00 and 710.28 makes this a pin-to-the-wall tape with 134.6%% 0DTE share dictating intraday flow. Fade strength into the wall, respect the flip - a breach flips the regime from mean-reverting to trend-following instantly.

Trading readDealer long gamma stacks just above spot at the call wall and thins immediately below the flip - that's the trading range. Fade strength into the wall, cover shorts into the flip, and recognize that a breach below the flip turns the tape from mean-reverting to trend-following in one move.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

The headline label reads positive gamma, but the second-order book tells a different story. Net vanna prints at -$731.3M - a classic accelerant configuration where a vol re-rating forces dealers to sell delta into weakness, converting today's dampening flow into tomorrow's amplifier. The cushion is conditional, not structural.

Charm is pressing at -$2.18B and grinding negative into the close, loading late-session hedging flow with a sell bias that punishes dated longs as theta bleeds delta. The single line that matters is the charm pivot at 711 - current bias reads Neutral with spot sitting only -0.3804039428 from the flip. That's a thin margin for a regime whose label depends on vol cooperating.

Trade the positive-gamma tape that's in front of you, but respect the vanna trapdoor: a VIX re-rate flips the regime faster than the top-line tag implies. Keep a convex hedge on.

What it means for your trading

Positive-gamma label masks a negative vanna/charm configuration - gamma cushion holds only while vol stays quiet, and the charm pivot at 711 is the intraday line where dealer flow direction flips.

Cross-Asset Confirmation

Cross-asset tape reads Aligned across the complex - MOVE at 67.70 sits well below stress thresholds, credit is quiet, and rates vol is not pricing a shock. This is an equity-internal regime, not a macro dislocation, and the options tape is behaving accordingly.

QQQ at 663.47 and IWM at 276.51 are both perched above their gamma flips, mirroring SPY's positive-gamma posture. With the index complex in lockstep and VIX term structure in Contango, the dampening dynamic is broad-based rather than a single-name artifact - dealers are long gamma in size wherever you look.

Fear & Greed at 66 in Greed is the contrarian tell - sentiment is supportive but not yet extreme. Iran headlines remain the overnight tape-driver, but equity vol has categorically refused to price it as systemic. Geopolitical shocks mean-revert; credit shocks compound. This is the former - trade the regime, keep the tail hedge cheap.

What it means for your trading

Full index complex aligned in positive gamma with 67.70 MOVE confirming no rates stress - the regime is clean for carry, but Greed sentiment flags contrarian risk if Iran escalates.

Scenario EV

Scenario EV work flags Iron Condor as the top-scoring structure at 45, clearing the put-spread alternative at 33 - defined-risk wins in this tape. The setup is a four-factor fit: positive-gamma dampening keeps realized inside the range, Steep contango - vol sellers favored term structure delivers roll-down tailwind, VVIX sits Normal so sizing stays standard, and steep skew means short-strike selection carries the trade rather than naked premium harvest.

Center the body around 711.00 up top and 710.00 underneath, with the wings sized off the 2.71% skew read. Optimal window is 30-45 DTE - front weeklies are too cheap to short and long-dated gives the roll back. Skip calendars; the Contango curve already prices the mean-reverting path higher, so the edge is in the iron condor's theta profile, not a volatility-surface bet.

Avoid naked strangles - VRP at -1.59% punishes undefined risk, and the charm pivot at 711 is the line that flips the regime.

What it means for your trading

Trade a Iron Condor at 30-45 DTE bracketing 711.00 and 710.00, standard size given VVIX Normal. Defined-risk only - negative VRP and a thin gamma cushion make naked strangles the wrong vehicle here.

Actionable Summary

Bottom line: the cleanest expression is an Iron Condor at 30-45 DTE, strikes bracketing the 711.00 call wall and 710.00 put wall. Regime tag is Elevated / Watchful - positive gamma is intact, term structure is in Contango, and VVIX at 96.86 supports Standard Size notional. Carry is clean, but the cushion is thin.

Avoid naked strangles and undefined-risk premium with VRP at -1.59% - realized is eating the implied, so defined-risk wins. Watch the charm pivot at 711; a breach flips dealer flow bias given net VEX of -$731.3M sitting as a hidden accelerant. Hedge the Iran/Hormuz tail with a cheap OTM put spread or VIX call spread - equity vol is not pricing the headline risk, which is the one variable that invalidates the setup overnight.

What it means for your trading

Sell the walls in defined-risk size at 30-45 DTE, respect the 711 pivot as the regime line, and carry a convex tail hedge against the Iran tape.

Oil up sharply on supply worries keeps the Iran/Hormuz tape front-and-center - equity vol is not pricing it, so a headline escalation is the asymmetric risk into the weekend.

Trump signaling Iran will make an offer is the kind of headline that can crush VIX further if confirmed - watch the front end of the curve for a whoosh lower on a confirmed deal.

Witkoff and Kushner traveling to Pakistan for Iran talks is the binary catalyst - a breakthrough compresses the entire vol complex, a breakdown spikes MOVE and re-prices equity tails.

The Fed independence analysis matters because rate-path uncertainty is the second-order risk sitting behind the Iran story - any resurfacing of political pressure on Powell re-prices the long end and flows through to duration-sensitive equity pockets.

Pentagon framing the Iran blockade as 'going global' raises the tail - this is the kind of headline that can turn a mean-reverting geopolitical shock into a compounding one, and credit would be the first place to check.

Pentagon email on suspending Spain from NATO is a low-probability but high-impact structural-risk headline - if it escalates, it re-prices the Europe risk premium and bleeds into US financials and defense names.

Only five ships through Hormuz in 24 hours is the quiet tail-risk datapoint - if it persists, oil squeezes higher regardless of talks, and energy-driven inflation re-enters the Fed calculus.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.69 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 710.28 against a spot of 713.72. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.85% with a volatility risk premium of -1.59%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.64. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime