Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

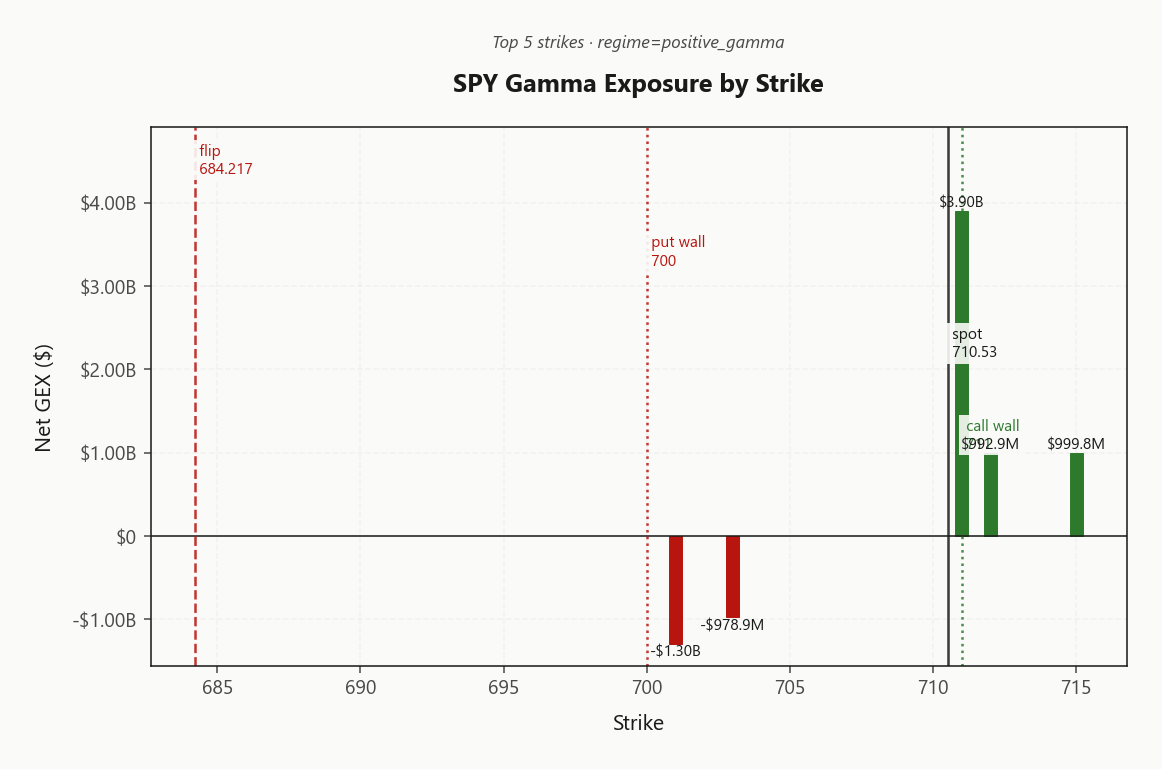

SPY settled at 710.53 in Positive Gamma with net GEX of $2.07B - dealers are long gamma and pinning flow stays mean-reverting. Call wall sits at 711.00 directly overhead; put wall 700.00 is the rally pocket floor; gamma flip at 684.22 sits well below spot, giving a deep cushion that turns any dip into a dealer-buy reflex. Dealer vanna is -$237.4B (negative) - a vol spike would force them to sell delta into weakness, the single asymmetric risk in this tape. Charm -$700.1M leans mildly supportive into expiry. VIX at 18.74 with term structure in Contango (VIX9D 17.02 / VIX3M 21.12) signals zero near-term event premium - VRP -2.3% says options are cheap to 20-day realized but vol sellers still earn carry further out. Bottom line: fade strength into 711.00, buy dips into gamma-flip cushion, and deploy iron condors in the 30-45 DTE window while VVIX stays contained.

SPY prints 710.53 squarely above the gamma flip at 684.22, keeping dealers long gamma and rally-dampening flow in charge into the close. VIX term structure is in Contango with VVIX at 98.75 - normal vol-of-vol, meaning the bid under vol carries is real. Iron condor emerges as the cleanest risk/reward given Unknown VRP conditions and the Elevated / Watchful backdrop.

Regime Assessment

Regime clocks in at Elevated / Watchful with VIX anchored at 18.74 - not panic, not complacent, and crucially sticky. The transition matrix prices panic escalation over the next week at only 0.05, while the fade-to-low path over two weeks runs 0.45. Asymmetry tilts toward decay, not escalation.

Half-life of 15 sessions is the number that matters - it is long enough to underwrite carry structures without the regime evaporating under you. Cross-asset tone is Aligned, with SPY, QQQ and IWM all camped in Positive Gamma and VIX term structure holding Contango. No regime-break signature in the cross-section.

Playbook: treat Elevated as the carry window, not the warning light. Deploy Iron Condor in the 30-45 DTE sleeve and let half-life do the work. The only trigger that shortens this clock is a VVIX break above 98.75.

What it means for your trading

Elevated / Watchful at VIX 18.74 with a 15-session half-life is a tradable carry window - panic transition priced at 0.05, fade-to-low at 0.45, asymmetry favors decay. Run Iron Condor structures until VVIX breaks.

Trading readVIX, VVIX, SKEW, and MOVE all pointing the same direction - no inter-metric divergence to flag a regime shift. Calm confirmed by multiple lenses.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

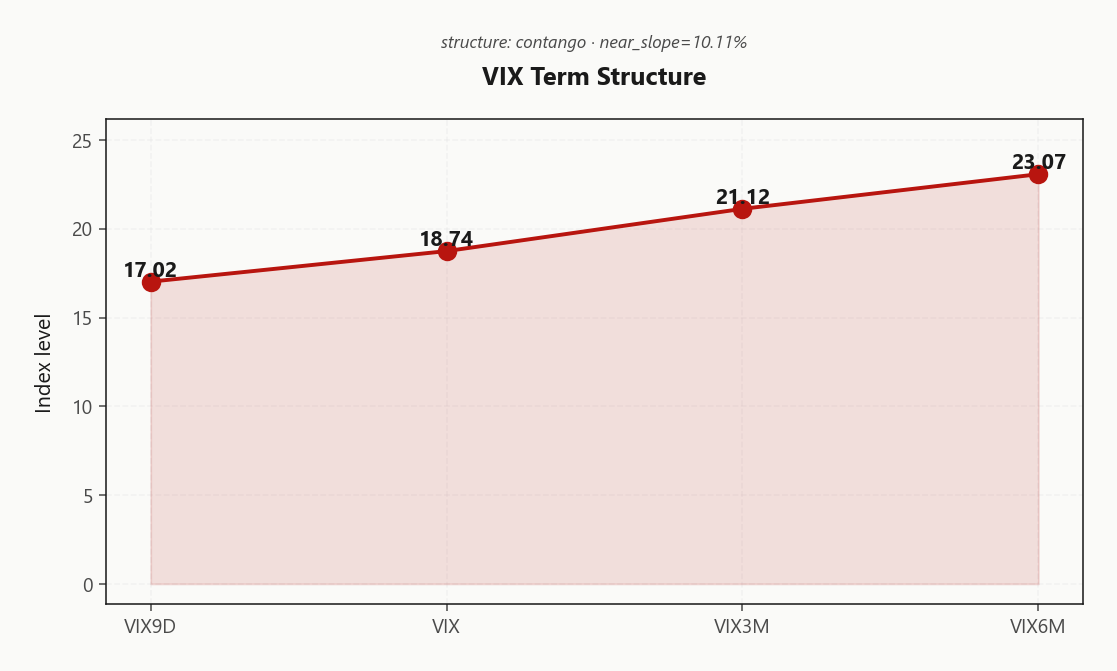

The VIX curve prints Contango with VIX9D at 17.02 sitting well beneath spot VIX 18.74 - zero short-dated stress bid, zero event premium baked into the front. The slope extends cleanly out to VIX3M at 21.12, the kind of shape where rolling short vol gets paid on carry alone.

Forward 30/60 vol at 22.2145852989 marks the inflection where the curve stops paying the seller linearly and starts rewarding structure - the sweet spot for iron condors rather than naked strangles. Calendar buyers need to stretch DTE to find a kink; the front is too flat to finance.

Steep contango from 17.02 through 21.12 pays vol sellers who stretch DTE; the front is too flat to monetize. Deploy carry in the belly, not the nose.

Trading readContango with Steep contango - vol sellers favored - vol carry is live and clean, market is not pricing near-term stress despite the geopolitical headline drip.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 15.79% prints materially below HV20 at 18.09 - options are genuinely cheap to what the tape has actually delivered. That is a rare footprint inside a Positive Gamma regime, where pinning flow usually crushes implieds through realized, not under it. The read: recent realized absorbed a pickup the front-end curve has not yet re-priced.

HV60 at 15.38 sits below HV20, confirming the delivered-vol impulse is decelerating from a local pickup rather than trending higher. VRP prints -2.3% - negative short-dated. Selling front-week naked here is picking pennies against a realized base that has not yet fully cooled; the premium-selling edge has migrated out the curve.

Preferred expression: calendars long front / short back to harvest the shape, or 30-45 DTE iron condors where carry re-emerges and Standard Size is green-lit by contained VVIX.

What it means for your trading

Options cheap to HV20 with VRP -2.3% negative short-dated - don't sell front-week naked; push premium sales into the 30-45 DTE window where carry lives.

Skew Convexity

Downside wings are doing the pricing work. 3.07% on the quarter-delta skew with a smile ratio of 1.25% says put protection is still bid hard even as spot rides the call wall - a one-sided convexity market where ATM at 13.32% sits anchored while the put-side carries 15.42% against a suppressed call-side 12.35%. Translation: hedgers are paying up for downside, nobody is paying up for upside participation.

That asymmetry is a financing gift. With call skew flat, call spreads are cheap and become the clean leg to fund put-side protection or spread structures. Naked puts overpay the vol; put spreads capture the skew premium without paying the full wing. Risk reversals lean decisively in favor of selling calls to buy puts here - the market will subsidize your hedge.

Watch the smile ratio for compression: if call-side firms while ATM stays anchored, the one-sided bid is breaking and the vanna-ambush thesis gets a real catalyst. Until then, trade the skew, don't fight it.

What it means for your trading

Quarter-delta skew at 3.07% with smile ratio 1.25% signals ordered downside demand, not panic - express via put spreads financed by cheap call spreads rather than naked wing buys.

Vol-of-Vol Structure

VVIX prints 98.75 against VIX 18.74, placing vol-of-vol squarely in the Normal band. Jump risk is on the board but not panic-bid - the market is not pricing a bimodal outcome, and the VVIX/VIX ratio at 5.27 confirms a single-mode distribution rather than a fat-tailed one.

That matters for sizing. With vol-of-vol contained, the Standard Size green-light holds - no need to half-size short-vol structures into the Iron Condor deployment. Contango at the front of the curve plus normal VVIX is the cleanest possible carry backdrop for the 30-45 DTE window.

The one trigger that flips the book: a VVIX break above the prior swing. That is the sizing-down signal and the moment the latent vanna risk embedded in -$237.4B turns active. Until then, treat the tape as mean-reverting and lean into the carry.

What it means for your trading

VVIX at 98.75 against VIX 18.74 keeps vol-of-vol Normal and clears Standard Size for short-vol structures. Watch a VVIX break of the prior swing as the single trigger to cut size.

Dispersion Spread

Index vol is priced too cheaply relative to the single-name complex sitting underneath it. SPY ATM IV at 15.79% against QQQ 21.38% and IWM 23.3% prints a Moderate dispersion tone - the index is absorbing the single-stock dance through correlation, not through outright vol.

IWM is the standout: its ATM IV runs rich to realized in a way the mega-cap indices do not, so small-cap correlation is offering less protection per unit of premium. That pushes the cleanest short-vol expression back to SPY and QQQ - where the correlation bid is doing real work - and argues against chasing cross-sectional single-name shorts when the index tape already bundles that exposure at a tighter spread.

Preferred expression: index-level vol selling on SPY/QQQ over single-name shorts, with IWM reserved as a dispersion-rich satellite for premium-seeking sleeves.

What it means for your trading

Dispersion prints Moderate with SPY ATM IV 15.79% well beneath QQQ 21.38% and IWM 23.3% - index vol selling offers cleaner risk-adjusted carry than single-name shorts today.

Liquidity & Microstructure

SPY's strike topology is doing the heavy lifting into the close: the 600 open-interest cluster sits as a deep structural anchor while the top GEX strike prints $3.9B right at 711.00 - the call wall itself. That concentration collapses dealer polarity onto a single pivot at 684.22: above it, hedging flow buys weakness; below it, the same book sells bounces.

With spot riding the 711.00 call wall and the 700.00 put wall framing the rally pocket floor, the microstructure is textbook Positive Gamma - dealers cushion dips into the flip, then fade strength into the wall. Cross-asset tape is Aligned, so no outside flow disrupts the pin.

Trade it as a range-compress: fade strength into 711.00, accumulate into the 684.22 cushion, and treat a close below the flip as the one signal that inverts the dealer reflex.

What it means for your trading

Strike-level OI concentration pins dealer flow tightly around 684.22, with the 711.00 call wall capping immediate upside and the 700.00 put wall backstopping dips. Trade the range until the flip breaks.

Trading readDeep positive gamma clustered at and above spot says dealers dampen every move - rallies into 711.00 should fade, dips into 684.22 should be bought unless the flip breaks.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Gamma pins, but vanna is the ambush. Net VEX at -$237.4B is deeply negative - a VVIX pop flips dealers into selling delta into weakness, converting the otherwise mean-reverting tape into an accelerant. That is the single asymmetric tail embedded in this book; everything else about the regime is supportive.

Charm tilts mildly hostile into the close with net CHEX at -$700.1M, but the read is modest, not directional. The charm pivot sits at 711 with spot 0.0661478052 away and bias tagged Neutral - no tailwind, no headwind, call it a wash into expiry.

One thing to watch: VVIX. While VVIX holds Normal at 98.75, the vanna risk stays latent and standard sizing is green-lit. A clean break higher is the trigger that converts this from a pinning tape into a dealer-sold delta cascade. Until then, trade the gamma; respect the vanna.

What it means for your trading

Gamma pins the tape but net VEX at -$237.4B means a VVIX spike is the one event that forces dealer delta-selling into weakness. Watch VVIX - that's the trigger that flips vanna risk from latent to active.

Cross-Asset Confirmation

Cross-asset tape reads Unknown with regime divergence Aligned - SPY, QQQ at 655.75, and IWM at 276.04 all sit above their gamma flips in positive_gamma, while VIX remains the lone negative-gamma outlier. This is the signature of a coordinated index bid, not a credit or macro shock.

MOVE at 70.78 is effectively asleep - rates vol refuses to confirm the geopolitical headline drip, and without a MOVE break the Hormuz/Iran tape stays a mean-reversion trade, not a tail-bid catalyst. Fear & greed prints 68 in the Greed zone: complacent enough to keep the carry live, not euphoric enough to mark a contrarian fade.

Implication: geopolitical headlines mean-revert inside this regime. The one thing that flips the read is a MOVE break - until then, cross-asset alignment is the green light to run the positive-gamma playbook.

What it means for your trading

Index complex aligned in positive gamma with MOVE at 70.78 and fear & greed at Greed - this is a mean-reversion tape, not a shock signature. Watch MOVE: a break there is the only cross-asset tell that invalidates the carry trade.

Scenario EV

Strategy bench ranks Iron Condor at the top with a best score of 41, clearing the put spread alternative at 29 on a risk-adjusted basis. Steep contango pays the carry, Positive Gamma across the index complex anchors the tape, and VVIX at 98.75 against VIX 18.74 lands Normal - green light for Standard Size, no need to half-size the book.

DTE window 30-45 is the sweet spot: far enough out the curve to capture term-structure carry past the Unknown VRP read that makes front-week naked premium a trap, close enough in to stay inside the Elevated / Watchful half-life of 15 sessions. Wings pin to 711.00 above and 700.00 below - the structural dealer anchors do the work.

Deploy the condor, skip the directional spread, and stretch DTE - VVIX break is the only trigger that flips the sizing verdict.

What it means for your trading

Iron condor at 41 dominates the put spread at 29 because contango carry and Normal VVIX stack the payoff; park it in the 30-45 DTE window and size Standard Size.

Actionable Summary

Playbook: deploy Iron Condor structures in the 30-45 DTE window where the carry actually pays. Fade SPY strength into the 711.00 call wall and buy dips toward the gamma flip at 684.22 - dealers long gamma do the heavy lifting on any weakness while spot holds above the flip.

Avoid short front-week naked vol: VRP prints -2.3%, meaning the edge lives out the curve, not at the front. Watch VVIX at 98.75 - a break higher is the single trigger that flips the latent vanna risk (net VEX -$237.4B) from dormant to active, forcing dealer delta-selling into weakness.

Pivot markers: charm level 711 frames the expiry drift, and the Elevated / Watchful regime backdrop with half-life of 15 sessions gives the carry trade room to run before mean-reversion risk dominates.

What it means for your trading

Iron condors in the 30-45 DTE window are the cleanest expression of a Positive Gamma tape with steep contango and contained VVIX. The only trade-killer is a VVIX break - until then, fade the call wall, buy the flip, and harvest carry.

Airline fuel-cost shock plus a headline-grabbing bailout keeps energy and transport under pressure even as index vol stays compressed - watch for sector rotation if crude catches a bid.

Ceasefire extension plus solid earnings explains the risk-on bid into the close and supports the positive-gamma tape - the single cleanest regime-confirming headline on the tape.

Iran war cost pass-through into input prices is the stagflation risk lurking under the vol-suppression rally - a slow-burn headline, not a tape-mover today but the reason tail hedges still matter.

Hormuz ship seizure is the kind of tail-event headline that would normally bid MOVE and crack skew - the fact that it isn't tells you how anesthetized the tape is to geopolitical drip.

Hormuz traffic still depressed signals the supply-chain tail is not resolved, even if ceasefire headlines are doing the heavy lifting for risk appetite.

Ceasefire uncertainty bleeding into FX and equity while focus shifts to central bank decisions is the setup where the positive-gamma tape is most vulnerable - single-catalyst risk.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.91 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 684.22 against a spot of 710.53. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 15.79% with a volatility risk premium of -2.3%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.74. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime