Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

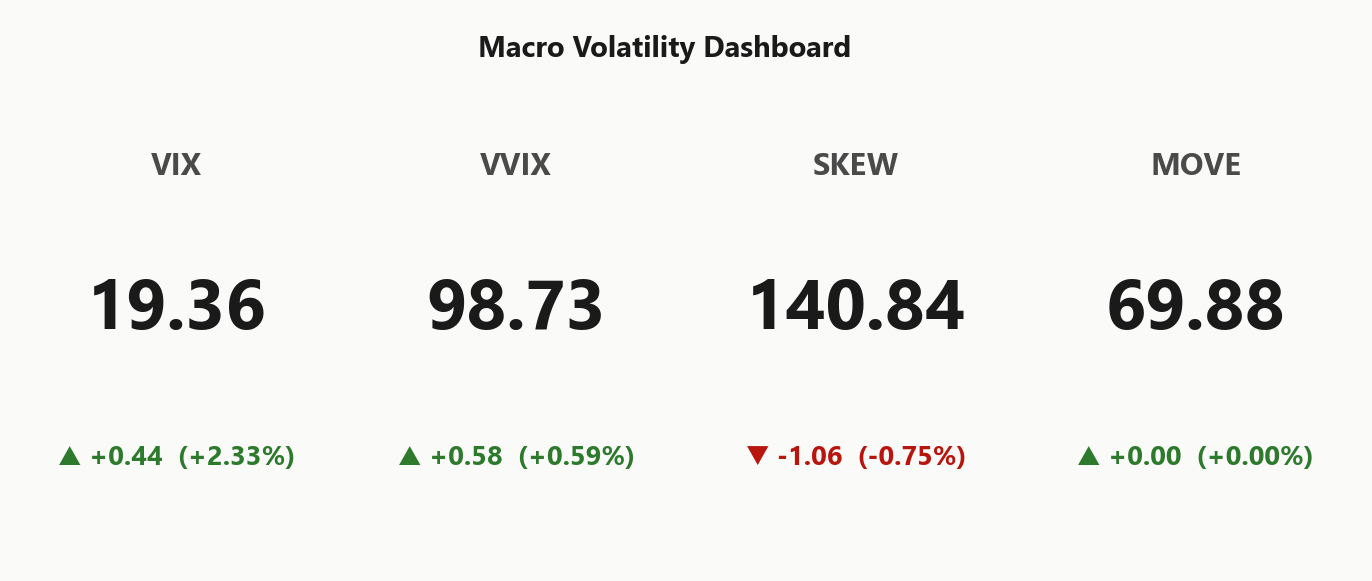

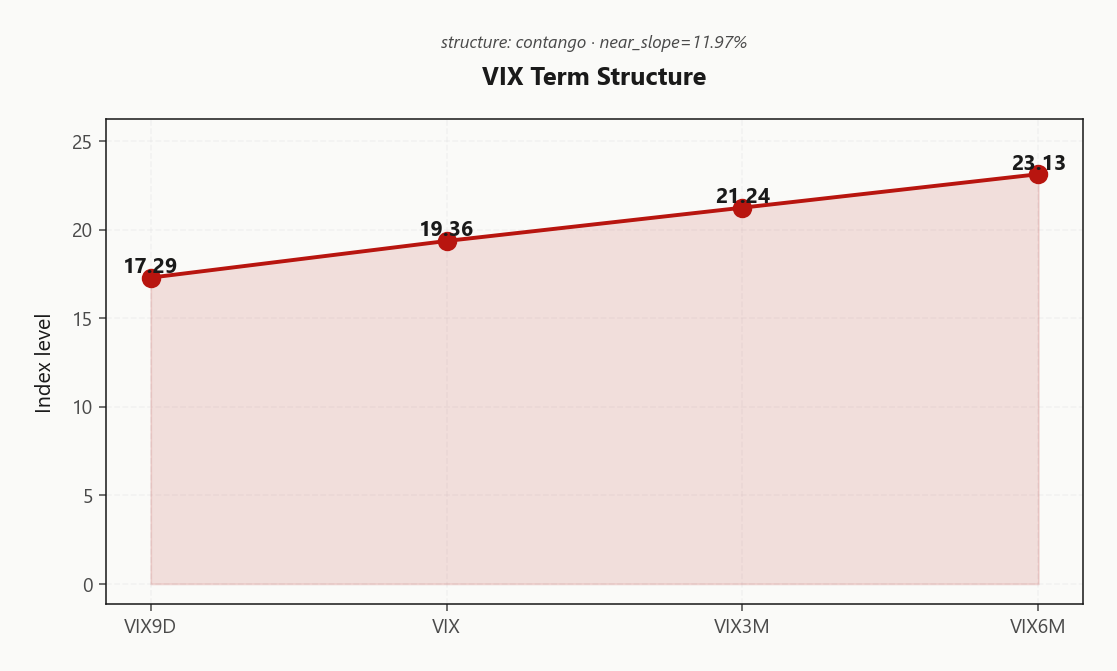

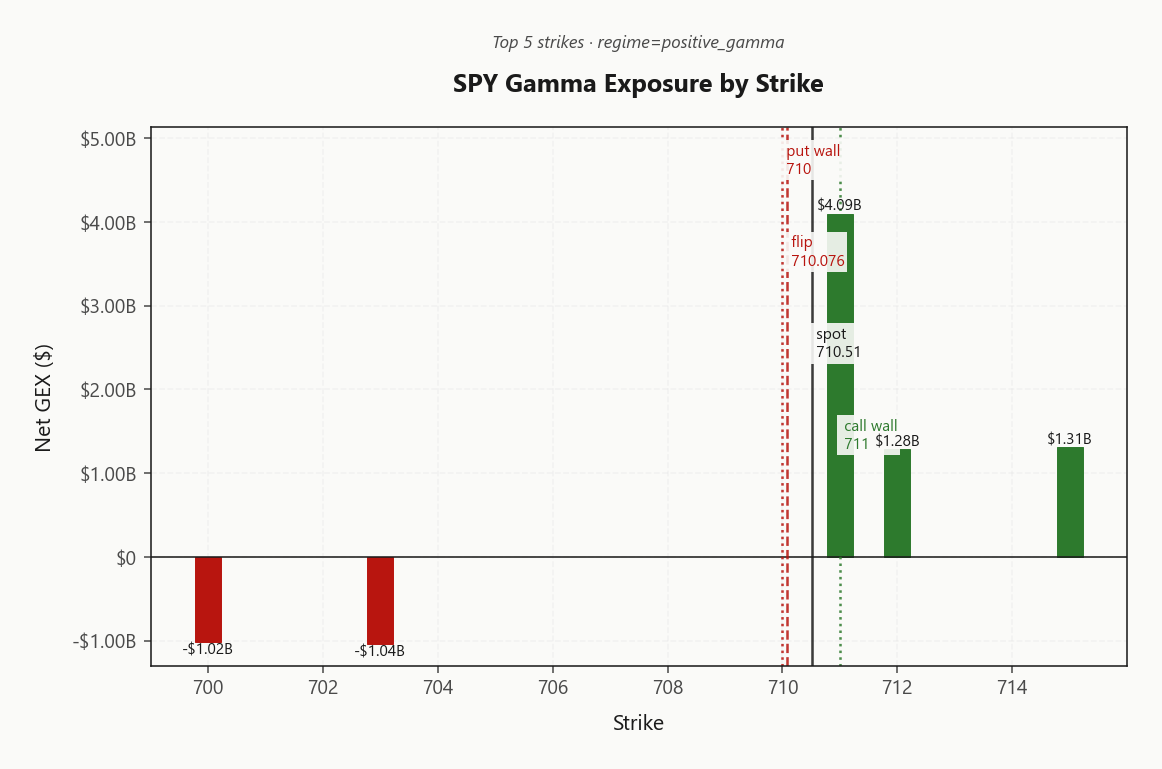

SPY at 710.51 sits in Positive Gamma with net GEX of $297M - dealers long gamma, range-compression mode. Call wall at 711.00, put wall at 710.00, gamma flip at 710.08 - spot sits essentially pinned AT the flip, meaning a single-dollar break either way changes the dealer reaction function. Dealer vanna is negative at -$235.01B - any VIX spike pulls dealer delta sharply lower, so the cushion is conditional on vol staying quiet. VIX at 19.36 with term structure in Contango (11.97%% near slope) says carry is harvestable; 20d RV of 18.18 above ATM IV of 16.52% puts VRP at -1.66% - options are quietly cheap to realized. Bottom line: sell 30-45 iron condors around the 711.00/710.00 rails, avoid naked upside, and cut risk if VIX cracks 21.24.

Positive gamma cushion holds as SPY pins 711.00 with VIX drifting in contango

SPY trades just above its gamma flip at 710.08 with dealers long gamma across the index complex, dampening intraday range even as Iran headlines pressure risk. VIX in Contango and VVIX at 98.73 say structural carry is available but the market is quietly paying up for vol-of-vol. Best edge sits in 30-45 iron condors, NOT naked strangles, while the charm pivot at 710.0758385663 stays supportive.

Regime Assessment

Regime classifies as Elevated / Watchful with VIX anchored at 19.36 - the Elevated state with a half-life of 15 sessions. Sticky, not cemented: the tape can sit here for weeks, but the exit is binary and the transition matrix does the talking.

Five-session panic probability reads 0.05 - small enough that tail hedges stay modest, large enough that zero hedge is negligent. Ten-session resolution to low-vol sits at 0.45, the base case: Iran headlines bleed out, contango carries, dealers stay long gamma. Signal color Yellow, not red - watchful, not defensive.

Translation: position for mean-reversion with a modest left-tail kicker. Cross-asset is Aligned, dealer book stays supportive at the charm pivot 710.0758385663. Don't fight the stickiness; don't ignore the asymmetry.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - carry the base case at 0.45 ten-session low-vol probability, hedge the 0.05 five-session panic tail.

Trading readVIX up, VVIX up modestly, SKEW elevated but easing, MOVE flat - the mix says equity-only nervousness without credit contagion; divergence NOT firing yet but VVIX is the tell to watch.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX curve stacks cleanly in Contango - VIX9D at 17.29 sits below spot VIX at 19.36, then steps up to VIX3M at 21.24 and VIX6M at 23.13. The immediate window is calm; the long end is quietly bid for Iran-headline uncertainty. Near slope of 11.97% reads as structural carry, not an event-implied kink - the curve is pricing premium, not conviction.

Regime registers Contango - Contango - structural carry available. That puts the monetizable edge squarely in the 30-45 DTE window: far enough out to harvest the slope between the front and intermediate buckets, close enough in to duck the geopolitical tail priced into the long end. Selling the belly, not the wings.

Front-end calm plus a bid long end is the textbook vol-seller's curve - but the kink sits in the back, and that's where naked length gets punished on any Iran de-escalation tape.

What it means for your trading

Stacked Contango from 17.29 through 23.13 with near slope 11.97% - carry is real, harvest it in 30-45 DTE and let the long end's event premium price itself out.

Trading readStacked Contango with 11.97%% near slope says carry is there and the market is not pricing imminent stress - vol sellers get paid in the 30-45 DTE window.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

The realized-implied gap is the tell: SPY 20d HV at 18.18 sits aboveATM IV at 16.52%, pinning VRP at -1.66% and flagging an Negative Spread. Options are quietly cheap to the recent sample, not rich - the reflexive premium-sell instinct is the trap here.

The longer window confirms the normalization: 60d HV at 15.37 and 5d RV at 12.84 bracket a tape that has dampened in real time while the historical print still carries the bigger moves. Pair that negative VRP with Positive Gamma dealer positioning and the edge is structural, not outright: sell iron condors around the 711.00/710.00 rails, not naked strangles whose short leg has no VRP cushion.

Cross-asset, IWM VRP at 2.24% prints positive - the idiosyncratic edge for premium-sellers sits in small-caps, while SPY itself pays only for defined-risk structure.

What it means for your trading

Negative VRP plus positive gamma means options are cheap to realized but the tape is dampening - harvest the spread via defined-risk condors on SPY, reserve naked short-vol for IWM where 2.24% is positive.

Skew Convexity

The 2.66% vol-point gap between 17.81% quarter-delta put IV and 16.22% ATM is the tell: downside is being paid for, not panic-bid. Smile ratio at 1.18% confirms ordered positioning - hedgers lifting wings on a schedule, not reflexive tail-grabs chasing headlines. SKEW index at 140.84 sits elevated but off the cycle highs, same story from the index-level lens.

The call wing is the more interesting leg. Quarter-delta call IV at 15.15% prints below ATM - a flat-to-inverted call skew that prices zero upside conviction. Lottery longs are dead on arrival here; no one is paying up for the right tail even with VIX drifting in Contango.

Trade implication: put spreads dominate naked puts on cost-of-protection given the paid-up put wing, and call-skew inversion kills any naked upside structure. Monetize the wing asymmetry, don't pay it.

What it means for your trading

Skew shape says hedged, not scared: put wing bid at 17.81% vs call wing cheap at 15.15% favors put spreads over naked puts and kills long-call lottos outright.

Vol-of-Vol Structure

VVIX prints 98.73 against VIX at 19.36, pinning the ratio at 5.10 - squarely in the Normal zone and well clear of the jump-regime threshold. Dealers are not pricing a bimodal crush-or-spike outcome; the vol-of-vol tape is telling you the distribution is still unimodal around a quiet mean. Signal color reads Green and sizing guidance is Standard Size - no haircut on short-premium books today.

That said, VVIX is up 0.59% on the session while spot vol barely moves - the first whisper of jump-premium creeping back into the wings. It is a monitoring flag, not a sizing cut: the ratio needs to pop materially above current levels before the book turns reflexive. Until then, the cushion thesis holds and the vol-of-vol tape corroborates the Positive Gamma read across the index complex.

Play it as approved: Iron Condor in the 30-45 DTE window, defined risk, standard clip. Watch VVIX/VIX for a regime escalation - that is the tell that precedes vanna turning hostile before spot even moves.

What it means for your trading

VVIX at 98.73 and a ratio of 5.10 keep the book in Normal territory with Standard Size sanctioned, but the 0.59% uptick is the early warning that jump-premium is leaking back in.

Dispersion Spread

Index vol sits rich to the single-name basket: SPY ATM IV at 16.52% against QQQ at 21.96% leaves the tech premium intact, while IWM ATM IV at 24.17% tops the complex. Cross-strike dispersion at 81.22 and cross-expiry at 2.04 read moderate - single-names are clustered tighter than the index implies, and the positive-gamma dealer book is quietly suppressing correlation transmission.

That flips the usual dispersion playbook. With the index complex Aligned in positive gamma, idiosyncratic noise isn't bleeding into SPY through correlation, so the cleanest edge is selling index vol (SPY/SPX) rather than paying up for a dispersion basket. QQQ VRP at -0.41% keeps mega-cap premium contained; IWM's positive VRP at 2.24% is the outlier where idiosyncratic short-vol still clears.

Bottom line: this is not a dispersion-trade-of-the-year regime. Harvest index rails over single-name strangles, keep small-caps as the cleaner short-vol sleeve, and resist rotating into basket dispersion until correlation actually breaks.

What it means for your trading

Index ATM IV sits elevated versus single-name cluster while correlation stays dampened by positive-gamma flow - sell SPY/SPX vol over dispersion baskets, with IWM at 24.17% the cleanest idiosyncratic short-vol sleeve.

Liquidity & Microstructure

The book is anchored by a towering positive-gamma ceiling at 711.00 carrying $4.09B of net GEX, with the deepest OI well rooted at the LEAPs-anchored 600 strike - two magnet zones bracketing the tape. The call wall at 711.00 sits a hair above spot and doubles as the gamma flip at 710.08, collapsing the cushion and the ceiling into the same knife-edge.

Spot pressed against that line means the dealer reaction function is binary: hold below and mean-reversion into the rails keeps winning as dealers bid dips; punch through and the same book flips from stabilizer to accelerant. The put wall at 710.00 marks the symmetric trapdoor where amplification turns on to the downside.

Zero-DTE carries -46.5% of total gamma - an outsized intraday pin engine that compresses mid-session range and loads the classic end-of-day unpin risk. Trade the rails, not the direction, and respect that every dollar of drift rewrites the script.

What it means for your trading

Spot is pinned on the gamma flip and call wall simultaneously at 711.00, making 710.08 the single pivot that decides whether dealer flow cushions or compounds; fade into the wall, respect 710.00 as the amplification trigger below.

Trading readDeep positive gamma stacked at 711.00 and the call wall caps upside; dealers buy on dips and sell into strength - fade rallies into the wall, let pullbacks find the flip at 710.08.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net vanna prints -$235.01B - deeply negative - meaning every uptick in 19.36 forces dealers to sell delta into weakness, the textbook accelerant. Charm at -$704.2M compounds the problem: time decay alone drags dealer hedges lower into the close. Two hostile second-order greeks sit masked beneath the positive gamma shell - the cushion looks real, but it's conditional.

The line in the sand is the charm pivot at 710.0758385663, current bias Supportive. Spot-to-pivot distance is -0.0611056049 - the tape is essentially on it. Above this level the dealer reaction function dampens; below it, vanna and charm reinforce each other into a feedback loop that gamma alone can't absorb.

Trade implication: positive gamma is conditional on VIX staying pinned. A breach of 21.24 on the term structure pulls vanna into the driver's seat and the cushion inverts. Keep structures defined-risk, watch the pivot, and respect that the calm is engineered, not earned.

What it means for your trading

Positive gamma masks deeply negative vanna at -$235.01B and negative charm at -$704.2M - the cushion holds only while VIX stays quiet and spot stays above the 710.0758385663 pivot. Breach either and the dealer book turns hostile inside a session.

Cross-Asset Confirmation

Cross-asset tape reads Aligned: SPY, QQQ at 654.57, and IWM at 277.22 all sit in Positive Gamma, with VIX holding its native negative-gamma state. No intra-index divergence to trade - the complex is aligned and the fragility sits in vol-of-vol, not spot products.

Critically, MOVE at 69.88 is quiet - credit vol is not firing, which rules out systemic contagion and confirms this as a geopolitical-shock profile rather than a credit crisis. Fear & Greed reads Greed at 68, the complacent side of the dial into Iran headlines - contrarian lean skews toward mild pullback risk before resolution.

Bottom line: geopolitical shocks mean-revert; credit crises compound. Until MOVE breaks or VVIX cracks its Normal zone, fade the tail and keep harvesting the Contango.

What it means for your trading

Aligned positive-gamma across SPY/QQQ/IWM with MOVE at 69.88 quiet and F&G at Greed (68) confirms geopolitical-shock, not credit-crisis - mean-reversion stays favored.

Scenario EV

The scoreboard reads clean: iron condor prints 26, the top risk-adjusted structure into this tape, while put spreads come in secondary at 13 - a tactical hedge, not the primary expression. Recommended structure is Iron Condor with VRP assessment Unknown, which is precisely the setup defined-risk was built for: negative VRP against a positive-gamma dealer shell rewards the rails, not the outright.

DTE sweet spot sits at 30-45 - far enough out to harvest the Contango slope running 11.97% near, close enough in to sidestep the long-end geopolitical premium bid into 23.13. Build the wings around the 711.00 / 710.00 rails with the flip at 710.08 as your tripwire. Sizing standard.

Avoid the traps: naked strangles die to the negative VRP cushion evaporating on the short leg, naked upside calls die to flat call skew at 15.15%, and outright long vol bleeds to contango carry. Structure over direction.

What it means for your trading

Iron condor at 26 is the highest-scoring expression of negative VRP plus positive-gamma cushion; deploy 30-45 DTE around 711.00/710.00 and cut if spot breaks 710.0758385663.

Actionable Summary

Structure beats direction here. With SPY at 710.51 sitting essentially on the gamma flip at 710.08 and net GEX of $297M anchoring a Positive Gamma shell, the trade is to sell 30-45 DTE Iron Condor structures around the 711.00/710.00 rails. Negative VRP at -1.66% paired with the positive-gamma cushion favors defined-risk over naked premium-selling.

Avoid naked upside calls - call skew at 15.15% sits below ATM, pricing zero upside conviction. Skip lottery strangles and outright vol length; Contango in the VIX curve will bleed carry. Keep sizing standard given VVIX at 98.73 stays in the normal zone, but size the tail hedge modest - vanna at -$235.01B is hostile if vol ticks up.

Watch the charm pivot at 710.0758385663 - break below and the dealer reaction function flips from supportive to accelerant. A breach of VIX3M at 21.24 drags vanna negative. Regime reads Elevated / Watchful - sticky, not panicked.

Iran de-escalation uncertainty is THE macro driver - it explains the bid in put wings, elevated VIX6M, and why dealers hold positive gamma but negative vanna

Global-economy spillover language means this is moving from geopolitical-shock (mean-reverts) toward macro-shock (compounds) - watch credit spreads and MOVE for confirmation

S&P Global cutting oil demand forecast 700k bpd is the demand-destruction signal - matters for cyclicals, energy, and inflation expectations feeding Fed reaction function

Gold weakness alongside equity chop means the USD is absorbing the safe-haven bid - unusual configuration, flags crowded USD positioning as next fragility

Oil back above $100 is the single most important level for re-rating inflation expectations and forcing the yield/equity correlation back to positive

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 19.17 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

Is SPY in positive or negative gamma today?

SPY is in Positive Gamma gamma with net dealer GEX at $297M. The gamma flip sits at 710.08, with the call wall at 711.00 and the put wall at 710.00.

Where is the SPY gamma flip level right now?

SPY's gamma flip is at 710.08 against a spot of 710.51. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.52% with a volatility risk premium of -1.66%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 19.36. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime