Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

Positive gamma anchored at 700.00 with contango VIX curve and Iran-war tail bid

Index complex sits in deep positive gamma with SPY pinned at 700.00, while VIX backdrop holds contango and forward vol stays in the steep-contango carry zone. The friction: realized vol still prints above ATM IV (-5.16% VRP), so options are paid less than recent moves — vol sellers want carry but must respect the Iran-war headline tape. VIX itself trades negative gamma (negative_gamma), the only fragility flag in an otherwise aligned cross-asset picture.

Regime Assessment

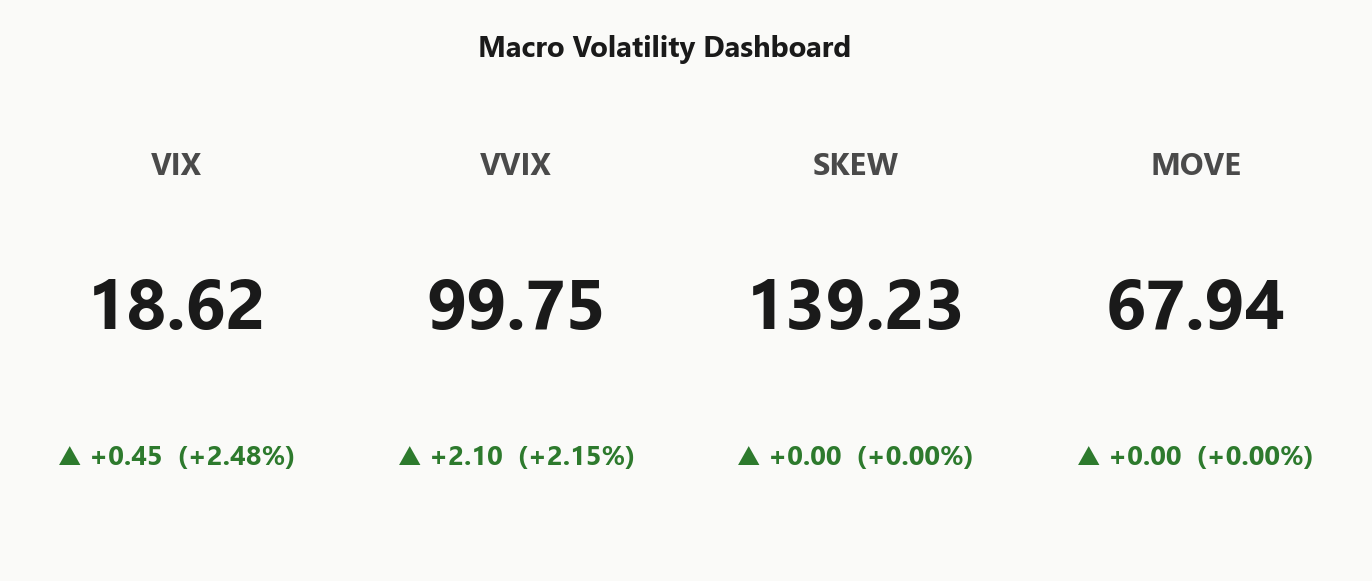

Engine tags the tape Elevated / Watchful — not panic, not low — with VIX at 18.62 planted squarely in the elevated/watchful band. The regime is elevated and, critically, sticky: half-life prints 15 sessions, so this is not a tape to fade on a single print or size for a fast decay.

Transition math argues for patience over positioning for a regime flip. Probability of escalation to panic inside five sessions sits low, probability of decay back to low-vol inside ten sessions only moderate — the modal path is drift within the current band, which is exactly the backdrop that lets the carry trade work without forcing a size-up or a size-down.

The single wildcard that breaks the half-life is the Iran-war headline tape. An escalation print is the one exogenous catalyst that can push elevated into panic before the statistical clock runs out, so size standard, keep risk defined, and treat any MOVE/VVIX confirmation as the trigger to re-rack.

What it means for your trading

Regime reads Elevated / Watchful with a 15-session half-life — plan for stickiness, not mean reversion, and respect the Iran-war tape as the only catalyst that breaks the clock.

Trading readVIX up, VVIX up, MOVE flat, SKEW unchanged — the divergence is bond vol refusing to confirm the equity vol bid, which historically argues for vol fade rather than vol chase.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

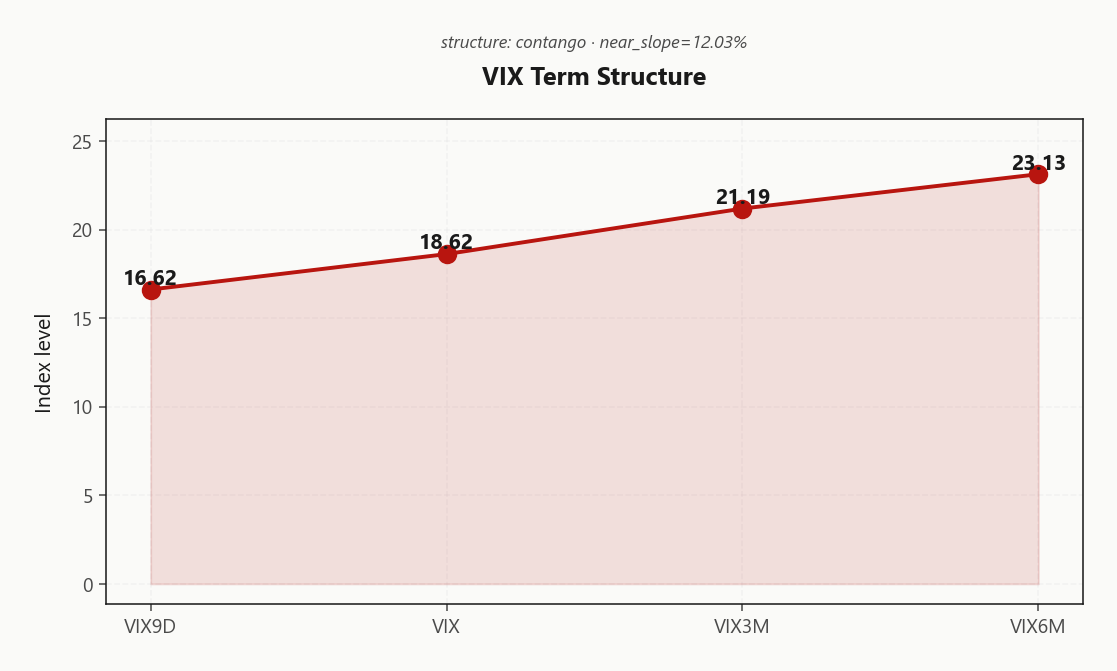

The VIX curve prints contango from the front all the way out, with 16.62 VIX9D undershooting spot 18.62 — near-dated vol is cheap to the headline tape, which tells you intraday realized is tracking calmer than the Iran-war news flow suggests.

Slope out to 21.19 VIX3M keeps the structural carry intact, and the 23.13 VIX6M print confirms steep_contango with no event premium stacked past summer. Forward 30-60d vol at 22.3645243634 sits exactly in the roll-down sweet spot.

Trade construction: in a steep_contango regime with the front-end dislocated lower, calendars and diagonals financed by front-week vol screen better than outright short vega. The steepest bucket is 30-45 DTE — own the back leg, sell the front, let the slope pay you while geopolitics resolves.

What it means for your trading

Forward vol geometry reads steep_contango with VIX9D 16.62 cheap to spot 18.62 — the carry is live, but harvest it through calendars in the 30-45 DTE bucket rather than naked front-end shorts.

Trading readSteep contango from VIX9D through VIX6M is the carry trade's home court — vol sellers get paid the roll, but the front-end undershoot says the headline tape isn't translating into actual realized panic.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

Here is the day's central contradiction: realized has run hot while implied has not followed. 19.22 RV20 sits well above ATM IV at 14.06%, dragging VRP to -5.16% — sellers are being paid less than the tape just delivered. The IV/RV diagnostic flags danger_zone, and that label is doing real work: this is not a premium-harvest setup, it is a vol-owning setup dressed up as one.

The shape of the realized curve matters. 8.22 RV5 has cooled hard off the RV20 print, telling us the move that built the spread is recent and concentrated, not a structural regime shift — HV60 sits much closer to ATM IV. Translation: the carry trade is not broken, but it is mispriced for the next gap, and the Iran-war tape is exactly the kind of catalyst that re-converges IV to RV through the wrong door.

Long-vol screens cleanly here unless you have high conviction RV mean-reverts down faster than IV catches up. Defined-risk only — naked short premium is offside to recent realized.

What it means for your trading

Negative VRP at -5.16% with IV/RV flagged danger_zone means options are cheap to recent swings — favor owning vol or defined-risk structures, not naked short premium, until RV20 decays back toward ATM IV.

Skew Convexity

Quarter-delta put skew prints 2.63% with smile ratio at 1.19% — downside is bid, but the bid is orderly. Put wing at 16.79% against ATM 14.78% and a flat call wing at 14.16% reads as steady institutional hedge demand, not capitulation chase. Left tail still owns more vol per delta, but the curve isn't pricing a panic.

The call wing tells the second half of the story: no upside conviction premium to harvest. Selling calls naked into a flat right wing is paying for nothing while wearing the gap-up tail from any Iran-war de-escalation headline. Symmetric this isn't — and the asymmetry favors owning the left over shorting the right.

Construction: put debit spreads and call credit spreads dominate naked tail premium. With VIX in negative_gamma and headline tape live, defined-risk wings collect the skew without renting jump risk. Skew steep, not broken — trade it, don't sell it.

What it means for your trading

Skew at 2.63% with smile ratio 1.19% says hedge demand is methodical, not desperate; favor put debit / call credit spreads over naked tail premium given the Iran-war headline overhang.

Vol-of-Vol Structure

VVIX prints 99.75 against VIX 18.62 — squarely in the normal band with the ratio parked in the carry-friendly zone. No bimodal jump premium baked in despite the Iran-war headline tape doing its best to wake up the convexity bid. The vol-of-vol surface simply isn't pricing a binary regime, which is itself the signal: dealers and end-users agree this is a discrete geopolitical shock, not the front edge of a systemic vol cascade.

That reading is the green light for standard_size deployment on the iron condor — full clip, not the half-size posture you'd take if VVIX were screaming. The carry trade earns its keep when vol-of-vol behaves, and right now it's behaving.

The one tell that flips this from carry to crush: a clean VVIX print through the one-thirty handle. That's the line where the distribution turns bimodal, the ratio breaks out of its comfort zone, and every short-premium book suddenly needs to halve. Until that print, size standard and let the contango pay you.

What it means for your trading

VVIX 99.75 in the normal band against VIX 18.62 permits standard_size on the iron condor. Watch the one-thirty VVIX line as the single trigger that forces a halving.

Dispersion Spread

Index ATM IV sits moderate at 14.06%, stepping up through 18.77% on QQQ and 20.8% on IWM — the complex is not pricing correlated panic, it's pricing idio. Cross-strike dispersion prints 80.81 against a cross-expiry read of 2.58, so the vol is in the wings and the names, not the index tape.

Top-mover GEX tells the same story louder. NVDA headlines the board with a gamma shift that dwarfs the rest of the mega-cap stack, with AAPL, GOOGL, AMZN, and TSLA all migrating independent of index beta. Single-name flow is doing the work the index isn't — classic live-dispersion regime where index hedges bleed theta against constituents that keep repricing.

Construction follows the geometry: short the index vol where the pin and the contango carry do the lifting, leave single-name premium to the names that own it. Selling SPX/SPY straddles against owned NVDA/TSLA optionality is the cleanest way to monetize the spread — don't cross the streams by shorting vol where dispersion is alive.

What it means for your trading

Index vol at 14.06% undershooting QQQ 18.77% and IWM 20.8% while single-name GEX rips wide confirms dispersion is live: sell index premium, own single-name convexity.

Liquidity & Microstructure

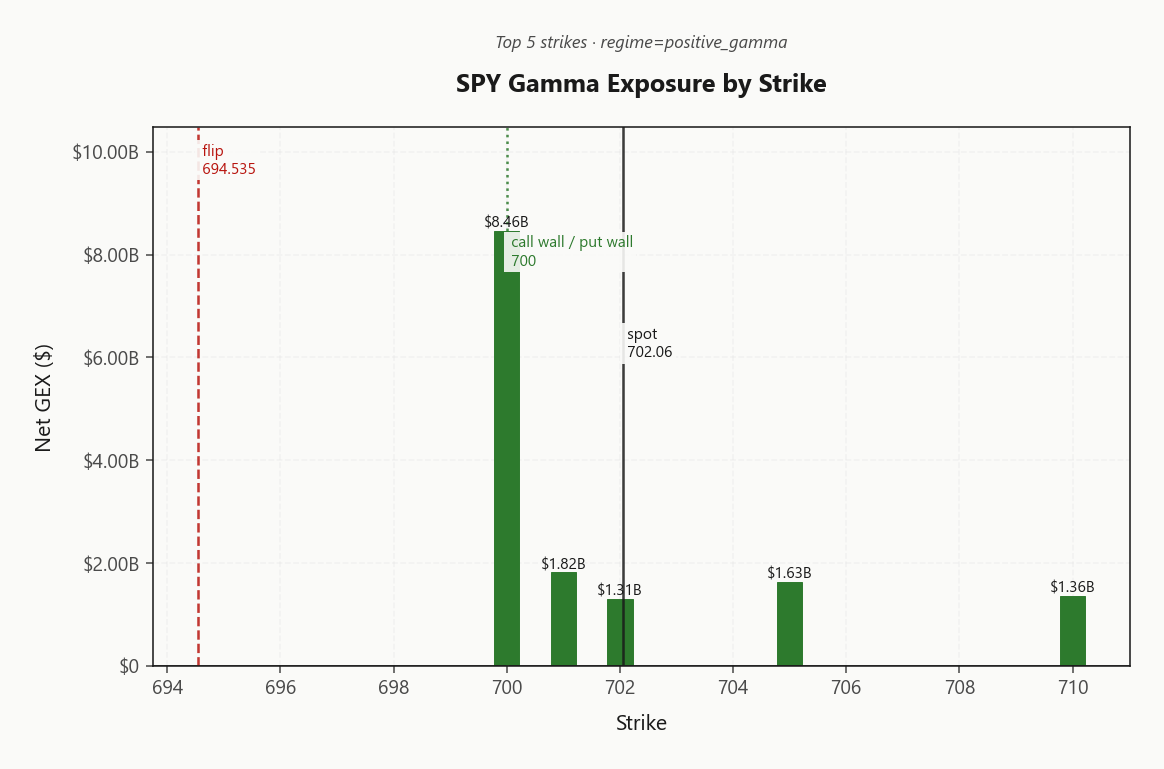

The 700.00 strike is the entire book today — $8.46B of net gamma concentrated at a single level that doubles as both call wall and put wall. This is the strongest pin we've seen in months, and spot sitting just beneath it makes the dealer-flow magnet overhead, not underfoot.

Gamma flip at 694.54 sits just below spot — the razor's edge where dealer behavior inverts. Above the flip and below the wall, dealers damp every move; a clean break through 700.00 flips the book into trend-amplifying mode and opens squeeze risk. A loss of the flip inverts the same mechanic to the downside, with dealer selling accelerating any weakness.

Deeper structural anchor sits at 600 on the longer-dated OI profile, but intraday gravity is entirely at the wall. Microstructure reads deep — fade strength into the pin, fade weakness off the flip, treat a clean wall break as regime change rather than continuation.

What it means for your trading

The 700.00 combined wall is THE level — inside the 694.54–700.00 corridor dealers dampen, outside either boundary they amplify. Trade the pin, respect the break.

Trading readMassive gamma cluster at the 700.00 strike makes it the day's gravitational center — fade strength into it, fade weakness off it, and treat any clean break above as a regime change rather than a continuation.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net VEX prints -$209.58B and CHEX -$1.31B — both deeply negative, which means any vol uptick on an Iran headline forces dealers to sell delta into weakness, while charm bleed compounds the pressure as the tape grinds toward the close. The long-gamma pin is real, but it is conditional on VIX staying contained; the second the curve twitches, vanna becomes the accelerant, not the dampener.

The single level that matters is the charm pivot at 700, which doubles as the call_wall. Current bias reads neutral — coiled, waiting for spot to resolve the wall. A clean break above flips dealer behavior into long-pressure and opens the squeeze path; rejection back through it activates the vanna whip on the next vol tick. Trade the level, not the narrative around it.

What it means for your trading

Negative VEX and CHEX make the 700 wall the entire trade — above it, dealer hedging turns supportive into a squeeze; below it on any Iran-driven vol pop, vanna forces accelerant selling.

Cross-Asset Confirmation

Cross-asset reads aligned: MOVE at 67.94 sits unchanged through the Iran tape, refusing to confirm the equity vol uptick — bond vol is the tell, and it isn't ringing. Fear & Greed holds greed at 63, sentiment still risk-on rather than capitulating into the headline flow.

QQQ at 641.19 and IWM at 269.73 both trade above their flips in positive_gamma, mirroring SPY's anchor — the index complex is regime-aligned, not fragmenting. The single dissent is VIX itself in negative_gamma, which keeps the vol-of-vol layer as the stress vector rather than credit or rates.

Translation: this is a geopolitical-isolated tape, not a systemic one. Mean-revert bias and the iron-condor carry trade hold until MOVE breaks higher or VVIX prints through the panic threshold; absent those, fade equity-vol pops rather than chase them.

What it means for your trading

With MOVE at 67.94 inert and Fear & Greed still greed, the cross-asset signal isolates Iran as a discrete shock rather than a credit spiral — mean-revert bias holds while the index complex stays regime-aligned.

Scenario EV

Engine prints iron_condor as the top-ranked structure at score 48, with the optimal window in the 30-45 DTE bucket. That bucket harvests the steepest part of the contango roll without taking on 0DTE pin convexity around the 700.00 wall.

The why-over-alternatives is the VRP read: with -5.16% printing and the assessment flagged unknown, naked short premium is mispriced to recent realized — sellers underwater to the tape. Range-defined wings let you collect the contango carry while capping the Iran-headline gap risk. Calendar diagonals rank second on the steep front-end slope from 16.62 through 21.19; put-spread score lags at 34.

Sizing guidance is standard_size with VVIX in the normal band — full clip on the condor, half-size only on a VVIX print through the binary threshold.

What it means for your trading

Deploy iron_condor in the 30-45 bucket centered on the 700 pin, defined-risk only given -5.16% VRP. Carry trade is paid here, but the wings — not naked premium — are how you cash the check.

Actionable Summary

BLUF: Deploy iron_condor in the 30-45 DTE bucket centered on the 700 pin while regime stays Elevated / Watchful. Spot trades just under the 700.00 wall with the gamma flip at 694.54 — the corridor is the trade, defined-risk wings are the guardrail.

AVOID naked short premium with VRP printing -5.16% (RV20 19.22 above ATM IV 14.06%) — sellers underwater to recent realized. Skip 0DTE long-gamma chases into the pin; charm bleed and net CHEX -$1.31B do the work for you. HEDGE Iran-war headline tape via put debit spreads, not naked puts — skew at 2.63% is orderly, not desperate.

WATCH: a clean spot break of 700 flips dealer bias from neutral to trend-amplifying via net VEX -$209.58B; VVIX through 99.75 toward the panic band forces half-size. Regime is sticky for ~15 sessions absent shock — cross-asset reads aligned, MOVE 67.94 not confirming the equity vol bid.

What it means for your trading

Sell the iron_condor corridor around 700 in the 30-45 bucket while Elevated / Watchful regime holds, but fund tail hedges with put spreads — VRP -5.16% means naked premium is mispriced into the Iran-war tape.

US military posture toward Iran energy infrastructure is the single biggest tail bid in vol today — explains why front-end VIX is up while term structure stays in contango.

German growth forecast halved on Iran-war drag is the first hard macro datapoint quantifying the conflict's economic cost — watch for follow-through in EU vol.

Iran halting petrochemical exports is the supply-shock confirmation — feeds directly into MOVE/credit risk and is the trigger that would break cross-asset alignment.

Oil's broken price compass is the cleanest read on why VVIX is elevated despite VIX being range-bound — the market doesn't know how to price the energy tail.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.62 with a contango term structure. The Fear & Greed index reads greed, and cross-asset volatility is aligned across SPY, QQQ, and IWM.

Is SPY in positive or negative gamma today?

SPY is in positive_gamma gamma with net dealer GEX at $18.56B. The gamma flip sits at 694.54, with the call wall at 700.00 and the put wall at 700.00.

Where is the SPY gamma flip level right now?

SPY's gamma flip is at 694.54 against a spot of 702.06. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.06% with a volatility risk premium of -5.16%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in contango with VIX at 18.62. Contango signals benign forward expectations; backwardation signals near-term stress.

What's the dealer positioning on QQQ and IWM?

QQQ shows positive_gamma gamma with net GEX at $2.55B (flip: 633.02). IWM shows positive_gamma gamma with net GEX at $709.2M (flip: 264.10).

Get today's live analysis

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime