Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY closed at 706.60, sitting just below the gamma flip at 707.14 - dealers are short gamma, regime is Negative Gamma, and moves get amplified from here. The structural map: call wall 710.00, put wall 700.00, max pain 689.00 - a thin band where any breach of the put wall opens an air pocket toward max pain. Net DEX at $74.88B with vanna -$186.92B means a vol spike will force dealers to sell delta, accelerating downside. VIX bid to 20.29 (+7.53%%), VVIX to 102.02, but term structure holds Contango with VIX3M at 22.03 - fear is real but bounded, no event premium pricing in. VRP at -1.47% says options are cheap to recent realized - short premium has poor edge here. QQQ at 646.89 holds positive gamma above its flip 644.62 - the divergence is the day's lead, IWM at 275.87 echoes SPY's fragility. Bottom line: defend below the flip, fade rallies into 710.00, and prefer 30-45 DTE iron condors over naked premium given the short-gamma backdrop.

Negative gamma in SPY/IWM with QQQ holding positive - divergence is the lead, vol bid into close

SPY closed at 706.60, just below its gamma flip at 707.14, flipping dealers short gamma into a destabilizing zone while QQQ remains in positive gamma - a clean cross-asset divergence. VIX popped to 20.29 with VVIX at 102.02, but term structure stays in contango and VRP is negative, telling you the bid is reactive, not panic. Iron condors in the 30-45 DTE window remain the highest-EV structure, sized standard given normal vol-of-vol.

Regime Assessment

Regime prints Elevated / Watchful with VIX parked at 20.29 - the zone where transition probabilities cut both ways and neither tail dominates. The model assigns 0.15 to an escalation into panic over the next week and 0.45 to mean-reversion back to low-vol over two weeks. Read that asymmetry literally: the base case is drift-lower, not break-higher, but the panic tail is fat enough to demand hedges.

Half-life sits near 15 sessions, so this footing sticks absent a fresh catalyst - don't chase a regime shift off a single bad close. Positioning should respect persistence: size for the modal path, carry tail protection for the minority one. The trigger that flips the probability mix is 700.00 - a clean breach of SPY's put wall converts the elevated label into something hotter and pulls the panic-transition weight forward.

What it means for your trading

Elevated/watchful at VIX 20.29 with a two-week half-life - the regime is sticky, mean-reversion is the base case at 0.45, and 700.00 is the level that re-prices the panic tail.

Trading readVIX, VVIX, and SKEW all pop in sync while MOVE stays muted - confirms equity-localized stress, not credit/rates contagion; mean-reversion within the equity complex still favored.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

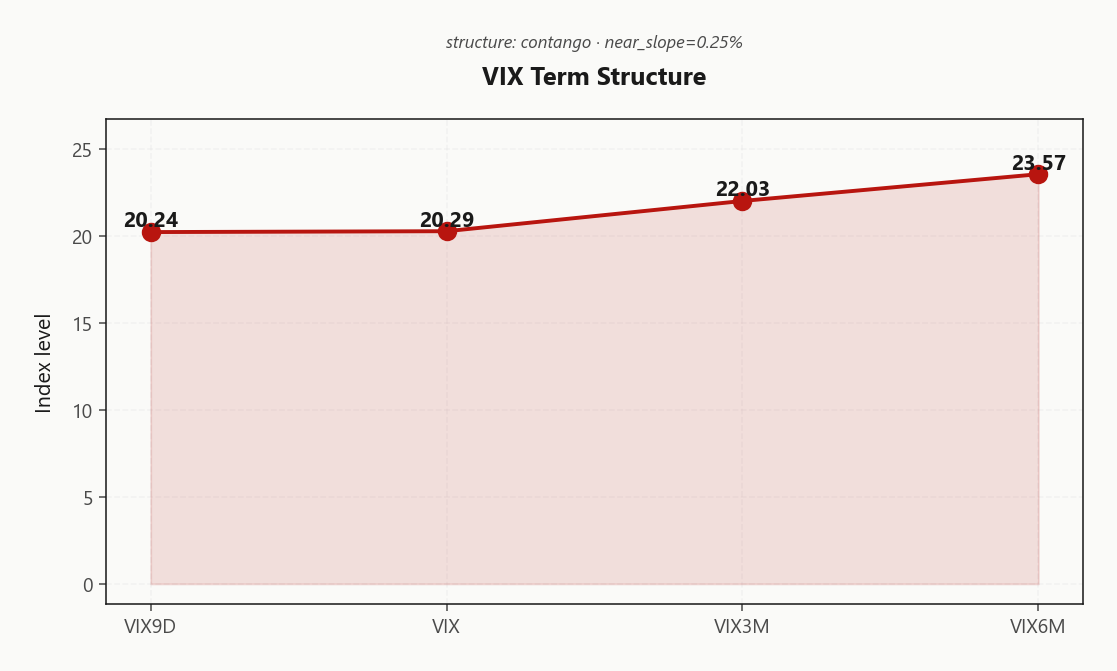

Curve prints Contango with VIX9D at 20.24 nearly co-located with spot VIX 20.29, while VIX3M holds 22.03 and VIX6M stacks to 23.57. The short-end bid is reactive to today's spot-vol stress, but the back-end premium signals no event panic - term carry remains Contango - structural carry available.

Forward 30-to-60 at 22.8503676119 sits richer than spot, and forward 60-to-90 extends to 25.0153732732 - calendar sellers get paid in the belly without taking binary event-premium risk. The cleanest geometry is the 14-to-30 day window; 0-to-7 DTE is muddied by the vol pop and hostile vanna/charm.

Roll-down edge persists but has compressed versus a week ago. Short-vol carry trades remain viable while structure holds Contango - watch VIX9D crossing VIX3M as the trigger that kills the trade.

What it means for your trading

Curve holds Contango - structural carry available with the belly richer than spot - calendar sellers in the 14-30 day window retain edge, but avoid 0-7 DTE where the front-end bid is pure reactive demand.

SPY's VRP prints -1.47% with HV20 at 18.14 running hot against ATM IV of 16.67% - realized is eating implied, and short premium has no edge here. HV60 at 15.28 confirms the recent pickup isn't a one-day artifact; it's a step-change the vol surface hasn't repriced. Vol sellers in SPY are handing over convexity at a discount.

IWM is the lone bright spot at 3.27% VRP - the only clean premium-sale real estate across the complex, and the name where short-wing structures still carry. QQQ sits at -0.74%, functionally neutral, neither a gift nor a trap.

Playbook: long gamma in SPY is the under-owned side, IWM is the lone condor candidate, and QQQ is a coin-flip on premium. Stop shorting SPY vol until realized cools.

What it means for your trading

SPY VRP at -1.47% means options are cheap to realized - long gamma is the underpriced trade and short premium should be redirected to IWM where VRP prints 3.27%.

Skew Convexity

Quarter-delta put skew is steepening across the complex with IWM at 6.59% leading the chase, SPY mid-pack at 3.76%, and QQQ tracking at 4.88%. Smile ratio at 1.23% confirms dealer flow pricing asymmetric left-tail risk - downside is being bid in an ordered way, not a panic bid.

The SPY wing map tells the story: put-25d IV at 20.49% sits well above ATM at 18.14%, while call-25d at 16.73% trades through the body - a textbook left-tail bid with zero upside conviction. IWM's outsized skew reading is small-cap downside being chased into a negative-gamma regime; the beta echo into Negative Gamma SPY is consistent, not divergent.

Trade implication: flat call skew hands you a clean financing leg - sell upside calls into the call wall at 710.00 to fund downside protection rather than paying full freight for puts. The geometry favors risk-reversals and condors that lean on cheap call sales, not naked premium into a steepening wing.

What it means for your trading

Skew is steepening in an ordered, left-tail-bid fashion - IWM at 6.59% leads, SPY smile ratio 1.23% confirms asymmetric pricing without panic. Flat call wing means selling upside to finance downside is the highest-edge overlay here.

Vol-of-Vol Structure

VVIX prints 102.02 against a VIX at 20.29, pinning the ratio at 5.03 - squarely in the Normal band. The vol pop is tracking spot-vol, not exceeding it, which means today's bid is mechanical hedging, not a repricing of jump risk.

Translation for the book: sizing stays at Standard Size. No need to half the strangles, no need to defensively monetize carry. The vol-of-vol surface is not yet telling you a binary regime is loading, even with SPY bias stamped Destabilizing below the flip.

The line in the sand is VVIX above the one-thirty handle - that is where dealer gamma-of-gamma hedging turns reflexive and forces us to cut size in half. Until then, run the standard strangle and iron-condor footprint the scenario grid recommends; the vol-of-vol green light is doing real work under a red charm pivot.

What it means for your trading

Vol-of-vol sits in the Normal zone with the VVIX/VIX ratio at 5.03, so Standard Size applies - trim only if VVIX breaks a fresh high.

Dispersion Spread

Index ATM IV sits elevated across the complex - SPY at 16.67%, QQQ at 21.55%, IWM at 25.32% - while single-name GEX shifts run large and one-directional. The top-five movers led by NVDA all print Positive resets, with MSFT, META, AMZN, and AAPL rounding out the mega-cap stack. Component vol is doing the work; index vol is the shell absorbing it.

That split is the trade. SPY ATM anchors the basket while individual names churn underneath - classic dispersion geometry where index premium decays faster than the sum of its parts. Sell the index, leave the names alone. Iron condors on SPY capture mean-reversion premium that single-name dispersion structurally cannot, because the component noise cancels into the benchmark while their vol stays bid.

With QQQ holding Positive Gamma and SPY flipped to Negative Gamma, prefer index condors over single-name strangles into the 30-45 DTE window.

What it means for your trading

Single-name GEX is resetting hot while index ATM IV at 16.67% absorbs the shock - sell index vol, not component vol, and let the Iron Condor harvest the dispersion spread.

Liquidity & Microstructure

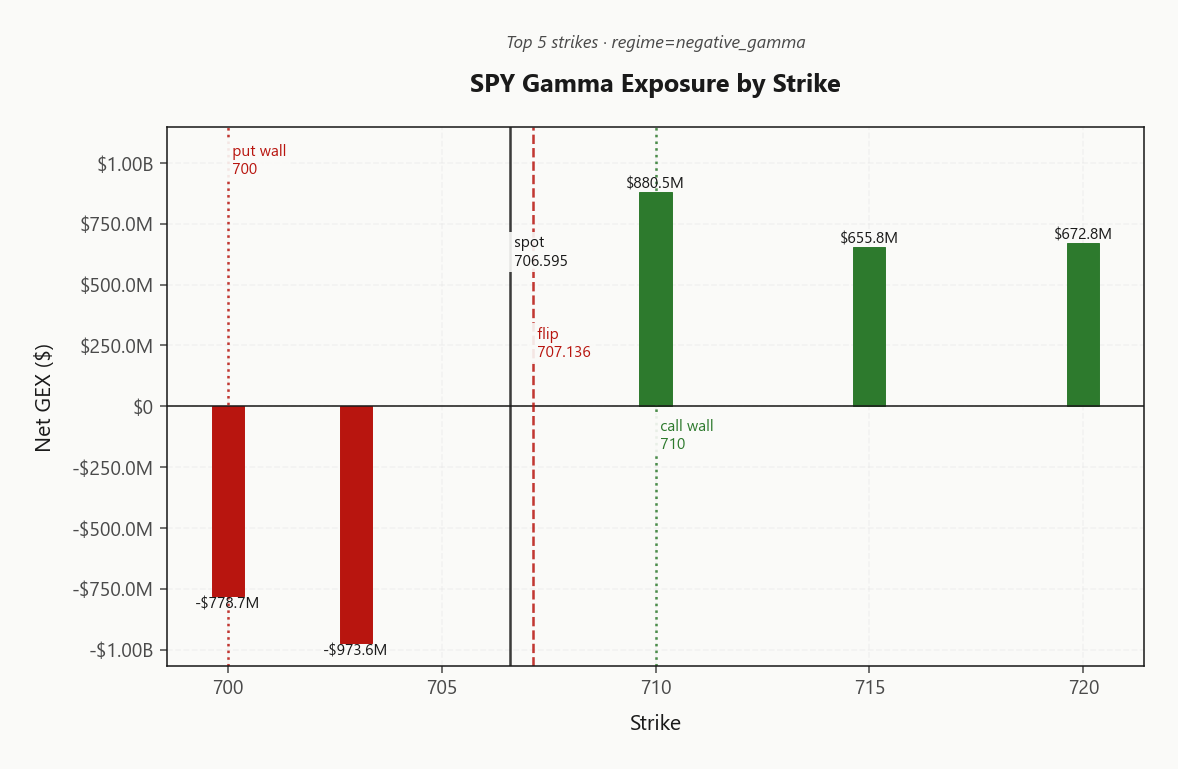

SPY's OI map is sandwiched: top strikes cluster at the call wall 710.00, the put wall 700.00, and a heavy cash-magnet strike at 703.00 bracketing the gamma flip 707.14. That triad defines the day's playable range - dealers sell into strength above the flip and lean against the call wall, while the put wall is the tape's last structural bid.

Below 700.00, the book thins sharply toward max pain at 689.00 - an air pocket where liquidity is sparse and any breach converts the band into a slide channel. The swing pivot sits at the top-strike net GEX print of -$973.6M at 703.00; it is the fulcrum between dampening and amplification.

The highest OI strike at 600 sits far below spot - legacy positioning, not an active magnet. Trade the current band: fade rallies into the call wall, defend the put wall, and treat any clean breach of 700.00 as the trigger to flip defensive.

What it means for your trading

OI is sandwiched between 710.00 and 700.00 around the gamma flip, with a thin void beneath toward 689.00. Breach of the put wall is the single microstructure trigger that flips today's playbook from mean-reversion to directional defense.

Trading readDealers dampen between the call wall and put wall but flip to amplifiers below - any close beneath the put wall converts the band into a slide channel toward max pain.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$186.92B - vanna is the accelerant, not a cushion. A vol spike from here mechanically forces dealers to sell delta, and with spot sitting below the gamma flip at 707.13592584, every hedging reflex compounds downside rather than dampens it. Charm exposure runs -$245.6M into the bell, layering passive selling on top of the vanna impulse as theta decay drags dealer deltas lower.

The pivot type is the Gamma Flip itself - current bias reads Destabilizing, signal Red. There is no secondary level to lean on; reclaim the flip and flow re-stabilizes, stay below it and hedges chase the tape. Size downside protection larger than a symmetric-gamma regime would warrant.

QQQ vanna is negative too, but with spot above its flip at 644.62 the positive-gamma cushion absorbs the vanna kick - the divergence reads Qqq Heavier. Trade the split: lean short SPY vol hedges against long QQQ gamma until the flip is reclaimed.

What it means for your trading

With net VEX at -$186.92B and charm at -$245.6M both pressing the same way below the Gamma Flip, the current bias is Destabilizing - size hedges for acceleration, not mean reversion, until spot reclaims 707.13592584.

Cross-Asset Confirmation

Cross-asset tape says this is localized equity stress, not systemic. MOVE sits at 67.90 - rates vol quiet, credit not transmitting - while Fear & Greed holds Greed at 68, telling you sentiment hasn't been wrung out. The mean-reversion playbook still applies; this is an Iran/Fed-chair headline event, not a credit shock.

The regime split is the lead: QQQ at 646.89 holds positive gamma above its flip while SPY and IWM sit below theirs - divergence direction reads Qqq Heavier, leadership rotation, not full risk-off. IWM at 275.87 echoing SPY weakness is beta confirmation, not independent fragility - but it's the canary. Watch IWM's put wall first; a break there is the signal that divergence collapses into synchronized downside and the mega-cap tech floor finally gives.

What it means for your trading

MOVE quiet and F&G still in Greed confirm equity-localized stress with QQQ at 646.89 still anchoring - trade the divergence, but IWM tracking SPY lower is the setup that flips this from rotation into risk-off.

Scenario EV

The EV grid lands on Iron Condor as the highest-scoring structure at 25, clearing the put-spread alternative at 15. The geometry justifies it: term structure in Contango supplies carry, vol-of-vol sits Normal at a VVIX/VIX ratio of 5.03, and steep put skew (3.76%) lets the call-spread wing finance the put-spread wing without overpaying either tail.

The sweet spot is 30-45 DTE - past today's vol pop where vanna and charm are most hostile, but before back-month theta dies. Avoid the 0-7 DTE bucket entirely; with net VEX at -$186.92B and the flip acting as a Destabilizing pivot, short-dated naked premium is the worst-EV trade on the board.

Sizing: Standard Size. The put-spread is the fallback if you want directional bias into a breach of 700.00, but the condor captures the mean-reversion premium the dispersion regime won't.

What it means for your trading

Iron condor in the 30-45 DTE window is the highest-EV structure - contango carry, normal vol-of-vol, and steep skew all align, while short-dated vanna hostility disqualifies 0-7 DTE premium sales.

Actionable Summary

Bottom line: defend the gamma flip at 707.14, fade rallies into the 710.00 call wall, and let the Iron Condor in the 30-45 DTE window carry the book at standard size. The put wall at 700.00 is the decision point - hold it and mean-reversion plays; breach it and an air pocket opens toward max pain at 689.00, flipping the playbook defensive.

Avoid naked short strangles in the front-week where vanna and charm are most hostile - Destabilizing flow below the flip means any vol pop forces dealers to sell delta into weakness. Pivot to long premium if VVIX prints a fresh high or QQQ loses its own flip at 644.62.

Trade the divergence directly: long QQQ versus short SPY captures the Qqq Heavier regime split while the complex sits in a Elevated / Watchful tape.

What it means for your trading

Iron condors at 30-45 DTE are the highest-EV structure while SPY defends 700.00; a breach reroutes toward 689.00 and flips the book to long premium and outright defensive posture.

Warsh confirmation chatter is the rates-narrative pivot - Fed-chair uncertainty drives the back-end of the VIX curve and explains why VIX3M holds premium even as spot-vol bounces.

Iran tensions weighing on European sentiment is the macro-overhang explanation for today's SPY weakness - geopolitical risk justifies the put-skew steepening across indices.

Hormuz shipping halt is the energy-supply tail risk that keeps vol bid into the close - this is the kind of headline that reprices the back of the VIX curve in a single session.

Trump's surprise at market resilience captures the cognitive dissonance - a destabilizing flip-zone close juxtaposed with greed sentiment is exactly the setup that breeds reflexive vol pops.

German investor morale at a three-year low confirms global risk-off undercurrents - when European sentiment cracks first, US indices typically catch the second wave.

"Tech overwhelms Iran tension" headline matches the QQQ-positive-gamma vs SPY-negative-gamma split exactly - single best framing of today's dispersion.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 19.49 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 707.14 against a spot of 706.60. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 16.67% with a volatility risk premium of -1.47%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 20.29. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime