Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

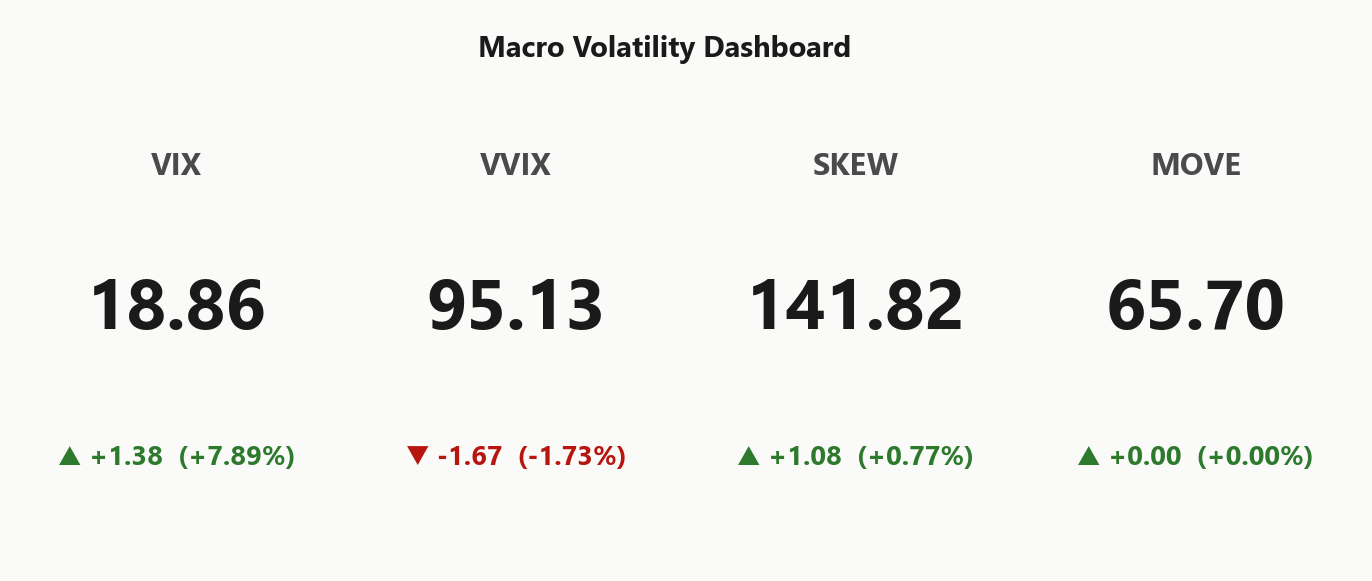

SPY trades at 708.80 with net GEX at $1.76B - dealers long gamma, moves dampened, mean reversion favored. Call wall 710.00 overlaps put wall 710.00 creating a magnet; gamma flip sits at 699.01, spot cushion ~N/A above. Dealer bias neutral via Neutral, but QQQ has already broken below its flip to Negative Gamma - divergence Spy Heavier is the tape's split personality. VIX at 18.92 popped 7.89%% on Iran headlines but term structure stays Contango - no panic priced. VVIX at 95.13 is Normal, standard sizing appropriate. VRP sits -3.05% - options cheap to realized - meaning short-vol harvest is marginal; scored winner is Iron Condor at 30-45 DTE. Bottom line: fade strength into the 710.00 wall on SPY, but don't assume QQQ follows - negative gamma trend there until it reclaims its flip.

SPY positive gamma at Positive Gamma but QQQ flipped negative - divergence is today's tape

SPY sits above 699.01 with dealers long gamma, while QQQ drops below its flip into negative territory - tech will trend, index will mean-revert. VIX at 18.92 in steep contango says no panic, but 7.89%% VIX pop on Iran headlines warrants tail respect. VRP active across the complex, iron condor the scored winner for 30-45 DTE.

Regime Assessment

Current state reads Elevated / Watchful with VIX parked at 18.86 - not quiet enough to fade tails, not hot enough to chase them. Transition probability into panic over the next week sits low at 0.05, while the decay path to a low-vol regime over ten sessions carries meaningfully higher weight at 0.45. The asymmetry favors mean reversion lower, not breakout higher.

Regime half-life of 15 sessions implies this watchful state sticks roughly three weeks absent a fresh headline shock. That is a chop window, not an explosion window - plan accordingly. Iran tape adds headline jump risk without altering the base rate.

Translation: position for stickiness. Premium-selling structures with defined wings carry the regime; outright long-vol is paying rent against a decay drift. Respect the tail, do not buy it at these levels.

What it means for your trading

Regime is Elevated / Watchful at VIX 18.86 - panic probability low, decay probability higher, half-life 15 sessions. Trade the chop, respect the tail, do not pay up for it.

Trading readVIX up, VVIX down, SKEW steady, MOVE flat - classic isolated equity event signature, not systemic. Divergences confirm geopolitical not macro regime shift.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

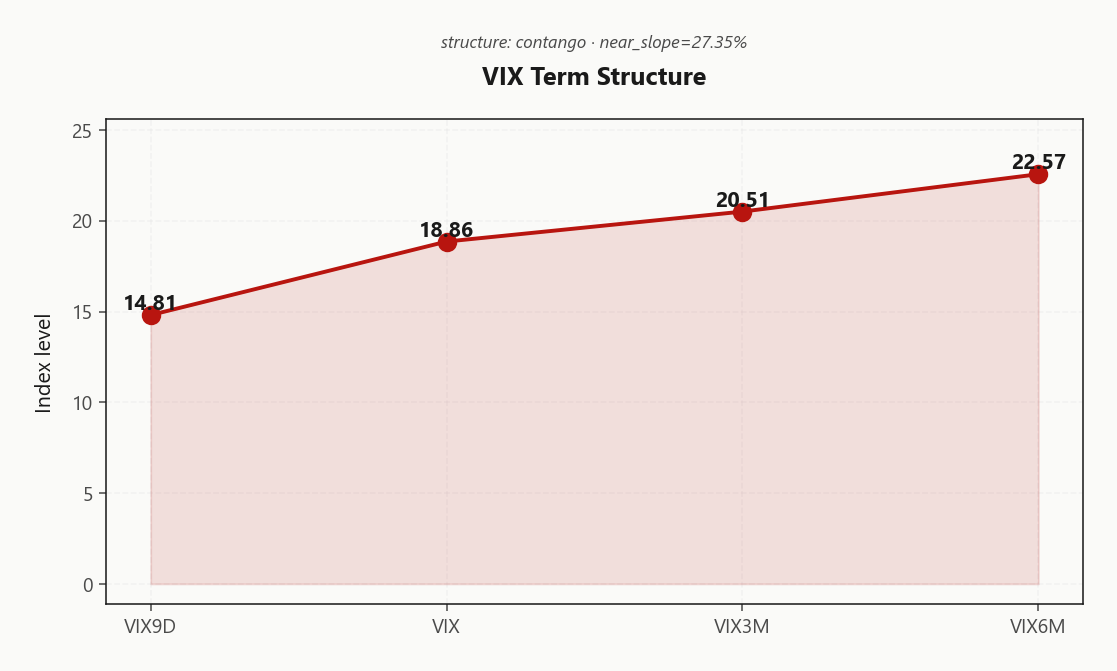

Term structure holds Contango from the front through the belly, with 14.81 printing below spot 18.86 and 20.51 stacked above - the two-week window is pricing calm even as headlines rattle. No systemic stress embedded; structural carry is the dominant signal, and the Contango regime grades Contango - structural carry available.

The tell is slope geometry. Front-to-belly steepness - 18.86 pushing toward 20.51 while 14.81 stays suppressed - flags localized event premium, not a regime shift. Iran tape is driving the near slope; credit and rates refuse to confirm. Fade the front, own the belly.

Best edge sits in 30-45 DTE short vol: far enough to clear 0DTE noise, close enough to harvest the steepest roll-down before vega exposure turns punitive if the front extends.

What it means for your trading

Forward vol geometry is Contango with 14.81 under 18.86 - carry is live, stress is not priced. Deploy short vol in the 30-45 DTE window where slope monetization is cleanest.

Trading readSteep contango from VIX9D through VIX6M says vol carry is available and market expects today's headline stress to fade. Front-end spike is reactive not anticipatory.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 14.84% prints well under RV20 at 17.89, pushing VRP to -3.05% - options are cheap to what the tape actually delivered. That is an unusual read for a gamma-long index and flags the spread as Danger Zone: recent realized outran what forward vol is charging.

Note the split inside realized - RV5 at 9.81 has cooled well below the trailing twenty-day, so the underpricing is a lag, not an active repricing. Dealers aren't overpaying for protection, which means short-strangle carry is underfunded relative to the realized envelope.

Skew premium to ATM keeps put spreads the efficient downside vehicle, but the core implication is structural: calendars and long-gamma legs - selling the underpriced front, owning convexity - carry more edge than pure short vol. Harvest the contango roll, not the ATM.

What it means for your trading

Negative VRP with ATM IV beneath RV20 makes this a Danger Zone tape for naked short premium; prefer calendars and long-gamma structures over strangles until IV repays the realized gap.

Skew Convexity

Quarter-delta put IV prints at 20.02% against an ATM reference of 17.45%, with the call wing flattening to 16.36%. The resulting skew of 3.66% and smile ratio of 1.22% describe ordered downside bid, not panic steepening - hedgers are paying up for puts in measured size while the upside wing confirms no FOMO into the 710.00 ceiling.

With the tail absent and the call skew inverted, naked put ownership is the wrong instrument - you overpay the belly without catching a convexity kicker. Put spreads finance the quarter-delta bid by selling the flat-to-cheap further-out strikes, netting a far superior cost-per-unit-delta into any break of 699.01.

Read-through: skew is Skew Steep but not disorderly - consistent with a Positive Gamma tape absorbing Iran headline premium without reaching for tail insurance.

What it means for your trading

Put-side bid at 20.02% vs ATM 17.45% is ordered, not panicked; flat call wing rules out upside chase. Express downside via put spreads, not naked tails.

Vol-of-Vol Structure

VVIX prints 95.13 against spot VIX at 18.86, leaving the ratio in Normal territory. Vol-of-vol is not bid - the market is not paying up for a bimodal outcome, and jump premium inside vol options themselves is absent despite Iran headlines reigniting the front VIX.

That calibration validates Standard Size on the scored Iron Condor at 30-45 DTE. No need to haircut notional for convexity-of-convexity risk here; the tape is pricing directional chop, not a regime break.

Early warning remains a VVIX push through the triple-digit zone - that is the flag to pull in size, lift tails, and respect the Call Wall pivot. Until then, carry the structure.

Index vol sits moderate with SPY ATM printing 14.84% while cross-strike dispersion runs 79.27 against cross-expiry at 1.85 - the skew is doing the work the term structure isn't. Single-name GEX churn tells the real story: NVDA leads the positioning shift, with AAPL and MSFT stacking behind it. Idiosyncratic risk is concentrated, and the index hedge isn't absorbing it.

That makes the classic dispersion trade - long single-name vol, short index - marginal here rather than structural. With SPY in Positive Gamma and QQQ already flipped to Negative Gamma, index short-vol carries cleaner edge than chasing correlation unwind through names where NVDA/AAPL weight is outsized. Concentration cuts both ways: a single mega-cap reversal can whip the basket faster than index vol responds.

Prefer SPY/SPX premium sale over single-name dispersion until the mover list broadens beyond the top cluster.

What it means for your trading

Index IV at 14.84% is moderate while single-name GEX churn is heavy and top-heavy in NVDA/AAPL - dispersion edge is thin, SPY short-vol is the cleaner expression.

Liquidity & Microstructure

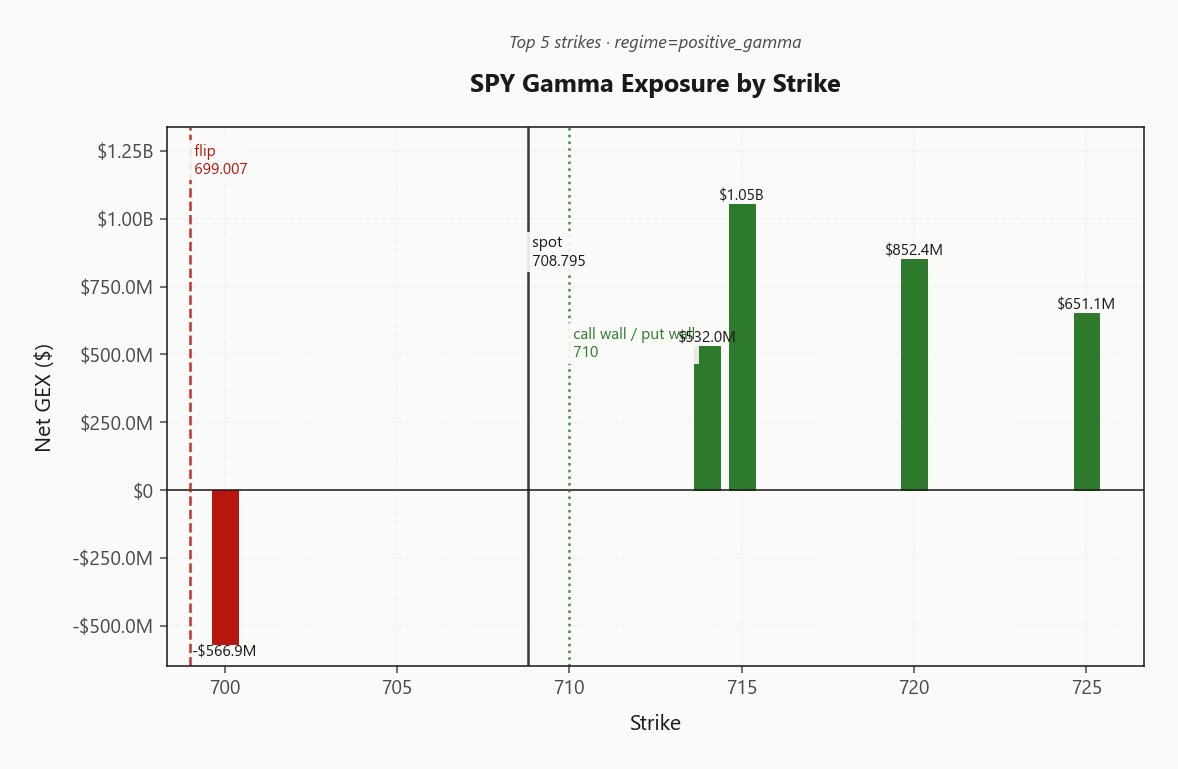

The book reads as a magnet-and-ceiling construct: call wall and put wall collapse onto the same strike at 710.00, a rare alignment that functions as both gravitational pull and hard lid. Spot pins tight to that cluster, with the gamma flip at 699.01 offering only a razor-thin cushion below - a fragile pivot where dealer long-gamma damping flips to amplification on breach.

Beneath the tactical field sits a much heavier anchor: the 600 OI cluster defines the long-term gravitational floor, a reference point dealers cannot unwind quickly. The single largest GEX concentration sits at 715.00 with $1.05B of positioning stacked there, reinforcing the overhead ceiling.

Playbook: fade strength into the 710.00 wall, respect pin behavior while spot holds above flip, and treat a clean break of 699.01 as a regime trigger - dealer hedging inverts and sell-flow stacks on any downside extension.

What it means for your trading

Call/put wall overlap at 710.00 creates a magnet into close while the flip at 699.01 is the single break-level for regime change. Deep OI at 600 defines the longer-horizon gravitational pull.

Trading readCall wall and put wall converging at the same strike creates a powerful magnet - expect spot to gravitate there into close, with dampened swings above flip and amplified selloffs if flip breaks.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$216.81B - deeply negative, meaning vanna is an accelerant, not a brake. Any uptick in implied vol forces dealers to sell delta into the move, so a VIX spike doesn't merely coincide with spot weakness, it manufactures it. The hedge flow runs with the tape, not against it.

Charm layers on top: net CHEX at -$5.8M bleeds decay-driven delta back to the street through the session, skewing dealer reconciliation net-sell into the close. Combined with the VEX posture, the path of least resistance for systematic flow is lower prints as the clock runs down - absent a fresh bid, the cash hours carry an asymmetric downside tilt.

The book pivots on a single level: 710, the call wall overlap. Current bias reads Neutral, but neutrality masks the asymmetry - upside grinds into a vanna-charm headwind, while a break below 699.01 releases the amplifier. Trade the pivot, not the print.

What it means for your trading

Vanna-charm complex is loaded for downside amplification: negative VEX turns a vol pop into a dealer sell-program, and charm bleed skews closing flow net-sell. Pivot is 710 - respect the asymmetry beneath the Neutral label.

Cross-Asset Confirmation

MOVE sits at 65.70 - rates vol isn't flinching - so today's VIX bid is an isolated equity-geopolitical event, not a compound credit-and-equity unwind. The bond market is telling you this is a headline tape, not a regime break. That matters for sizing: cross-asset stress signatures are absent, so vol spikes here are fade material, not chase material.

Fear & Greed reads Greed at 68 - complacency tilt into a live Iran escalation path, which is the textbook asymmetric downside setup. QQQ at 646.90 already broke its flip while IWM at 275.50 and SPY hold positive gamma - regime divergence is Spy Heavier, tech is the fragile node.

Play the isolation: fade VIX pops, respect the tail. Iran headlines move oil and equity vol, not credit - so premium-selling edge holds in SPY/IWM while QQQ stays off the short-vol menu until it reclaims flip.

What it means for your trading

MOVE steady at 65.70 with F&G at Greed = isolated geopolitical event masked by complacency - fade VIX pops in SPY/IWM, avoid QQQ short-vol until it reclaims its flip.

Scenario EV

The scorecard lands on Iron Condor at a best score of 50, edging the put spread alternative. The edge is structural: Contango through the curve pays roll-down, Normal VVIX keeps wing convexity affordable, and the call/put wall overlap at 710.00 builds a genuine pin magnet around spot.

Optimal window is 30-45 DTE - far enough out to dodge the 0DTE negative-gamma chop that has been dictating intraday tape, close enough to avoid eating a vega shock if Iran headlines push VIX from 18.86 toward the next handle. Shorter tenors get whipsawed below flip; longer tenors carry unhedged vega into an Elevated / Watchful regime.

Size standard - VVIX at 95.13 is not pricing a bimodal outcome, and Standard Size is the read. Anchor the short call around 710.00, short put under 710.00, and treat a break of 699.01 as the kill-switch.

What it means for your trading

Iron condor wins on carry plus pin dynamics at 30-45 DTE; standard sizing appropriate while VVIX sits Normal, but cut risk on any break of 699.01.

Actionable Summary

SPY holds Positive Gamma above 699.01, but QQQ has already slipped into Negative Gamma - the tape's split personality is the trade. Dealer bias sits Neutral at the 710 pivot where call wall overlaps put wall, creating a magnet into close. VIX popped 7.89% on Iran headlines but term structure stays Contango and VVIX at 95.13 reads Normal - no panic priced.

TRADE: sell SPY Iron Condor at 30-45 DTE bracketing the 710.00/710.00 cluster, standard size. AVOID short strangles on QQQ below its flip - negative gamma will punish trend moves. HEDGE with long VIX calls; vol-of-vol is Normal, asymmetric insurance is cheap.

WATCH699.01 as the single break-level - a breach flips the regime and mandates risk reduction. Bias neutral with downside tail respect; regime reads Elevated / Watchful and Iran tape is live.

Oil price volatility tied to US-Iran peace hopes is the primary transmission channel for today's equity vol

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.92 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Spy Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 699.01 against a spot of 708.80. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.84% with a volatility risk premium of -3.05%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.86. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime