Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

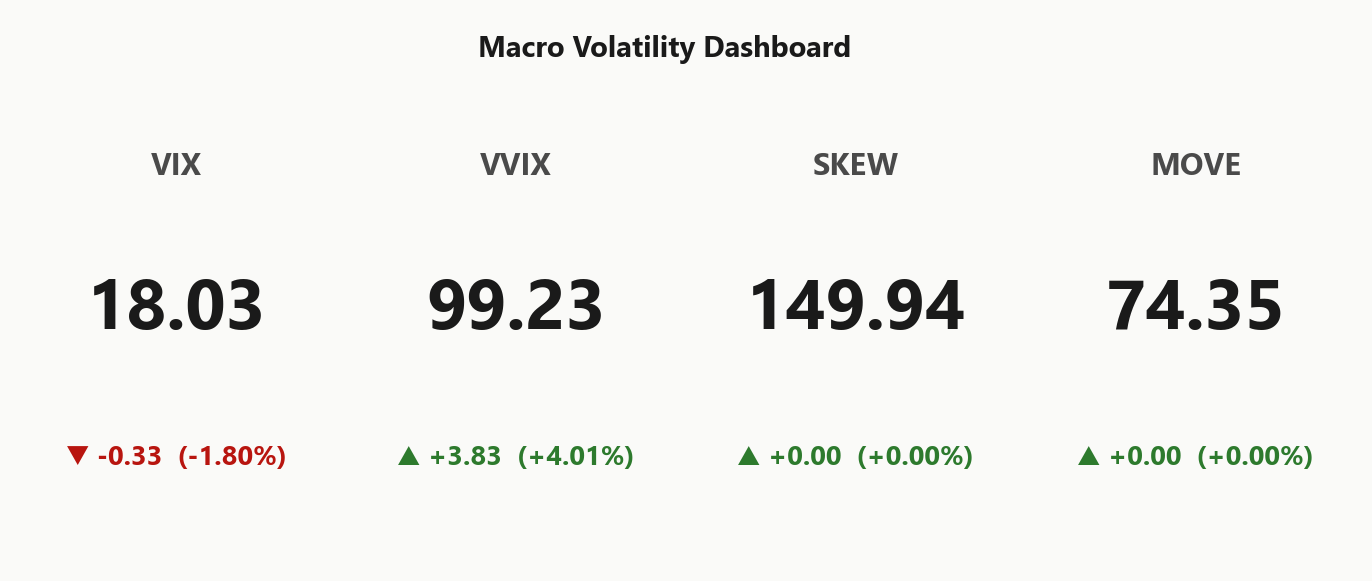

The index complex opens fractured: SPY sits in positive_gamma above its gamma flip while QQQ trades in negative_gamma below its own — the first divergence story of the session. VIX term structure is in contango with VVIX at 99.23, keeping vol-of-vol risk contained and favoring premium-selling structures. Geopolitical de-escalation hopes are unwinding the Iran war premium, but negative VRP across all indices says realized vol still exceeds what the options market is pricing.

Regime Assessment

The vol regime registers Elevated / Watchful with VIX printing 18.03 — elevated enough to sustain rich theta but well below panic thresholds. Escalation probability over the next five sessions sits at —, confirming that the geopolitical de-escalation bid is suppressing left-tail pricing even as realized vol continues to outrun implied across the complex. The path to normalization carries better odds: probability of transitioning to a low-vol regime within ten sessions is —, consistent with the steep contango term structure already discounting calmer conditions forward.

The half-life of 15 sessions is the operative constraint — this elevated state is sticky enough to frustrate directional conviction in either direction. The yellow signal warrants a watchful posture: lean into defined-risk premium structures that benefit from carry while the regime persists, but avoid sizing for a swift resolution. The SPY/QQQ gamma divergence adds a rotational overlay to what is otherwise a grind-and-decay setup.

What it means for your trading

Regime is Elevated / Watchful with a half-life of 15 sessions — moderately persistent, favoring defined-risk premium collection over directional bets while the elevated state decays toward normalization at — probability over ten sessions.

Trading readVIX, MOVE, and Fear & Greed are all in benign territory, but VVIX crept higher today — a subtle divergence. When vol-of-vol rises while vol itself compresses, it often precedes a regime transition. Not alarming yet, but worth tracking session over session.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

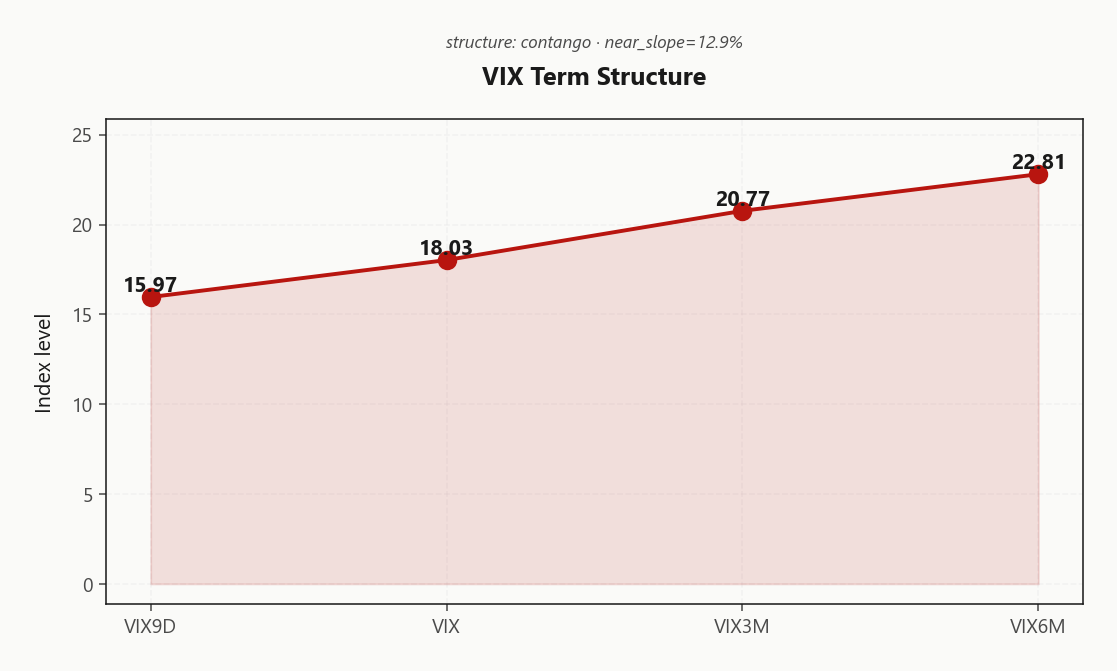

The VIX term structure opens in clean contango with VIX9D at 15.97 printing well below spot VIX at 18.03 — near-term demand for protection is depressed even as the curve prices elevated uncertainty further out through VIX3M at 20.77 and VIX6M at 22.81. The near-term slope of 12.9%% is steep by historical standards, creating structural carry for short-vol positions anchored in the belly of the curve.

Forward vol regime reads steep_contango: Steep contango — vol sellers favored. VIX futures front month at 20.77 versus spot at 18.03 embeds a 15.2%% basis premium — roll-down carry is live and favors sellers who size into the 30-45-day window where forward vol is fattest relative to near-term implied.

The steep upward slope signals the market expects contained realized vol now but refuses to discount uncertainty past the quarterly horizon. Best edge sits in the belly — short enough to harvest theta, long enough to avoid the compressed front end.

What it means for your trading

Full contango with a steep_contango regime and 15.2%% futures basis premium favors premium-selling structures in the 30-45-day DTE window, where the carry between depressed near-term vol and elevated forward vol is maximized.

Trading readClean contango from spot through six months with steep near-term slope — the vol carry trade is live but the negative VRP is the asterisk. Sellers collect roll-down but realized moves are wider than implied, so sizing discipline matters more than usual.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

The volatility risk premium is inverted across the entire index complex. SPY ATM IV at 13.84% sits well below twenty-day realized at 20.04, producing a VRP of -6.2% — the IV/RV spread assessment reads danger_zone. QQQ mirrors the dislocation: ATM IV at 18.14% against HV20 at 24.02, with VRP at -5.88%. IWM confirms at -4.51%. No corner of the index complex is offering positive carry to premium sellers on a realized basis.

This is not a transient spike. SPY sixty-day realized at 15.75 also clears current ATM IV, confirming the under-pricing extends across horizons. Five-day realized has compressed to 8, hinting at near-term spot-vol mean-reversion — but the structural deficit remains. Sell premium only inside defined-risk wrappers; naked short vol carries negative edge until VRP normalizes.

What it means for your trading

Negative VRP across SPY (-6.2%), QQQ (-5.88%), and IWM (-4.51%) confirms options are cheap to realized moves on every relevant horizon — favor iron condors and spreads over naked premium until the IV/RV gap closes.

Skew Convexity

SPY's quarter-delta skew at 3.24% reflects orderly put demand — institutional hedging, not capitulation. Put-side IV at 16.14% runs well above ATM at 13.79%, while calls sit compressed at 12.9%. The surface prices downside protection methodically; upside conviction is notably absent.

QQQ tells a sharper story — skew steeper at 3.98% with smile ratio at 1.23%, confirming heavier tech tail demand consistent with its negative-gamma regime. SPY's own smile ratio at 1.25% is elevated enough to favor spread-based hedges over naked puts — wing premium makes verticals more efficient. CBOE SKEW at 149.94 is elevated but stable, embedding tail risk without accelerating.

Actionable read: the steep smile rewards put spreads over outright puts, and compressed call-side IV makes call credit spreads structurally cheap to sell. This is a surface that says hedged but not fleeing.

What it means for your trading

Quarter-delta skew is moderately steep across the complex — SPY at 3.24%, QQQ steeper — with elevated smile ratios favoring spread protection over naked puts while flat call-side IV at 12.9% confirms thin upside conviction despite the rally.

Vol-of-Vol Structure

VVIX at 99.23 is contained despite the geopolitical whipsaw that drove the March-to-April range — the options-on-options market is not pricing bimodal outcomes. The VVIX/VIX ratio near 5.50 sits squarely in the normal band, confirming that jump risk is being priced as standard rather than elevated. Vol-of-vol regime reads normal, which keeps convexity hedges cheap and removes any structural reason to haircut notional.

The nuance: VVIX rose modestly on the session but from a depressed base — the move reflects repricing of near-term uncertainty, not a regime shift. With VIX at 18.03 and the term structure in contango, the vol complex is orderly from spot through the curve. Sizing guidance remains standard_size. The trigger to revisit: any acceleration in VVIX that compresses the ratio toward the elevated band while VIX itself stays anchored — that divergence would signal hidden tail demand building beneath a calm surface.

What it means for your trading

Vol-of-vol is normal with VVIX/VIX ratio at 5.50 — no binary pricing, standard_size warranted. Watch for VVIX acceleration decoupling from spot VIX as the early warning of regime transition.

Dispersion Spread

SPY ATM IV at 13.84% sits compressed while the mega-cap complex undergoes significant gamma repositioning — AAPL, MSFT, and AMZN are all accumulating positive GEX without lifting index-level implied vol. Cross-strike dispersion at 79.94 confirms single-name moves are not translating into index premium, keeping correlation suppressed and the dispersion regime moderate.

This setup structurally favors SPX/SPY iron condors over single-name short vol. The positive-gamma anchor across the largest names creates a dampening floor beneath the index while individual stocks digest idiosyncratic flows — dealers are absorbing single-stock gamma without repricing the index surface. Until correlation spikes to compress the gap between single-stock realized and index implied, the edge sits in collecting index theta where the positive_gamma cushion provides natural range support and the call wall at 700.00 caps the upside mechanically.

What it means for your trading

Moderate dispersion with compressed index IV at 13.84% and active single-stock gamma repositioning favors defined-risk index premium selling — the mega-cap GEX buildup stabilizes the index while idiosyncratic moves stay contained below the surface.

Liquidity & Microstructure

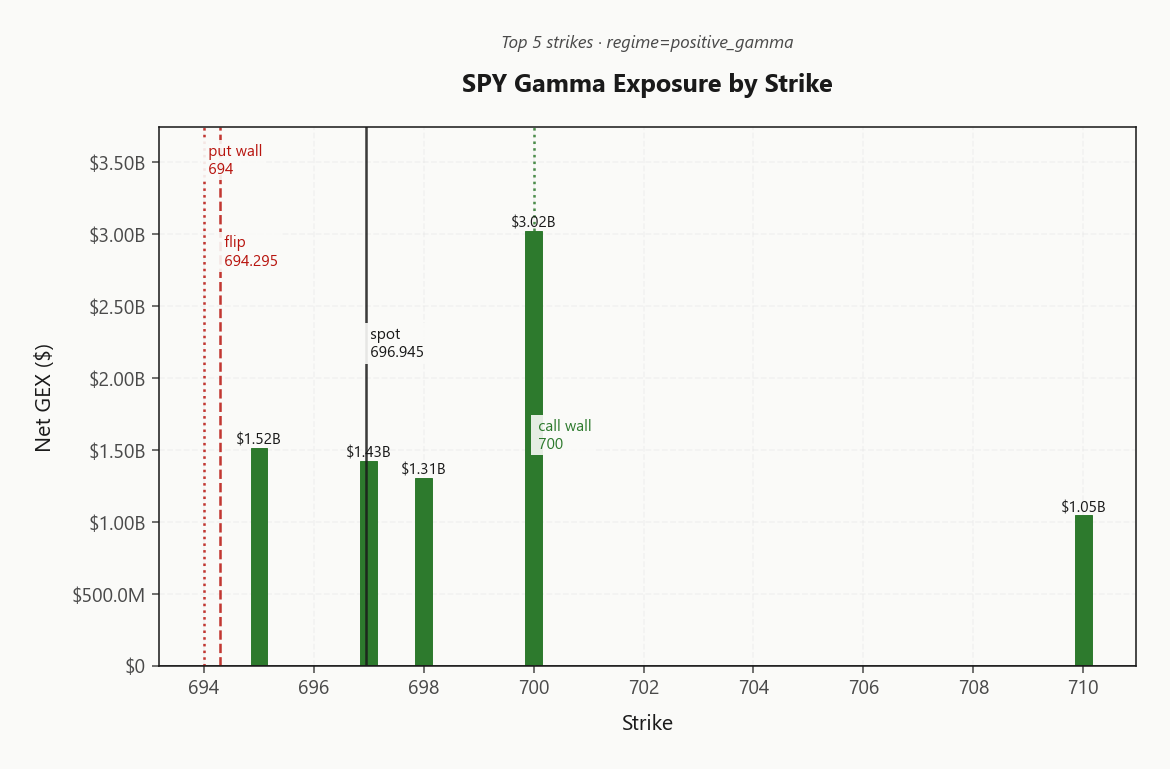

Massive open interest concentration anchors the tape. The call wall at 700.00 commands $3.02B in net GEX — the dominant gravitational strike where dealers will mechanically sell into any probe. Gamma flip at 694.29 sits just below spot, defining the session's key inflection: above it, dealer hedging dampens moves; below it, flow reverses and amplifies.

The put wall at 694.00 brackets the flip tightly, compressing the dealer support zone into a narrow band. Any simultaneous breach of both levels converts the cushion into an accelerant. Highest OI concentration at 600 reflects deep downside positioning from longer-dated institutional hedges — structural demand that won't roll off quickly.

Same-day expiry accounts for 32% of total GEX — sufficient to generate intraday chop around the walls but not dominant enough to override the multi-day structure. Fade rallies into the call wall; lean on the flip as your risk line.

What it means for your trading

The tape is structurally pinned between 694.29 support and 700.00 resistance, with deep dealer gamma capping upside and cushioning dips — favor mean-reversion positioning within the range until the flip breaks.

Trading readSPY's gamma is stacked heavily around the call wall — dealers will cap rallies into that level with mechanical selling, while the cluster just above the gamma flip provides a floor. Trade the range: fade into the wall, buy dips toward the flip.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Vanna is the session's hidden accelerant. Net VEX at -$195.08B is deeply negative — any expansion in implied vol forces dealers to sell delta mechanically, amplifying downside through the gamma flip. The positive-gamma cushion damping SPY's tape is a spot phenomenon; a vol shock reverses the entire hedging flow through vanna before gamma can absorb it.

Charm at -$18.9M layers mild but persistent selling pressure into the close as time decay erodes dealer hedges. The charm pivot sits at 694.2945178954 with spot -0.3803000387 above, keeping the current bias supportive. That margin is thin. The destabilizing path: spot slips through the pivot while vol expands simultaneously, flipping vanna from latent risk to active accelerant and compounding the charm drain into a self-reinforcing selloff. Monitor VIX acceleration — that is the trigger converting this supportive regime into a mechanical unwind.

What it means for your trading

Deeply negative vanna dominates the greek complex — the supportive bias above 694.2945178954 holds only while vol stays contained, and any VIX spike converts dealer flow from stabilizer to accelerant.

Cross-Asset Confirmation

MOVE at 74.35 is benign — rates vol is not confirming credit stress, and the bond market is offering no contagion signal into equities. Fear & Greed sits at 55 (neutral), a market that has mean-reverted from panic without tipping into euphoria — no contrarian extreme to fade in either direction.

The critical divergence: SPY anchors in positive_gamma above its gamma flip while QQQ at 633.22 trades in negative_gamma below its own — regime split confirmed at true. Tech is the vulnerable leg; dealer flow amplifies QQQ moves while dampening SPY. IWM at 268.41 carries a unknown regime, offering no structural clarity. This is not a macro-credit shock — it is a rotation and dispersion story, with the index complex fractured rather than uniformly stressed.

What it means for your trading

Cross-asset indicators are benign: MOVE at 74.35 and sentiment at neutral show no contagion or contrarian extremes, isolating the SPY/QQQ gamma regime divergence as the session's lead positioning story rather than a broad risk event.

Scenario EV

iron_condor scores highest at 48 on the structure board — the steep contango term structure and contained VVIX at 99.23 create a favorable carry backdrop for defined-risk premium collection in the 30-45-day DTE window, where theta decay is fattest against the forward vol curve. Put spreads score 35 as a viable alternative for desks wanting a directional lean toward the 694.00 support cluster.

Negative VRP across the complex — SPY at -6.2%, QQQ at -5.88% — is the critical asterisk: realized vol is outrunning implied on every relevant horizon, making naked short strangles a negative-edge expression. The iron condor's defined wings cap the realized tail that implied is under-pricing. Standard sizing applies per standard_size guidance, and the gamma flip at 694.2945178954 serves as the structural risk line — supportive above, destabilizing below.

Regime context reinforces the call: Elevated / Watchful with a half-life of 15 sessions suggests this elevated state is moderately sticky. Collect carry, keep the wings tight, and let the positive_gamma cushion do the work.

What it means for your trading

Iron condors at 30-45 DTE exploit steep contango carry while capping the negative-VRP tail risk that naked structures cannot absorb — the positive_gamma regime and contained vol-of-vol keep the setup constructive, but 694.2945178954 is the line where the thesis breaks.

Actionable Summary

The index complex opens fractured — SPY sits in positive_gamma above its gamma flip while QQQ trades in negative_gamma below its own, setting up a session where SPY dampens and QQQ amplifies. Position in iron_condor structures on SPY at 30-45 DTE to harvest the steep contango carry, using the gamma flip at 694.2945178954 as your hard risk line — dealer hedging is supportive above it, destabilizing below. Negative VRP across the entire complex means options are cheap to realized moves; avoid naked short strangles until that spread normalizes.

The convergence trigger to monitor: negative_gamma flipping to positive gamma would confirm broad stabilization and widen the premium-selling opportunity set beyond SPY. Until then, respect the divergence — fade SPY into its walls, honor QQQ trends. Regime reads Elevated / Watchful with a moderately persistent half-life, favoring defined-risk expressions over outright directional bets. Vol-of-vol is contained at 99.23, warranting standard sizing — no need to haircut notional here.

What it means for your trading

SPY's positive-gamma cushion and steep contango favor iron_condor structures at 30-45 DTE, pivoting around the 694.2945178954 gamma flip. Negative VRP demands defined-risk only; watch for QQQ regime convergence as the all-clear for broader premium selling.

Overbought readings after a sharp rally from March lows create the backdrop for today's regime call — extended positioning meets positive gamma, favoring mean-reversion over momentum chasing.

A Congressional probe into Strait of Hormuz contingency planning signals the geopolitical risk premium hasn't fully unwound — energy supply disruption remains a tail risk that could re-steepen the vol curve.

EU warning of prolonged energy cuts if the Iran conflict resumes is the bear case for global growth and the reason the VIX term structure still prices elevated vol further out despite near-term calm.

Rising farmer input costs tied to shipping disruptions are a second-order inflation signal — if fertilizer and fuel squeeze margins, food prices follow, complicating the Fed's path.

Bank of America earnings set the tone for financials — a beat extends the comeback narrative and supports the risk-on regime, while a miss in credit provisions would signal cracks beneath the surface.

The dollar shedding its Iran war premium confirms the rates market is de-risking — supportive for equities near-term, but a rapid unwind can itself become disorderly.

Markets betting the Iran war is over is THE macro theme today — this is the catalyst behind the rally from March lows and the reason VIX is pressing toward the teens despite elevated realized vol.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.14 with a contango term structure. The Fear & Greed index reads neutral, and cross-asset volatility is spy_heavier across SPY, QQQ, and IWM.

Is SPY in positive or negative gamma today?

SPY is in positive_gamma gamma with net dealer GEX at $9.76B. The gamma flip sits at 694.29, with the call wall at 700.00 and the put wall at 694.00.

Where is the SPY gamma flip level right now?

SPY's gamma flip is at 694.29 against a spot of 696.94. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 13.84% with a volatility risk premium of -6.2%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in contango with VIX at 18.03. Contango signals benign forward expectations; backwardation signals near-term stress.

What's the dealer positioning on QQQ and IWM?

QQQ shows negative_gamma gamma with net GEX at $29.2M (flip: 637.00). IWM shows unknown gamma with net GEX at $823.1K (flip: —).

Get today's live analysis

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime