Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

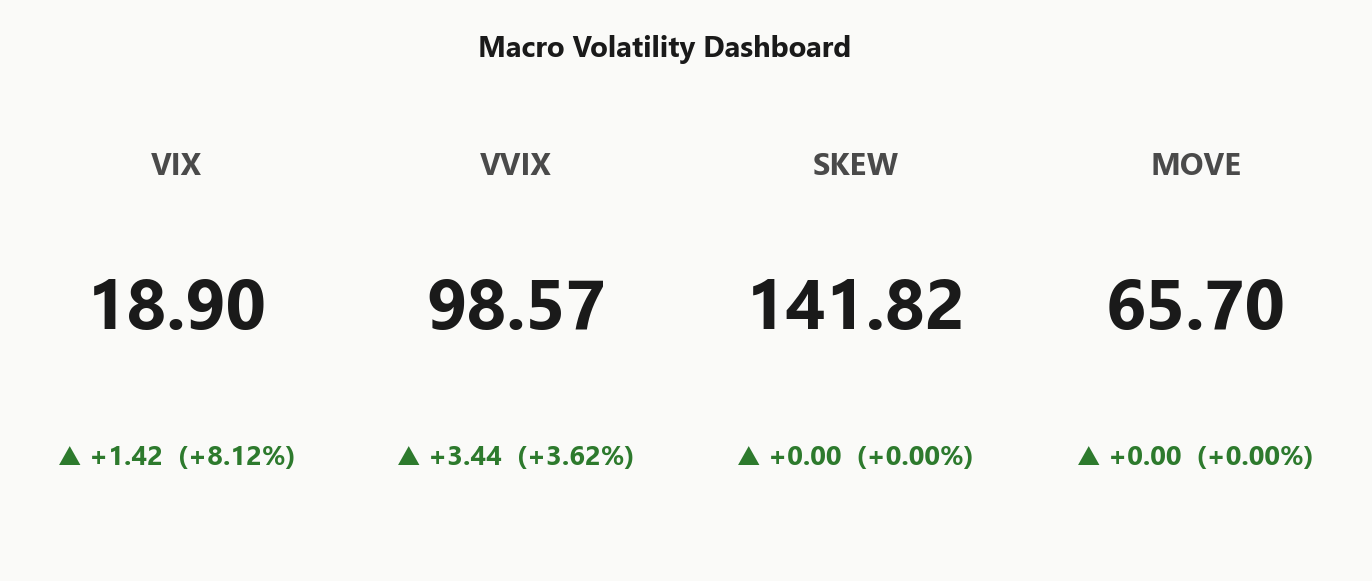

SPY at 708.61 is parked essentially on top of its gamma flip 708.23 with net GEX -$28.6M - technically positive-gamma but the cushion is razor-thin, not a deep mean-reversion regime. Call wall and put wall both stack at 710.00/710.00, max pain sits well below at 687.00, so dealers are pinning the tape near current spot into close. Net VEX -$213.01B and CHEX -$31.3M mean any vol expansion forces dealers to sell delta - the hostile-vanna setup, not supportive. VIX 18.90 (+8.12%%) with term structure in Contango (slope 5.76%%) and VVIX 98.57 - carry is intact, vol-of-vol is normal, no panic bid yet. QQQ has already slipped to Negative Gamma below its flip 649.17, so tech is the fragile leg if Hormuz headlines escalate overnight. Bottom line: harvest the Iron Condor in 30-45 DTE around the SPY 710.00 pin, but keep tech-side hedges on - the cross-asset divergence is the leak.

SPY positive gamma cushion intact above flip; QQQ slipped negative - tech the fragile leg

SPY at 708.61 sits a hair above its gamma flip with dealers still long gamma, while QQQ has rolled into negative-gamma territory below 649.17 - that's the divergence to trade. VIX term structure is in Contango with VVIX at 98.57, so vol sellers keep carry, but Hormuz headlines are the gap-risk that won't show up in the curve. Bias: harvest premium in SPY/IWM walls, treat QQQ as the trend leg if 649.17 fails.

Regime Assessment

Regime reads Elevated / Watchful with VIX parked at 18.90 - not panicked, not complacent, the awkward middle where carry still pays but the tail is unhedged. Transition math says drift-to-low runs 0.45 over ten sessions as the base case, while the jump-to-panic probability sits at 0.05 across five - small, non-zero, and entirely Hormuz-contingent.

Half-life of 15 sessions means the Elevated print is moderately sticky absent a catalyst; with one, the half-life collapses overnight. SPY/QQQ regime divergence (Spy Heavier) is the structural tell that the drift-lower base case is already fraying at the tech leg.

Trade the stickiness, respect the tail: harvest around the SPY pin, keep QQQ downside convexity live, and size for the fact that a 0.05 jump probability is a payer, not a hedge line item.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - sticky enough to fade vol spikes, fragile enough that the 0.05 panic-jump tail deserves real sizing discipline into the Hormuz window.

Trading readVIX up sharply but VVIX up less proportionally and MOVE quiet at 65.70 - divergent signal where equity vol moves but bond vol and vol-of-vol don't confirm; classic geopolitical-shock not credit-shock fingerprint.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

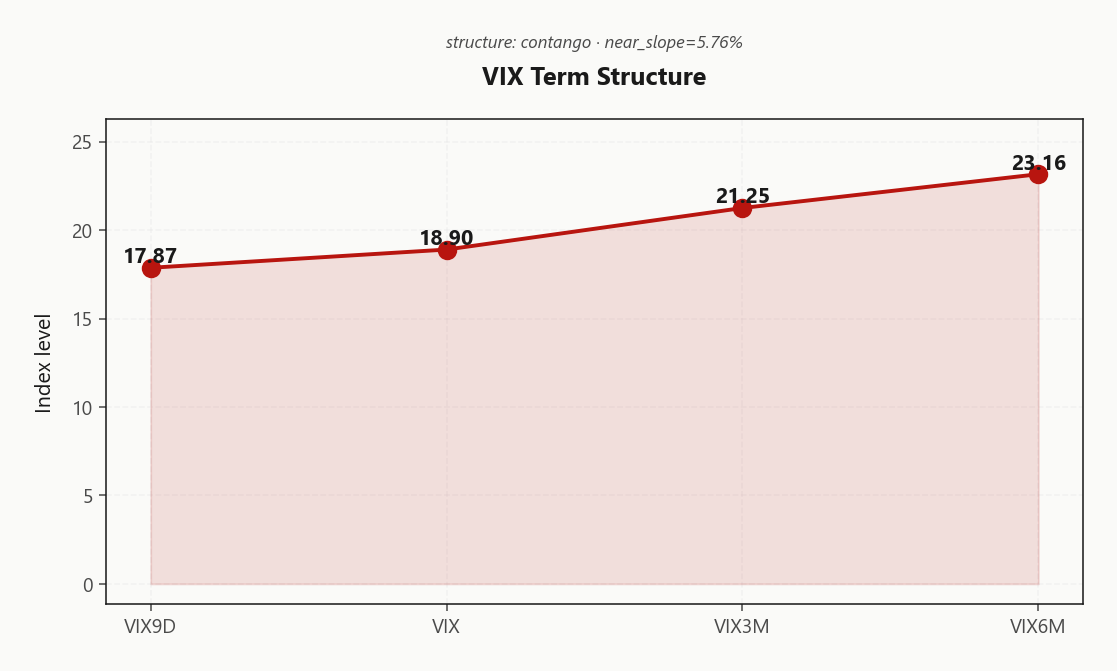

The VIX curve prints textbook Contango across the board - 17.87 under 18.90 under 21.25 under 23.16. That's a paid carry trade for vol sellers, and the Steep Contango regime keeps the structural wind at your back.

But look at the near-slope: 5.76%% is steeper than a benign contango should run. Forward 22.33245956 sits richer than spot 18.90 - that's where the Hormuz event premium is concentrated, bid into the front-end without leaking to the back.

Trade it: calendar spreads that short front-month IV against long 30 - 60 DTE capture the richness asymmetrically. Core short-vol structures belong in the 30 - 60 DTE sweet spot where carry is cleanest. Avoid selling 1-DTE into the headline window - that's the unhedgable gap, not premium to harvest.

What it means for your trading

Contango is paying sellers but the front-end carries concentrated Hormuz event premium - harvest it through calendars short the bid-up front against long 30 - 60 DTE, and keep 1-DTE off the sheet until the headline tape clears.

Trading readSteep contango with near-slope 5.76%% says vol sellers' carry is intact and the market is NOT pricing systemic stress - but front-month is bid relative to the curve, holding event-premium for the Iran headline window.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

The carry trade is broken. SPY ATM IV prints 14.7% against HV20 of 17.89 - VRP sits at -3.19%, and HV20 above HV60 (15.21) confirms realized is accelerating, not decaying into the tape.

The negative-VRP signature is uniform: QQQ at -3.13%, IWM at -0.17%. Index options are cheap to the moves actually printing. Pure premium-harvest structures lose their statistical edge here - the iron condor recommendation (Iron Condor, score 29) is a pin trade now, not a carry trade, and must be sized accordingly.

Flip the playbook: long convexity pays. Long-gamma and long-vega trades in the 30-45 DTE window screen positive-EV against cheap IV, and downside puts in QQQ stack dealer-flow amplification on top of the vol mispricing. Short premium only paired with directional thesis, not as standalone carry.

What it means for your trading

Negative VRP across SPY, QQQ and IWM with HV20 above HV60 means IV is under-pricing realized - statistical edge flips to long-convexity structures, while short-premium setups need a directional overlay to justify the trade.

Skew Convexity

SPY quarter-delta skew prints 2.46% with smile ratio 1.2% - steep, but ordered. Put quarter-delta IV at 14.87% sits well above ATM 13.09%, while the call wing inverts to 12.41% - classic equity shape, downside bid hard, upside unloved. No panic convexity, but no upside chase priced in either.

The flat call wing is the tell: dealers and books have zero conviction above spot, which ratifies the 710.00 call wall as a real ceiling rather than a speed bump. Smile ratio is elevated but sub-panic, so put richness is harvestable - not something to pay through.

Structure the downside as a spread, not a naked leg. Long the quarter-delta put, short a further-OTM put monetizes skew steepness while keeping the Hormuz tail defined. Naked puts overpay the wing; put spreads capture the richness at 2.46% without buying the fear outright.

What it means for your trading

Skew is steep but ordered at 2.46% with a flat call wing - downside is bid, upside is dead, and put spreads beat naked puts on risk-adjusted terms given the geopolitical tail.

Vol-of-Vol Structure

VVIX at 98.57 (+3.62%%) sits squarely in Normal territory, and the VVIX/VIX ratio of 5.22 is benign - no bimodal-outcome pricing, no panic premium stacked into vol options themselves. Sizing guidance reads Standard Size; this is not a cut-risk tape by the vol-of-vol math alone.

The tell is in the rate of change: VVIX lifted 3.62%% against VIX's 8.12%% - a quiet convexity bid starting to build under the surface while headline vol drifts. That's jump-protection being accumulated without the curve confirming it yet, and it's the first place a Hormuz escalation would print before the front-month VIX catches up.

Trade it as standard-size until VVIX clears 110 - that's the half-size threshold where vol-of-vol itself flags bimodal pricing and the standing short-premium playbook loses its cushion.

What it means for your trading

Vol-of-vol reads Normal with ratio 5.22 - no panic bid, sizing remains Standard Size, but VVIX outpacing VIX on the day is the early convexity-accumulation signal to respect.

Dispersion Spread

Index vol is cheap to its single-name proxies: SPY ATM IV prints 14.7% against QQQ at 19.01% and IWM the richest of the complex at 21.8%. That gap is the widest SPY/QQQ dispersion in months and signals dealer-owned correlation - the index is being pinned by diversified gamma while the component names carry the real risk premium.

The trade writes itself: short SPY/SPX vol against the 710.00/710.00 pin, keep long single-name vega on the movers - NVDA, AAPL, MSFT, META - where idiosyncratic catalysts are not captured by index hedges. With QQQ already slipped to Negative Gamma below 649.17, an index put is thin protection against a tech-led unwind.

IWM at 21.8% with the least-negative VRP at -0.17% is the cleanest premium-sale in the complex; SPY vol is the correlation short, not the carry trade.

What it means for your trading

Dispersion wide: sell index vol around the SPY pin, own single-name vol on the mega-cap movers - index hedges fail against NVDA/AAPL idiosyncratic shocks while dealer-owned correlation caps SPX realized.

Liquidity & Microstructure

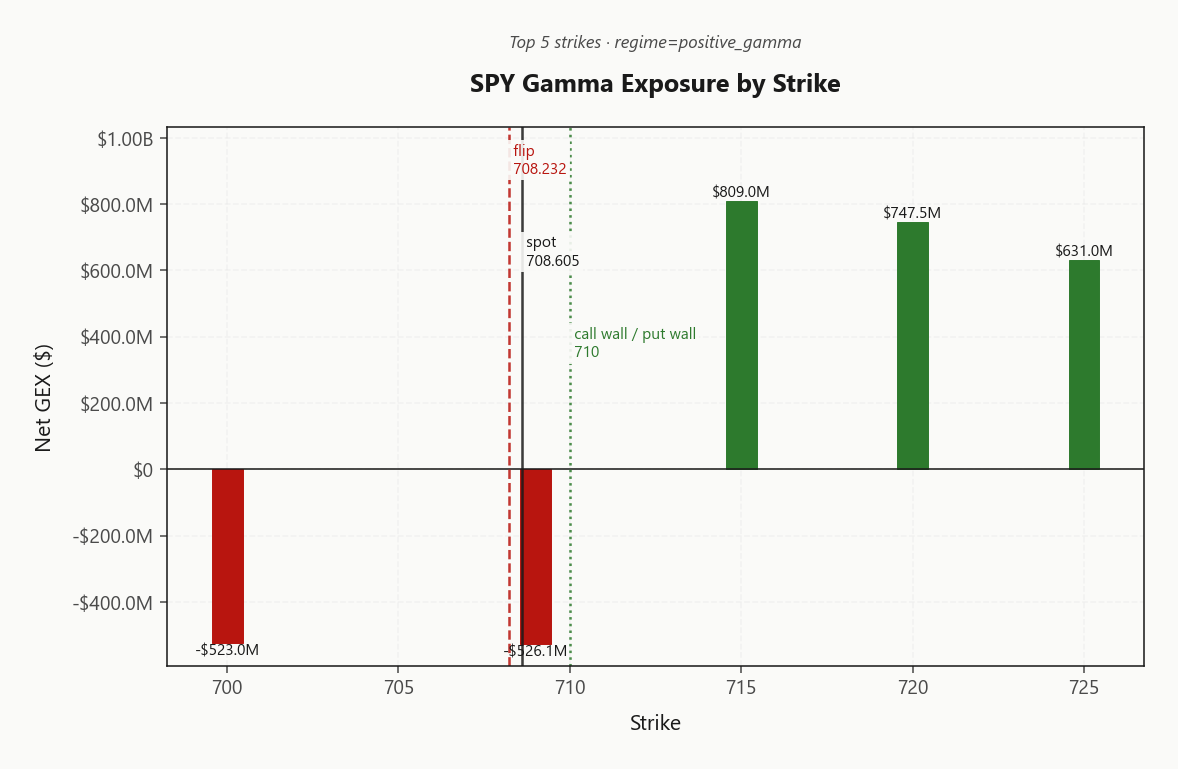

The OI cluster at 600 is stale real estate - deep ITM, not where tomorrow's fight gets decided. The live battle is the collision at 710.00, where call wall and put wall stack the same strike, turning it into a true pin rather than a one-sided cap. Top GEX magnet at 715.00 carries $809M of net gamma - that's the ceiling dealers defend into close.

The regime line is the gamma flip at 708.23, and spot 708.61 sits within a hair of it. Above, dealers buy dips and the tape mean-reverts; below, they sell into weakness and trends extend. With QQQ already tipped to Negative Gamma below 649.17, any SPY breach of flip recombines the complex into a uniformly hostile book.

Trade it: harvest premium tight to the 710.00/710.00 pin while spot holds flip; flatten and rotate to QQQ downside the moment 708.23 cracks.

What it means for your trading

SPY's gamma flip at 708.23 is tomorrow's regime switch - spot 708.61 is parked on top of it, with the 710.00 pin defining the ceiling. Above flip dealers cushion, below flip they amplify - trade the line, not the level.

Trading readMassive call-side gamma stack above current spot dampens upside chase, while the lone negative-gamma strike right at-the-money is where any selloff would accelerate - the 708.23 line is the regime switch.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$213.01B - deeply negative vanna means any uptick in vol forces dealers to sell delta, not buy it. That's the hostile configuration: a Hormuz-driven IV spike doesn't get absorbed, it gets amplified. CHEX at -$31.3M layers charm decay on top - time pressure into the close leans the same direction, compounding rather than cushioning.

The charm pivot resolves to 708.2317723081 (Gamma Flip), with current bias reading Supportive - but distance to pivot is -0.0526707675%, hairline. A small spot move flips the sign on the whole dealer book.

Playbook: treat the supportive tag as technically true, structurally fragile. Vanna and charm both point the wrong way under stress, so harvest premium only tight to the pin and keep tech-side convexity on for the cross-asset leak.

What it means for your trading

Vanna and charm are both pulling hostile - the positive-gamma label is real but the second-order greeks will amplify, not dampen, any shock. Pivot sits essentially on spot at 708.2317723081, so the Supportive bias is one move from inverting.

Cross-Asset Confirmation

MOVE at 65.70 stays suppressed - bond vol isn't confirming any credit or macro shock, so the Hormuz tape is priced as a geopolitical event, not a systemic one. Fear & Greed registers 70 / Greed - sentiment has not flipped to a panic bid, which is precisely the complacency pocket where unhedged tails bite.

The structural tell is the SPY/QQQ regime split: divergence flag True, direction Spy Heavier. Tech is leading down through its flip while the broad tape holds dealer cushion. IWM at 277.31 sits in positive_gamma, absorbing better than QQQ at 646.72 - small-caps are the cross-check that this is a tech-concentrated leak, not broad risk-off.

Trade the split: QQQ is the fragile leg for downside expression, SPY/IWM the premium-harvest side until MOVE or VVIX confirms escalation.

What it means for your trading

Bond vol at 65.70 and F&G Greed say no systemic bid yet, but SPY/QQQ regime divergence (Spy Heavier) marks tech as the fragile leg - hedge there, harvest elsewhere.

Scenario EV

Scoring engine flags Iron Condor as the top structure with a score of 29 against the put-spread alternative at 16, optimal window 30-45 DTE. But the signal prints red - VRP assessment Unknown with SPY realized running hotter than implied means the classic carry thesis is gone. Condor profitability migrates from premium decay to pure pin behavior around the 710.00/710.00 stack.

Tactical read: deploy the condor only if wings hug the walls tight and DTE stays short enough that gamma pin dominates vega bleed. Otherwise pivot to a calendar straddling the Hormuz headline window - short front-month richness, long 30-45 DTE where forward vol 22.33245956 carries cleaner.

Sizing: standard per Standard Size, but stand down entirely if the Vance-Iran headline window is live into the session. Negative VRP plus a hostile-vanna book is not the tape to press premium-short into a gap.

What it means for your trading

Engine says Iron Condor at 29, but the red signal from Unknown VRP means the trade only works tight to walls in 30-45 DTE - otherwise calendar the event window.

Actionable Summary

Trade the divergence. SPY holds Positive Gamma with spot pinned a hair above the 708.2317723081 charm pivot, while QQQ has already slipped Negative Gamma below 649.17. Harvest the Iron Condor in SPY tight to the 710.00/710.00 pin in 30-45 DTE, and pair with QQQ put spreads where dealer flow amplifies downside rather than cushions it.

Watch the pivot.708.2317723081 is the regime line on SPY - bias flips on a half-percent move, so exit the condor if spot breaches. Regime read is Elevated / Watchful; VVIX sizing guidance is Standard Size, but cut a quarter for the Vance-Iran headline window and avoid 1-DTE short premium into the weekend. Hormuz is the unhedgable tail; contango carry does not price it.

What it means for your trading

SPY's Iron Condor edge lives at the 710.00/710.00 pin, but QQQ's negative-gamma slip is the leak - treat tech as the trend leg, not the pin trade.

US-Iran negotiation framing matters because any cement of Tehran's Hormuz position permanently re-prices the global oil risk premium - the dominant macro tape driver this week

Confirms the equity-tape mechanic - geopolitics-driven dips on otherwise positive-gamma days are the fade setups for premium harvesters but the trap if escalation sticks

Real-economy supply chain disruption signal - when Hormuz friction hits Christmas-good prices it converts geopolitical risk into a sticky CPI threat the Fed has to acknowledge

Canadian CPI uptick attributed to Iran-driven gasoline = first real inflation print confirming the geopolitical-to-macro channel; expect more global prints to follow

Pre-market summary that frames the day's tape - useful baseline for retail-flow expectations and confirms oil-vol-equity linkage as today's dominant theme

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.88 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Spy Heavier across SPY, QQQ, and IWM.

SPY's gamma flip is at 708.23 against a spot of 708.61. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.7% with a volatility risk premium of -3.19%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 18.90. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime