Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

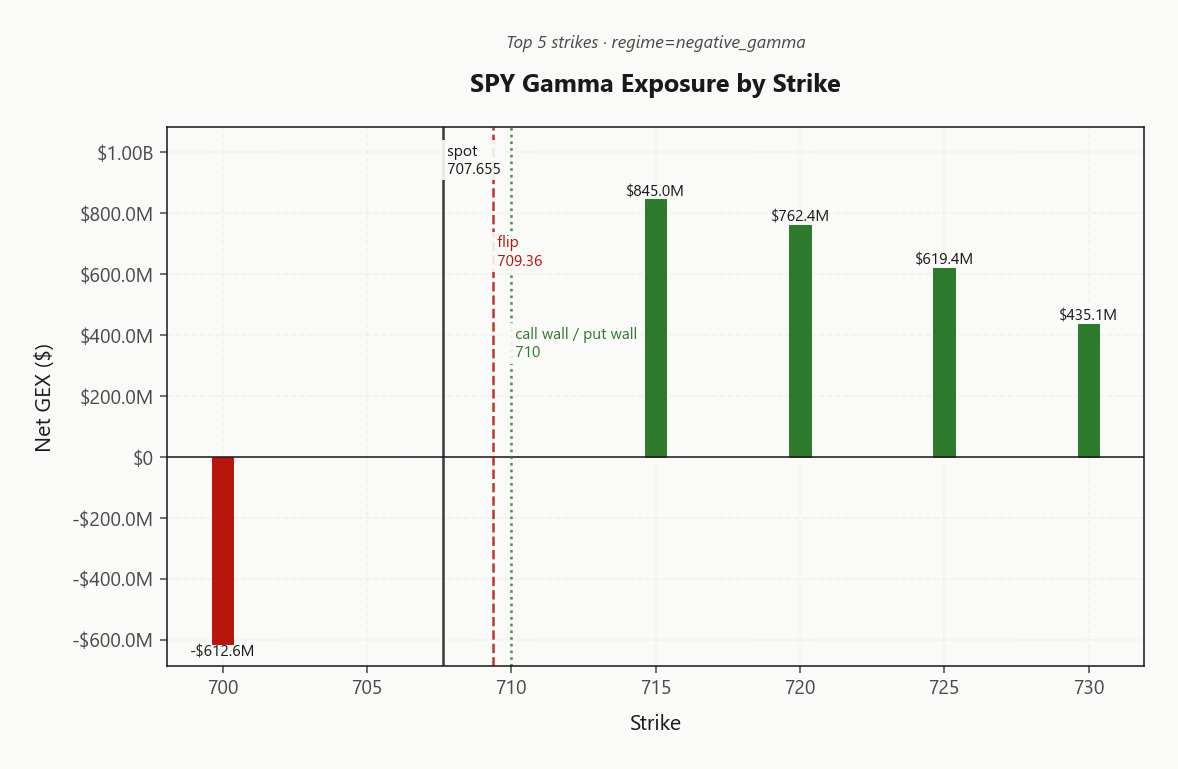

SPY prints 707.66 sitting just under the gamma flip at 709.36 - net GEX of $220.4M flips the regime to Negative Gamma, meaning dealer hedging amplifies rather than dampens moves. Call wall and put wall collapse together at 710.00, with max pain down at 687.00 and the highest OI cluster all the way at 600. Dealer flow is hostile: Time decay pushing dealers to sell - pressure into close and vanna adds fuel if vol extends - Destabilizing bias with pivot at 709.3596009895. VIX at 19.23 popped 10.01%% on Iran/Hormuz headlines but term structure holds Contango - VIX9D 18.46 / VIX 19.23 / 3M 21.30 - and VRP reads -3.07% so front-week IV is cheap versus 20d realized 17.97. QQQ at 645.08 and IWM at 276.51 remain in Positive Gamma - index complex is diverged, SPY the weak link. Bottom line: Iron Condor in 30-45 DTE is the edge; avoid SPY 0DTE directional bets through the flip, and any reclaim of 709.36 flips dealer flow supportive.

SPY pinned below flip in negative gamma while QQQ/IWM hold positive - index complex diverged

SPY sits just beneath its gamma flip at 709.36, putting dealers short gamma into a jittery tape while QQQ and IWM retain positive-gamma cushions. VIX term structure remains in contango at Contango with VVIX at 98.98, yet 25d put skew of 3.47% shows the left tail being bid on Iran/Hormuz headlines. Edge is in Iron Condor structures in 30-45 DTE - not chasing 0DTE through a destabilizing charm pivot.

Regime Assessment

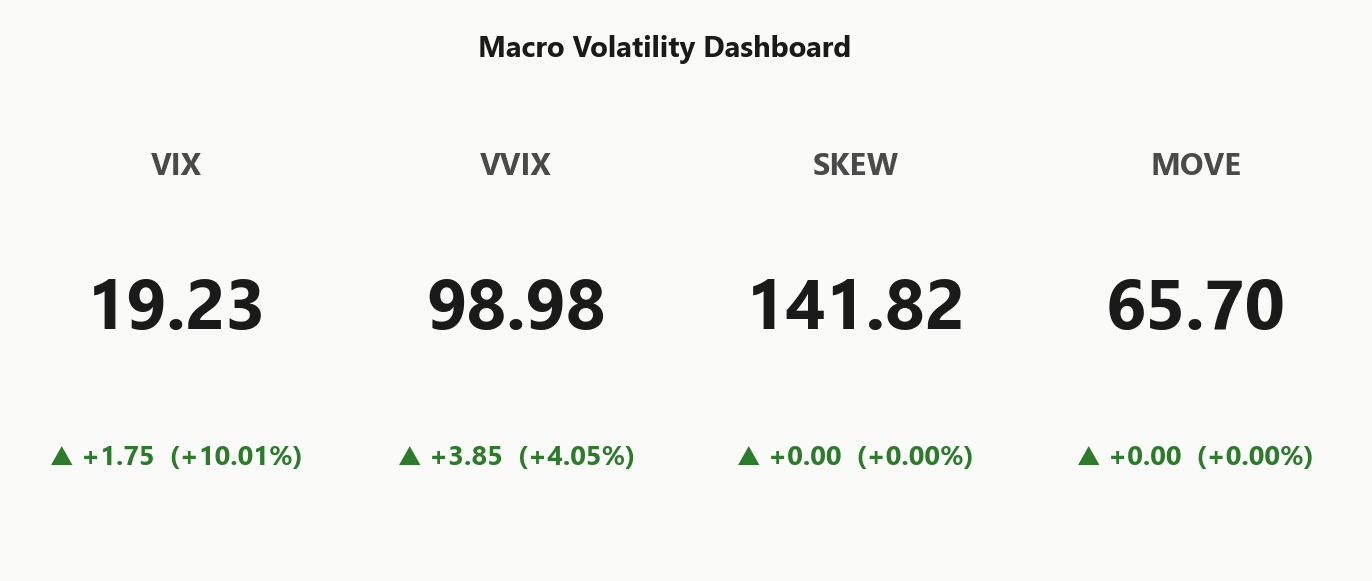

Regime reads Elevated - Elevated / Watchful - with VIX anchored at 19.23. Transition probability to outright panic over the next five sessions sits at 0.05, a low bar that frames today's Iran-driven wobble as positioning noise rather than the start of a vol phase-change.

Mean-reversion odds are more meaningful: probability of decaying back to a low-vol regime within ten sessions prints 0.45, and the half-life on this state runs 15 sessions. Positioning around watchful vol is durable enough to structure around but not permanent - don't marry the hedge.

Actionable read: size Iron Condor in 30-45 DTE to the regime's shelf life; sizing stays Standard Size. Watch for VIX drift back under the low-regime threshold - that's your signal the elevated state is resolving ahead of schedule.

What it means for your trading

Elevated but not extreme - panic transition priced at 0.05 while reversion to low-vol runs 0.45 over ten sessions. Structure trades to the 15-session half-life, not beyond it.

Trading readVIX/VVIX/SKEW moved in line, MOVE didn't - the divergence-that-matters: equity vol repricing without rates stress means this is a contained equity event, not a credit shock.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

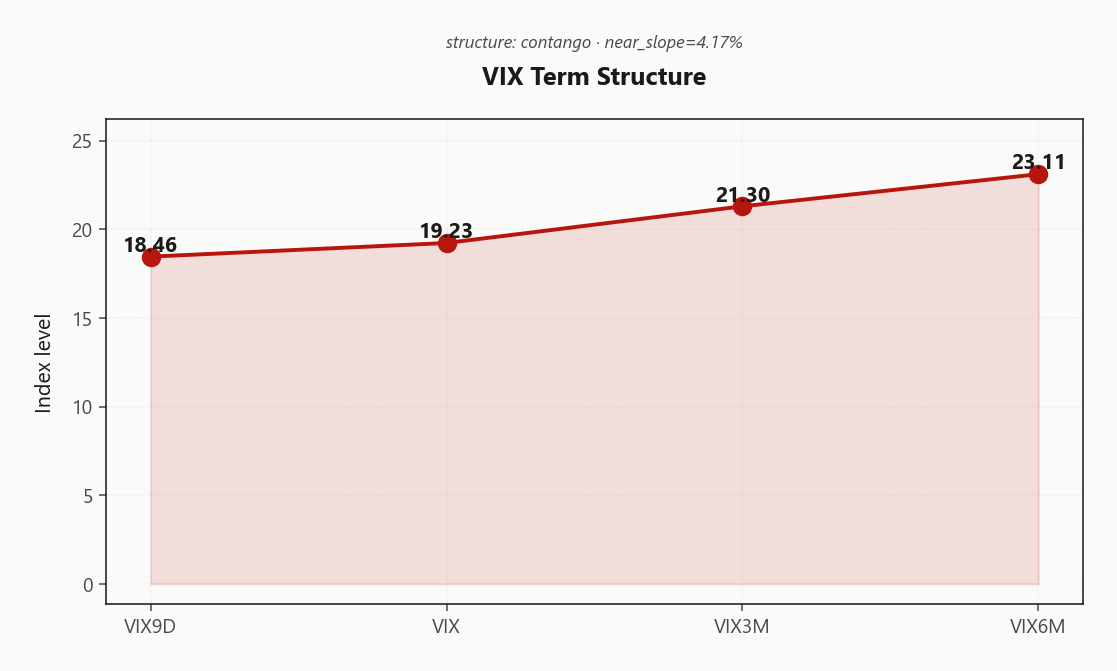

Term structure holds Contango through the headline pop - VIX9D at 18.46 still prints below spot VIX at 19.23, with near slope at 4.17%%. Front lifted less than the tape suggests; carry trade is intact, not broken.

Edge sits in the 30-45 DTE belly where forward vol prices thickest. Size the structural short assuming headline-driven front-end pops; wings non-negotiable on any short vol structure into Hormuz tape.

What it means for your trading

Contango intact at 4.17%% near slope with forward 30→60 at 22.2629411804 - carry favors vol sellers in 30-45 DTE, but wing protection required against headline front-end whips.

Trading readContango intact despite the VIX spike says vol carry trade still alive - front lifted less than the move suggests, and selling forward vol in 30 - 60 DTE has the best risk-adjusted payoff.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 14.9% is trading below 20-day realized of 17.97, leaving VRP at -3.07% - a negative premium that pays gamma buyers, not sellers. HV60 at 15.23 sits beneath HV20, confirming realized is accelerating, not decaying. Front-week options are cheap to what the tape has actually been doing.

The discount is complex-wide: QQQ VRP prints -3.57% and IWM -0.11%, both negative. This is the opposite of a classic short-vol setup - premium sellers are being underpaid across the board while the tape chops on Iran/Hormuz headlines.

Edge: lean long gamma and calendars into headline risk; resist the reflex to fade IV dips with short premium. With SPY short-gamma beneath the flip and realized outpacing implied, the convexity buyer has the cleaner risk-adjusted trade.

What it means for your trading

Negative VRP across SPY/QQQ/IWM with HV60 below HV20 means implied is underpricing an accelerating realized tape - buyers of gamma hold the edge until IV catches up to 17.97.

Skew Convexity

Left tail is getting paid. SPY 25-delta puts mark 17.55% against an ATM of 15.14% while the matching call wing trades through at 14.08% - a skew differential of 3.47% and a smile ratio of 1.25% that confirms puts are being demanded over calls on Iran/Hormuz tail bids.

The shape is elevated but ordered across the complex: QQQ skew prints 3.43% and IWM 2.98% - fear-bid, not panic-bid. VIX skew inverts hard to -91.59% with smile ratio 0.35%, the upside-vol wing paying up as traders hedge a second-derivative spike rather than position for mean reversion.

Convexity is fairly priced, not cheap. Favor put spreads over naked puts - you are paying fair value for downside, so finance the long leg by selling the steep wing. Skip chasing VIX calls outright; the inverted call-wing premium is already in.

What it means for your trading

Left-tail skew is bid but orderly at 3.47% with smile ratio 1.25% - convexity is priced fair, not discounted. Express downside through put spreads, not naked puts; VIX wing at -91.59% already prices the jump.

Vol-of-Vol Structure

VVIX prints 98.98 (up 4.05%%) against a VIX move of 10.01%% to 19.23 - the vol-of-vol bid is not outrunning spot vol. VVIX/VIX ratio sits at 5.15, squarely in the Normal band. No bimodal premium being paid for an Iran/Hormuz binary - the tape is pricing a routine headline wobble, not a jump-risk regime.

Sizing guidance reads Standard Size. That means the jump-risk multiplier isn't flashing and there's no need to haircut notional on vol structures. Edge is in conditioning trades on levels - SPY's flip at 709.36, the wall stack at 710.00 - not on shrinking clip size.

Translation: run Iron Condor in 30-45 DTE at full size. Watch VVIX/VIX expansion as the tell - if the ratio breaks out of Normal, that's when the playbook flips to defensive sizing.

What it means for your trading

VVIX/VIX at 5.15 sitting in the Normal band confirms a clean, contained vol pop - no binary-event premium baked in. Trade the levels at Standard Size; cut size only if the ratio expands.

Dispersion Spread

Index vol is bid but not uniformly - SPY ATM prints 14.9% against QQQ at 18.72% and IWM at 21.9%. IWM is the absolute premium payer, QQQ trades richer than SPY on a mega-cap vol bid, and SPY sits cheapest of the three despite carrying the Negative Gamma regime flag. That ordering matters: the bellwether is the weak leg on price but not the richest on vol.

Iran/Hormuz is a macro catalyst, not a stock-specific one - correlation should rise, which mechanically rewards index vol sellers and punishes single-name dispersion buyers. Defense and energy single-names carry the most event beta into the headline tape; shorting vol there against an index hedge is a trap when the driver is the basket itself.

Trade the complex, not the constituents. Favor SPX/SPY structures where skew is steep enough to fund wings, and avoid short vol on Iran-sensitive single names where idiosyncratic jump risk overwhelms the index carry. IWM pays the most IV but also absorbs the most event beta - size accordingly.

What it means for your trading

Index vol ranks IWM > QQQ > SPY at 21.9% / 18.72% / 14.9%, and with correlation set to rise on a macro catalyst, index short vol beats single-name - especially in Iran-beta energy and defense names.

Liquidity & Microstructure

SPY trades at 707.66 with the gamma flip just overhead at 709.36 - a 0.2408802297% gap that makes this the single most consequential level on the tape. Reclaim it and dealer flow turns supportive; fail it and the Negative Gamma regime keeps amplifying every tick.

The book collapses the call wall and put wall onto one strike at 710.00, turning it into both magnet and battleground into expiry. The dominant GEX cluster sits slightly above at 715.00 carrying net GEX of $845M, reinforcing the pin once spot clears the flip.

Below, the highest open-interest cluster anchors all the way down at 600 - a deep structural floor, not an intraday bid. Expect whippy, headline-driven tape between flip and wall; the supportive dealer bid does not engage until price is back above 709.36.

What it means for your trading

Liquidity geometry is binary around 709.36: reclaim flips dealers to supportive and pins toward the 710.00 wall, failure leaves the tape unanchored until the 600 OI floor.

Trading readWith SPY just under the flip, dealers amplify moves in either direction until spot reclaims 709.36 - above that line the same chart tells you dealers buy dips; below, they feed selling.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

The charm pivot sits at 709.3596009895, roughly 0.2408802297 above spot - current bias Destabilizing. Below it, vanna and charm pull the same direction; reclaim flips dealer flow supportive and collapses the feedback loop. Until then, any VIX pop is an accelerant, not a fade.

Trade the geometry, not the narrative: avoid naked downside in the short-dated tenors where charm bleed is sharpest, size hedges assuming a vol-up move gets monetized by dealer selling, and treat a clean print back above 709.3596009895 as the first genuine risk-on signal.

What it means for your trading

Destabilizing vanna/charm stack with net VEX -$205.07B and charm pivot at 709.3596009895 - dealers amplify downside on any VIX extension until spot reclaims the pivot.

Cross-Asset Confirmation

Cross-asset tape argues this is an equity wobble, not a credit event. MOVE at 65.70 sits inert while VIX repriced - rates vol refuses to confirm the equity spike, and without a bond-vol transmission channel geopolitical shocks like this historically mean-revert inside a handful of sessions. The absence of credit stress is the single most important tell against chasing puts here.

Sentiment corroborates. Fear & Greed prints 69 (Greed) - no panic in the positioning data, just headline-driven repricing at the margin. QQQ at 645.08 and IWM at 276.51 hold their positive-gamma cushions while SPY carries the short-gamma weight alone, leaving the complex Qqq Heavier with SPY the idiosyncratic laggard rather than the leading edge of a broad de-risking.

Trade the divergence: fade the VIX pop while MOVE stays anchored, and treat any reclaim of the SPY flip as confirmation that today's wobble was positioning noise - not the opening move of a structural fear regime.

What it means for your trading

MOVE inert at 65.70 and F&G still in Greed at 69 frame today as an equity/geopolitical wobble - fade the VIX pop, do not chase tail hedges at these skew levels.

Scenario EV

The EV stack lines up on Iron Condor with a best score of 50, clearing the put spread alternative at 38. Negative VRP at -3.07%, standard vol-of-vol with VVIX/VIX at 5.15, and Contango across VIX9D→3M→6M together price the condor as the highest-EV structure - cheap IV against realized, but carry still alive in the back.

Sweet spot is 30-45 DTE, where forward vol 22.2629411804 into 24.7881867025 carries richest. Pick wings outside the collapsed 710.00 call wall and 710.00 put wall; the structural OI floor at 600 gives the downside wing a natural anchor.

VRP reads Unknown - hold sizing at Standard Size, no cut required with vol-of-vol benign. Avoid SPY 0DTE directional through the flip at 709.36; charm is Destabilizing into the close and short-gamma dealers will feed the trigger either way.

What it means for your trading

Edge is in Iron Condor at 30-45 DTE with wings beyond 710.00/710.00, sized at Standard Size. Skip SPY 0DTE directional - short gamma below the flip turns dealer hedging into the accelerant, not the brake.

Actionable Summary

The trade:Iron Condor in 30-45 DTE with wings parked outside the collapsed 710.00 wall and 710.00 floor - negative VRP at -3.07% makes premium selling a carry-not-edge play, so let the structure do the work rather than forcing size. Scenario EV scores 50 against a put spread at 38; the condor wins on geometry.

The watch: SPY reclaim of 709.3596009895 flips dealer flow from Destabilizing to supportive - until then, charm is hostile into the close and Vol up = dealers sell delta - downside amplified if vol spikes adds fuel on any VIX extension from 19.23. Avoid SPY 0DTE directional under the flip, and skip single-name Iran-beta short vol in energy/defense where idiosyncratic tail is mispriced relative to index.

Relative value: index vol over single-name, SPY structures over QQQ given skew economics at 3.47%. Sizing:Standard Size - regime reads Elevated / Watchful, not extreme, so cuts aren't warranted; condition on levels.

Potential de-escalation pathway via Pakistan broker - a headline-driven vol spike like this compresses fast if talks progress, supporting mean-reversion trades.

Gold weak despite geopolitical risk is a tell: dollar bid and real-yield move dominating, means this is an equity wobble not a flight-to-safety regime.

European defence stocks cooling suggests the 'war winners' trade is crowded - rotation risk if ceasefire holds, relevant for any single-name short vol screen.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 19.14 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Qqq Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 709.36 against a spot of 707.66. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.9% with a volatility risk premium of -3.07%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 19.23. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime