Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

Positive gamma pinning near call walls as market digests geopolitical risk in Elevated / Watchful regime

Equity indices closed higher with SPX touching intraday records despite the Iran-war overhang — all three ETFs sit in positive_gamma with spot above their gamma flip levels. The paradox today is negative VRP across the board: realized volatility continues to exceed implied, meaning options are cheap to actual moves even as VIX term structure holds steep contango at contango. Dealers are long gamma and pinning spot near the 700.00 call wall, but the deeply negative vanna exposure (-$199.87B) warns that any vol spike would flip the supportive flow sharply negative.

Regime Assessment

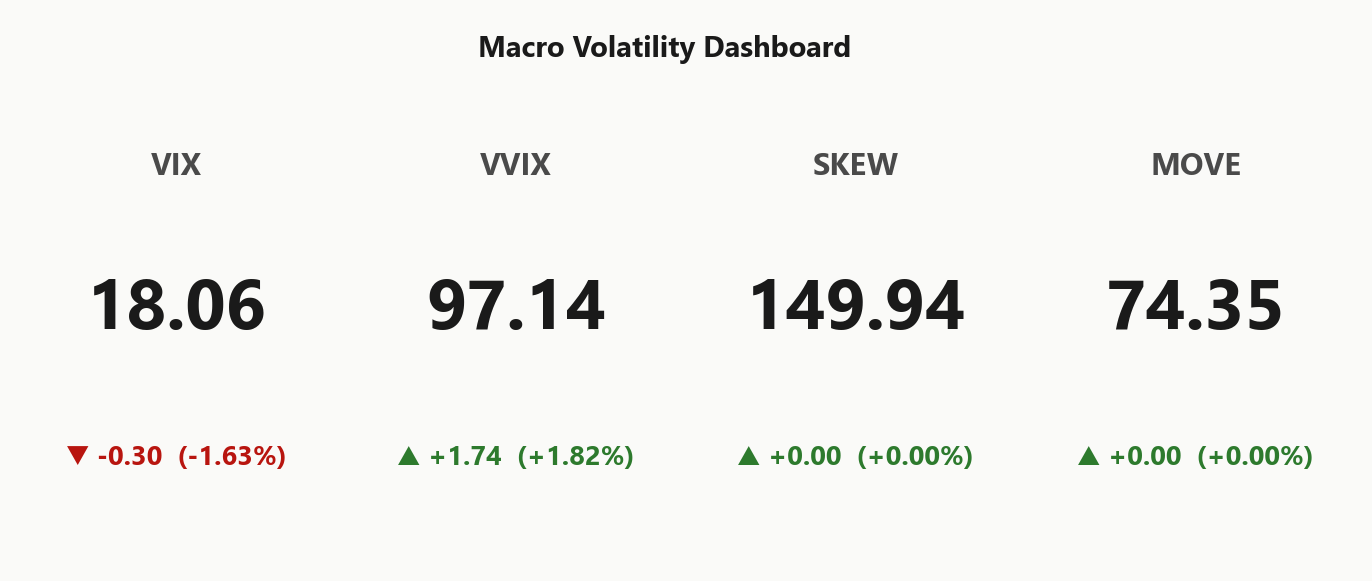

The vol regime sits at elevated — Elevated / Watchful — with VIX at 18.06, above the long-run median but well short of stress thresholds. Positive gamma across SPY, QQQ, and IWM provides a mechanical dampener that keeps realized moves compressed, while the Iran overhang prevents the term structure from collapsing into the low-vol regime the contango curve would otherwise imply.

This regime is moderately sticky: half-life of 15 sessions argues against positioning for a rapid transition in either direction. The path to panic requires a discrete vol catalyst — Hormuz escalation, an earnings shock, or a VVIX breakout — none of which carry elevated near-term probability given de-escalation signals in the diplomatic channel. The path to low-vol is more plausible over a medium-term horizon but remains gated by the geopolitical risk premium embedded in back-month tenors.

Net: the watchful state persists. Structures that benefit from range compression and carry extraction fit this regime; directional vol bets require a catalyst not yet present in the data.

What it means for your trading

Elevated but anchored regime with a half-life of 15 sessions favors carry-harvesting structures over directional vol positioning — the positive gamma cushion suppresses downside acceleration while the Iran-driven risk premium prevents a collapse to low-vol.

Trading readVIX declining while VVIX rises is the divergence to watch — headline vol is calming but the distribution of vol outcomes is widening. SKEW holding elevated and MOVE subdued confirms this is an equity-vol story, not a rates-credit contagion — classic geopolitical shock pattern that tends to mean-revert.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

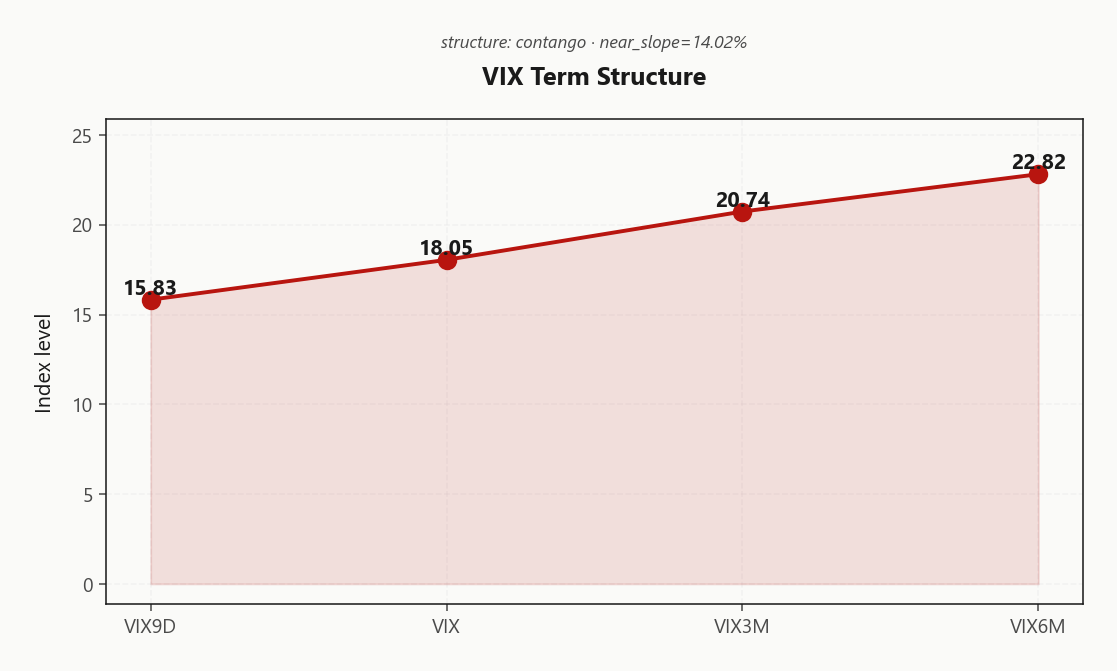

The full VIX curve sits in contango from 15.83 through 18.05 to 20.74 and out to 22.82 — a clean upward slope that confirms structural carry for vol sellers at every tenor. Near-term event premium has fully deflated post-session, with VIX9D well below spot VIX and the near slope running at 14.02%%, leaving the steep_contango regime firmly intact. The futures basis at 14.84%% contango — front month at 20.74 versus spot 18.06 — provides additional roll-down carry for short vol books.

Forward vol tells a more nuanced story. The implied forward between the one-month and two-month tenors steepens to —, while the two-to-three-month forward pushes higher still at 24.7256385155 — the curve is pricing geopolitical tail risk into the back months even as near-dated vol compresses. Back-month vol at 22.82 remains elevated, anchoring the Iran-related premium in tenors beyond where dealers can easily arbitrage it away.

The carry edge is steepest in the front of the curve: sell near-term premium where contango decay is most aggressive, roll systematically, and let the steep_contango regime do the work. The optimal DTE window sits in the 30-45-day range where the slope-to-theta ratio is richest.

What it means for your trading

steep_contango across the VIX term structure favors front-month premium selling with systematic rolls — the steepest carry sits inside 30-45 DTE, but back-month vol at 22.82 warns the curve is still embedding geopolitical tail risk that near-term compression has not resolved.

Trading readClean contango from spot through six-month tenors says the vol carry trade is on — but the steepness itself tells you the market expects VIX to climb, just not today. The spread between spot and front-month futures is wide enough to fund tail hedges with the carry.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

The vol risk premium is flashing danger_zone for premium sellers. SPY ATM IV at 13.89% sits well below realized vol on a trailing basis — HV20 at 20.14 — yielding a VRP of -6.25%. Options are meaningfully cheap to the moves the market is actually delivering. This is not an SPY-specific anomaly: QQQ carries a VRP of -5.15% and IWM prints -3.59%, confirming the mispricing is broad-based across the equity complex.

The wrinkle is tenor. Near-term realized vol has decelerated sharply — RV5D at 7.71 already converging back toward implied — while HV60 at 15.81 sits closer to current ATM IV, suggesting the recent spike in realized is the statistical outlier. But with Iran tail risk still embedded in back-month vol and the conflict unresolved, dismissing the elevated HV20 print as mean-reverting feels premature. Selling vol here means selling cheap; the edge favors owning wings or waiting for IV to re-price higher before engaging short premium.

What it means for your trading

Negative VRP across SPY, QQQ, and IWM flags a danger_zone environment where implied vol has not caught up to recent realized moves — avoid naked premium selling until the spread normalizes or RV decelerates further toward the 7.71 trajectory.

Skew Convexity

SPY quarter-delta skew prints 2.61% with a smile ratio of 1.21% — puts are getting bid in orderly fashion, consistent with institutional hedging demand rather than crash-fear convexity. The put-ATM-call ladder reads 14.95% / 13.37% / 12.34%, a standard defensive tilt that lacks the steep wing premium you'd expect with an active geopolitical conflict priced in. Flat call skew confirms the options market is not endorsing the record-high equity tape with leveraged upside conviction.

QQQ skew runs steeper at 2.94% with smile ratio 1.16%, reflecting more pronounced tech hedging demand — mega-cap concentration risk commands a higher downside premium. The cross-complex read: protective structures are being added methodically, not urgently. Spread-based downside protection is favored over naked puts — the orderly skew shape means you capture the steepness without paying for dislocation that isn't there.

What it means for your trading

Skew is elevated but disciplined — hedging, not panic — with flat call wings flagging zero upside conviction despite equity records. Favor put spreads over outright puts to monetize the steep smile ratio at 1.21% without overpaying for tail convexity.

Vol-of-Vol Structure

VVIX at 97.14 sits in normal territory — remarkable given an active geopolitical conflict backdrop. The vol-of-vol market is explicitly refusing to price bimodal outcomes, with the VVIX/VIX ratio at 5.38 well below the threshold that would warrant defensive position scaling. Sizing guidance: standard_size applies across the book.

The subtlety worth flagging: VVIX ticked higher by 1.82%% on the session even as VIX at 18.06 drifted lower — a nascent divergence. When vol-of-vol leads headline vol higher, it often signals the distribution of outcomes is widening before the market reprices the mean. This is how jump risk gets marked in early innings: not through VIX itself, but through the convexity of VIX options quietly bid underneath.

No action required yet — but if VVIX continues climbing against a falling VIX into tomorrow's session, that divergence becomes a leading indicator worth hedging against, particularly given the deeply negative vanna exposure that would amplify any vol spike into a dealer-driven selloff.

What it means for your trading

Vol-of-vol at normal with standard_size guidance confirms no embedded jump premium — but the intraday VVIX-VIX divergence is the canary, and the negative vanna backdrop means any repricing of tail risk would cascade faster than the normal label suggests.

Dispersion Spread

The index diversification discount is wide and actionable: SPY ATM IV at 13.89% trades meaningfully below QQQ at 19.16% and IWM at 21.05%, reflecting the dampening benefit of broad-basket hedging while single-name vol remains elevated. Cross-asset regimes are aligned — all three indices sit in positive_gamma with spot above their respective gamma flips, leaving no inter-index dislocation to exploit.

Dispersion opportunity is compressed. The top GEX movers — NVDA, AAPL, MSFT, AMZN, META — all shifted positive in lockstep, collapsing the idiosyncratic spread that dispersion traders need. Cross-strike IV dispersion at {"cross_expiry":2.62,"cross_strike":69.77} confirms the surface is orderly, not dislocated. When mega-caps rally in unison beneath a uniform dealer regime, single-name vol sells rich relative to the index.

Favor SPY/SPX premium structures over single-name equivalents here — the deeper gamma cushion and lower implied base give index vol sellers a structurally better entry than chasing richer but more fragile single-stock IV.

What it means for your trading

With cross-asset regimes aligned and mega-cap flows moving in lockstep, the dispersion bid is thin — index-level vol selling in SPY at 13.89% offers cleaner carry than single-name strategies priced off richer but correlated individual surfaces.

Liquidity & Microstructure

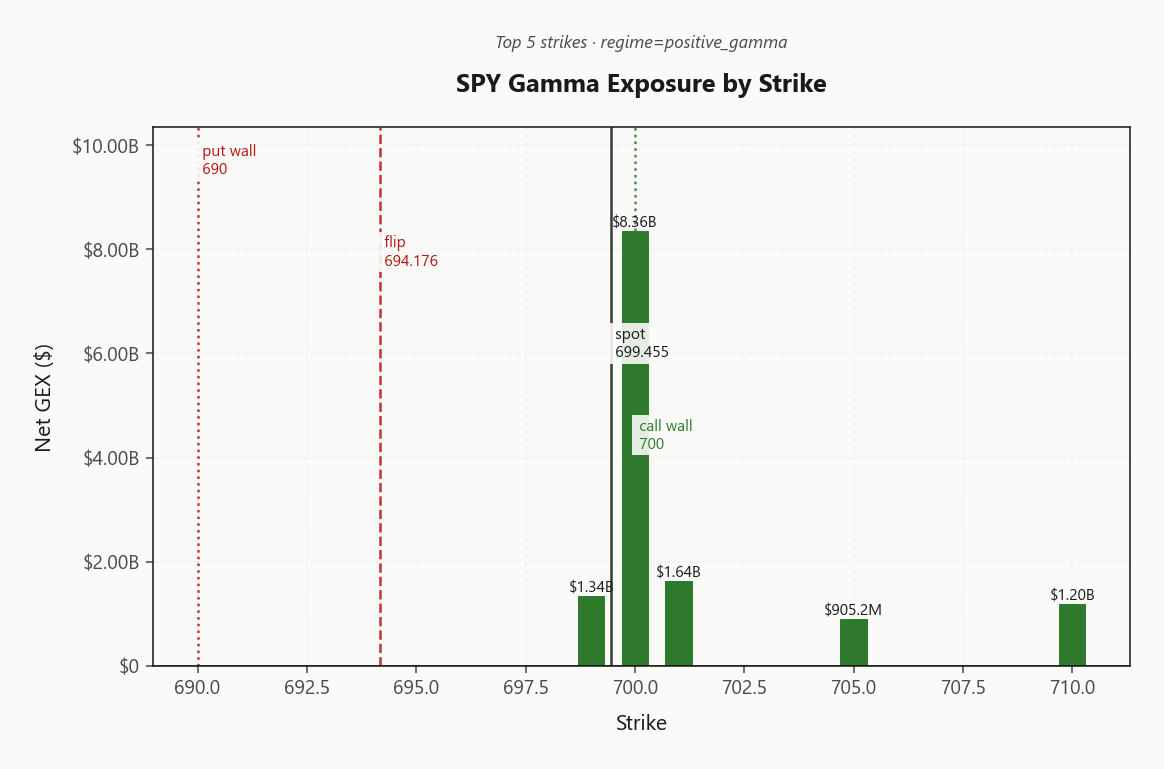

Massive open interest concentration at the 700.00 strike — carrying $8.36B in net GEX — anchors the tape to a single gravity well. The call wall at 700.00 caps upside; the put wall at 690.00 floors the near-term range. Spot trades above the gamma flip at 694.18, keeping dealers in positive_gamma — buying dips, selling rips, dampening every directional impulse. The highest OI strike at 600 reflects legacy put positioning, not today's magnet.

Zero-DTE flow accounts for 50.7% of total GEX, meaning intraday gamma resets overnight and tomorrow's microstructure may look entirely different. QQQ mirrors the setup with its call wall at 637.00 pinning spot at the same level — cross-asset dealer positioning is synchronized, reinforcing the dampening regime but also ensuring any catalyst that breaks one index threatens to flip them all simultaneously.

Breakout attempts above the call wall face mechanical dealer selling; dips toward the put wall trigger mechanical buying. Range compression is the base case until the 694.18 gamma flip is breached.

What it means for your trading

Dealer gamma is deeply concentrated at the 700.00 call wall, creating a suppressive pinning regime that favors mean-reversion and iron condors over directional bets — but the entire structure hinges on spot holding above the 694.18 flip, below which dampening converts to amplification.

Trading readConcentrated positive gamma at the call wall creates a powerful magnet — expect dealers to aggressively fade moves in both directions, making breakouts expensive and mean-reversion the dominant intraday playbook. The gamma flip level is the tripwire: below it, the dampening flips to amplification.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Beneath the supportive positive-gamma surface lies a coiled vanna spring. SPY net vanna exposure sits at -$199.87B — deeply negative and outsized relative to the gamma cushion. Any meaningful vol expansion forces dealers to sell delta mechanically, converting today's dampening regime into a self-reinforcing accelerant on the downside. QQQ vanna at -$5.51B skews the same direction but at far smaller magnitude, making SPY the clear epicenter of convexity risk should implied vol reprice.

Charm adds a quieter drag. Net CHEX at -$1.3B bleeds mild selling pressure into every close as time decay works through the book. The charm pivot at 700 — the call_wall — sits just 0.0779178074% from spot, holding bias at neutral. Dealers are balanced here, but the asymmetry is stark: a vol spike doesn't just erode gamma support — it weaponizes the vanna book against the tape.

What it means for your trading

Positive gamma pins the tape near the charm pivot at 700, but the deeply negative vanna exposure (-$199.87B) means any vol catalyst flips supportive dealer flow into mechanical selling — treat the calm surface as fragile until VEX magnitude compresses.

Cross-Asset Confirmation

Cross-asset regimes read aligned — SPY, QQQ, and IWM all sit in positive_gamma with spot above their respective gamma flips, leaving dealers uniformly long gamma and dampening moves across the equity complex. The MOVE index at 74.35 confirms the Iran conflict remains an isolated geopolitical event, not a credit contagion: bond vol is contained while SPX prints intraday records at 7022.95. Breadth confirms — QQQ at 636.78 and IWM at 269.08 both participated in the session's advance, ruling out a narrow mega-cap carry.

Fear & Greed at 57 (greed) is the contrarian flag worth noting: sentiment is warming toward complacency territory just as the tape tags records into a geopolitical overhang. Uniform dealer positioning creates synchronized dampening today, but also means any shock that breaches one index's gamma flip likely cascades across the complex simultaneously. VIX in negative_gamma on the other side of the ledger is the accelerant — a headline-driven vol spike meets negative gamma there first, then threatens the equity indices' flip levels in sequence.

What it means for your trading

Cross-asset alignment in positive_gamma with subdued MOVE at 74.35 supports range-bound structures, but the uniform positioning cuts both ways — synchronized dampening today becomes synchronized fragility if any single flip level breaks on an escalation catalyst.

Scenario EV

The regime scores iron_condor as the optimal structure at 39, a moderate-conviction setup anchored by positive_gamma dampening and steep contango carry across the curve. The 30-45-day DTE sweet spot captures the steepest forward-vol gradient — front-month premium rolls off fastest here while back-month protection stays cheap. Center the condor around the 700 charm pivot where dealer flows are neutral, and let the 700.00 call wall and 690.00 put wall define your wing boundaries.

The complication is the VRP read: unknown across the complex, with SPY implied at 13.89% lagging realized vol at 20.14. You are selling cheap premium into a tape that moves more than the surface suggests. Widen wings accordingly — the carry edge from contango subsidizes the extra width, and VVIX at 97.14 (normal) confirms no jump-risk premium demanding tail overhedges. Put spreads score 26, but with cross-asset regimes aligned and all indices above their gamma flips, outright directional conviction lacks structural support.

What it means for your trading

Iron condors score 39 in the 30-45-day window — a defensible but not aggressive setup where contango carry funds the trade but negative VRP (-6.25%) warns against tight wings.

Actionable Summary

Elevated / Watchful regime with positive gamma across SPY, QQQ, and IWM favors defined-risk, range-bound structures. Recommended: iron_condor in SPY centered on the 700 charm pivot, targeting the 30-45-day DTE window where contango carry is steepest. Score: 39 — moderate conviction, not a table-pounding setup. Negative VRP (-6.25%) means vol is cheap to realized across the complex — widen wings rather than selling naked premium into underpriced implied.

The 694.18 gamma flip is the downside tripwire: breach converts supportive dealer hedging into amplifying delta supply. Deeply negative vanna (-$199.87B) is the accelerant — any vol spike overwhelms the gamma cushion. VVIX at 97.14 ticking higher while VIX drifts to 18.06 is an early divergence worth monitoring for jump-risk repricing.

Avoid naked short vol and aggressive upside calls — skew shows no conviction above the 700.00 call wall. Size at standard_size per VVIX guidance. The Iran backdrop remains a latent vol catalyst, but cross-asset regimes aligned and record SPX prints say the tape is pricing de-escalation.

What it means for your trading

iron_condor anchored to the 700 charm pivot in 30-45-day DTE captures contango carry while the Elevated / Watchful regime pins spot — but respect the negative VRP and geopolitical tail by widening wings and treating the 694.18 gamma flip as a hard stop.

SPX tagging intraday records for the first time since the Iran conflict began signals the market is pricing de-escalation — a sentiment inflection that reshapes the vol surface and dealer positioning outlook.

Iran offering a Hormuz shipping corridor is the most concrete de-escalation catalyst today — directly reduces the energy supply-chain tail risk that has kept back-month vol elevated.

Import prices rising below expectations but with a sharp increase anticipated from the Iran war sets up a delayed inflation impulse — rates vol and equity vol may decouple if this materializes in coming prints.

Trump asking Xi to cut off Iranian weapons supply internationalizes the conflict — if China complies, de-escalation accelerates; if not, the geopolitical risk premium widens beyond the Middle East.

EU warning of prolonged energy shock and forced cuts if the conflict continues is a macro tail-risk anchor — European exposure names and energy-sensitive sectors carry asymmetric downside from here.

Congressional probe into Hormuz closure preparedness highlights structural energy supply risk still unpriced in near-term vol — a policy catalyst that could re-steepen the term structure.

US rejection of Russia's uranium proposal signals diplomatic deadlock on the nuclear dimension — keeps the conflict tail heavier than the equity market's record-high tape implies.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.17 with a contango term structure. The Fear & Greed index reads greed, and cross-asset volatility is aligned across SPY, QQQ, and IWM.

Is SPY in positive or negative gamma today?

SPY is in positive_gamma gamma with net dealer GEX at $16.72B. The gamma flip sits at 694.18, with the call wall at 700.00 and the put wall at 690.00.

Where is the SPY gamma flip level right now?

SPY's gamma flip is at 694.18 against a spot of 699.45. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 13.89% with a volatility risk premium of -6.25%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in contango with VIX at 18.06. Contango signals benign forward expectations; backwardation signals near-term stress.

What's the dealer positioning on QQQ and IWM?

QQQ shows positive_gamma gamma with net GEX at $2.86B (flip: 633.02). IWM shows positive_gamma gamma with net GEX at $519.8M (flip: 263.90).

Get today's live analysis

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime