Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

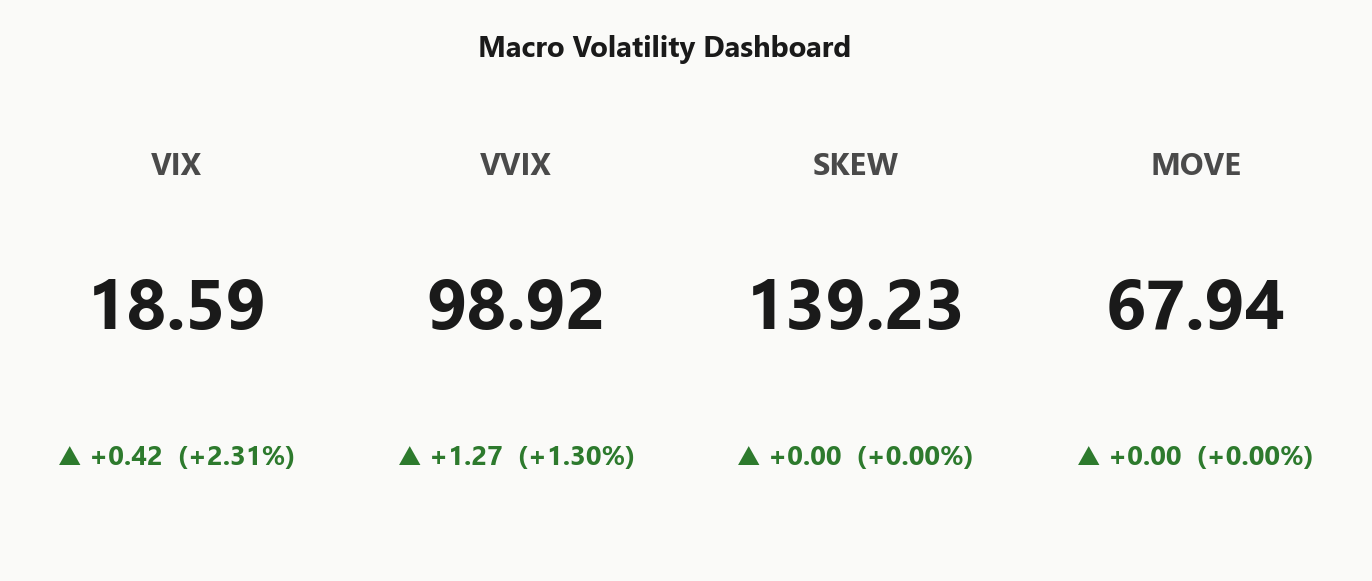

Positive gamma on SPY/IWM, QQQ below flip — divergence is today's tell, with VIX in contango

SPY and IWM sit in positive gamma with spot hugging the call wall at 700.00, while QQQ has slipped below its gamma flip at 636.04 — a regime split that is the day's lead signal. VIX term structure in contango with VVIX at 98.92 leaves vol sellers paid, and VRP negative across the complex (-4.16%) says options are cheap to realized. Iran de-escalation hopes are driving the tape, but oil and MOVE remain the tell for whether the rally has legs.

Regime Assessment

The tape is in a Elevated / Watchful regime with VIX at 18.59 — elevated enough to keep hedgers honest, but nowhere near stress. The transition math matters more than the level: half-life of 15 sessions says this state is sticky, not entrenched, and it will not flip on a single headline.

Path probabilities skew to the upside for vol sellers. Panic transition over the next week sits at — — a tail, not a base case — while the odds of reverting to a low-vol regime over two weeks run —. Clean Iran de-escalation is the asymmetric catalyst: it compresses VIX, crushes the belly of the curve, and pays carry trades already aligned with the steep_contango term structure.

The binary cuts both ways. Nuclear and Hormuz remain unpriced tails, so carry a cheap front-month VIX call against the short-vol book. Current regime elevated is the anchor; spot above SPY's flip at 694.54 is the confirmation.

What it means for your trading

Regime is Elevated / Watchful and sticky — vol sellers have the structural edge with low panic risk (—) and meaningful mean-reversion probability (—), but the Iran binary demands a tail hedge on top of the carry.

Trading readVIX, VVIX, SKEW, MOVE all in confirming ranges — no divergence warning yet. But SKEW elevated with MOVE calm is the combo to watch: means equity hedging is active while bond market isn't buying the stress story, which is an unstable equilibrium.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

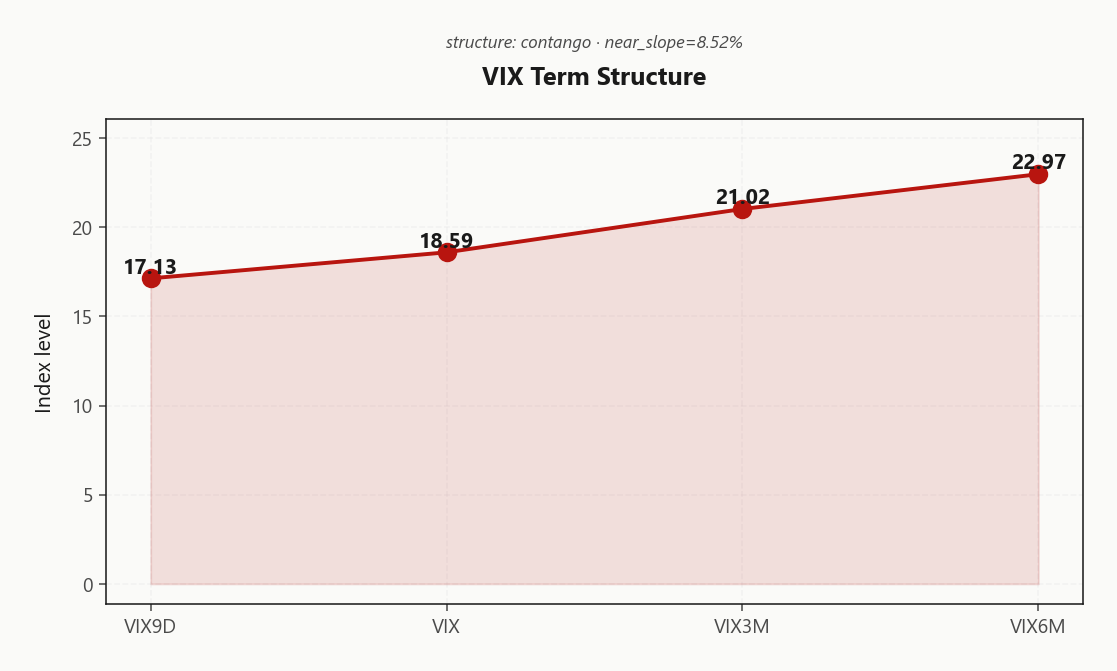

Term structure is in contango with VIX9D at 17.13 printing below spot VIX at 18.59 — the front is clean, no event premium packed into the near wing. VIX3M at 21.02 and VIX6M at 22.97 stack the curve upward, anchoring the longer-dated bid and confirming a near slope of 8.52%%.

Forward vol does the talking: the 30→60 segment lifts to 22.1351880498 and 60→90 climbs to 24.7669416764, materially richer than spot. That is where carry lives. Regime reads steep_contango — Steep contango — vol sellers favored — and the structural short-vol trade is paid so long as the front stays orderly.

Edge sits in the belly. Selling the 30-45 DTE window captures the steepest forward-vol premium without buying weekly event risk or paying up for the longer-dated hedge bid. Weeklies are too clean to sell, the wings are too bid to fade — the middle of the curve is the trade.

What it means for your trading

Curve is in steep_contango with forward vol climbing materially from spot — the 30-45 DTE belly is where short-vol carry is richest relative to realized event risk.

Trading readSteep contango with front below spot VIX = no near-term event stress, vol sellers' carry is live. But the curve's upward slope means forward vol is being paid — the 30-45 DTE belly is where the carry trade belongs, not the front week.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

Realized is the louder tape today. SPY 19.28 HV20 is running above ATM IV 15.12%, pushing VRP to -4.16% and pinning the IV/RV spread in danger_zone territory. Shorter-window RV at 9.82 has cooled versus the 19.28 twenty-day print, but the belly of the distribution still sits above what the tape is charging for optionality.

QQQ carries the hottest burn — VRP -3.91% against ATM 19.68%, with tech realized doing most of the work on the index complex. IWM is the cleanest fit to fair, VRP -2.1% against ATM 21.54% — small-caps are where short premium gets paid without fighting the realized tape.

Implication: naked short vol is uncompensated here. Defined-risk condors and flies with wings anchored at 700.00 and 697.00 earn the contango carry without taking the realized-vol tail. Favor shorter DTE on QQQ where realized is most likely to decay into implied, longer belly on SPY/IWM where the regime is structurally stickier.

What it means for your trading

Options are cheap to recent realized across the complex, most acutely in QQQ (-3.91%) — sell premium in defined-risk structures only, size shorter DTE where RV mean-reverts fastest.

Skew Convexity

Quarter-delta skew sits at 3.41% with smile ratio 1.22% — downside is bid but ordered, not dislocated. Put-wing IV at 18.85% prints well over ATM at 16.15%, while the call wing at 15.44% sits below ATM — no upside chase priced in despite SPX near records.

Cross-asset, QQQ skew at 4.58% runs wider — tech left tail is bid harder, consistent with QQQ already below its flip. IWM skew at 3.47% is the cheapest left tail in the complex, aligned with small-cap positive gamma. Contango curve leaves downside protection structurally expensive; paying up for naked puts funds the dealer.

Trade expression: put spreads over naked puts, financed by overwriting the flat call wing. Sell the upside into the 700.00 pin; buy the put structure inside realized.

What it means for your trading

Put skew is paying up in an ordered regime while calls sit flat — the efficient expression is put spreads financed by short upside calls, not outright long puts at 18.85%.

Vol-of-Vol Structure

VVIX at 98.92 against VIX 18.59 prints a ratio of — — squarely in the normal band. The vol-of-vol tape is normal: no binary jump premium, no convex repricing embedded in the VIX options complex, and no reason to trim gross. Sizing stays standard_size.

That calm is the trap. VIX ticked +2.31%% on the session and the Iran headline tape remains a binary overhang — interim-deal optimism one tweet away from unwinding. With dealer vanna deeply negative, a VIX gap does not stay contained in the VIX options book; it transmits straight into spot through forced delta selling. The vol-of-vol gauge tells you how the market is currently priced, not how it reprices on a hostile headline.

Carry a cheap VIX call or VXX upside as tail insurance against a vol-of-vol regime break. Do not oversize short-premium just because VVIX is well-behaved — the skew of outcomes into an unresolved geopolitical catalyst is not symmetric.

What it means for your trading

VVIX/VIX at — keeps the regime normal and sizing standard_size, but Iran headline risk argues for layering a cheap VIX call hedge on top.

Dispersion Spread

Single-name vol is trading rich to index across the complex — 19.68% on QQQ against 15.12% on SPY, with IWM splitting the difference at 21.54%. That spread says implied correlation is moderate and dispersion is alive, but with the tape being steered by Iran headlines, idiosyncratic blow-ups remain the live tail even as the macro beta stays coherent.

In that mix, selling index vol beats selling single-name vol. SPX/SPY is the highest-carry, lowest-dispersion leg of the complex and the cleanest expression of the steep_contango carry trade; QQQ sits below its flip at 636.04 and needs tighter wings; single-names carry the full dispersion tail. Iron condor on SPY around the 700.00 / 697.00 band isolates the carry without wearing the name-specific gap risk.

The corollary on hedges: if the tape stays macro-led, index puts will underperform single-name puts dollar-for-dollar as protection. Keep hedges name-specific where beta is cleanest, sell premium at the index level where dispersion is cheapest.

What it means for your trading

QQQ ATM IV at 19.68% rich to SPY 15.12% argues sell index vol, hedge single-name. Iron condor on SPY is the carry seat; name-level puts are the hedge seat.

Liquidity & Microstructure

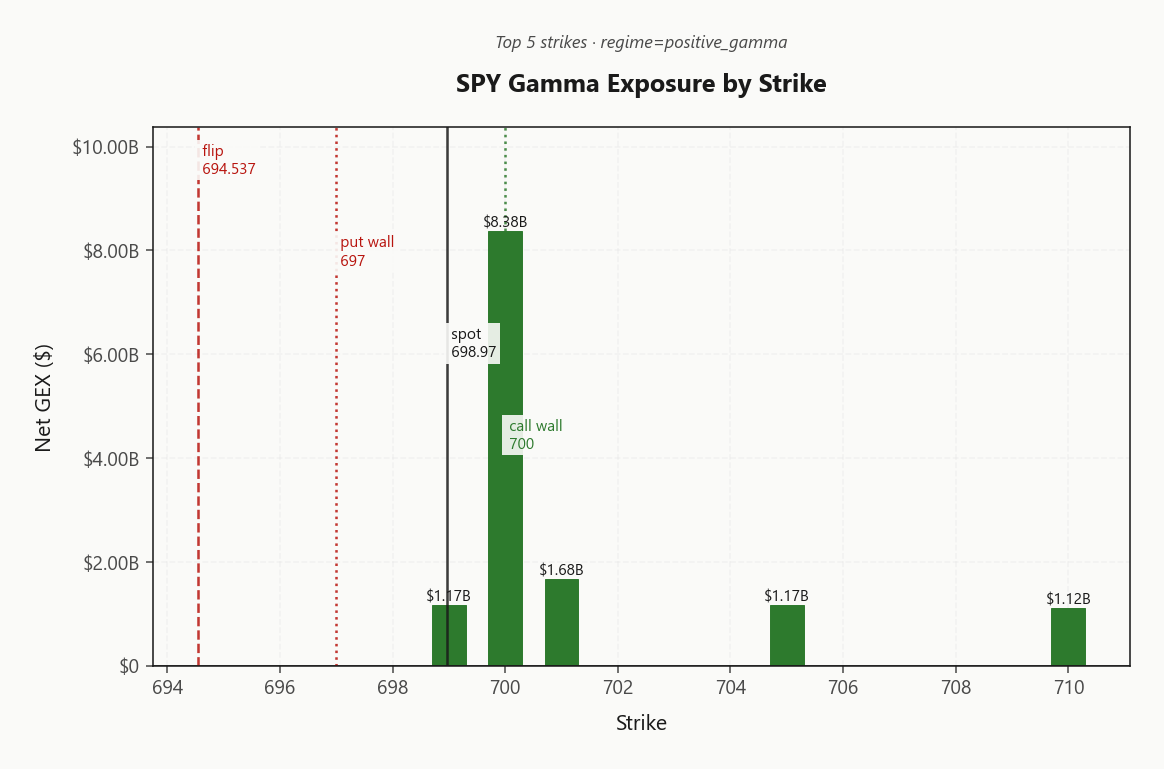

SPY is pinned right under the 700.00 call wall with net GEX massively clustered at 700.00 ($8.38B) — dealers are dampening every push higher and pin risk is the dominant intraday force. The gamma flip at 694.54 is the line in the sand: spot above keeps the mean-reversion machine running, spot below flips the regime to amplification. Max pain at 680.00 adds a structural gravitational pull into the close.

The fragile leg is QQQ, already trading below its flip at 636.04 — that is where any headline-driven break shows up first, and it drags the complex before SPY's own flip is even threatened. Highest OI at 600 is legacy open interest, not today's battleground; the active fight is between the 697.00 floor and the 700.00 ceiling.

Playbook: fade strength into 700.00, fade weakness into 697.00, stop out below 694.54. Watch QQQ's flip as the early-warning tape.

What it means for your trading

SPY is in a dealer-dampened pin between 697.00 and 700.00 with the flip at 694.54 as the regime-change trigger; QQQ below its own flip at 636.04 is the first crack to watch.

Trading readMassive call-wall cluster right overhead says dealers are dampening any push through — fade strength into the wall, and only get aggressive short once spot breaches the flip, where the tape mechanically flips to amplification.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net vanna at -$181.63B is the structural accelerant in the book — deeply negative, meaning any pop in implieds mechanically forces dealer delta lower. With charm at -$1.3B bleeding the same way into the bell, the afternoon carries a built-in sell tilt that sits dormant while spot pins, and goes live the moment vol ticks.

The pivot to watch is the 700 —, currently — away — current bias reads neutral. Above it dealers lean into strength; lose the gamma flip at 694.54 and the regime inverts to amplification, with QQQ already sub-flip at 636.04 as the leading tell.

The asymmetric risk: a VIX print through 18.59 coinciding with a red close stacks vanna and charm into the same direction — pin breaks fast, and the mechanical bid that defended the tape all session evaporates in minutes.

What it means for your trading

Vanna and charm are both pointed lower, so the tape stays orderly only while implieds stay quiet and spot holds 700; a vol uptick into the close is the trigger that converts dormant negative exposures into forced dealer selling.

Cross-Asset Confirmation

MOVE at 67.94 is conspicuously calm against the Iran backdrop — the rates desk is not hedging credit stress, which frames this tape as a geopolitical shock (mean-reverting) rather than a compounding credit event. Fear & Greed prints greed at 63, confirming the risk-on posture under the headline noise.

Cross-asset internals corroborate: QQQ 635.64 alongside IWM 268.67 shows small-caps still participating, but the SPY/QQQ regime split flags spy_heavier — broad index anchors while tech carries the fragility. That role reversal is the chain of custody if headlines crack.

The actionable read: oil and gold are the real tells, not equity vol. With MOVE this calm, the rates book is structurally unhedged for escalation — meaning any Hormuz or supply-side surprise repriced through energy and metals first, then bleeds back into MOVE and VIX with a lag. Keep a cheap tail on; do not mistake bond-market silence for safety.

What it means for your trading

Cross-asset tape reads spy_heavier with MOVE at 67.94 and Fear & Greed in greed — risk-on holds, but oil and gold remain the asymmetric tells the rates desk is not pricing.

Scenario EV

The scenario EV model prints iron_condor as the optimal structure with a best score of 50, with the belly at 30-45 DTE where forward vol is richest relative to spot. The condor beats the put spread (— vs —) because the pin near the call wall dominates directional downside — dealers are dampening, not directional.

VRP assessment reads unknown, which argues for defined-risk wings over naked short premium; realized is too hot to sell uncovered. Short legs align cleanly with dealer flow at 700.00 overhead and 697.00 below, and vol-of-vol sits in the normal band so sizing stays standard_size. Contango carry plus negative VRP plus a gamma pin is the textbook condor setup — you just have to define the wings.

What it means for your trading

Trade the iron_condor in 30-45 DTE with short legs pinned to 700.00 and 697.00. Pin beats direction, carry beats chase, wings beat naked.

Actionable Summary

The book resolves to a single trade: iron_condor on SPY in the 30-45 DTE belly, short legs pinned to the 700.00 call wall and 697.00 put wall where dealer flow does the work. Regime reads Elevated / Watchful with the charm pivot sitting at 700 — fade strength into the wall, fade weakness into the floor, and let carry do the lifting.

Avoid naked short premium: VRP at -4.16% means realized is eating implied, so wings stay defined. QQQ has already slipped below its flip at 636.04 — that is the first crack and the reason short calls on tech are off the table. SPY's own flip at 694.54 is the regime line; a break there flips the tape from dampening to amplification.

Carry a cheap VIX call against the Iran binary — don't fade spikes naked. Size standard_size per the vol-of-vol read.

What it means for your trading

Optimal structure is iron_condor around pivot 700 in a Elevated / Watchful regime; QQQ's flip at 636.04 is the first thing that breaks if headlines turn.

Cramer's watch list frames the tape — record-setting prior session plus Iran peace optimism is exactly the greed-regime backdrop that punishes chasers.

Interim-deal reporting is the binary driver of today's vol — any material hint of breakdown repriced oil, gold, and the VIX front; traders need to monitor headlines continuously.

Hegseth's combat-ready posture is the hawkish counter-narrative to the dovish peace-deal tape — exactly the asymmetric tail that argues for keeping a cheap VIX hedge on.

Iran halting petrochemical exports is a real supply-side shock signal that oil vol stays bid regardless of diplomatic progress — energy complex is the stealth story under the headline optimism.

Strait of Hormuz toll question is the fat-tail risk that would crater risk assets and blow out MOVE — worth tracking as the asymmetric scenario even at low probability.

Gold bid on softer dollar with peace hopes rising is a signal of positioning rotation — gold holding up into optimism tells you hedges are still being accumulated quietly.

Nuclear issues unresolved is the key qualifier on peace-deal optimism — markets are pricing resolution before the hardest piece is settled, a classic setup for headline reversal.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.94 with a contango term structure. The Fear & Greed index reads greed, and cross-asset volatility is spy_heavier across SPY, QQQ, and IWM.

Is SPY in positive or negative gamma today?

SPY is in positive_gamma gamma with net dealer GEX at $14.03B. The gamma flip sits at 694.54, with the call wall at 700.00 and the put wall at 697.00.

Where is the SPY gamma flip level right now?

SPY's gamma flip is at 694.54 against a spot of 698.97. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 15.12% with a volatility risk premium of -4.16%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in contango with VIX at 18.59. Contango signals benign forward expectations; backwardation signals near-term stress.

What's the dealer positioning on QQQ and IWM?

QQQ shows negative_gamma gamma with net GEX at $6.22B (flip: 636.04). IWM shows positive_gamma gamma with net GEX at $380.6M (flip: 264.24).

Get today's live analysis

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime