Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

SPY is trading at 707.19 in a Positive Gamma regime with net GEX at $12.8B - dealers are deeply long gamma and will buy any dip, dampening intraday moves and favoring mean reversion. Key levels: call wall at 710.00 is the upside magnet and resistance, put wall at 700.00 provides the floor, and the gamma flip sits at 674.01 - spot is well above the flip, providing a deep cushion where dealer hedging flow is structurally supportive. Dealer vanna exposure at -$234.05B is heavily negative, meaning a vol spike would push dealers to sell delta and amplify downside - but with VVIX at 96.80 in Normal territory, that trigger is distant today. Charm at -$20M is mildly negative, implying light dealer selling pressure into the close. Vol read: VIX at 17.23 in Contango from 15.46 to 22.78, but VRP at -6.03% is negative - implied is cheap to realized, meaning premium sellers are undercompensated relative to actual recent moves. Sentiment at Greed (65) is supportive but not extreme. Bottom line: fade intraday strength into the 710.00 call wall, consider Iron Condor structures in 30-45 DTE, but widen wings given negative VRP - the carry looks better than it is.

Iran ceasefire optimism is driving risk-on across the index complex, with SPY at 707.19 in Positive Gamma territory and net GEX at $12.8B. The tape is structurally dampened - dealers buy every dip, sell every rip - but negative VRP at -6.03% warns that realized moves are outrunning what options are pricing. Today's question: does the Iran peace narrative compress vol further, or does the gap between implied and realized snap shut the hard way?

Regime Assessment

The vol regime sits at Elevated - Elevated / Watchful - with VIX printing 17.23 and the transition math skewed decisively toward calm. Probability of a panic escalation within five sessions is just 0.05 - negligible - while the odds of decaying into a low-vol regime over ten sessions run at 0.45, meaningfully higher and the base case if Iran peace headlines hold. Half-life of the current state is 15 sessions; size trade duration inside that window.

This is a watchful regime that statistically favors gravitating toward suppression rather than spiking into dislocation. Tail hedges remain insurance, not urgency. The asymmetry worth positioning around: if ceasefire solidifies, the transition to low-vol compresses VIX rapidly and the elevated label unwinds - front-end vol sellers capture that regime decay. If talks fracture, the watchful label turns sticky, but the path to panic still requires a multi-standard-deviation catalyst that the market is not pricing today.

What it means for your trading

Regime is Elevated / Watchful with a half-life of 15 sessions - statistically biased toward decay into low-vol (0.45 probability over ten sessions) rather than escalation to panic (0.05 over five), making this a structurally supportive backdrop for defined-risk premium selling with duration calibrated inside the half-life.

Trading readVIX declining with VVIX subdued while SKEW ticks higher creates a subtle divergence: spot vol is calm but tail pricing is quietly firming. MOVE staying low confirms this is an equity-specific geopolitical story, not a cross-asset credit event - calibrate hedges accordingly.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

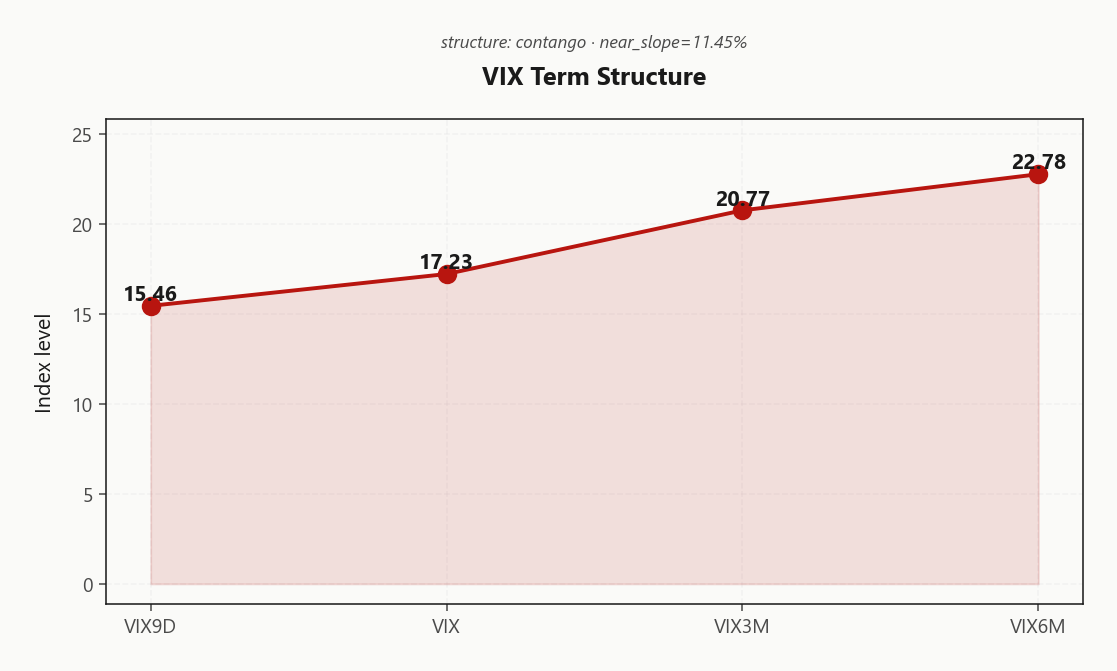

Forward Vol Geometry

The term structure prints a textbook ascending staircase - 15.46 through 17.23, 20.77, and out to 22.78 - confirming deep Contango and live vol carry across every tenor. But the slope is not uniform: forward vol steepens sharply in the belly, with the implied forward between the monthly and quarterly tenors at 22.3305373872 and the quarterly-to-semi-annual leg reaching 24.6264877723. The back end is pricing event risk the front refuses to acknowledge - Iran peace reads as a near-term reprieve, not a structural regime reset.

The Steep Contango regime and the Steep contango - vol sellers favored read are unambiguous: front-end vol selling is structurally supported where dealer gamma compresses realized and contango delivers positive roll yield. Best edge sits in the shortest-dated tenors where dampening is most acute. But negative VRP at -6.03% is the offset - realized is outrunning implied, meaning carry looks richer on paper than in execution. Size down, tighten stops, and let the gamma cushion do the heavy lifting rather than levering into headline carry.

What it means for your trading

Steep contango from 15.46 to 22.78 with forward vol accelerating sharply in the belly favors front-end vol selling where the Steep Contango regime and dealer gamma alignment compress realized - but negative VRP demands reduced sizing and defined-risk structures over naked premium.

Trading readTextbook contango from VIX9D through VIX6M says the market expects near-term calm to gradually normalize higher - vol carry trades are structurally supported, but the steepness of the slope reveals embedded uncertainty about whether geopolitical calm persists beyond the immediate horizon.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM implied at 13.15% sits well below trailing realized, leaving VRP at -6.03% - squarely in Danger Zone territory. Options are genuinely cheap to what the tape has delivered, and the contango carry visible in the term structure is being eroded by realized moves that outsize premium collected. Sellers are structurally undercompensated.

The realized hierarchy adds critical nuance: short-lookback RV at 5.65 versus medium-term at 19.18 reveals sharp deceleration - the Iran peace bid is already compressing actual moves even as the trailing window stays elevated. If this convergence holds, implied looks less cheap within sessions. But until the medium-term reading catches down, the VRP gap remains a live headwind for vol-selling strategies.

Net: gamma and contango invite premium selling; the Danger Zone read demands defined-risk structures and wider wings. Do not sell naked into negative VRP.

What it means for your trading

IV-RV spread assessment reads Danger Zone with VRP at -6.03% - options are underpricing realized, but short-term RV at 5.65 is decelerating sharply from 19.18, signaling the gap may close from the realized side rather than through an IV repricing higher.

Skew Convexity

Quarter-delta skew prints at 2.66% with the smile ratio at 1.28% - puts are paying up meaningfully relative to calls. Put quarter-delta IV at 12.28% versus ATM at 11.16% versus call quarter-delta at 9.62% reveals moderate but orderly richness in downside protection. This is structural hedging demand beneath the positive-gamma cushion, not dislocation - institutions are maintaining their put books while the tape grinds higher.

Call skew is notably flat, confirming zero upside conviction through the options complex. The Iran peace rally is entirely futures- and spot-driven; no one is reaching for calls to express it. That asymmetry matters: if ceasefire momentum holds, skew flattens as hedging unwinds and the left tail reprices cheaper. If talks collapse, that orderly put premium reprices violently higher with vanna amplifying the move.

Favor spread protection over naked puts given the well-behaved skew surface - risk reversals are relatively cheap, and defined-risk structures capture the hedge without overpaying for dislocated convexity.

What it means for your trading

Orderly but steep put skew at 2.66% with an elevated smile ratio of 1.28% signals systematic institutional hedging, not panic - favor put spreads over naked structures while risk reversals remain cheap and call skew stays flat.

Vol-of-Vol Structure

VVIX at 96.80 against VIX at 17.23 puts the ratio at 5.62 - squarely in Normal territory. The vol-of-vol surface is not pricing regime transition risk. Despite a geopolitical backdrop that could credibly produce bimodal outcomes, the options-on-options market has digested Iran uncertainty and shifted into price-discovery mode. Jump risk, as expressed through VVIX, reads as low-probability today.

Sizing stays at Standard Size. There is no structural reason to cut exposure or move to half-size caution - the vol-of-vol complex is giving a clean green light for standard positioning within the prevailing Positive Gamma regime. If VVIX were to spike above elevated thresholds, that would be the signal to derisk and widen, but the current read is unambiguous: the market trusts the Contango carry trade and is not hedging against a sharp repricing of the volatility surface itself.

Watch for a dislocation between VVIX and spot VIX if Iran headlines turn - that ratio compressing rapidly would be the earliest signal that tail protection is repricing before directional vol catches up.

What it means for your trading

VVIX/VIX ratio at 5.62 in Normal range confirms vol-of-vol is not flagging regime transition - Standard Size positioning is appropriate with no need to hedge against a jump-risk repricing today.

Dispersion Spread

Index ATM IV at 13.15% with cross-expiry dispersion at 2.76 and cross-strike dispersion at 76.19 - the vol surface is moderately uniform, not dislocated. Single-stock gamma is converging toward the index regime: NVDA, AAPL, META, AMZN, and TSLA all shifted positive today, compressing the correlation gap that dispersion trades need to breathe. When the top five movers align with SPY's Positive Gamma posture, implied correlation rises and index vol sells richer relative to the basket.

That alignment favors SPX structures over single-name premium selling. Index gamma dampening flows directly into your short vol P&L; single-name positioning carries idiosyncratic earnings risk that the index hedge cannot absorb. With the vol surface this coherent, dispersion is moderate at best - the edge is in harvesting the index-level dampening, not in picking off component mispricings.

Watch for upcoming mega-cap earnings to fracture the alignment and re-open dispersion.

What it means for your trading

Cross-expiry dispersion at 2.76 and cross-strike at 76.19 signal a moderately uniform surface with single-stock gamma aligning to index gamma - favor SPX vol selling over single-name until earnings catalysts break the correlation convergence.

Liquidity & Microstructure

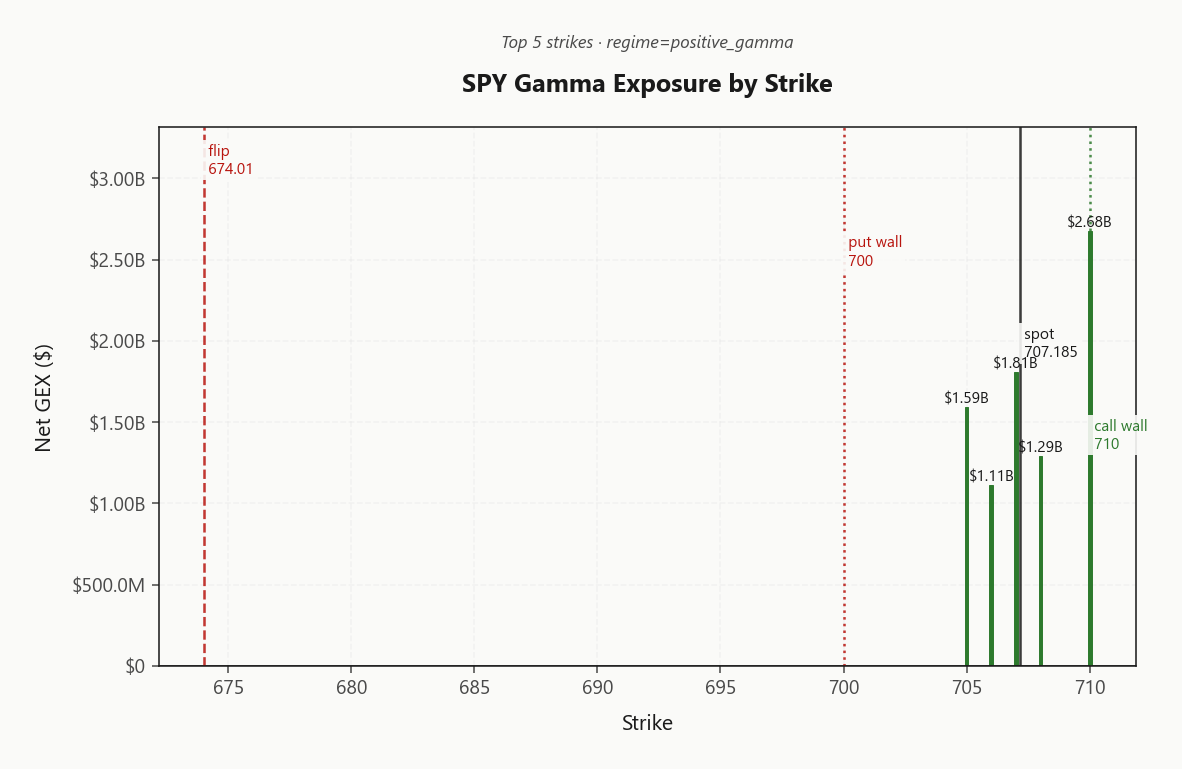

The book is pinned. SPY's call wall at 710.00 and put wall at 700.00 frame a compressed range, with the top strike cluster at 710.00 carrying $2.68B in net GEX - dealers will sell aggressively on any approach to that ceiling. Below, the put wall provides a dampened floor where hedging flow absorbs selling pressure before it gains traction.

Spot sits well above the gamma flip at 674.01, confirming deep Positive Gamma territory - every dip gets bought by dealer rebalancing, and that floor is structural, not discretionary. The highest OI strike at 600 is legacy positioning far below spot; ignore it as a magnet. In tech, QQQ's call wall at 645.00 is acting as an independent lid - watch for convergence or divergence between both walls as the session develops, since a QQQ breakout above its ceiling would signal broader momentum the SPY book is not yet pricing.

Net positioning favors mean-reversion scalps inside the walls. Fade strength into 710.00, lean on 700.00 as support, and respect the gamma flip at 674.01 as the regime line - a break below it shifts the entire dealer flow calculus.

What it means for your trading

Deep positive gamma with spot well above 674.01 means dealer hedging structurally buys dips and sells rips - fade into the 710.00 call wall, lean on 700.00 as the floor, and treat the gamma flip as the line where the regime breaks.

Trading readMassive positive gamma clusters near spot with the call wall as the dominant magnet - dealers will aggressively buy dips and sell rallies, making breakouts in either direction difficult today. Fade moves into walls until the gamma flip is threatened.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Vanna is the regime's loaded spring. Net VEX at -$234.05B is deeply negative - dealers are structurally short vanna, meaning any VIX spike forces them to sell delta into weakness rather than buy it. Gamma is buying every dip today, but vanna sits underneath as the Achilles heel: a ceasefire collapse that reprices front-end vol would flip dealer flow from mean-reversion support to pro-cyclical liquidation. That asymmetry demands defined-risk structures over naked premium.

Charm tells a quieter story. Net CHEX at -$20M is mildly negative - expect gentle selling pressure into the close as time decay shifts dealer hedging obligations, but nothing that overrides gamma's dominance. The charm pivot sits at 710 (the Call Wall), with spot just 0.3980570855 away and current bias reading Neutral. No strong directional pull from second-order flows today - gamma owns the tape until vol moves.

What it means for your trading

Gamma provides the floor, but deeply negative vanna at -$234.05B is the latent accelerant - any vol spike converts dealer flow from supportive to destructive. Charm pressure via -$20M is too mild to override, and the Neutral bias near the 710 pivot confirms second-order greeks are passengers, not drivers, in today's session.

Cross-Asset Confirmation

All three equity indices - SPY, QQQ, and IWM - are printing Positive Gamma with regime alignment Aligned, delivering uniform dealer dampening across the complex. No rotational stress, no intermarket divergence - the Iran peace bid is lifting boats indiscriminately. QQQ at 645.96 and IWM at 273.91 both sit above their respective gamma flips, confirming structurally supportive hedging flow in tech and small caps alike.

Rates vol is a non-event: MOVE at 65.89 confirms bond markets are not leaking stress into equities. This is a pure geopolitical de-escalation trade, not a cross-asset credit repricing. Fear & Greed at 65 (Greed) is supportive for continuation but edging toward contrarian caution territory - not yet a fade signal, but the next leg higher narrows the margin.

The canary is IWM: net GEX at $926M is the thinnest cushion in the complex. If the ceasefire narrative fractures, small caps crack first - that is your early-warning read for broader regime deterioration.

What it means for your trading

Cross-asset gamma alignment at Aligned with suppressed rates vol confirms a structurally coherent, mean-reversion-dominant tape - monitor IWM's thinner gamma cushion at $926M as the leading indicator if geopolitical sentiment reverses.

Scenario EV

The structural read favors Iron Condor at a score of 47 in the 30-45 DTE window - Positive Gamma dealer flow across the complex dampens breakout risk while steep contango from 15.46 through 22.78 delivers term structure carry into the wings. This is the textbook condor setup: rangebound hedging mechanics, ascending vol curve, and Aligned regimes compressing realized dispersion.

Directional structures lag - put spreads score just 33 because dealer gamma structurally fights every selloff, making downside bets a grind against the floor at 700.00. The call wall at 710.00 caps upside with equal conviction. Fade the temptation to get directional when dealers are buying every dip and selling every rip.

The caveat is VRP: -6.03% negative spread means realized is outrunning implied, so collected premium understates actual move risk. Widen wings beyond standard width, size per Standard Size - VVIX at 96.80 in Normal territory permits full allocation - and anchor to the 30-45 DTE bucket where contango carry is richest.

What it means for your trading

Iron condors in 30-45 DTE score 47 on the back of Positive Gamma dampening and steep contango, but negative VRP at -6.03% demands wider wings and defined-risk structures - premium looks richer than it is.

Actionable Summary

Primary structure: Iron Condor on SPX in the 30-45 DTE window, centered near spot and sized per Standard Size guidance. Widen wings - VRP at -6.03% means realized is outrunning implied, and the carry is thinner than the term structure suggests. Fade strength into the 710.00 call wall, which converges with the charm pivot at 710 as today's hard ceiling. Defined-risk only; naked premium selling is mispriced given the VRP backdrop.

The Elevated / Watchful regime sits on a deep Positive Gamma floor - dealers buy every dip above the 674.01 flip - but vanna at -$234.05B is the latent accelerant. If Iran ceasefire talks collapse and vol spikes, dealer flow inverts from supportive to liquidating. IWM's thinner cushion at $926M is the canary - if small caps crack, the regime breaks there first. Stay structured, stay defined-risk, and respect the walls.

What it means for your trading

Iron Condor structures in 30-45 DTE capture the Contango carry while positive gamma dampens breakouts, but negative VRP at -6.03% demands wider wings and defined risk - fade into the 710.00 call wall and watch $926M as the regime's first point of failure.

Iran declaring the Strait of Hormuz open during ceasefire is the single biggest overnight catalyst - this directly unwinds the energy supply-shock premium that has been elevating cross-asset vol and depressing risk appetite for weeks.

Hedge funds deploying massive capital on Iran peace hopes signals institutional conviction that the geopolitical risk premium is compressing - this flow underpins the positive gamma regime and supports continuation of the rally.

Trump framing the war as ending soon adds political weight to the ceasefire narrative - markets will trade this as a binary: peace holds and vol crushes, or talks fail and vanna-driven selling kicks in.

Gold extending its weekly winning streak despite risk-on equity flows signals that safe-haven demand has not fully unwound - smart money is hedging the tail scenario where ceasefire collapses.

A second consecutive weekly dollar decline reflects macro regime rotation - weaker dollar supports US equities and commodity exporters, reinforcing the risk-on bid across the index complex.

Oil crashing on Hormuz reopening directly reduces inflation expectations and takes pressure off the Fed - this is the mechanism through which geopolitical de-escalation becomes structurally bullish for equities.

G7 finance chiefs coordinating on peace and flagging economic damage from the war is a policy signal - expect coordinated central bank accommodation if peace holds, which would further compress vol.

The US military remaining locked and loaded despite peace talks is the tail risk the market is discounting - this is why skew and back-end vol have not collapsed even as VIX falls, and why defined-risk structures beat naked premium selling today.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.74 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 674.01 against a spot of 707.19. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 13.15% with a volatility risk premium of -6.03%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.23. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime