Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

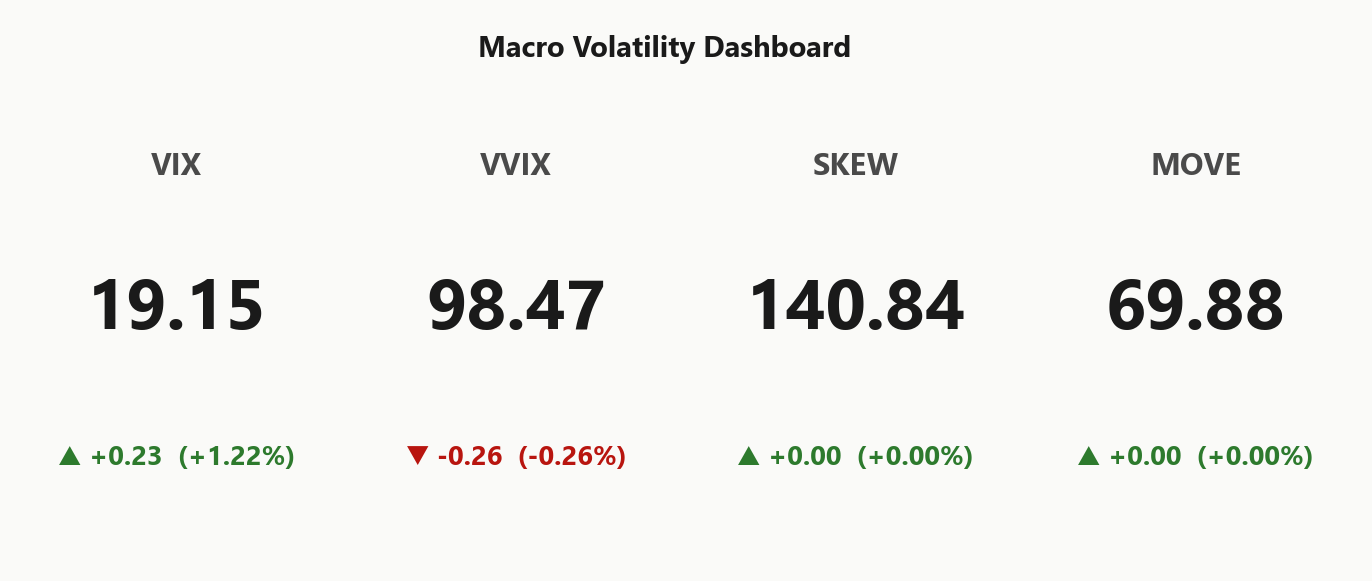

SPY at 710.73 sits inches below its call wall at 711.00, with net GEX at $848.9M keeping the regime firmly Positive Gamma - dealers dampen ranges, mean reversion wins. Gamma flip at 710.11 is essentially at spot, so any break below flips the tape from stabilizing to amplifying; put wall at 710.00 is the immediate downside magnet, max pain deeper at 695.00. Dealers are long gamma but net vanna at -$235.07B means a vol spike flips them into forced delta selling - that's the real accelerant risk, not today's drift. VIX at 19.15 with term structure in Contango (Steep contango - vol sellers favored) keeps the carry trade alive; VVIX at 98.47 says jump risk is normal, not extreme. VRP at -2.08% is modestly rich vs RV20 at 18.17 - options are fairly priced, not a giveaway. SKEW at 140.84 and the put-heavy 2.168 OI ratio confirm tail is bid into the Iran war news flow. Bottom line: Iron Condor in the 30-45 DTE zone is the cleanest expression - sell the carry, respect 710.11 as the regime hinge.

Positive gamma across index complex with VIX at 19.15 in contango - mean-reversion regime, Iran war tail bid

SPY at 710.73 is pinned tight to its call wall at 711.00 with net GEX at $848.9M - dealers dampen, not amplify. VIX term structure in steep contango (Steep contango - vol sellers favored) pays vol sellers, but 140.84 SKEW and Iran war headlines keep the left tail bid. The trade is carry inside the wall, not chase above it.

Regime Assessment

Current regime reads Elevated / Watchful with VIX at 19.15 - elevated enough to command respect, not enough to force defensive posture. Signal color is Yellow: watchful, not risk-off. The transition matrix is the tell - panic probability over five sessions sits at 0.05, a low-confidence move to dislocation, while the drift toward low-vol over ten sessions carries 0.45. Stasis is the base case.

Regime half-life of 15 sessions makes this state sticky - dealers stay long gamma, contango stays intact, mean-reversion keeps paying. The catch: half-lives describe ordinary decay, not catalyst-driven phase shifts. Iran war headlines are the one input that can collapse the distribution fast, flipping Elevated into backwardation without warning.

Trade the stickiness, respect the tail. Carry trades inside the wall remain the highest-edge expression; left-tail warrants stay cheap insurance against the one path the transition matrix underweights.

What it means for your trading

Regime labeled Elevated / Watchful with half-life of 15 sessions - sticky base case favors carry, but Iran war is the nonlinear catalyst the matrix can't price.

Trading readVIX elevated, VVIX normal, SKEW elevated, MOVE calm - the equity tail is bid but credit/rates are not confirming. Divergence says this is a geopolitical equity premium, not a systemic risk event.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

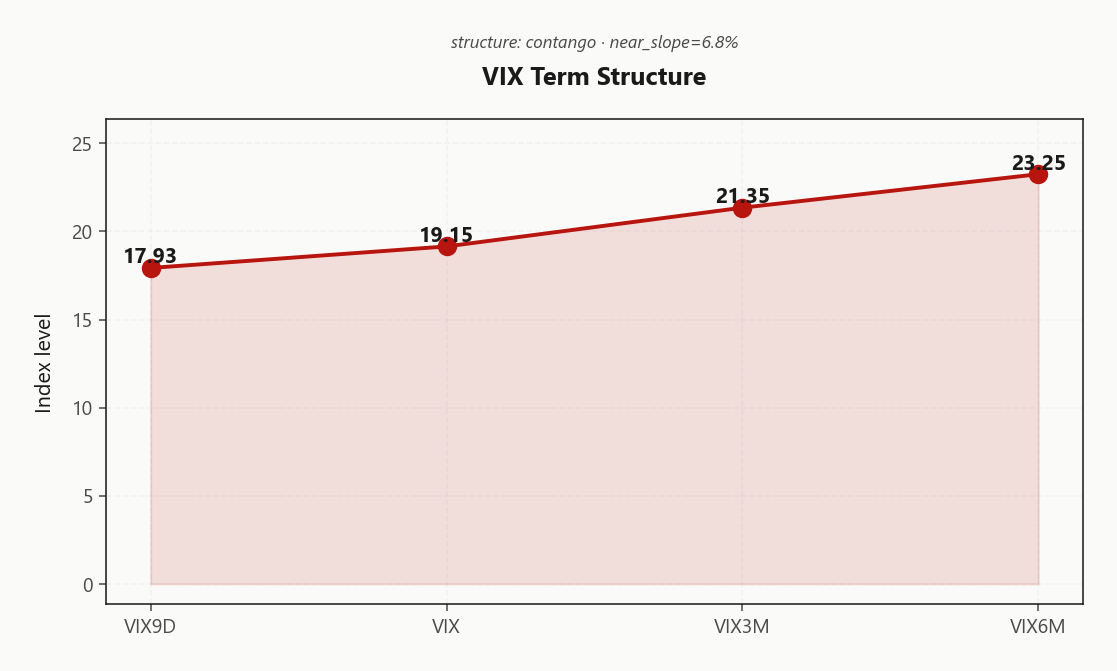

The VIX curve is in textbook Contango with front at 17.93, spot at 19.15, three-month at 21.35 and six-month at 23.25 - near-slope prints 6.8% and the regime tag reads Steep Contango. That is a carry trade paying you to be short forward variance into upstream event premium, with the Iran war tail bid paid for in the wings rather than in the belly.

Forward 30-60 sits at 22.3690075774 against spot VIX at 19.15, and forward 60-90 at 25.0060492681 - the curve is explicitly pricing mean reversion into a regime that has not happened. Long-dated vol is the richest leg; the cleanest monetization is the 30-45 DTE pocket where slope flattens and roll-down dominates theta.

Signal is Steep contango - vol sellers favored. The trade stays on until contango breaks - a flip toward backwardation is the first-class regime-change tell, and it comes before MOVE confirms. Until then, short the belly, own the wings, respect 710.11 as the hinge.

What it means for your trading

Steep VIX contango with near-slope at 6.8% and forward 30-60 at 22.3690075774 pays the carry trade cleanly in the 30-45 DTE window. Watch for contango breakdown as the earliest regime-shift signal.

Trading readContango with 6.8%% near-slope is textbook carry-trade regime - roll-down edge intact, and market is explicitly not pricing imminent stress despite Iran war. Breakdown in this curve is the first-class regime-change signal.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 16.09% is trading below HV20 at 18.17, pinning VRP at -2.08% - a negative print is unusual inside a Positive Gamma regime and flags that options have been cheap to the tape dealers are supposedly dampening. The IV/RV spread reads Negative Spread; sellers aren't being paid, they're paying to take risk.

The structural tell is RV5 at 12.81 collapsing well under RV20 at 18.17 - realized spiked off a calmer base and is already rolling over. If that cooling persists into the next tape, VRP re-riches fast and condor edge widens materially; if RV5 re-accelerates, short-vol books get squeezed before the gamma cushion can catch them.

Cross-index, 1.42% is the only positive-carry print in the core complex - small-cap condors pay today, SPY and QQQ don't. The trade is patience: wait for RV to bleed, or rotate the premium sale into IWM where the VRP math actually works.

What it means for your trading

Negative VRP with IV at 16.09% below RV20 at 18.17 means SPY vol is not a giveaway here - rotate carry into 1.42% IWM or wait for RV5 at 12.81 to cool further before reloading index condors.

Skew Convexity

Quarter-delta skew at 2.52% with a smile ratio of 1.18% prints an ordered tail bid - persistent, not panicked. Put 16.4% sits well above ATM 15.07%, confirming the Iran war headline tape is paying up for left-tail insurance without dislocating the broader surface.

The call wing is the tell: call quarter-delta at 13.88% is inverted versus ATM - traders are not paying one basis point for upside convexity. Zero breakout conviction, total asymmetric hedging demand. SKEW index at 140.84 corroborates the structural tail demand beneath the headline vol print.

The trade writes itself: skew is paying you to spread off. Buy put spreads over naked puts - you are shorting the steep wing against the belly and keeping the protection. Short upside call spreads or let the iron condor's call wing do the work; the inverted call curve means premium capture on that side is essentially a gift given zero upside chase priced in.

What it means for your trading

Ordered skew with put premium at 16.4% over ATM 15.07% and inverted calls at 13.88% means tail is bid but upside is dead - spread the puts, sell the calls, let the surface pay you on both wings.

Vol-of-Vol Structure

VVIX at 98.47 sits comfortably in Normal territory - below the jump-risk threshold that would force a binary-pricing regime. The VVIX/VIX ratio at 5.14 against spot VIX of 19.15 confirms the convexity bid is orderly, not panicked, which underwrites Standard Size across premium-selling books.

This is a clean environment for condor sellers: dealer gamma hedging is predictable, no convex regime surprise is priced, and the vol-of-vol tape isn't front-running an Iran war escalation that hasn't landed. The caveat is transmission speed - VVIX is precisely the surface that re-rates fastest on geopolitical tape, and the catalyst stack is live.

Operating trigger: VVIX punching through the mid-teens-above-current handle on Iran escalation flips sizing to half and pulls wings tighter. Until then, stay full-size inside the carry, respect the hinge at 710.11, and treat today's vol-of-vol print as permission - not invitation - to press the short-gamma premium trade.

What it means for your trading

VVIX at 98.47 with a Normal read supports Standard Size - press the condor carry, but the Iran war tape is the one catalyst that can bid convexity fast.

Dispersion Spread

Index IV at 16.09% against QQQ at 21.44% and IWM at 23.4% shows the complex trading moderately correlated - not tight enough to squeeze dispersion shorts, not loose enough to reward single-name strangles. Cross-asset tape is Aligned, with every core index carrying a Positive Gamma stamp. The dispersion trade has no dislocation to harvest today.

Single-name variance is where the noise lives. The mover book - NVDA, AAPL, AMZN, MSFT, META - sits inside an earnings parade that bids idiosyncratic vol without a matching index hedge. Index puts won't catch an NVDA gap; single-name strangles won't carry if the benchmarks stay pinned to 711.00. The cleaner expression is Iron Condor on SPX/SPY, selling index carry and letting earnings risk stay unhedged in cash sizing.

Watch for a dispersion squeeze if cross-asset tone breaks from Unknown - that's the signal single-name premium starts funding itself.

What it means for your trading

Moderate index-vs-single-name correlation leaves no dispersion edge to harvest; sell index carry via Iron Condor in the 30-45 DTE window and keep earnings risk in cash, not in strangles.

Liquidity & Microstructure

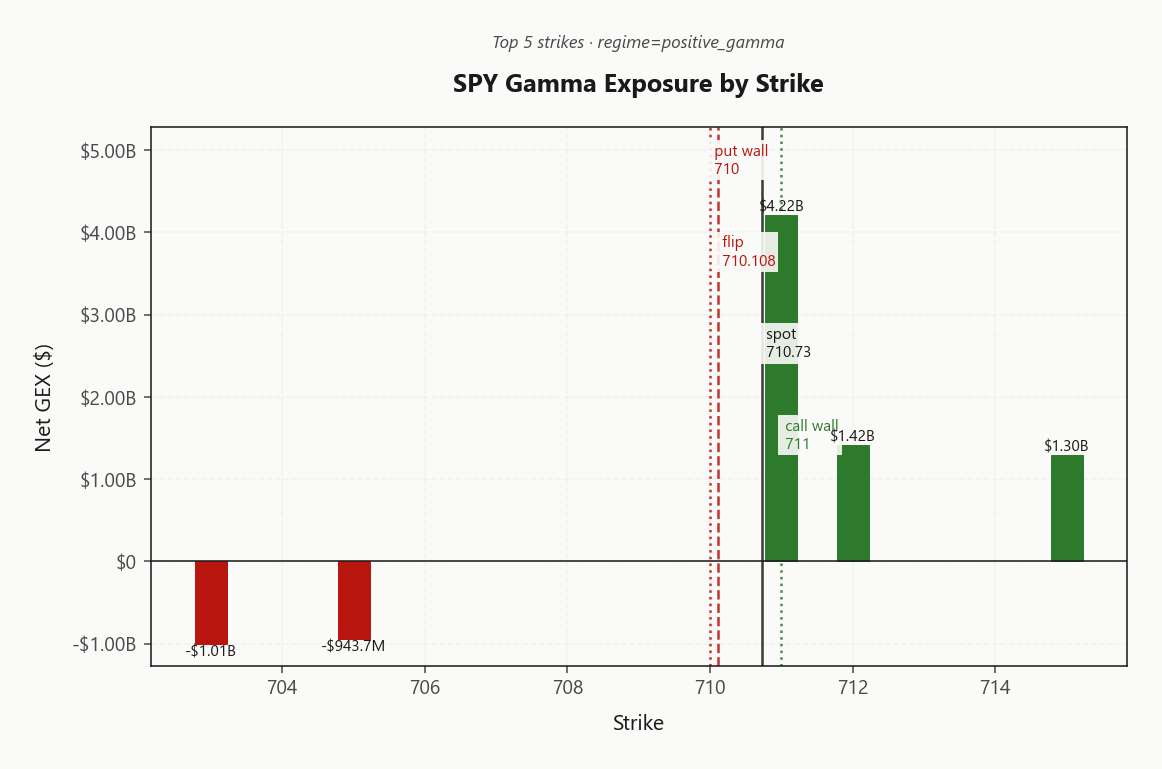

The book is organized around a single dominant cluster: top strike 711.00 carries net GEX of $4.22B, with highest OI anchored deeper at 600 acting as the longer-term magnet. Call wall at 711.00 caps rallies while the put wall at 710.00 catches dips - a tight corridor where mean-reversion flow dominates and dealers dampen excursions rather than amplify them.

The hinge is live. Gamma flip sits at 710.11 - essentially kissing spot at 710.73. Above it, dealers buy dips and the tape stabilizes; a break below flips the regime from Positive Gamma dampening into forced selling. Zero-DTE GEX at -$95.9M is negative, injecting intraday chop amplifier under a positive-gamma broader book - whippy action that doesn't translate to daily range expansion.

What it means for your trading

Fade excursions toward 711.00 inside the 710.00/711.00 corridor; treat 710.11 as the regime hinge - break below flips dampening to amplifying.

Trading readDealers are long gamma densely around 711.00 which caps rallies, and the top strike cluster at 711.00 is where mean-reversion flow is heaviest - fade excursions toward it, respect the gamma flip at 710.11 as the regime switch.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealers are long gamma but net VEX at -$235.07B is deeply negative - a vol spike transmits directly into forced delta selling. That is the accelerant risk hiding underneath today's pinned tape, not the drift. Net CHEX at -$705.8M adds mechanical time-decay pressure into the close, leaning sellers into rallies.

Trade it accordingly: harvest carry inside the wall while the regime is intact, but keep cheap left-tail on - the vanna channel is the route through which an Iran war headline would compound a VIX tick into a delta cascade.

What it means for your trading

Dealers stabilize today but net VEX at -$235.07B means a VIX pop flips them into forced selling; the charm pivot at 711 is the regime hinge to watch.

Cross-Asset Confirmation

MOVE sits at 69.88 unchanged - rates and credit are flatly refusing to confirm the equity tail bid. Fear & Greed prints Greed at 68, a risk-on undertone that is not what a compounding geopolitical shock looks like across asset classes.

QQQ at 655.30 and IWM at 276.53 are Aligned with SPY in the same positive gamma regime - no index is cracking first, no divergence lead to trade. Iran war premium is being paid in commodities and shipping, not in credit spreads or swaption vol. That compartmentalization is the tell: equity-only event premium, not systemic.

Bottom line: mean-reversion regime intact. The signal that regime compounds - and the moment to cut carry - is a MOVE breakout. Until then, the cross-asset tape is pricing a contained shock, and the aligned positive gamma book across the index complex keeps the condor carry trade structurally live.

What it means for your trading

Credit and rates aren't confirming the equity tail bid - MOVE at 69.88 and Fear & Greed at Greed (68) flag this as a contained geopolitical equity premium, not a systemic regime break. Stay in carry until MOVE breaks.

Scenario EV

Scoring shakes out clean: Iron Condor takes the book at 36, decisively ahead of the put spread alternative at 23. Positive gamma anchoring the tape, VIX term in Contango, and vol-of-vol running Normal is the textbook three-factor alignment for range selling - dealers dampen, carry pays, and jump risk isn't priced convex enough to chew through premium.

Sweet spot is the 30-45 DTE band, where term slope flattens and roll-down edge compounds inside the Iran-war event window without buying dated vol that's priced for a regime that hasn't arrived. VRP reads Unknown in the framework, so this is carry harvesting off structural contango, not a rich-vol giveaway - respect it.

Structure the wings outside 711.00 and 710.00, size per Standard Size, and treat 710.11 as the regime hinge that kills the trade if it breaks.

What it means for your trading

The condor at 36 is the cleanest expression today - sell 30-45 DTE carry with wings parked outside 711.00 and 710.00, standard size, gamma flip as the kill switch.

Avoid naked upside calls - call skew is inverted at 13.88% versus ATM 15.07%, zero conviction to chase. Skip short vol in 0DTE where net GEX at -$95.9M amplifies intraday chop. Respect the charm pivot at 711 - spot is 0.0379891098 away and this is the regime hinge, with the gamma flip at 710.11 essentially kissing tape.

Iran war keeps tail warrants warranted while SKEW holds at 140.84 - buy cheap lottery puts outside the condor, don't skip them. Watch 69.88 MOVE for a breakout; that's the signal the shock is compounding into credit and the Elevated / Watchful regime cracks.

What it means for your trading

Sell the Iron Condor carry in 30-45 DTE inside the 711.00/710.00 walls, with cheap tail puts bolted on while SKEW at 140.84 stays bid. The 710.11 flip and 711 charm pivot are today's regime hinges - a MOVE breakout from 69.88 is the signal to cut.

Iran war impasse is the single dominant tape driver - explains why skew is bid, MOVE isn't breaking out, and why call wall holds despite no bullish catalyst.

Macro-global impact of Iran war means this isn't an isolated equity shock - it's feeding into commodities, logistics, and inflation, which is why vol term structure stays in contango rather than backwardation.

S&P Global PMI showing Iran war is driving input prices up is the stagflation-lite tell - Fed reaction function complicates any vol-down path and keeps put wings bid.

Trump approval plunge on economy is a political-risk tail few traders are pricing - compresses the administration's crisis-response options and feeds regime-shift probability.

S&P Global cutting 2026 oil demand forecast by 700k bpd reframes the Iran war from acute shock to structural growth drag - bearish for cyclicals, neutral-to-bullish for defensive positioning.

Foreign flows into Japan on US-Iran peace hopes and AI rally is the cross-asset read - risk appetite exists globally but is staying out of US beta while the flip hinge is live.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 19.11 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 710.11 against a spot of 710.73. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.09% with a volatility risk premium of -2.08%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 19.15. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime