Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

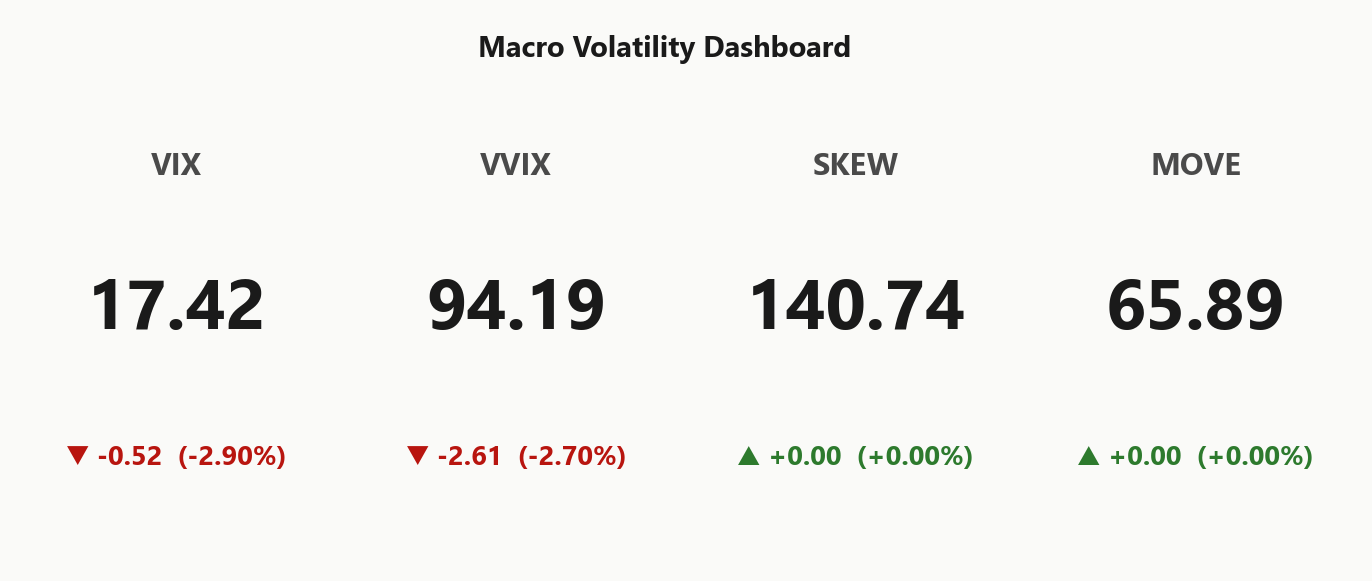

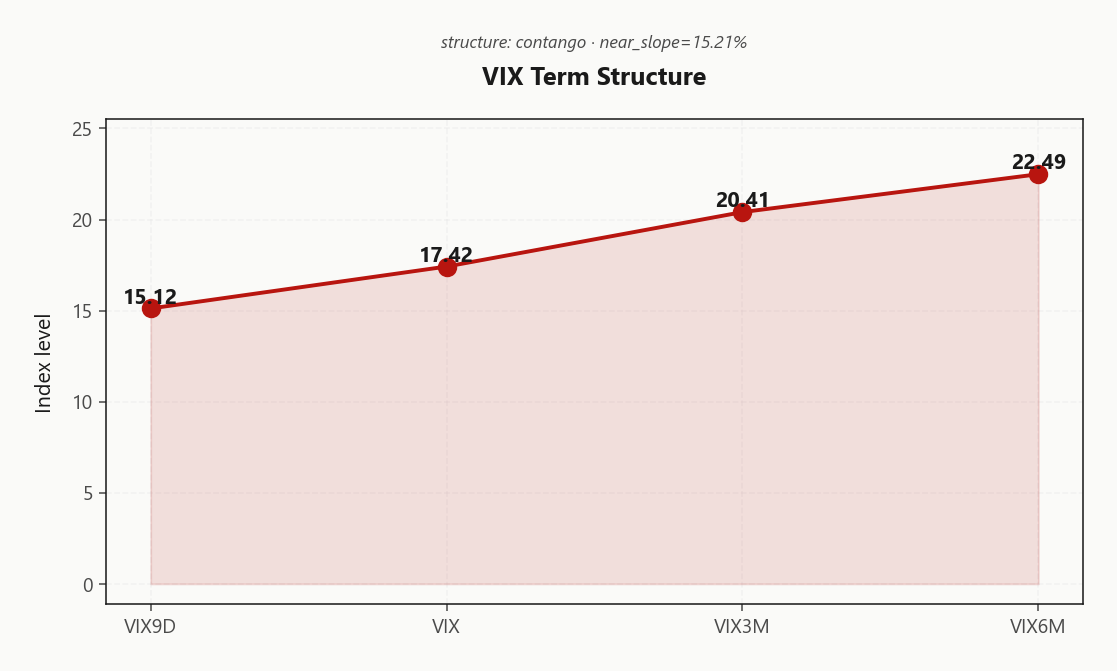

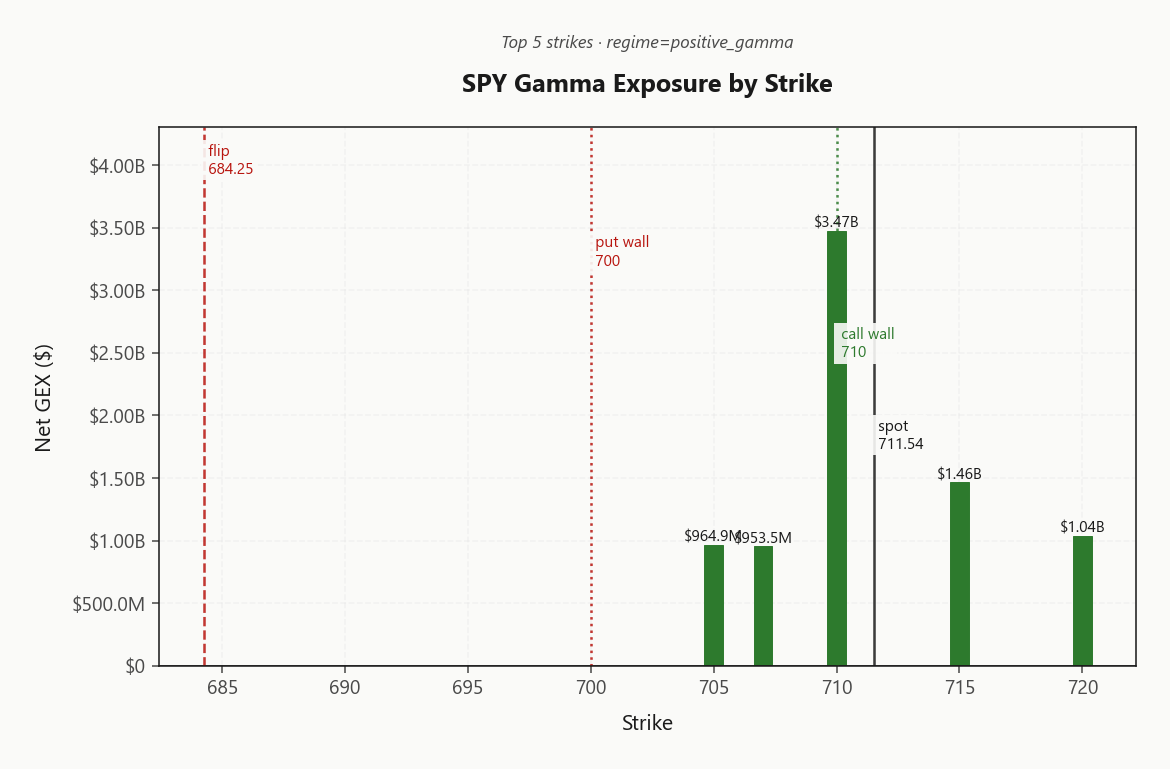

SPY at 711.54 in a Positive Gamma regime with net GEX at $13.11B - dealers are firmly long gamma. Call wall at 710.00 is the ceiling, put wall at 700.00 the nearby floor, gamma flip at 684.25 - spot is deep into the cushion zone so mean-reversion dominates. On a dip, dealers buy $13.11B notional, keeping selloffs shallow. Vanna exposure at -$256B is the tail risk - a vol spike forces dealers to sell delta, amplifying any break below the put wall. VIX at 17.42 in Contango from 15.12 to 20.41, with VVIX at 94.19 confirming no jump-risk premium. VRP at -6.88% means IV is actually below recent realized - options are cheap despite the calm tape. Preferred structure: Iron Condor in the 30-45 DTE bucket - fade into walls, do not chase breakouts.

Positive gamma + Contango - fade rallies into 710.00 wall

Iran ceasefire optimism has pushed the index complex sharply higher, compressing VIX to 17.42 while the full term structure stays in Contango. All three index ETFs sit in Positive Gamma territory well above their gamma flips - dealer hedging flow is dampening moves and pinning price near the call walls. The paradox: negative VRP (-6.88%) says options are cheap to recent realized vol, so the suppressive gamma overlay may be masking unresolved volatility.

Regime Assessment

The vol regime sits squarely at Elevated / Watchful with VIX at 17.42 - watchful, not crisis. Near-term panic probability is negligible: the synchronized positive gamma cushion across SPY, QQQ, and IWM is doing exactly what it should, absorbing intraday impulses before they cascade. Ceasefire euphoria has compressed front-end vol aggressively, but the regime half-life at 15 sessions argues against assuming a clean reversion to calm - elevated regimes are sticky by nature, and this one carries residual geopolitical optionality that the back-end of the curve still prices.

The medium-term path to a low-vol regime is conditional on Iran peace actually materializing beyond headlines. If it does, expect a grinding compression rather than a snap lower in vol - the contango structure already reflects that base case. If it doesn't, the vanna exposure dormant beneath the positive gamma overlay reactivates fast. Position for the grind, hedge the gap: Iron Condor in the 30-45 DTE window captures the carry while the regime persists.

What it means for your trading

Regime is Elevated / Watchful with a half-life of 15 sessions - sticky enough to trade around but not permanent. Fade into walls, do not chase, and treat the gamma flip as the hard invalidation level where the entire dealer support framework reverses.

Trading readVIX and VVIX declining together confirms orderly vol compression - no divergence. SKEW stable says tail pricing is unchanged despite the rally. MOVE subdued means bond market is not adding stress. All macro vol indicators are confirming each other: calm, ordered - the risk is that this consensus is exactly what precedes a surprise.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The full VIX curve sits in Steep Contango from 15.12 out to 22.49, with spot VIX at 17.42 carving a steep slope through the belly. Near-term IV has been crushed by the ceasefire bid while back-end tenors remain stubbornly elevated - the curve is granting a reprieve, not an all-clear. Forward vol between the front-month and mid-curve nodes is rising steeply, pricing residual geopolitical optionality that the spot tape has already discounted.

That divergence is the trade: Steep contango - vol sellers favored. Front-month sellers capture the widest carry roll-down where IV compression is most aggressive relative to term structure slope, while back-end longs warehouse tail protection at a fraction of the front's theta bleed. The optimal DTE bucket is 30-45 - far enough past the weekly to harvest contango decay, close enough to avoid the sticky elevated vol in the belly.

Critically, 20.41 and 22.49 staying bid while the front collapses tells you the market expects this calm is temporary. If peace headlines hold, the back-end converges lower and calendar sellers win on both legs. If they don't, the back-end was right all along - and your long wing absorbs the shock.

What it means for your trading

The VIX term structure in Contango with a Steep Contango profile favors front-month premium harvesting in the 30-45 DTE window, where carry roll-down is steepest - but the elevated back-end signals the curve is not endorsing sustained calm, making back-month tail longs a necessary counterweight.

Trading readFull contango from VIX9D through VIX6M - the carry trade is alive and the market is not pricing near-term stress. The steep near-slope says short-dated vol is aggressively cheap relative to the curve, which either means the market is right about calm or is about to get caught offsides if headlines shift.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

VRP is negative across the index complex at -6.88% for SPY - implied vol at 12.61% has been crushed well below trailing realized at 19.49, a historically rare setup where sellers are not getting paid above realized. The ceasefire bid repriced IV aggressively lower while daily ranges from recent turbulence remain embedded in the lookback window. The IV/RV spread assessment reads Danger Zone.

QQQ carries even wider negative VRP at -7.31% - tech vol compression is the most aggressive across the complex. Short-lookback RV at 7.06 is already collapsing below the longer-window print at 19.49, but convergence with compressed IV is incomplete. If realized continues to fade, the VRP gap closes and short vol wins retroactively; if elevated ranges reassert, vol buyers hold a rare edge at these levels.

What it means for your trading

Negative VRP at -6.88% with IV/RV spreads in Danger Zone territory means premium sellers lack their usual cushion - favor defined-risk structures over naked short vol until realized converges lower or IV reprices higher.

Skew Convexity

SPY quarter-delta put skew prints 2.36% with a smile ratio of 1.29% - orderly, not panic-bid. Put wing IV at 10.62% versus ATM at 9.28% reflects institutional programs rolling protection, not fear-driven demand for downside convexity. The surface reads as programmatic hedge maintenance, consistent with a Positive Gamma regime where dealers are already long gamma.

Across the complex, QQQ carries steeper skew at 2.87%, pricing the concentration risk that persists even in a broad relief rally - tech's higher beta demands a richer put wing. IWM sits flattest at 1.63%, with small-cap downside the least actively hedged corner of the book. Call wing IV compressed to 8.26% on SPY confirms what the tape already shows: this move is short-covering and gamma-driven, not new call-buying conviction.

Favor put spreads over naked puts - the orderly smile shape makes verticals more capital-efficient, and the positive gamma overlay argues against paying up for standalone convexity.

What it means for your trading

Skew surface is orderly across the index complex - institutional hedging, not fear - with QQQ's steeper profile flagging residual tech concentration risk while compressed call wings confirm no upside conviction in the options market.

Vol-of-Vol Structure

VVIX at 94.19 sits squarely in Normal territory - the options-on-options market is pricing no jump-risk premium and no bimodal outcome distribution despite the geopolitical headline cycle. Vol-of-vol is declining in lockstep with VIX at 17.42, confirming the compression is orderly rather than a vol-selling trap building toward a snap-back. When VVIX diverges higher while VIX falls, that flags hidden convexity demand; the current parallel move says the marketplace genuinely believes near-term realized paths are narrow.

The VVIX/VIX ratio is unremarkable - no regime-break signal, no elevated kurtosis bid, just steady-state grinding. This reading directly supports Standard Size across premium-selling structures: iron condors and short strangles carry no outsized gamma blowup risk at these levels. Traders who would normally halve notional when VVIX prints elevated or extreme readings can deploy full standard size here. The vol surface is telling you the distribution is Gaussian enough to trust your Greeks - lean into the positive gamma cushion without hedging for a tail that the market itself refuses to price.

What it means for your trading

VVIX at 94.19 confirms Normal vol-of-vol with no jump-risk premium - Standard Size is appropriate for iron condors and premium-selling structures without tail-risk reduction.

Dispersion Spread

Dispersion is compressed and staying that way. Every mega-cap mover - AAPL, MSFT, AMZN, TSLA, GOOGL - posted positive GEX shifts in lockstep with the index, pushing implied correlation higher and single-name vol spreads tighter. Cross-expiry IV dispersion at 3.14 with cross-strike dispersion at 81.75 confirms the regime: constituents are trading as a bloc, not as individual stories. When the entire cap-weighted complex aligns in Positive Gamma, index vol selling is structurally cleaner than single-name premium harvesting.

SPY ATM IV at 12.61% sits at moderate spread to QQQ (16.29%) and IWM (19.21%) - no extreme richness or cheapness across the complex favors index-level structures over name-picking. Prefer SPX iron condors here; the correlated gamma overlay means idiosyncratic blowups are unlikely to offset index pin action.

The exception to watch: TSLA. Its higher idiosyncratic vol profile makes it the most likely candidate to break correlation first - any divergence there is an early warning that the dispersion compression is unwinding.

What it means for your trading

Mega-cap gamma alignment suppresses dispersion and elevates implied correlation - index vol selling via Iron Condor in 30-45 DTE is preferred over single-name premium strategies until TSLA or another high-beta constituent breaks rank.

Liquidity & Microstructure

The tape is pinned. Massive open interest concentration at 710.00 carries $3.47B in net GEX - the single largest gamma node in the book and the mechanical ceiling for today's session. Dealers are short calls at that strike; every tick above triggers delta selling that caps the advance. The put wall at 700.00 defines the nearby floor, creating a tight corridor where mean-reversion flow dominates.

The gamma flip at 684.25 sits deep below spot, confirming this positive gamma regime is entrenched - not marginal. QQQ mirrors the setup, pinned near its own 650.00 call wall with the flip at 635.97. Cross-index alignment means no divergence trade; dampening is uniform across the complex.

Notably, the highest OI strike at 600 remains far below spot - legacy protective structures from earlier stress that have not been unwound. As charm erodes those positions, expect gradual delta release adding mild selling pressure into the close.

What it means for your trading

Dealer gamma is deeply suppressive with the call wall acting as a hard ceiling and the gamma flip far enough below spot that only a material catalyst can flip the regime - fade strength into 710.00 and treat 684.25 as the invalidation level where hedging flow reverses from dampening to amplifying.

Trading readMassive positive gamma clustered at the call wall creates a hard ceiling - dealers mechanically sell into any push higher, making breakouts fail until positioning shifts. Below the gamma flip, the profile inverts and dealers amplify rather than dampen. Trade the range between put wall and call wall; the edges are walls, not targets.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Vanna dominates the greek risk stack. Net VEX at -$256B is massively negative - if VIX rips from 17.42, dealers are forced to sell delta at scale, converting today's suppressive cushion into a mechanical accelerant. As long as vol stays compressed under the Contango curve, that exposure remains dormant. A vol spike flips the entire framework.

Charm at -$26.3M is modestly negative - mild directional selling pressure into the close, not a dominant force. The charm pivot sits at 710, coincident with the call wall, carrying a Neutral bias. Spot hovering just above that line puts charm flow direction on a knife-edge: any drift lower through the pivot flips charm from headwind to tailwind.

The convergence of gamma, charm, and vanna flows at 710.00 makes it the single most consequential level on the board. Fade into it - do not press through. The regime holds until vol breaks the spell.

What it means for your trading

Vanna at -$256B is conditionally hostile - dormant while vol stays compressed, destructive if VIX spikes. Charm pivot at 710 aligns with the call wall, making it the fulcrum where all dealer greeks converge and the level to fade.

Cross-Asset Confirmation

Cross-asset gamma alignment is complete: SPY, QQQ at 649.38, and IWM at 277.24 all sit in Positive Gamma territory with regime divergence Aligned. Synchronized dealer dampening across the index complex compresses realized ranges and reinforces the pin - no divergence trade exists today.

The MOVE index at 65.89 confirms the bond market is not compounding equity risk - this is a geopolitical relief rally, not a credit event. Fear & Greed at 69 (Greed) is approaching contrarian pullback territory but not yet extreme enough to fade outright. Another strong session pushes into the zone where historical reversal rates spike.

When all three indices dampen simultaneously on a single catalyst, the tape mean-reverts within sessions - the ceasefire bid is broad but shallow. IWM carries the thinnest absolute gamma cushion and breaks first if the narrative shifts. Treat this as range-bound until a regime crack emerges.

What it means for your trading

Uniform Positive Gamma across SPY, QQQ, and IWM with MOVE subdued at 65.89 removes cross-asset stress from the equation, but Fear & Greed at 69 (Greed) warrants contrarian caution on another leg higher - relief rallies on geopolitical de-escalation historically mean-revert, not trend.

Scenario EV

Iron Condor leads the structure screen at 47 - a moderate conviction score that reflects the core tension: positive gamma pins the tape in a tradeable range, but negative VRP (-6.88%) means the premium you collect is thin relative to recent realized moves. No structure scores decisively well here; iron condors win by staying delta-neutral inside walls that dealers are actively defending, harvesting whatever edge the range-bound regime offers without taking a directional view the tape will punish.

Put spreads trail at 33 - directional downside bets carry poor expected value when dealers are mechanically buying every dip above 684.25. The DTE sweet spot sits at 30-45 days, pushing past front-week to capture the steepest segment of the Contango roll-down from 15.12 toward 20.41. VVIX at 94.19 reads Normal - Standard Size applies, no need to haircut for jump risk.

What it means for your trading

Iron condors in the 30-45-day bucket offer the highest-EV structure at 47, anchored between the 710.00 ceiling and 700.00 floor - size normally per Normal VVIX, but respect that negative VRP compresses the premium cushion.

Actionable Summary

An Aligned index complex in Elevated / Watchful territory with steep Contango and net GEX at $13.11B sets up the preferred trade: Iron Condor in the 30-45 DTE bucket, centered near the charm pivot at 710. Fade strength into the 710.00 call wall - dealers mechanically cap upside - and lean on 700.00 as the nearby floor. Do not chase this rally above the wall.

Negative VRP at -6.88% means naked short vol is uncompensated - use spreads exclusively. The Contango curve from 15.12 through 20.41 funds the carry, but only inside defined-risk wrappers. VVIX at 94.19 confirms Standard Size sizing - no jump-risk premium to hedge around.

Regime invalidation:684.25 is the line. A close below flips dealer flow from supportive to hostile. The dormant risk is vanna at -$256B - a vol spike activates delta selling at scale, unwinding the entire cushion.

What it means for your trading

Sell Iron Condor spreads in 30-45 DTE near the 710 charm pivot, fading into the 710.00 call wall - invalidation is a close below 684.25, where the positive gamma thesis reverses and vanna becomes the dominant force.

Direct catalyst for today's rally - Hormuz Strait reopening removes the oil supply disruption premium that had been elevating cross-asset vol and geopolitical risk premia.

Tension between Hormuz reopening and continued blockade rhetoric creates headline whipsaw risk - the market is pricing peace but policy is still confrontational.

Hedge fund buying surge on peace hopes quantifies the positioning shift behind today's positive gamma expansion across mega-caps - this is the flow that built the call walls.

European oil majors outperforming US peers on the conflict trade is a sector rotation signal - energy dispersion matters for single-name vol sellers picking names.

Gold strength alongside an equity rally is unusual - continued safe-haven bid suggests the market is hedging the ceasefire optimism rather than fully trusting it.

Supply chain cost pressures from the conflict are real-economy drags that persist even if a deal is reached - watch for earnings impact in coming quarters.

EM equity strength on peace deal hopes shows this is a global risk-on repricing, not just a US event - confirms the cross-asset aligned regime read.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.43 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 684.25 against a spot of 711.54. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.61% with a volatility risk premium of -6.88%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.42. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime