Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

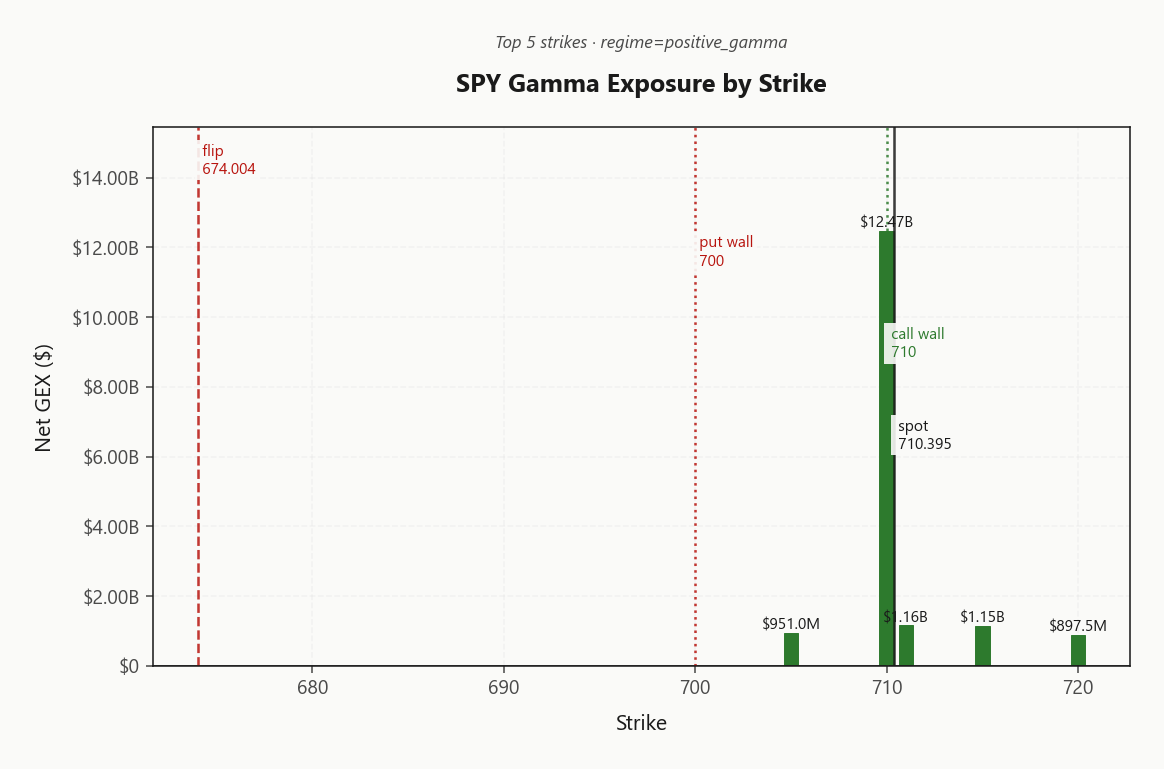

SPY closes at 710.40, firmly in Positive Gamma with net GEX at $20.29B - dealers are heavily long gamma and will absorb moves in both directions. Call wall sits at 710.00 acting as a ceiling, with put wall support at 700.00 and gamma flip well below at 674.00 - spot is deep above the flip, giving substantial cushion before a regime change. Dealers are long delta via $156.07B but short vanna at -$237.93B, meaning a vol spike would force aggressive delta selling - the supportive positioning is contingent on vol staying suppressed. VIX at 17.51 with the term structure in Contango - VIX9D at 14.83 versus VIX3M at 20.54 confirms steep carry. VRP is deeply negative at -7.03% - options are cheap to recent realized moves, so premium sellers aren't getting paid much. VVIX at 94.95 is normal range with sizing guidance Standard Size. Bottom line: the tape is pinned and dampened at the call wall - fade rallies above 710.00, buy dips toward 700.00, avoid chasing while gamma is this thick.

Iran's Hormuz opening triggered a broad risk rally, but SPY has run straight into its call wall at 710.00 where dealers sit on massive positive gamma of $20.29B. The VIX term structure is in Contango with VIX at 17.51, confirming the market is pricing de-escalation as base case - but trailing realized vol still dwarfs current implied at -7.03%, meaning this calm is fragile if headlines reverse.

Regime Assessment

Vol regime sits at Elevated - classified Elevated / Watchful - with VIX at 17.51 compressing on Iran de-escalation but still above the low-vol threshold. The regime half-life of 15 sessions makes this sticky enough to lean into but not so entrenched that transition risk can be ignored.

Near-term tail risk is contained: panic-spike probability over the next few sessions prints at just 0.05, while the probability of transitioning to low-vol within a broader window registers 0.45 - a meaningful path if the Hormuz narrative holds. The critical distinction is whether this is elevated and falling (constructive for carry) or elevated and coiling before the next spike. Steep Contango across the VIX curve and Aligned cross-asset gamma regimes favor the former, but Iran headline optionality keeps the latter on the table.

Position for compression with defined risk - the regime supports range structures but demands tail awareness given the geopolitical conditionality embedded in every vol metric.

What it means for your trading

Regime Elevated with a half-life of 15 sessions favors carry trades tilted short vol, but the path from here is binary on Iran - lean into compression via defined-risk structures while maintaining tail hedges for the re-escalation scenario that would invert the curve and flip dealer positioning hostile.

Trading readVIX and VVIX declining together - orderly de-escalation with no hidden fear divergence. SKEW holding steady means institutional tail hedges remain in place despite the rally - hedgers haven't removed their puts. MOVE is subdued, confirming no rates or credit stress. The setup (VIX falling, SKEW stable) is healthy and sustainable until it isn't.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

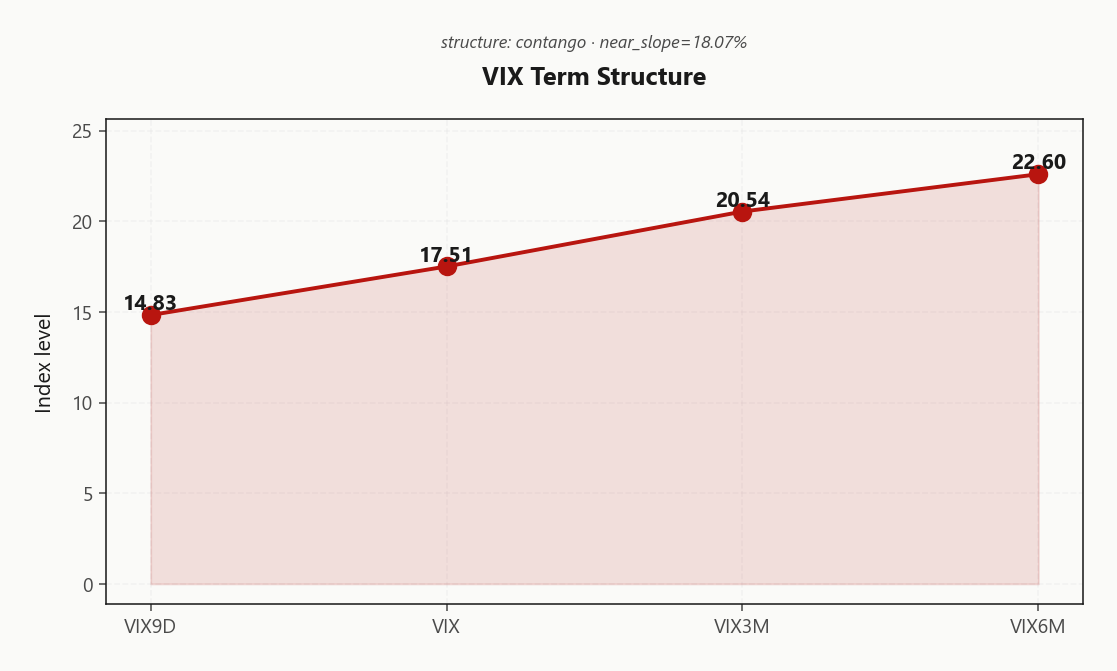

Forward Vol Geometry

The VIX curve is in steep Contango - front-end vol crushed on Hormuz de-escalation while the back end refuses to follow. VIX9D at 14.83 anchors the low end, extreme suppression reflecting a market that has fully priced ceasefire into near-dated options. VIX3M at 20.54 and VIX6M at 22.60 remain elevated - lingering geopolitical tail premium the front has entirely shed. The near slope prints at 18.07%%, confirming this is not a gentle roll but an aggressive step-up.

Forward vol regime is Steep Contango - Steep contango - vol sellers favored. Implied forwards between the intermediate tenors sit well above spot VIX at 17.51, signaling the market expects vol to re-expand from here, not compress further. Best expression: sell front-month against owning the belly to capture roll-down and convexity protection simultaneously.

VIX futures reinforce the picture - front month at 20.51 trades at a 17.13%% premium to spot. That basis is wide enough to fund calendar structures but fragile enough to collapse on a single Hormuz headline reversal. The steepness of this curve is a direct measure of how much capital is riding on de-escalation holding.

What it means for your trading

Steep contango with VIX9D at 14.83 and VIX3M at 20.54 prices de-escalation as base case while embedding re-expansion risk in the belly - sell front-month vol against intermediate tenors for maximum roll-down, but size for rapid curve inversion on any Hormuz reversal.

Trading readClassic steep contango - front-end vol collapsed on de-escalation while back end holds premium. The vol carry trade is alive via short-dated structures, but contango also signals the market expects vol to re-expand from here. Any ceasefire reversal would flatten or invert this curve within hours - the steepness is a measure of how much is riding on the Hormuz narrative holding.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

ATM IV at 12.33% has collapsed below trailing realized at 19.36, producing deeply negative VRP of -7.03%. The IV-RV spread sits in Danger Zone territory - the surface is pricing de-escalation as fait accompli while rolling windows still embed war-period variance. QQQ shows an even wider dislocation at -7.27%, confirming tech vol was crushed most aggressively on the Hormuz bid.

The RV term structure reveals the convergence mechanics: short-window realized at 6.27 has already collapsed below ATM implied, while the trailing window at 19.36 remains elevated as older high-vol sessions roll off. The gap is closing from the realized side - if de-escalation holds, normalization accelerates and the negative VRP self-corrects. If headlines reverse, IV is mispriced low and long gamma captures the re-expansion.

Premium sellers face thin edge: short vol below fair realized, dependent entirely on gamma support rather than VRP harvest. Favor long gamma where theta offsets via contango roll-down, or stand aside until realized decays toward the surface.

What it means for your trading

VRP deeply negative at -7.03% with IV-RV spreads in Danger Zone - options are cheap to realized and premium selling lacks edge until trailing RV at 19.36 decays toward ATM IV at 12.33%. Short-window realized at 6.27 confirms convergence is underway from the RV side, favoring long gamma or contango structures over outright short vol.

Skew Convexity

SPY quarter-delta put skew at 2.4% with a smile ratio of 1.3% reads as institutional hedging on autopilot - puts bid above calls by a standard margin, not a panic premium. Quarter-delta puts print at 10.37% against ATM at 8.85% and quarter-delta calls at 7.97% - the call wing is flat, confirming no aggressive upside conviction despite the Iran relief bid.

QQQ skew runs steeper at 2.79%, reflecting heavier relative demand for tech downside protection even as the surface narrative is de-escalation. Tail convexity at -0.06 shows far-wing steepness is not accelerating - smart money is maintaining existing hedges, not layering fresh tail protection. The smile is orderly and symmetrically fading into the wings.

Given moderate steepness without convexity acceleration, put spreads dominate outright puts on capital efficiency. Sell the belly, own the wing - skew is pricing enough to make spreads cheap without signaling dislocation.

What it means for your trading

Quarter-delta skew is moderate at 2.4% with flat tail convexity at -0.06 - hedges are maintained, not expanded. QQQ's steeper skew at 2.79% flags tech as the preferred vehicle for downside protection via put spreads.

Vol-of-Vol Structure

VVIX at 94.95 against VIX at 17.51 puts the ratio at 5.42 - squarely Normal territory with no jump-risk premium embedded. The options-on-options market is confirming the de-escalation narrative outright: if smart money feared a binary reversal on Hormuz headlines, VVIX would be diverging higher even as VIX compressed. It isn't. Both are declining in lockstep - orderly, not complacent.

That co-movement matters. A falling VIX paired with sticky or rising VVIX is the classic tell for hidden tail fear beneath a calm surface. The absence of that divergence here gives vol sellers a cleaner signal than the headline VIX alone provides. Sizing guidance is Standard Size - full position sizes are warranted across the vol complex without half-sizing or convexity overlays.

Caveat: normal vol-of-vol in an active geopolitical backdrop is itself a fragile consensus. Any ceasefire rupture re-prices VVIX before VIX moves - monitor the ratio for early divergence as the leading indicator of regime stress.

What it means for your trading

Vol-of-vol is Normal with VVIX and VIX declining together, confirming orderly de-escalation rather than complacent bottoming - Standard Size positioning is appropriate, but watch the VVIX/VIX ratio at 5.42 for any divergence that would signal hidden fear re-emerging ahead of headline VIX.

Dispersion Spread

The de-escalation rally is a correlation event - all five top mega-cap movers (TSLA, AAPL, NVDA, AMZN, GOOGL) printed positive GEX shifts in lockstep, compressing single-stock vol alongside index vol and driving implied correlation sharply higher. SPY ATM IV sits at 12.33% with cross-expiry dispersion registering just 3.12, confirming the term structure is tightly packed - the market is pricing one narrative across all tenors. Cross-strike dispersion at 80.24 tells a different story: the smile is steep even as the level is crushed, meaning wing demand persists beneath a placid surface.

In this correlated regime, index premium selling via SPY/SPX is structurally preferred over single-name - you harvest the elevated correlation without absorbing idiosyncratic earnings risk from any individual mega-cap. The key forward question: as Hormuz de-escalation becomes consensus, macro correlation should decay and stock-pickers will start differentiating. Watch cross-expiry dispersion for the first signs of widening - that is the signal that dispersion trades are repricing and the index-over-single-name edge is fading.

What it means for your trading

Compressed cross-expiry dispersion at 3.12 with elevated cross-strike dispersion at 80.24 defines a correlated-but-hedged surface - favor index structures over single-name until dispersion widens on narrative fragmentation.

Liquidity & Microstructure

Spot is pinned directly on the dominant gamma cluster at 710.00, which alone concentrates $12.47B in dealer gamma - the majority of total net GEX at $20.29B. The call wall at 710.00 converges with this strike, creating a hard ceiling where dealers will aggressively sell any push higher. The put wall at 700.00 provides gravitational support on pullbacks, defining a tight dampening corridor for the tape.

The gamma flip sits well below at 674.00, giving deep positive-gamma cushion - the regime will not flip absent a multi-percent drawdown. Highest OI at 600 reflects legacy positioning from the prior range, now irrelevant to current dynamics. Critically, zero-DTE flows account for 67.3% of total GEX, making intraday gamma the primary microstructural force - but that cushion rolls off entirely at the close, leaving overnight gap risk materially elevated relative to intraday.

What it means for your trading

Dealer gamma is overwhelmingly concentrated at the call wall - spot is mechanically pinned until a catalyst strong enough to overwhelm $20.29B in suppressive GEX emerges, but zero-DTE dominance at 67.3% of total means Monday's open resets with a materially thinner cushion.

Trading readGamma is dominated by a single massive cluster at the call wall - spot is pinned directly on top, meaning dealers will aggressively sell any push higher and buy any dip from here. This is a high-conviction mean-reversion setup: trade the range between call wall and put wall, fading any breakout attempt until a catalyst strong enough to overwhelm this gamma concentration emerges.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Dealers are short massive vanna at -$237.93B - the single most consequential greek in the book tonight. While Positive Gamma keeps spot dampened around the 710.00 call wall, the vanna channel runs in the opposite direction: any vol spike forces aggressive delta selling as dealers scramble to re-hedge short vanna into a rising-IV tape. Net GEX of $20.29B buys you time in an orderly tape - it does not buy you protection in a headline shock where implied rips higher on an Iran reversal.

Charm adds a modest directional lean via net CHEX at -$1.1B, translating to mild mechanical selling pressure into each close. The charm pivot sits at 710 - a Call Wall convergence - with spot Neutral relative to that level at just -0.0556028688 away. That convergence pins the late-day hedging flow squarely at the call wall, reinforcing the ceiling rather than offering directional drift.

The regime tension is binary: calm tapes stay dampened under thick gamma, but a vol event activates the vanna accelerant and flips dealer flow from supportive to hostile. Monitor VIX at 17.51 and the term structure in Contango - any flattening is the early warning that vanna is about to overwhelm gamma.

What it means for your trading

Gamma suppresses realized moves while vol stays low, but deeply negative vanna at -$237.93B means any vol expansion triggers cascading dealer delta selling - the positioning is conditionally stable, not unconditionally safe. Charm pivot convergence at the Call Wall reinforces the 710.00 ceiling into the close.

Cross-Asset Confirmation

Cross-asset gamma regimes are fully Aligned - SPY, QQQ, and IWM all hold positive gamma with spot above their respective flips, confirming broad risk-on participation across the cap spectrum. When all three indices print the same regime simultaneously, rotational divergence signals go silent and the dominant read is structural: dealer hedging flows enforce mean-reversion uniformly, leaving no weak link for directional capital to exploit. SPX closed at 7126.06, up 1.2%% on the session, with QQQ at 649.03 and IWM at 275.93 tracking in lockstep - the Iran de-escalation bid was indiscriminate.

MOVE at 65.89 confirms the rates complex is not transmitting stress - this is a geopolitical event normalizing, not a credit dislocation unwinding. The absence of fixed-income contagion narrows the vol re-expansion catalyst set to pure headline risk. Fear & Greed sits at 68 (Greed) - elevated but not yet extreme, leaving room for continuation before contrarian positioning becomes warranted. VIX in negative gamma remains the mirror: any reversal self-amplifies through the vol complex while equities stay mechanically dampened.

What it means for your trading

Full regime alignment across SPY, QQQ, and IWM with MOVE subdued and sentiment in Greed territory validates the de-escalation thesis - the tape is structurally range-bound and mean-reverting until a catalyst forces regime divergence or pushes sentiment into extreme territory.

Scenario EV

The tape favors Iron Condor - scoring 39 - but conviction is moderate, not screaming. Positive gamma pins spot between the 710.00 call wall and 700.00 put wall, mechanically enforcing the range short-premium structures require. The catch: VRP reads Unknown, meaning you are selling options cheap to trailing realized. Edge here is structural - dealer gamma keeping spot range-bound - not vol premium harvest.

Target the 30-45-day window where contango steepness maximizes roll-down through the belly of the term structure. VVIX at 94.95 confirms Normal vol-of-vol - sizing guidance is Standard Size, no scaling required. Put spreads score 25 against the condor's 39 - downside demand is orderly, reducing standalone hedge payoff. Center wings around the call wall and put wall where dealer gamma concentration enforces mean-reversion.

What it means for your trading

Gamma support justifies the Iron Condor at Standard Size position size, but thin VRP means edge comes from range enforcement, not premium - fade the wings, respect the 674.00 flip as the regime invalidation level.

Actionable Summary

Trade: Iron Condor in the 30-45-day window, centered on the charm pivot at 710 where call-wall convergence anchors the book. Positive gamma at $20.29B mechanically dampens moves in both directions, and steep Contango delivers roll-down edge through the belly - but VRP at -7.03% means premium is thin, so the carry comes from structure, not from selling rich vol. Use the 710.00 call wall and 700.00 put wall as wing references.

Avoid naked short puts. Vanna exposure at -$237.93B is deeply negative - any vol shock cascades through dealer delta selling and overwhelms the gamma cushion. Spread protection only; the Iran de-escalation narrative is priced but not locked.

Watch 674.00 as the regime line in the sand. Spot sits well above with deep cushion, but a breach flips dealers from supportive to hostile. Regime reads Elevated / Watchful - favor range structures, fade breakouts, keep tail hedges live.

What it means for your trading

Pin spot at the 710.00 call wall with Iron Condor structures while the Elevated / Watchful regime and steep contango persist - but size for vanna fragility and defend the 674.00 gamma flip as the hard stop on the thesis.

THE session catalyst - Iran declaring Hormuz open removes the single biggest energy supply risk, directly compressing oil premia and vol, driving the equity rally into the call wall.

Bank earnings confirming financial resilience through the Iran war reduces credit contagion fears - this is a geopolitical event, not a financial crisis, which matters for how vol mean-reverts.

Significant US-Iran differences remaining, including on nuclear issues, is the tail risk keeping back-end vol elevated and preventing the VIX curve from flattening - this is why contango persists.

Quantified oil supply disruption frames the macro backdrop for energy vol and inflation expectations - if supply normalizes, another leg of vol compression is coming across the complex.

Trump constraining Israeli action in Lebanon broadens the de-escalation narrative beyond Iran bilateral - reduces probability of conflict re-escalation from a third-party trigger.

Contradicting the Hormuz rally, Trump confirming blockade remains until a deal suggests de-escalation is conditional - headline risk persists and supports maintaining tail hedges.

Equity fund inflows on de-escalation hopes confirm institutional money is re-risking, not just short covering - real money flow validates the positive gamma build across the complex.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 17.47 with a Contango term structure. The Fear & Greed index reads Greed, and cross-asset volatility is Aligned across SPY, QQQ, and IWM.

SPY's gamma flip is at 674.00 against a spot of 710.40. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 12.33% with a volatility risk premium of -7.03%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in Contango with VIX at 17.51. Contango signals benign forward expectations; backwardation signals near-term stress.

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime