Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

Positive gamma suppression holds; options cheap to realized — sell structure, not direction

All three equity indices hold in positive_gamma with spot pinned just below the call wall at 700.00, where dealers dampen rallies and dips alike. VIX term structure remains in contango — carry is available — yet VRP at -6.52% means realized vol still outpaces implied, leaving options cheap to actual recent moves. The market is rallying into Iran ceasefire optimism, but the vol surface hasn't repriced the calm yet.

Regime Assessment

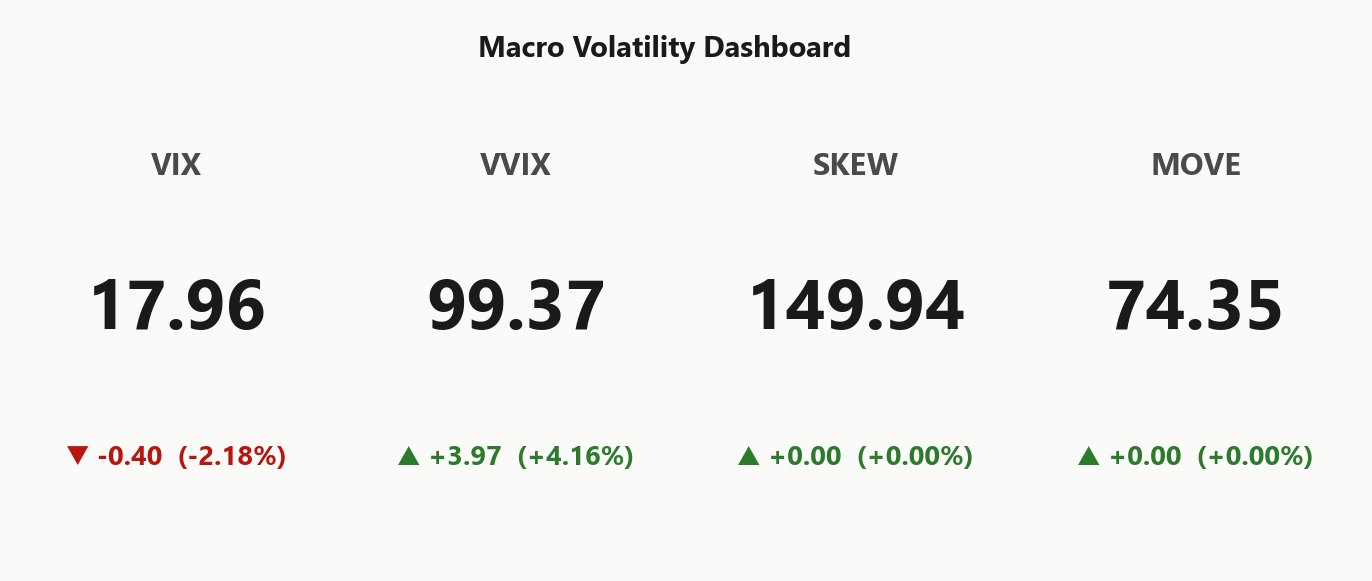

The vol regime sits at elevated — Elevated / Watchful — with VIX at 17.96 and a half-life of 15 sessions. This is transitional territory, not sticky: the regime either compresses toward low-vol as the ceasefire narrative firms, or re-escalates if headlines reverse. Near-term panic probability is negligible, and the higher-probability path resolves toward suppression — structure accordingly.

Cross-asset alignment reinforces the base case. SPY, QQQ, and IWM all hold in positive_gamma with regime divergence aligned, term structure in contango, and VVIX at 99.37 flagging normal vol-of-vol — no bimodal pricing embedded. The setup favors defined-risk premium collection in the 30-45-day window, but the half-life reminds you this regime has an expiration date. Hedge the tail with spread protection, not naked exposure — a single headline can re-ignite the war premium faster than dealers can re-hedge.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life — transitional, not entrenched. Base case is compression to low-vol; position for that outcome via iron_condors while respecting the geopolitical toggle that could extend or invert the regime.

Trading readVIX and MOVE are both moderate and confirming each other — no equity-credit divergence. VVIX ticked up while VIX eased, a minor but notable split suggesting the vol-of-vol market is slightly less sanguine than spot vol. SKEW elevated confirms tail hedging is being maintained underneath the calm surface.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

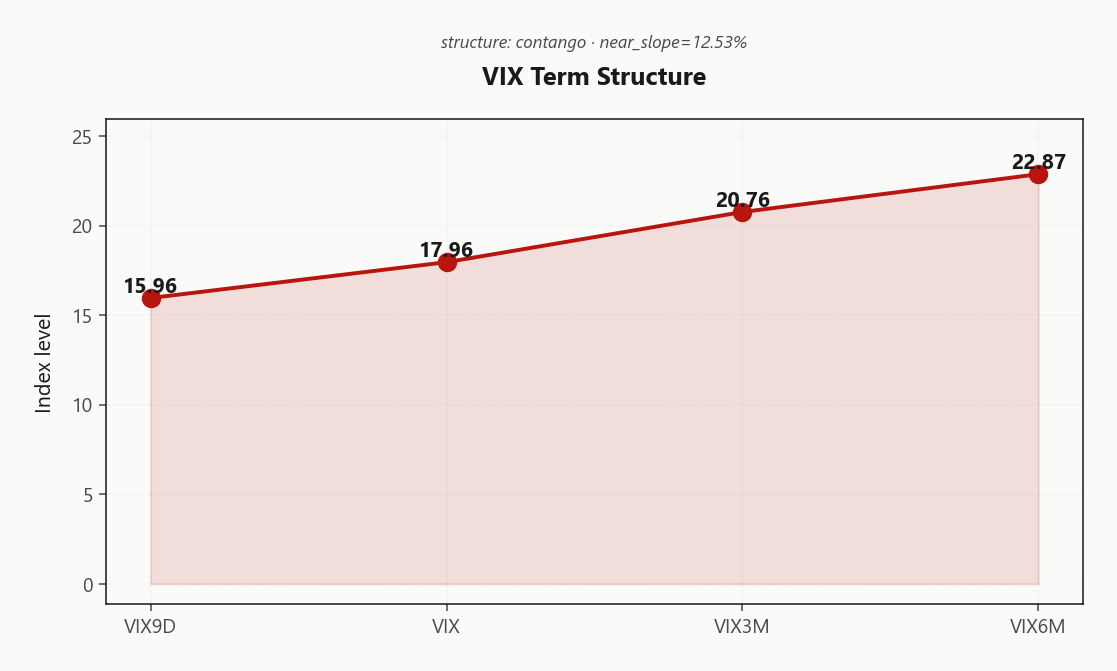

The VIX term structure is in full contango with VIX9D printing 15.96 well below spot VIX at 17.96 — the front end is pricing near-term calm with conviction. VIX3M at 20.76 and VIX6M at 22.87 build a steep ascending slope, confirming structural carry for anyone willing to sell the near leg and collect roll-down into expiry.

Forward vol steps up meaningfully between the one-to-two-month and two-to-three-month buckets, signaling the market expects no imminent catalyst to flatten the curve but still embeds lingering geopolitical uncertainty further out. The forward vol regime is flagged steep_contango — the steepest configuration for harvesting calendar decay. Front-end implied is the sell zone; back-month premium reflects residual Iran optionality the spot market has already begun discounting.

Sell near-dated IV, ride the contango. Calendars and short-dated iron condors capture the richest roll-down while geopolitical carry remains available.

What it means for your trading

Term structure in contango with regime steep_contango — front-end vol is cheap to the back end, making near-dated premium sales the highest-carry expression available while the ceasefire narrative compresses the short end of the curve.

Trading readFull contango from spot VIX through the six-month tenor confirms the vol carry trade is on — sell near, collect roll-down. The steep near-term slope says the market sees no imminent catalyst to invert, but respect the geopolitical optionality embedded further out on the curve.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

The vol surface is mispricing the tape. SPY ATM IV at 13.53% sits well below trailing realized — the five-day print at 7.88 has compressed sharply from the twenty-day at 20.05, but even against this fading backdrop, VRP at -6.52% confirms options remain genuinely cheap to recent moves. The IV-RV spread assessment reads danger_zone — the surface hasn't caught up to the recovery's actual velocity.

This isn't isolated to large-cap. QQQ carries VRP at -5.75%, confirming tech implied is equally underpriced relative to realized. Cross-index negative VRP with aligned gamma regimes means the discount is structural, not idiosyncratic — the entire complex moved more than the options market expected.

The pivot question is whether ceasefire-driven de-escalation compresses realized vol toward implied, retroactively validating sellers, or whether the recovery pace sustains elevated realized and hands long-vol positions a widening edge. Until that resolves, defined-risk structures capture the gamma suppression without betting naked on a VRP normalization that hasn't started.

What it means for your trading

Negative VRP across all indices with the spread flagged as danger_zone means the surface is underpricing actual moves — sell premium only through defined-risk vehicles until realized vol compresses toward 13.53% implied.

Skew Convexity

Quarter-delta skew prints 3.43% with the smile ratio at 1.28% — put premium is elevated but orderly, reflecting maintained tail hedges rather than panic bidding. The left wing is being serviced, not chased, and that distinction matters for structure selection: outright puts carry a skew tax that spread strategies largely neutralize.

The vol smile tells a directional story. Put quarter-delta IV at 15.84% stands well above ATM at 13.23%, yet call quarter-delta IV at 12.41% trades below ATM — the options market is funding downside protection while expressing near-zero upside conviction. Spot rallies into ceasefire optimism, but the vol surface refuses to confirm the bid. That flat call wing is the tell: institutional desks are hedging, not reaching.

In this skew environment, put spreads dominate naked puts on premium efficiency. Wing steepness adds cost without the convexity payoff that justifies outright tail hedges — spread the protection, collect the skew differential, and let the smile ratio do the work.

What it means for your trading

Orderly skew with a smile ratio above parity confirms maintained — not panicked — downside hedging, while flat call skew reveals the options market's skepticism toward the rally; put spreads offer superior premium efficiency over outright puts until skew steepens materially.

Vol-of-Vol Structure

VVIX holds at 99.37 against a VIX print of 17.96, keeping the ratio in normal territory — no bimodal event premium is embedded, and standard_size applies across the book. The vol-of-vol surface is not demanding any jump-risk surcharge, which validates defined-risk premium-selling structures over outright straddle ownership.

The wrinkle: VVIX ticked higher today while VIX eased — a subtle but notable divergence. Spot vol is buying the ceasefire narrative; vol-of-vol is hedging around it. That split has historically preceded either a swift convergence (VIX catches up) or an early regime warning (VVIX was right). In an elevated regime with forward vol in steep_contango, the base case is convergence — but the divergence bears watching as the single best early-warning indicator that dealer hedging assumptions are shifting beneath a calm surface.

Sizing implication is straightforward: standard notional, standard wing width. If VVIX accelerates above the session high while VIX remains anchored, tighten wings and reduce size preemptively — do not wait for VIX to confirm.

What it means for your trading

VVIX at 99.37 signals normal vol-of-vol with standard_size appropriate, though the intraday VVIX-up/VIX-down divergence warrants monitoring as a potential leading indicator of regime transition from elevated toward re-escalation.

Dispersion Spread

Dispersion is a non-event. SPY, QQQ, and IWM all hold in positive_gamma with regimes aligned — no index is breaking ranks, eliminating cross-asset spread opportunities. ATM IV prints at 13.53% for SPY, 18.29% for QQQ, and 20.12% for IWM — the typical ordering holds with small-cap vol richest, but the spread is unremarkable.

Single-name flow confirms the alignment. Today's top movers — NVDA, META, AAPL, AMZN, AVGO — are uniformly positive-direction, signaling coordinated macro buying rather than idiosyncratic rotation. No earnings blowups, no sector dislocations, no single-stock vol events disrupting index correlation. When the entire mover board points one way, constituent dispersion compresses and index-level structures capture the regime cleanly.

Sell index vol, not single-name. Positive gamma across the complex means dealer buying supports every dip at the index level — that dampening doesn't apply to individual names approaching earnings. Iron condors on SPY or QQQ harvest the suppressive regime and contango carry without single-stock event risk contaminating the position.

What it means for your trading

Cross-index aligned alignment and uniformly positive single-name flow compress dispersion, making index vol selling the cleanest expression of the suppressive gamma regime — harvest contango carry at the index level and leave single-stock event risk to someone else.

Liquidity & Microstructure

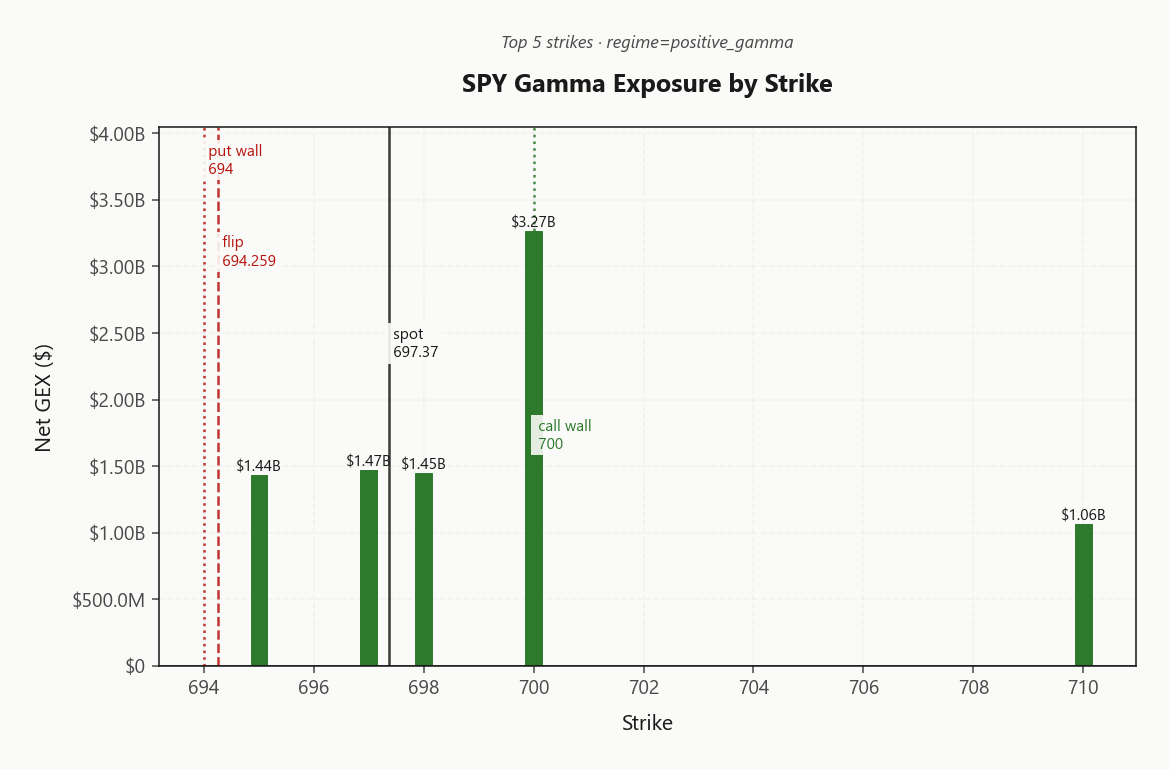

The call wall at 700.00 is the gravitational center of today's tape — top-strike GEX of $3.27B concentrates dealer hedging at this round number, creating a magnetic ceiling that mechanically caps rallies. Spot at 697.37 sits just below, and every tick higher forces dealers to sell delta into strength. Highest open interest anchors at 600, but the active pin is the wall — that's where the hedging flow lives.

The gamma flip at 694.26 aligns tightly with the put wall at 694.00, establishing a hard floor where the regime flips from suppressive to accelerative. Spot well above both confirms deep positive gamma — dealers buy every dip within the corridor and sell every rally into the wall.

0DTE accounts for 35.7% of total GEX — substantial intraday dampening that evaporates at the close, opening a window for directional resolution in the final hour as that gamma rolls off the book.

What it means for your trading

Deep positive gamma pins spot within the 694.00–700.00 corridor with the call wall as the active ceiling; elevated 0DTE share at 35.7% of total GEX means suppression weakens materially into the close, creating late-session breakout risk.

Trading readDeep positive gamma concentrated at the call wall creates a hard ceiling for today's rally — dealers sell into strength at that level and buy dips above the flip. Fade moves into the wall and only chase a breakout if spot holds above it on sustained volume.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Vanna exposure at -$197.87B is deeply negative — a VIX spike from here forces dealers to sell delta into the downdraft, flipping the suppressive gamma cushion into a self-reinforcing accelerant. The positive_gamma regime dampens small moves, but vanna overwhelms gamma on any meaningful vol expansion. That asymmetry is the hidden fragility beneath today's calm tape.

Charm exposure at -$20.6M compounds the directional drag: time decay pushes dealers toward selling into the close, adding programmatic supply into the final hour as 0DTE gamma rolls off. The charm pivot sits at 700 — coincident with the 700.00 call wall — with neutral bias. A sustained break above that level flips charm flow from headwind to tailwind; below it, the selling pressure accumulates into each session's close.

Net: gamma suppresses, but vanna and charm erode the cushion directionally. Respect the pivot as the fulcrum — it is where the regime's character changes.

What it means for your trading

Negative vanna and charm exposure create a latent accelerant beneath the positive gamma surface — any vol spike converts dealer hedging from dampening to amplifying. The charm pivot at 700 is the single level where flow direction toggles; fade into it, but do not fight a sustained break.

Cross-Asset Confirmation

Cross-asset confirmation is unambiguous: SPY, QQQ, and IWM all hold in positive_gamma with regime divergence aligned — the broadest suppressive alignment the complex has printed since the March lows. MOVE at 74.35 keeps bond vol moderate with no credit-stress signal bleeding into equities, while Fear & Greed at 54 (neutral) sits in no-man's-land — no sentiment extreme to fade, no contrarian trigger to pull. The dollar shedding its Iran war premium confirms FX and equity vol are pricing the same de-escalation thesis in lockstep.

QQQ at 633.73 and IWM at 268.72 are both spot-above-flip with VIX term structure in contango, confirming carry is available across the board. Critically, IWM's thinner gamma cushion makes it the canary — if the ceasefire narrative fractures, small-caps crack first and regime divergence surfaces there before it reaches SPY. Today that divergence is absent, reinforcing the coordinated bid.

Key distinction: this is a geopolitical de-escalation trade, not a fundamental growth upgrade. These trades mean-revert violently on headline reversals. The macro backdrop supports selling structure within defined risk — but position for the snap-back, not the breakout.

What it means for your trading

Full cross-asset alignment in positive_gamma with MOVE at 74.35 and sentiment at neutral confirms a coordinated de-escalation bid — no credit stress, no sentiment extreme, and no regime divergence — but geopolitical trades unwind fast, so defined-risk structures dominate naked directional exposure.

Scenario EV

iron_condor scores highest at 47 in the current regime — positive_gamma suppression plus contango carry create the textbook premium-collection setup. The optimal DTE window of 30-45 sessions captures the steepest roll-down on the term structure curve, sitting beyond the intraday chop zone where 35.7% of GEX evaporates nightly while harvesting front-end theta before back-month event risk thickens.

The headwind is real: VRP at -6.52% means realized vol still outpaces implied across the complex — you are selling options that are genuinely cheap to recent moves. Tighter wings are warranted. Center the structure around the charm pivot at 700 where dealer flow bias sits neutral, and cap the upside leg at the call wall near 700.00. Put spreads score materially lower at 35 — directional conviction is absent when all three indices hold aligned positive gamma.

Size standard per VVIX at 99.37 — standard_size applies. The regime is Elevated / Watchful, not panicked; defined-risk structures collect carry while respecting the transitional state.

What it means for your trading

Iron condors in the 30-45-session window offer the highest expected value at 47, but negative VRP demands tighter wings and disciplined sizing — sell the regime, not the vol level.

Actionable Summary

Sell structure, not direction. All indices hold in positive_gamma, term structure sits in contango, and VVIX reads normal — the trifecta for defined-risk premium collection. iron_condor in the 30-45 DTE window, centered on the charm pivot at 700 where dealer bias is neutral, captures contango roll-down while gamma suppression enforces the 694.00-to-700.00 corridor.

Avoid naked short puts — VRP at -6.52% confirms options are cheap to realized moves, leaving unhedged downside uncompensated. Skip naked long gamma while vol-of-vol holds normal with standard_size sizing — no binary premium to harvest. The call wall at 700.00 caps rallies; the gamma flip at 694.26 is the trapdoor where suppression becomes acceleration. Net vanna at -$197.87B means a vol spike flips dealers to sellers — keep wings defined.

Regime: Elevated / Watchful with a half-life of 15 sessions — transitional, not sticky. The VVIX/VIX divergence and Iran ceasefire headlines are the toggle switches. Position for vol compression as the base case; hedge the reversal with defined-risk wings, not directional bets.

What it means for your trading

iron_condor centered on 700 offers the highest EV in a Elevated / Watchful regime, collecting contango carry within the 694.00-to-700.00 corridor. Negative VRP at -6.52% demands tighter wings and defined risk — naked exposure is uncompensated.

Overbought-territory warnings after a V-shaped recovery from March lows raise positioning risk — crowded longs are vulnerable to any ceasefire headline reversal, reinforcing the case for defined-risk structures over naked directional exposure.

Strait of Hormuz closure preparedness highlights the energy tail risk still embedded in the geopolitical backdrop — even as markets price de-escalation, a shipping disruption would spike commodities and re-invert the vol term structure overnight.

EU energy shock warning introduces a second-order consequence: if the Iran conflict persists, European industrial demand destruction becomes a global growth headwind that equity vol hasn't fully priced.

Turkey's ceasefire extension effort is the proximate catalyst compressing risk premiums today — progress here sustains the vol carry trade; failure re-ignites the war premium the dollar just shed.

Bank of America earnings kick off the big-bank reporting wave — strong results validate the overbought rally and financial-sector resilience; a miss would break the cross-sector confirmation pattern the market is relying on.

Dollar shedding its Iran war premium confirms the FX market agrees with equity's de-escalation bet — currency and equity vol moving in tandem strengthens the macro coherence of the current suppressive regime.

The single most important macro headline: markets betting the Iran war is over. If correct, vol compresses further and the regime transitions to low; if wrong, this is the crowded trade that unwinds the fastest.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.01 with a contango term structure. The Fear & Greed index reads neutral, and cross-asset volatility is aligned across SPY, QQQ, and IWM.

Is SPY in positive or negative gamma today?

SPY is in positive_gamma gamma with net dealer GEX at $10.87B. The gamma flip sits at 694.26, with the call wall at 700.00 and the put wall at 694.00.

Where is the SPY gamma flip level right now?

SPY's gamma flip is at 694.26 against a spot of 697.37. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 13.53% with a volatility risk premium of -6.52%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in contango with VIX at 17.96. Contango signals benign forward expectations; backwardation signals near-term stress.

What's the dealer positioning on QQQ and IWM?

QQQ shows positive_gamma gamma with net GEX at $7.58B (flip: 625.46). IWM shows positive_gamma gamma with net GEX at $487.9M (flip: 259.90).

Get today's live analysis

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime