Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

Steep contango + deeply negative VRP: options mispriced cheap beneath a neutral tape as geopolitical risk simmers

Equity indices push higher despite escalating Iran-Hormuz headlines, with VIX at 18.09 falling in steep contango from 16.74 through 20.55 to 22.58. The disconnect: realized vol exceeds implied across SPY (VRP -5.61%), QQQ (VRP -6.43%), and IWM (VRP -3.27%) — options are cheap to the moves actually being delivered. QQQ sits in negative_gamma while SPY reads unknown, a cross-asset divergence that typically precedes directional resolution.

Regime Assessment

The vol regime reads elevated — Elevated / Watchful — with VIX at 18.09 and a half-life of 15 sessions. This is a moderately sticky elevated state: not panicked, not complacent, but priced for watchful continuation. Full contango across the term structure and suppressed VVIX confirm the market's base case is diplomatic resolution, not escalation.

Transition math reinforces the thesis. Near-term panic probability sits at — — the tape is pricing Islamabad talks as a de-escalation vector, not a binary catalyst. Medium-term reversion to low vol scores —, reflecting moderate odds of normalization if the geopolitical overhang clears. The asymmetry: regime decay is gradual on resolution, but re-escalation reprices abruptly.

Two macro catalysts offset: Bessent's pivot away from rate-cut urgency removes a dovish tailwind that had been compressing vol expectations, while peace-talk optimism provides a countervailing lid on fear. Net effect is regime stasis — elevated but range-bound until one catalyst dominates.

What it means for your trading

Vol regime is Elevated / Watchful with a 15-session half-life — sticky enough to structure around but with moderate reversion probability at — if Islamabad delivers, and negligible panic risk at — unless talks collapse and Hormuz enforcement tightens.

Trading readVIX dropping while VVIX also compresses — both confirming the de-escalation narrative. But SKEW holds elevated at 156.93, meaning tail risk hasn't repriced even as headline vol fades. The divergence between SKEW stability and VIX decline is the subtle warning that hedgers aren't standing down. MOVE is quiet, confirming equity-specific stress.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

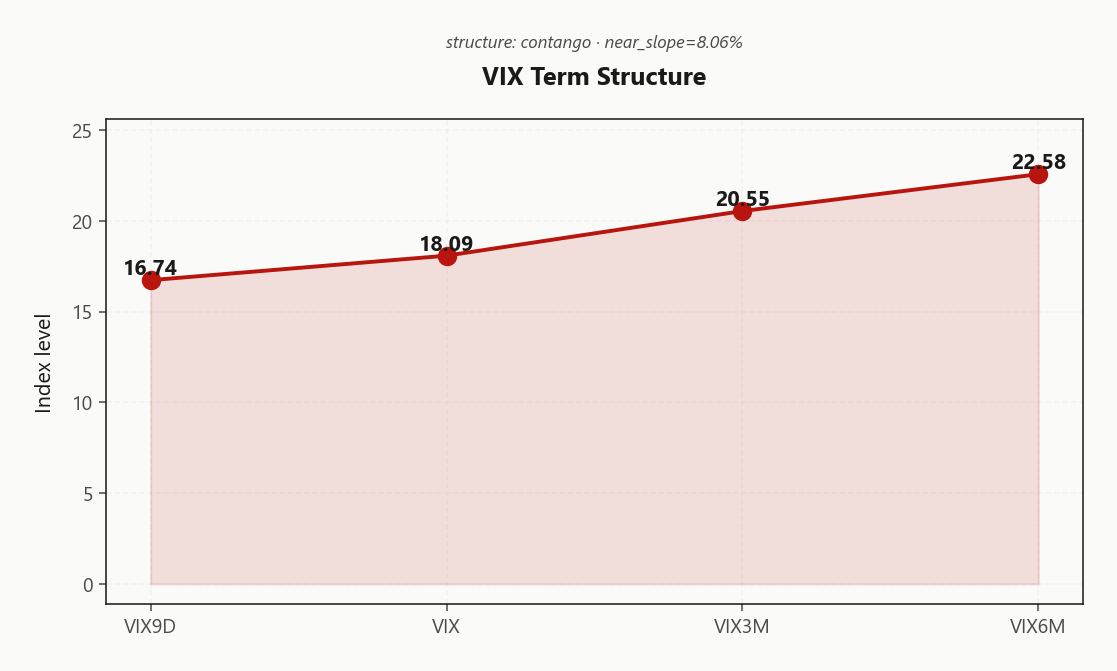

The VIX term structure prints full contango from 16.74 through 18.09 to 20.55 and out to 22.58 — front vol priced cheapest despite an active Hormuz blockade. The near slope at 8.06% confirms no event premium embedded in short-dated expiries: the market has fully discounted imminent escalation.

Forward vol regime reads steep_contango — Steep contango — vol sellers favored. VIX futures basis at 13.6% contango means structural roll-down accrues to short vol positions passively. The carry is real and compounding, but it sits atop a geopolitical fault line that reprices in hours, not sessions.

Best edge concentrates where the curve steepens most: calendar and diagonal spreads selling the front leg against longer-dated wings capture maximum roll-down while maintaining convexity against a VIX spike. Defined-risk structures only — naked front-month selling into this backdrop ignores the binary that Islamabad represents.

What it means for your trading

Steep contango with steep_contango regime and 13.6% futures basis delivers structural carry — calendars and diagonals exploiting the steepest part of the curve offer the best risk-adjusted edge while Islamabad talks remain the unpriced binary catalyst.

Trading readFull contango from spot through six-month with substantial futures basis says the carry trade is alive — vol sellers collect structural roll-down. But the steep slope also means the market expects vol to stay elevated longer-term. Sell the front, respect the back.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

Realized vol is running well above implied across the entire index complex, and the gap is not subtle. SPY posts a VRP of -5.61% with HV20 at 19.73 against ATM IV of just 14.12% — options are materially cheap to the moves being delivered. HV60 at 15.58 confirms this is not a transient spike; the realized regime has been running hot for weeks.

QQQ carries the widest dislocation at -6.43% VRP, with HV20 printing 23.35 versus ATM IV of 16.92% — tech has moved far more than its options priced. IWM's VRP at -3.27% is the narrowest of the three, making small-caps the relatively cleaner venue if short premium is the mandate.

Negative VRP persisting during an active geopolitical catalyst cycle is a warning, not an invitation. Naked short premium fights the tape here — defined-risk structures with wings are mandatory until the realized-implied spread compresses back toward zero.

What it means for your trading

Options are definitively mispriced cheap across SPY, QQQ, and IWM with QQQ showing the widest VRP gap at -6.43%. Selling naked premium into negative VRP and live geopolitical catalysts is swimming upstream — prefer defined-risk wings and treat IWM (VRP -3.27%) as the least-bad short-vol venue.

Skew Convexity

SPY quarter-delta skew prints 2.64% with a smile ratio of 1.21% — moderate downside premium that reads as orderly institutional hedging, not panic-bid protection. Put quarter-delta IV at 15.18% versus ATM at 13.5% confirms the skew is steep but structured. Critically, call quarter-delta IV at 12.54% sits flat to ATM — the rally is entirely spot-driven with zero upside conviction expressed through vol markets.

QQQ tells a more defensive story: skew widens to 3.04% with smile ratio at 1.2%, reflecting elevated hedging demand concentrated in tech. The wider QQQ skew aligns with its negative_gamma regime — hedgers are paying up where dealer amplification makes downside velocity highest.

Structurally, put spreads dominate over naked puts here. Deeply negative VRP across the complex means long put legs retain edge while short wings defray cost — defined-risk downside exposure without fighting realized vol on the short strike.

What it means for your trading

Skew is steep but disciplined — institutional hedges accumulating without tail panic. Flat call skew confirms the tape lacks upside conviction through vol; fade the rally via put spreads in QQQ where skew and negative gamma converge.

Vol-of-Vol Structure

VVIX prints 99.29 against a VIX of 18.09 — vol-of-vol sitting at normal with no jump-risk premium embedded. That reading is remarkably complacent for a tape running an active Hormuz blockade and unresolved Iran escalation. The market is pricing a single-mode outcome — diplomatic resolution via Islamabad — and discounting the bimodal tail entirely. Sizing guidance holds at standard_size, meaning standard position sizes are appropriate and no convexity surcharge is being demanded.

This is where the mispricing hides. VVIX declining while geopolitical catalysts remain live flags a conditional calm that could unwind violently. If Islamabad talks collapse this week, the repricing from normal toward stress levels would be swift and asymmetric — the gap between current complacency and the magnitude of the outstanding risk is wider than the headline VIX suggests. Owning vol-of-vol optionality here is cheap precisely because nobody is bidding it.

Positioning implication: structures with defined wings carry embedded VVIX insurance at minimal cost. Naked short premium, by contrast, is implicitly short a VVIX spike — and that spike is one failed phone call away.

What it means for your trading

VVIX at 99.29 reads normal despite active military conflict — the market has fully discounted geopolitical tail risk, creating asymmetric repricing potential if Islamabad peace talks fail; standard_size sizing holds but defined-risk structures are mandatory given the conditional nature of the calm.

Dispersion Spread

SPY ATM implied vol at 14.12% sits well below QQQ at 16.92% and IWM at 21.17% — index-level hedging is compressing broad-market vol while single-name activity runs hot underneath. The spread between SPY and QQQ implied vol alone flags an elevated dispersion regime: constituent moves are outpacing what the index surface reflects.

NVDA and META lead the single-stock GEX shift leaderboard by orders of magnitude over the next-ranked names, confirming that mega-cap gamma repositioning is the engine behind the dispersion widening. All top-five movers are accumulating positive gamma individually, yet QQQ remains pinned in negative_gamma — index-level put structures, not single-stock selling, are driving that divergence.

The trade implication is clean: sell index vol, respect single-name vol. SPY/SPX gamma is structurally more stable and benefits from the hedging compression, while single-stock dispersion makes naked short premium on individual names a rougher carry. Let the index absorb the theta; let the names move.

What it means for your trading

Index implied vol is being artificially suppressed by portfolio hedging flows while single-stock dispersion runs elevated — favor SPY/SPX vol selling over single-name structures until the 14.12%-to-16.92% spread compresses.

Liquidity & Microstructure

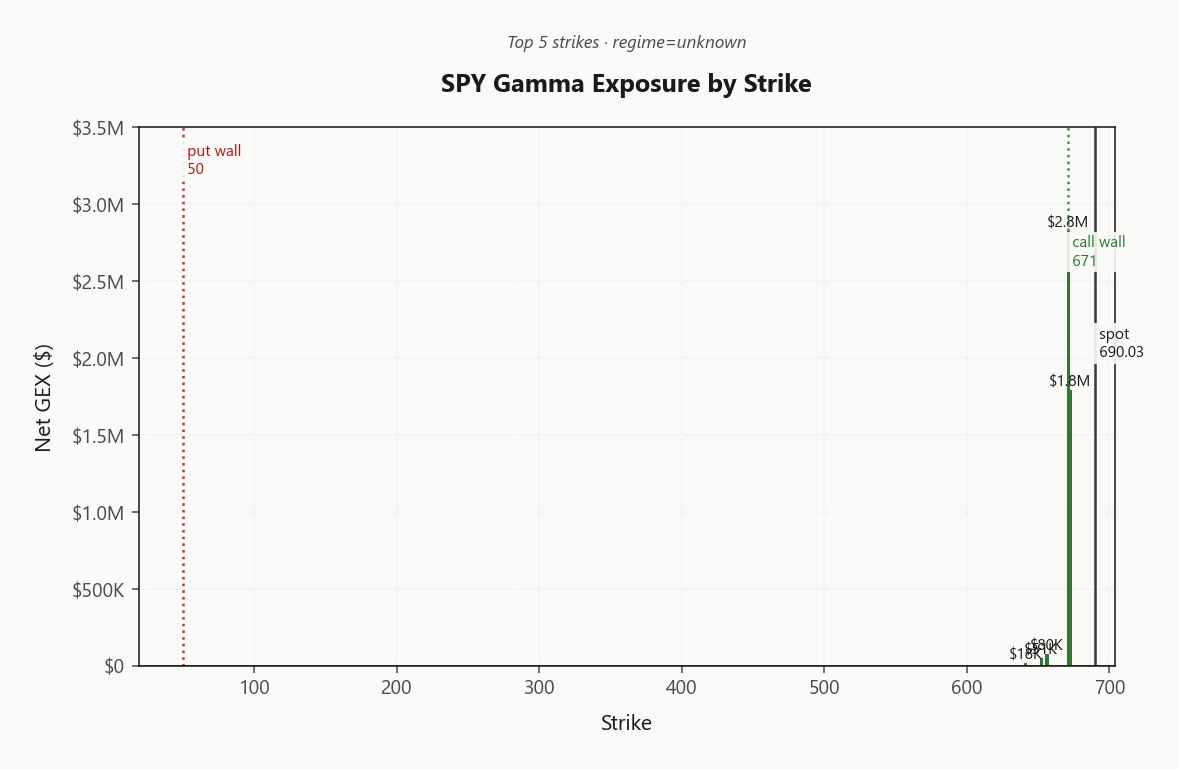

SPY open interest clusters at 671, coinciding with the call wall at 671.00 — dealers are pinned to a single magnetic strike carrying $2.8M net GEX. That concentration creates a well-defined resistance zone but leaves gamma sparse on either side, thinning the cushion for any directional break. The put wall at 50.00 sits far below, offering no meaningful downside anchor.

The structural fragility: 96.4%% of SPY gamma is 0DTE. Nearly all dealer hedging resets at the close, leaving overnight positioning naked. SPY's gamma flip at — is undefined, making regime classification ambiguous — intraday mean-reversion is real but structurally ephemeral.

QQQ tells the cleaner story: gamma flip at 628.00 with spot below it in negative_gamma. Dealer hedging amplifies directional moves in tech — trend-following mechanics dominate until spot reclaims the flip. Fade SPY into the call wall intraday, but respect that the cushion evaporates at the bell.

What it means for your trading

SPY gamma is almost entirely 0DTE and concentrated at 671.00, creating intraday mean-reversion that vanishes at the close. QQQ in negative_gamma below its 628.00 flip amplifies tech directional moves — after-hours risk is structurally unhedged.

Trading readSPY gamma is concentrated in a narrow band near the call wall — dealers are anchored there, creating a magnetic pull on spot. Below that cluster, gamma thins out rapidly, meaning a break lower finds no dealer cushion until much further down. Fade moves toward the wall, but if it breaks, expect acceleration.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

SPY net vanna sits at -$27.5M — negative exposure that forces dealers to sell delta on any vol uptick, mechanically amplifying downside. Net charm at -$35.9K reinforces the same directional bias: time decay pushes dealers to shed delta into the close. Both greeks are directionally aligned bearish, stacking afternoon selling pressure at precisely the window where geopolitical headlines tend to land.

The charm pivot anchors at 671 with a neutral read — spot trades above the pivot, keeping dealer flow balanced for now, but a vol spike flips that equilibrium fast. QQQ is where the real vulnerability concentrates: vanna exposure at -$987.7M dwarfs SPY by an order of magnitude, with charm at -$564.3K compounding the pressure. Tech is the fragility locus — any vol expansion hits QQQ's dealer book hardest, making it the leading indicator for forced-flow acceleration across the index complex.

What it means for your trading

Vanna and charm are aligned bearish across both SPY and QQQ, with QQQ vanna at -$987.7M flagging tech as the amplification center if vol reprices higher — fade afternoon rallies and watch for charm-driven selling into the close.

Cross-Asset Confirmation

MOVE at 74.42 is the single most important cross-asset read today: bond vol refuses to confirm the equity stress narrative. Despite active Hormuz blockade headlines and Iran escalation, fixed-income implied vol sits well below crisis thresholds — this is geopolitical noise, not credit contagion. Geopolitical shocks carry shorter half-lives than credit events, and MOVE is confirming exactly that taxonomy.

Fear & Greed at 46 (neutral) during active military conflict is itself the signal — the market has front-run diplomatic resolution via Islamabad. QQQ at 622.24 running negative_gamma while SPY holds unknown confirms the cross-asset regime divergence flagged in positioning. IWM at 267.41 trades between the two, offering no directional tiebreak.

The actionable read: MOVE is the canary. A spike there means risk has metastasized from equities into fixed income — and the playbook shifts from mean-reversion to contagion defense. Until then, treat this as a geopolitical premium that decays.

What it means for your trading

Bond vol via MOVE at 74.42 definitively classifies the current stress as geopolitical rather than systemic credit — favor mean-reversion structures, but monitor MOVE for any sign of fixed-income contagion that would invalidate the base case.

Scenario EV

The scoring framework ranks iron_condor highest at 47, optimal in the 30-45-day DTE window where steep contango delivers maximum theta carry. The logic is structural: contango across the full VIX curve from 16.74 through 22.58 funds the short strikes, VVIX at 99.29 (normal) keeps sizing at standard_size, and defined-risk wings insulate against the geopolitical tail that Islamabad talks could activate overnight.

Why not strangles? Negative VRP across the complex—SPY at -5.61%, QQQ at -6.43%—means realized is running hotter than implied. Naked short premium fights every tick of that spread. Wings are mandatory, not optional. The iron condor's defined risk converts that headwind into a bounded variable rather than an open-ended bleed.

If peace talks collapse and directional bias emerges, pivot to put spreads scoring 33. QQQ's negative_gamma regime amplifies downside there—spreads in tech capture the acceleration while capping the cost of being wrong on timing.

What it means for your trading

Iron condors score 47 in the 30-45-day window, exploiting steep contango theta carry with wings that neutralize the negative-VRP headwind; rotate to put spreads at 33 if the Islamabad binary resolves bearishly and QQQ's negative_gamma regime accelerates directional flow.

Actionable Summary

Lean into iron_condor structures in SPY/SPX at 30-45 DTE with defined wings. Steep contango delivers structural theta carry while deeply negative VRP makes naked short premium untenable. The charm pivot at 671 anchors dealer support — spot trades well above, and the neutral bias holds as long as that level does. Size standard_size per VVIX — vol-of-vol at normal shows no embedded jump-risk premium.

Avoid: naked short premium across the complex — VRP is deeply negative and you are fighting realized. Skip overnight zero-DTE holds where 96.4% of SPY gamma evaporates at the bell, and steer clear of single-name strangles where dispersion runs hot. QQQ in negative_gamma amplifies directional moves — tighter wings or reduced notional on any tech overlay.

Watch: Islamabad peace talks as the week's binary catalyst, MOVE at 74.42 for credit contagion, and VVIX at 99.29 for regime repricing if diplomacy stalls. The Elevated / Watchful regime is sticky enough to respect, not panicked enough to capitulate.

What it means for your trading

Iron condors in SPY/SPX at 30-45 DTE with defined wings exploit steep contango carry; the Elevated / Watchful regime and deeply negative VRP make naked short premium the wrong trade while Islamabad peace talks remain the week's binary catalyst.

Nasdaq extending its longest winning streak in years while geopolitical risk escalates is the tension defining this session — complacency builds until it doesn't, and stretched momentum raises the stakes of any negative catalyst.

Bessent reversing on Fed rate urgency removes a key dovish tailwind — rate-sensitive positioning needs to adjust, and it signals the administration is more concerned about oil-driven inflation than growth support.

IEA supply-cut warning is the fundamental catalyst behind elevated realized vol — if disruption worsens, the VRP gap widens further and complacent VVIX reprices sharply.

Hormuz blockade hitting India as Russian oil waiver expires creates a secondary energy shock — this is the contagion vector that could turn a regional conflict into a global macro event for vol markets.

Islamabad peace talks are THE binary catalyst this week — success collapses vol back to pre-conflict levels, failure spikes VVIX and shifts the regime toward panic.

Tankers still passing Hormuz on day one of blockade suggests enforcement is partial — the market reads this as de-escalation, which supports the contango thesis for now but is fragile.

China export engine stuttering on Iran war demand chill is the demand-side signal — if this extends, it shifts the vol regime from geopolitical-shock to recessionary, which compounds differently.

Broad risk-on with dollar nearing pre-war levels confirms the market's base case is diplomatic resolution — but this consensus positioning also means the unwind would be violent if talks fail.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.09 with a contango term structure. The Fear & Greed index reads neutral, and cross-asset volatility is unknown across SPY, QQQ, and IWM.

Is SPY in positive or negative gamma today?

SPY is in unknown gamma with net dealer GEX at $4.8M. The gamma flip sits at —, with the call wall at 671.00 and the put wall at 50.00.

Where is the SPY gamma flip level right now?

SPY's gamma flip is at — against a spot of 690.03. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.12% with a volatility risk premium of -5.61%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in contango with VIX at 18.09. Contango signals benign forward expectations; backwardation signals near-term stress.

What's the dealer positioning on QQQ and IWM?

QQQ shows negative_gamma gamma with net GEX at $83.3M (flip: 628.00). IWM shows unknown gamma with net GEX at $1.5M (flip: —).

Get today's live analysis

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime