Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

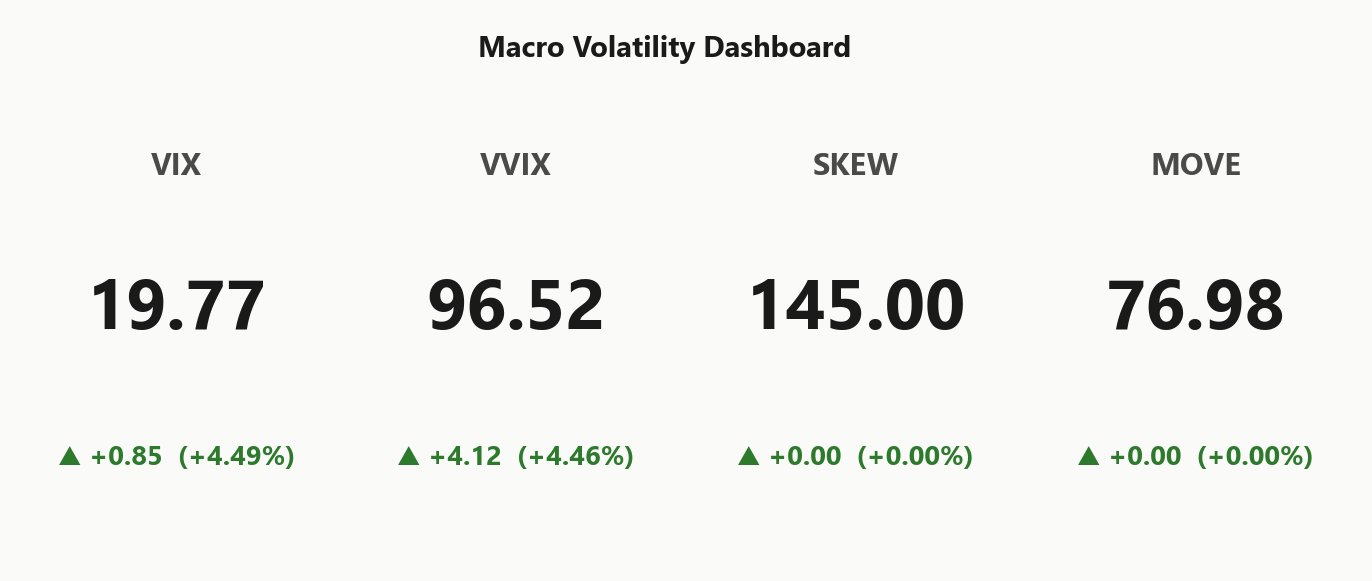

SPY closed at 736.38 with net GEX at -$11.55B - dealers are short gamma and the regime is Negative Gamma. Gamma flip sits at 742.84 (spot below = amplification mode), call wall 750.00, put wall 735.00 acting as the line in the sand. Net VEX at -$68.1B means a vol spike forces dealers to sell more delta - vanna is hostile here. Net CHEX is $601.1M, mildly supportive into the close. VIX at 19.77 (+4.49%%) with VVIX at 96.52 - term structure in Contango but the front is bid, VRP sits at 5.15%. Fear & Greed reads 33 (Fear) heading into CPI. Bottom line: trade for a CPI-driven break of 735.00 or a pin into 730.00 - but half-size, vanna is loaded against the tape.

Negative gamma across SPY/QQQ/IWM with VIX in Contango - amplified moves, watchful regime

SPY closed below the gamma flip at 742.84 with dealers net short gamma, leaving moves amplified into tomorrow's CPI print. VIX term structure remains in Contango but VVIX is bid alongside spot VIX, signaling rising vol-of-vol under a fear-rated tape. Iron condor scoring leads Iron Condor in the 30-45 window - but size down: the put wall at 735.00 is the only thing between spot and a vanna-accelerated air pocket.

Regime Assessment

Regime registers as Elevated / Watchful with VIX printing 19.77 - squarely in the Elevated bucket, not panic, not complacent. The half-life sits at 15 sessions, which is the load-bearing number: this state is sticky, and stickiness rewards carry-collection structures over directional bets.

The transition math backs that read. Probability of escalation to panic inside five sessions is only 0.05, while the probability of mean-reverting back to low-vol within ten sessions is 0.25 - base rates favor the fade, not the chase. The asterisk is CPI: a hot print reprices that panic probability in a single session, so the base rate is the right anchor but the wrong sole input.

Trade implication: structures should target the 30-45 DTE window where regime persistence pays you, not the front-week where the event kink lives. Recommended expression is Iron Condor at half size into the print, full size after.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life - sticky enough to fade extremes, but conditioned entirely on CPI not breaking the base rate.

Trading readVIX rising, VVIX rising in lockstep, SKEW unchanged, MOVE unchanged - equity vol is bidding alone. That divergence pattern is event-specific (CPI), not regime-shifting; a clean print snaps it back.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

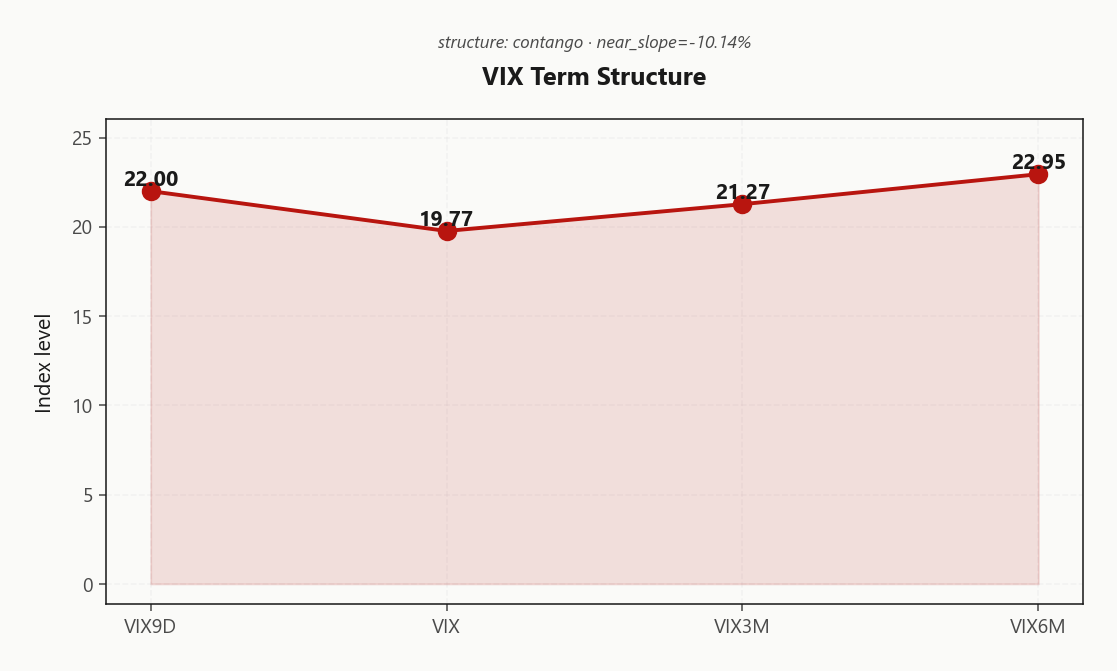

The VIX curve carries an unmistakable event-premium kink at the front: VIX9D at 22.00 prints above spot VIX at 19.77, while VIX3M holds 21.27 and VIX6M anchors at 22.95. The CPI window is being paid for explicitly; beyond it, the structure resolves cleanly to Contango.

Forward 30 - 60 vol clears at 21.9816491647 and 60 - 90 at 24.5151402199 - the back end is pricing regime stability, not contagion. Front-month VIX futures at 21.27 with basis at 7.59% keep the carry alive for short-vol overlays sitting behind the kink.

Trade: sell the rich front-week vol against long 30-45 DTE - calendars own the structural edge. Front is rich versus realized; the belly is the hedge that survives a CPI miss without surrendering carry on a clean print.

What it means for your trading

Event-premium kink at the front masks an otherwise Contango curve with a Flat forward regime - sell front-week vol, hold 30-45 DTE as the structural hedge.

Trading readContango holds beyond the front-week, but VIX9D printing above spot VIX is a clear event kink. Carry trade lives on the back of the curve; the front is paying you to hedge, not to harvest.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

SPY ATM IV at 18.08% trades well above realized - HV20 prints at 12.93 and HV60 sits below it, leaving the VRP at 5.15% vol points. The IV/RV spread reads Healthy Premium - vol sellers carry structural edge, but CPI is the binary that decides whether the premium gets paid or repriced overnight.

The tell: HV60 above HV20 means realized has been decelerating even as IV bids up, widening the carry rather than compressing it. RV5 at 19.13 is the warning shot - the short window is creeping back toward implied, and a single hot print closes the gap in a session. Until then, the fat tail of the spread is rent the desk collects.

Iron condor scored 49 on the back of this VRP - the structural expression at 30-45 DTE, clear of the front-week event kink. Size half into the print; the carry only survives if CPI lands inside the priced cone.

What it means for your trading

VRP at 5.15% points is rich enough to underwrite Iron Condor structures at 30-45 DTE, but RV5 at 19.13 shows realized is already creeping - a hot CPI closes the gap in one session, so half-size the carry.

Skew Convexity

The 3.99% vol-point spread between put and call quarter-delta wings tells the positioning story cleanly: put 25d marks 24.47% against ATM at 21.96% and call 25d compressed to 20.48%. Crowd is paying meaningful premium for downside protection while showing zero upside conviction - calls flat tells you nobody is chasing into CPI.

Smile ratio at 1.2% reads as ordered, not panicked - this is hedging flow, not capitulation. With skew classified Skew Steep, put spreads and put ratios harvest more decay per unit risk than naked short puts; the steep wing funds the short strike. Tail still cheap relative to the body - convex hedges like put butterflies get underwritten by the VRP at 5.15%.

Actionable into the print: harvest the steepness now via put spreads, or pre-position convex hedges before a downside CPI surprise steepens skew further. Either way, do not sell naked puts here - the per-vol economics favor the spread every time.

What it means for your trading

Steep, ordered put skew with compressed call wing means the desk is hedged but not chasing - sell put spreads to capture skew decay, not naked puts, and treat put butterflies as cheap convex insurance funded by the 5.15% VRP.

Vol-of-Vol Structure

VVIX sits at 96.52 against spot VIX at 19.77, with the ratio printing 4.88 - bucketed Normal. Technically benign, but the tape is climbing 4.46% on the session in lockstep with spot VIX. That coupling is the tell: this is not a headline VVIX print, it is a real bid for jump optionality ahead of CPI.

Model sizing guidance reads Standard Size - short-vol structures can run at full clip on the carry. But the lockstep move with spot VIX argues for discipline at the threshold: if VVIX breaches triple digits intraday post-print, cut size in half on any short-strangle exposure. The convex hedge side of the book is the under-owned trade - long-vol wings remain underpriced versus the bimodal CPI outcome the curve is pricing.

What it means for your trading

Vol-of-vol is bucketed Normal at a 4.88 ratio with sizing cleared to Standard Size, but the rising-with-VIX pattern means convex long-vol hedges are the cheap side into CPI.

Dispersion Spread

Index vol at 18.08% sits alongside QQQ at 29% and IWM at 26.81% - dispersion is wide and IWM remains the cheapest premium in the complex. The gap isn't noise: single-name IVs are bid because mega-cap catalyst risk (AAPL post-Siri, NVDA earnings runway, META quietly repositioning) lives inside the cap-weighted index but doesn't show up in an SPY hedge. Cross-strike dispersion confirms it - narrow ATM at 40.41, blown out in the wings, where tail premium is doing the hedging work.

Implied correlation reads moderate, which is the textbook setup: buy index vol, sell single-name vol if you want a clean dispersion expression. For pure VRP carry, SPY/SPX is the cleanest line - it strips the idiosyncratic blowup risk that an AAPL or NVDA single-name short would carry into a binary catalyst window. Trade the macro print in SPY, isolate single-name vol only against company-specific catalysts; don't cross the streams.

What it means for your trading

Wide single-name premium against index IV at 18.08% signals idiosyncratic risk an SPY hedge won't catch - keep macro exposure in index vol and isolate single-name vol to its own catalysts.

Liquidity & Microstructure

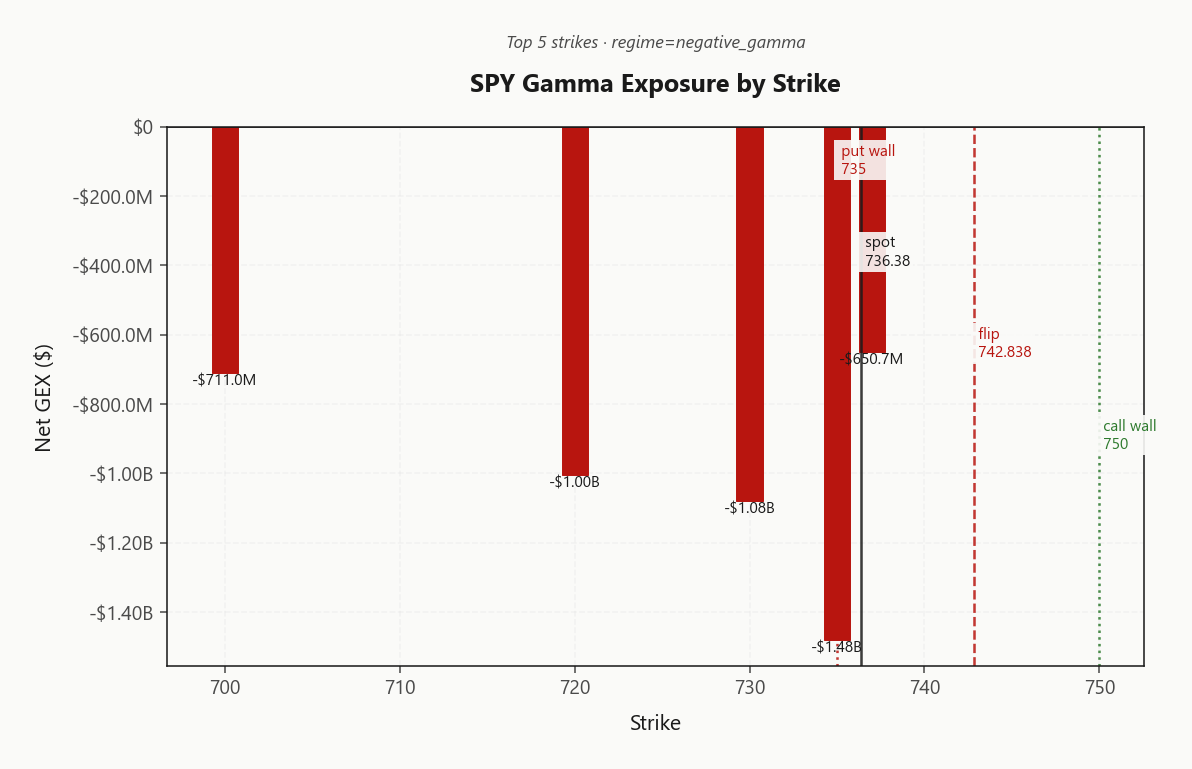

Spot at 736.38 trades beneath the gamma flip at 742.84 - dealers are short gamma and any directional impulse gets amplified into close. The book's center of gravity sits at the 735.00 put wall, where top-strike concentration registers net GEX of -$1.48B at 735.00. That's the defended floor into CPI.

Below the wall, OI thins into the 700 magnet - a gravity well the tape can travel to fast if dealers lose the line. Upside is capped by the 750.00 call wall; in this regime, rallies into it are short-able rather than chase-able. Charm pivot at 735 reads Neutral, leaving the structure balanced on a single level.

One actionable framing: a sustained CPI-driven break of 735.00 opens a vanna-accelerated path toward 700; a hold flips the regime back to mean-reversion against the call wall.

What it means for your trading

The 735.00 - 742.84 corridor defines tomorrow's tape: hold reverts toward 750.00, break accelerates into the 700 OI magnet.

Trading readNegative gamma stacked from spot down through the put wall - dealers will amplify selloffs into the 735.00 - 700 corridor. The call wall at 750.00 caps any CPI relief rally; fade strength into it.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints deeply negative at -$68.1B - vanna is the dominant accelerant here. Any IV spike forces dealers to dump delta into the move, compounding downside. Charm at $601.1M offers only modest into-close support (Time decay pushing dealers to buy - supportive into close) - a fragile counterweight against a vol-driven slide, not a floor.

The pivot sits at 735 (Put Wall), with spot hovering -0.1874032429 from the line and bias reading Neutral. Below pivot, vanna accelerates losses on any IV kick - defensive sizing is mandatory. Above it, vanna stabilizes and short-vol structures can run at full size.

Bottom line: the pivot is the on/off switch for risk appetite. Hold above 735 and the Iron Condor carries cleanly; lose it on a CPI surprise and the vanna trap snaps shut against 735.00.

What it means for your trading

Vanna is loaded against the tape with VEX at -$68.1B; the 735 pivot is the line that flips dealers from accelerant to stabilizer - trade it, don't fight it.

Cross-Asset Confirmation

MOVE sits at 76.98 with credit vol unchanged on the session - the bid is equity-only, not a macro shock bleeding through rates. That decoupling matters: when VIX climbs alone, the premium is event-specific and snaps back on a clean catalyst clear, whereas a coincident MOVE bid would force defensive structures across the book.

Fear & Greed reads 33 (Fear) - positioning is already skewed defensive, which is contrarian fuel if CPI doesn't disappoint. QQQ at 707.55 and IWM at 284.65 both close beneath their flips, putting the complex in Aligned negative-gamma posture across SPY/QQQ/IWM.

No divergence to fade here: the lead story is the catalyst, not relative dislocation. Cross-asset tone reads Unknown - single-driver tape into print, so trade the macro event in its cleanest expression rather than hunting for inter-index alpha.

What it means for your trading

Equity-only vol bid against a quiet MOVE and uniformly negative-gamma index complex - this is a CPI-driven tape, not a credit shock, and defensive positioning at Fear sets up contrarian fuel on a benign print.

Scenario EV

The scoring engine lands on Iron Condor at 49 in the 30-45 DTE window - the structural trade tonight. VRP at 5.15% funds the carry, steep put skew at 3.99% cheapens the downside wing, and flat call skew lets the upside cap fund itself. Condor neutrality is the feature, not the bug - it sidesteps the CPI binary while still harvesting the rich front-belly premium.

Put spread runs a close second at 44 - the directional alternative if the tape tips its hand before the print. Avoid the front-week: event premium is too rich, gamma too sharp, and naked short strangles walk straight into the negative-VEX trap at -$68.1B.

The 30-45 belly cleanly separates from the kinked front-week vol at 22.00 and rides regime stickiness - half-life of 15 sessions rewards the carry. Half-size into the print, restore after.

What it means for your trading

Iron condor in 30-45 DTE is the recommended expression at score 49 - rich VRP and steep skew fund the structure, condor neutrality dodges the CPI binary. Put spread at 44 is the directional fallback if conviction develops.

Actionable Summary

Trade: short Iron Condor in the 30-45 DTE window - VRP at 5.15% pays the carry, the regime is sticky at a 15-session half-life, and the structure scored 49 against the alternative book. Half-size into the CPI print; restore full size only after the catalyst clears and VVIX at 96.52 stabilizes.

Watch: the 735 pivot - a sustained break below opens a vanna-accelerated path toward 700 with net VEX at -$68.1B doing the damage; hold above and the condor runs as charm at $601.1M drips supportive flow into the close. Avoid: front-week 0 - 3 DTE structures (event kink plus sharp gamma), naked short strangles (vanna trap), and single-name short vol where idiosyncratic catalysts dominate.

Context: regime classed Elevated / Watchful at VIX 19.77 with index complex Aligned below their flips - fade extremes into the walls, don't chase moves through them.

What it means for your trading

Sell Iron Condor in 30-45 DTE at half size into CPI, anchored on the 735 pivot. Regime is Elevated / Watchful - sticky enough to harvest VRP, but vanna at -$68.1B is loaded against the tape if 735.00 breaks.

May CPI prints Wednesday morning with consensus pointing to a 4.2% annual pace - the singular catalyst that will reprice the entire VIX term structure and validate or destroy the current VRP carry trade.

Trump blaming Iran for a helicopter downing and signaling a US response is the geopolitical wildcard that explains MOVE's quiet bid and the front-week VIX9D kink - equity vol is partially pricing escalation risk.

Apple sliding on the Siri reveal is the proximate cause of the AAPL GEX repositioning and helps explain QQQ's negative gamma posture - single-name catalyst rippling through the cap-weighted index.

Gulf markets rebounding on the Iran-Israel attack pause is the cross-asset confirmation that geopolitical premium is reverting, leaving CPI as the dominant risk factor in tomorrow's session.

US energy chief flagging rising oil exports through Hormuz matters because oil-vol feedthrough to CPI is non-trivial - a geopolitical premium reset in crude could amplify or dampen tomorrow's inflation read.

Higher open with oil declining and a heating SpaceX IPO sets the risk-on backdrop for today's session - but the gamma regime says fade strength into walls regardless of headline tone.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 19.87 with a Contango term structure. The Fear & Greed index reads Fear, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 742.84 against a spot of 736.38. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 18.08% with a volatility risk premium of 5.15%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 19.77. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime