Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY at 709.13 is holding just above the gamma flip at 707.63, net GEX -$2.72B in Positive Gamma - dealers damping intraday moves. Key levels: call wall at 705.00, put wall at 705.00, max pain 706.00 - tight pin zone into the bell. Dealer vanna $80.5M and charm -$242.6M say vol-up buys delta (supportive) but time decay leans offer into close. VIX at 19.32 with term structure Contango at 8.24% slope - carry regime, but VVIX at 100.93 is not cheap, tail hedges still warranted. VRP reads -2.5% - options not richly priced to recent realized. Cross-asset: IWM at 275.50 sits below its flip at 275.82 in Negative Gamma - small-cap fragility is the tell. Bottom line: run Iron Condor in 30-45 DTE on SPY/QQQ, avoid naked IWM premium sales, and treat 707.63 as the line that flips dealer behavior.

SPY sits in positive_gamma above 707.63 with contango term structure and Steep contango - vol sellers favored, keeping dealer flow mean-reverting. IWM diverges in negative_gamma below its flip, so small-cap downside is amplified even while the large-cap complex pins. With Elevated / Watchful regime and VVIX at 100.93, the playbook is carry with tail respect - Iron Condor in the 30-45 window.

Regime Assessment

Regime read: Elevated / Watchful with VIX at 19.32 - the transition matrix prints a 0.05 five-session probability of a panic flip against a 0.45 ten-session drift into low-vol. The asymmetry favors mean-reversion lower, but the panic tail is non-zero and that is the number to respect when sizing.

Half-life clocks at 15 sessions - stickiness is moderate, not glacial. That is a two-week planning horizon, not a month; carry structures beyond that window are fighting the regime clock. Cross-asset tape is Aligned across large-cap, but IWM sitting in Negative Gamma below its flip is the fragility tell that would lead any repricing.

Elevated / Watchful regime with VIX at 19.32 and half-life 15 sessions - carry is the base case but the 0.05 panic probability keeps tail hedges on the book.

Trading readVIX moderate, VVIX elevated, SKEW at 140.91, MOVE muted - the tell is VVIX holding up against a contained VIX: vol-of-vol hedgers are active even while headline vol is calm. Watch for VVIX to lead VIX if this regime breaks.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

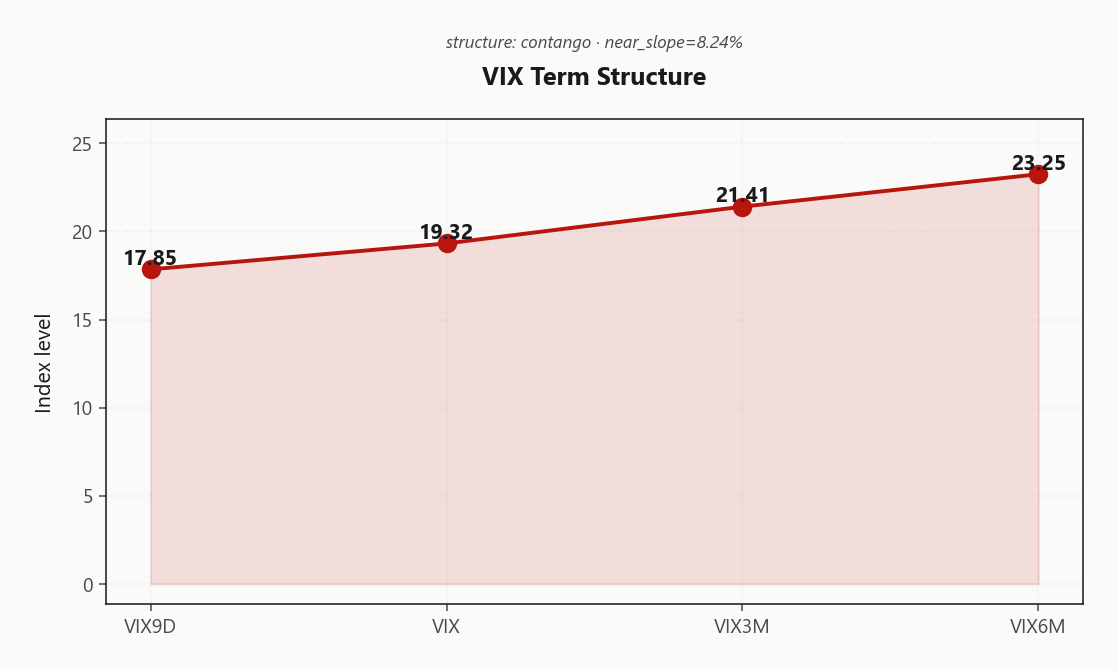

VIX term structure prints Contango with near-slope at 8.24% - VIX9D 17.85 sits well under VIX 19.32, VIX3M 21.41, and VIX6M 23.25. No event premium is priced into the front; the curve is structurally paying carry and the regime label reads Steep contango - vol sellers favored.

Forward 30-60 at 22.3819335626 marks the richest roll-down on the curve - the kink in the belly is where theta meets vega without giving back to near-date realized. Selling the ultra-front chews through thin premium; the edge lives in the middle.

Playbook: sell in the 30-45 DTE bucket and roll down the kink. Front-month shorts fund nothing after slippage; mid-curve vega earns the contango paycheck while leaving room to reload if the curve flattens.

What it means for your trading

Curve is Steep Contango with no event risk priced short-dated - carry regime favors mid-curve short vol. Sweet spot sits at the 22.3819335626 forward in the 30-45 DTE window, not the front.

Trading readContango with near-slope 8.24% and front-month futures basis 10.89% over spot - textbook carry regime, market expects no near-term stress, roll-yield is the paycheck.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

HV20 at 18 is printing hotter than ATM IV at 15.5%, leaving SPY VRP at -2.5% - index options are not rich to recent realized. The short-vol edge at the front of the curve has been compressed out, and HV20 running above HV60 at 15.31 says near-term realized is still accelerating, not decaying.

QQQ mirrors the same under-pricing with VRP -1.72% - large-cap tech offers no premium cushion either. The lone exception is IWM, where VRP prints 1.52%: the only index surface where writers are actually being paid over recent realized, even with small-caps in Negative Gamma below the flip.

Trade implication: step out the curve to the 30-45 DTE bucket where IV firms up and the carry math works, or stay strictly defined-risk at the front. Naked premium sales on SPY/QQQ ATM are earning structure, not vol - the cushion isn't there.

What it means for your trading

Index ATM IV trades below realized - short-vol edge lives in the 30-45 belly, not the front. IWM VRP at 1.52% is the only outright premium, but the negative-gamma backdrop demands defined-risk expression.

Skew Convexity

The 4.4% quarter-delta skew with a smile ratio of 1.32% prints an ordered downside bid, not a panic grab. Put wing at 18.04% sits cleanly over ATM 15.29% - the kind of hedging demand that shows up when PMs are rolling protection, not chasing it. Smile geometry remains inside the typical index band, so there is no dislocation to fade on the wing itself.

The call side tells the other half of the story: 13.64% prints below ATM, an inverted upside wing that says the tape is paying nothing for a melt-up. Zero call-chase conviction into a positive-gamma grind - consistent with mean-reverting dealer flow above 707.63. Do not fund downside by selling the call wing; there is nothing to harvest.

Trade expression: put spreads beat naked puts given the ordered put bid - you are buying the wing at a premium, finance it against a further OTM put, not the call side. The real tail bid lives in VIX options, where quarter-delta skew reads -94.46% - VIX upside calls remain the cheapest convex hedge on the book.

What it means for your trading

Ordered put bid with an inverted call wing - buy put spreads for SPY downside cover and keep VIX upside calls as the convex tail, since the index call wing offers nothing to sell at 13.64% below ATM.

Vol-of-Vol Structure

VVIX at 100.93 against VIX 19.32 puts the ratio at 5.22 - squarely in Normal territory. Not extreme, not cheap. The tape isn't pricing a bimodal jump, but a VVIX holding triple digits against a contained VIX says hedgers are still live in VIX options - the convex bid hasn't left the building.

VVIX ticked 2.83% today; watch for acceleration, not absolute level, as the break signal. The ratio sitting in the normal regime band is what keeps sizing constructive - Standard Size is the call. Don't halve until VVIX breaches extreme.

Takeaway: run standard book size on short-vol expressions, but keep VIX upside calls on as the cheap tail - vol-of-vol is telling you the hedge bid is structurally there even when headline vol looks sleepy.

What it means for your trading

Vol-of-vol sits in Normal range with VVIX/VIX at 5.22 - Standard Size, but keep VIX upside convexity given VVIX 100.93 isn't cheap.

Dispersion Spread

Dispersion is the cleanest tell on the tape. IWM ATM IV at 23.58% trades meaningfully rich to SPY at 15.5%, with QQQ at 20.31% sitting modestly above the broad index - a textbook small-cap idiosyncratic premium with a mega-cap concentration kicker layered on top. The spread is wide enough that single-name vol is doing the work the index complex is not.

That divergence dictates vehicle selection. SPX/SPY is the preferred surface for any short-vol expression - index correlation is suppressing realized at the headline level, and the dispersion trade is implicitly being paid by anyone short component vol versus long index vol. Avoid naked single-name premium sales here; the regime is paying you to be long dispersion, not short it.

The one exception is IWM itself: VRP at 1.52% is the only tradable positive surface in the complex, so condor or defined-risk premium harvest can be expressed there directly - but size around the Negative Gamma backdrop, not the headline IV print.

What it means for your trading

With IWM IV at 23.58% rich to SPY at 15.5% and QQQ at 20.31% in between, dispersion is alive - express short-vol through index, not single names, and reserve IWM premium sales for defined-risk structures given the positive VRP at 1.52%.

Liquidity & Microstructure

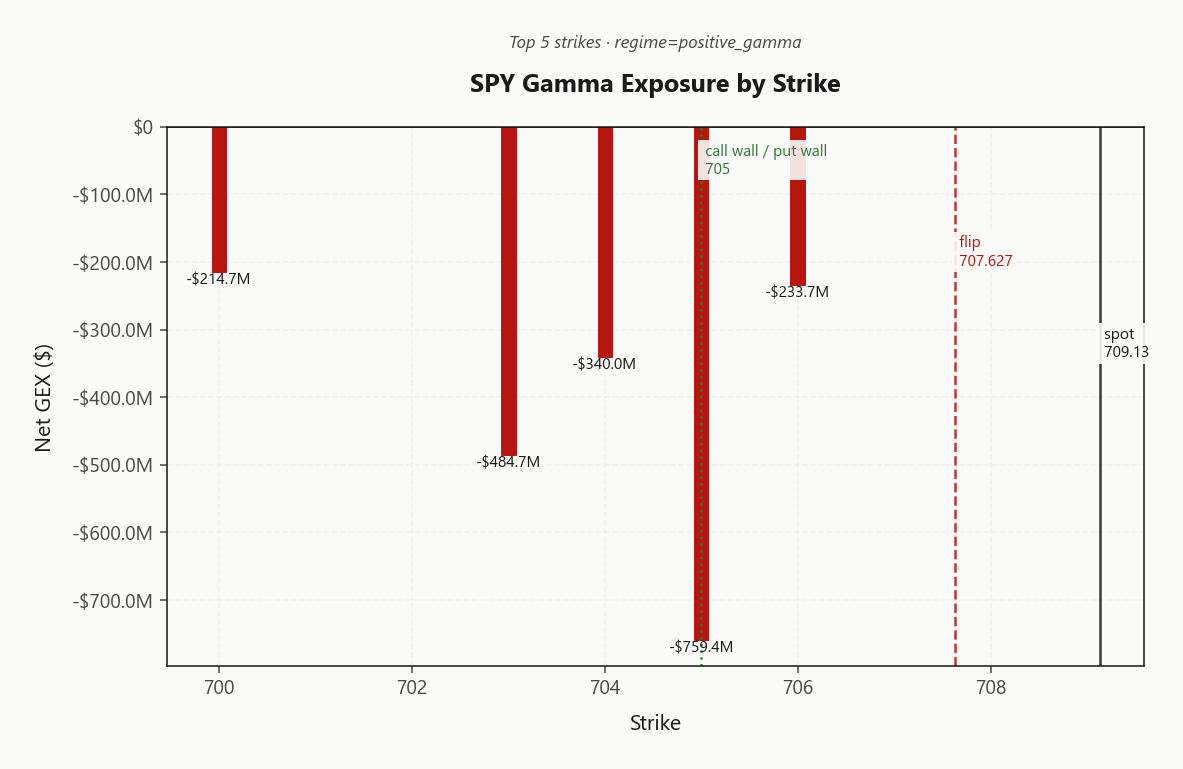

The book's center of gravity is unambiguous: top-GEX strike at 705.00 carrying -$759.4M is the operative magnet, with the call wall and put wall stacked at the same strike at 705.00 / 705.00 - a textbook pin geometry. Max pain at 706.00 sits inside that same zone, and highest OI at 693 anchors the structural floor of open interest below.

The line that matters is the gamma flip at 707.63. Above it, dealers buy dips and sell rips - the mean-reverting hedging signature that makes the pin work. Lose it and the polarity inverts: dealers sell strength and chase weakness, and the magnet releases.

Trade the geometry, not the tape. Range-fade into the stacked wall while spot holds north of the flip; treat any clean break below 707.63 as the regime signal that flips dealer flow and ends the pin.

What it means for your trading

Stacked walls at 705.00 with -$759.4M of GEX at 705.00 define a tight pin; 707.63 is the binary switch between mean-reverting dealer flow and trend-amplifying selling.

Trading readGamma stacks into the call wall and put wall at the same strike with a top-cluster just below spot - that's a pin geometry, meaning dealers dampen every push until price clears 707.63, at which point flow flips and the magnet releases.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealer second-order book splits the tape: net VEX reads $80.5M positive while net CHEX prints -$242.6M - vanna is a buyer of delta on any vol spike, charm is a seller of it as theta bleeds into the bell. Translation: rising VIX props the bid, a flat tape lets charm-driven offers win the close.

The single line that matters is the pivot at 707.627423607, with spot riding -0.2118901179 to it and current bias reading Supportive. Cushion is razor-thin - above, vanna and gamma co-operate to pin; lose it and charm flips from background drag to active seller, accelerating into settlement.

Trade it as two regimes separated by one level: while spot holds the pivot, fade strength and buy weakness inside the 705.00 - 705.00 corridor. Breach below 707.627423607 and the supportive-vanna trade dies - covers first, shorts second.

What it means for your trading

Vanna $80.5M is supportive on vol up, charm -$242.6M is hostile into close - regime hinges entirely on holding the 707.627423607 pivot where bias reads Supportive.

Cross-Asset Confirmation

Rates vol is asleep - MOVE at 70.78 tells you this is not a credit- or duration-led episode, which is the first confirmation the equity pin geometry can be trusted. Sentiment corroborates: Fear & Greed at 68 reads Greed, a risk-on tape where hedging demand is mechanical rather than panicked.

The single crack in the cross-asset picture is small-cap. SPY at 709.13 and QQQ at 652.41 are both parked in Positive Gamma above their flips, while IWM at 275.50 has slipped beneath its flip at 275.82 into Negative Gamma. Regime divergence reads Aligned on the large-cap complex - tone Unknown - but the Russell is the carry the room is short.

Playbook: fragility is small-cap-specific, not systemic. Express short-vol on SPY/QQQ, keep IWM on the avoid list, and watch MOVE as the first confirming tape if this ever turns credit.

What it means for your trading

MOVE at 70.78 and Fear & Greed Greed confirm a risk-on, non-credit tape; the only divergence is IWM at 275.50 beneath its flip 275.82 while SPY 709.13 and QQQ 652.41 hold positive gamma - trade the large-cap pin, respect small-cap fragility.

Scenario EV

The EV surface ranks Iron Condor at 50 - the cleanest fit for a Unknown VRP tape paired with Steep contango - vol sellers favored. Sweet spot is the 30-45 DTE window, where curve carry and vega decay compound without bleeding through the thin near-date premium that's making the front of the book uneconomic.

Put spread scores 39 - a distant second and not a standalone directional expression here. Deploy it as a hedged overlay against the condor's downside wing or against IWM fragility below 275.82, not as a naked bearish bet. Size to Standard Size: VVIX at 100.93 isn't flashing a halve-the-book signal, but a Elevated / Watchful regime doesn't pay for heroics either.

Execution: work the condor on SPY/QQQ where the positive-gamma pin geometry around 705.00 does the heavy lifting, skip IWM short-premium outright, and keep VIX upside calls as the convex tail.

What it means for your trading

The book is Iron Condor in 30-45 DTE at 50, with put spread as overlay at 39. Carry the mid-curve at Standard Size and let the pin do the work.

Actionable Summary

Synthesis is carry-with-respect: SPY and QQQ anchor in Positive Gamma above their flips while IWM dangles in Negative Gamma below 275.82. The regime label reads Elevated / Watchful with VVIX at 100.93 and term structure in Contango - the curve pays to sell, but vol-of-vol is not giving you the all-clear.

Trade expression: run Iron Condor on SPY/QQQ in the 30-45 DTE bucket where VRP firms up, and keep the dealer pivot at 707.627423607 as your regime line - spot above it, dealers damp; below it, charm flips offer and the pin releases. Avoid naked IWM premium; its short-gamma surface amplifies, not absorbs.

Convex tail hedge stays cheap in -94.46%-skewed VIX upside calls - size the book Standard Size and treat any breach of the flip as the signal to cut short-vol, not add.

What it means for your trading

Carry the mid-curve with Iron Condor on the large-cap complex, treat 707.627423607 as the dealer-flow switch, and fund VIX upside convexity while Elevated / Watchful keeps tails live.

Strait of Hormuz semi-closed with ongoing ship seizures keeps an energy-supply tail risk live - the reason VIX is not collapsing despite positive gamma and why any VIX upside call remains the cheapest tail hedge.

Wall Street rallying on ceasefire-extension and earnings relief is the proximate cause of today's positive-gamma pin - it explains why dealers are long gamma and mean-reversion is working, until a headline breaks it.

Germany halving its growth forecast while raising inflation on the Iran war is the macro tape bomb that could re-price EU front-end rates and bleed into global risk - watch MOVE as the confirming indicator.

Ambiguity over who is actually running Iran raises binary-outcome risk - exactly the kind of headline that would crack the contango curve into backwardation if it intensifies; keep VIX upside convexity on.

FX and stock dip on ceasefire uncertainty with central bank decisions as the next catalyst - confirms the market wants to carry but is one headline from a vol repricing.

UK inflation jumping to 3.3% on the first Iran-war hit is the live evidence that the supply shock is already in CPI prints - supports structurally higher vol in back-month index options even if the front is calm.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 19.38 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 707.63 against a spot of 709.13. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 15.5% with a volatility risk premium of -2.5%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 19.32. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime