Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

Positive-gamma cushion in SPY masks QQQ negative-gamma fragility; steep contango and subdued VVIX favor premium sellers, but geopolitical tail risk from Hormuz blockade keeps regime elevated and watchful

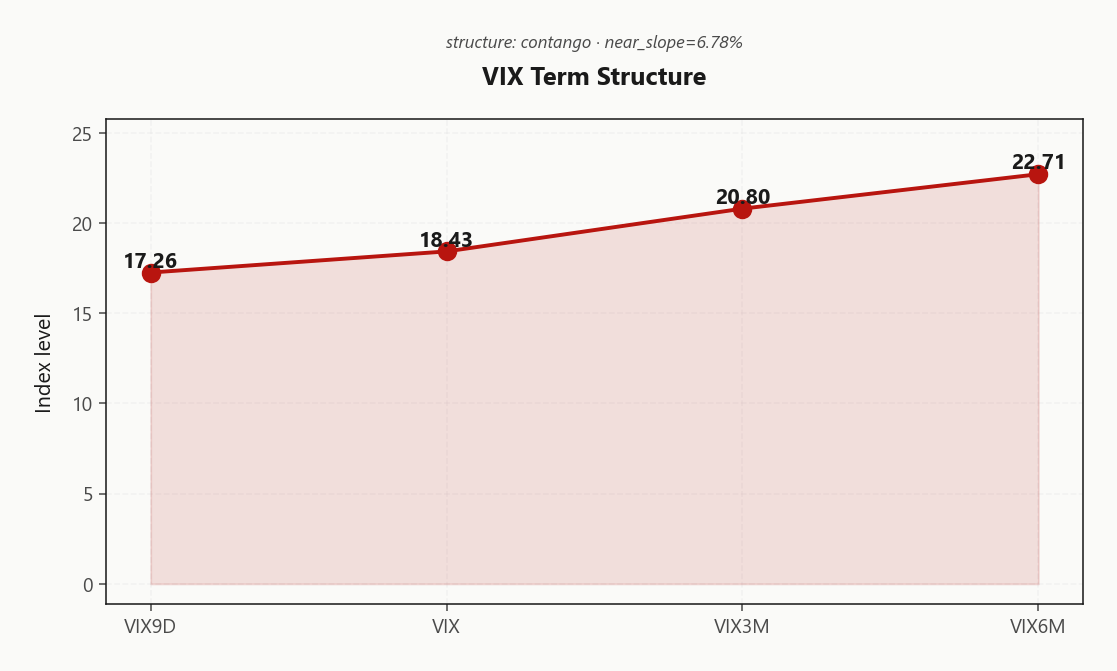

The index complex is split: SPY sits comfortably in positive_gamma above its gamma flip at 674.04, while QQQ trades in negative_gamma below 639.00 — a divergence that makes QQQ the fragile link if geopolitical headlines escalate. VIX term structure in contango with VIX9D at 17.26 well below VIX6M at 22.71 says the market expects normalization, but negative VRP across the board means options are still cheap relative to what the tape has actually delivered.

Regime Assessment

The vol regime sits at Elevated / Watchful with VIX anchored at 18.43 and steep contango across the full term structure. The yellow signal demands watchfulness without forcing defensive repositioning — elevated enough to respect, not severe enough to retreat from premium selling.

Transition probabilities frame the base case clearly: only — likelihood of a panic-regime jump over the near-term horizon, while the path to low-vol carries — probability over the intermediate window — plausible and consistent with the contango thesis grinding forward. A half-life of 15 sessions gives this elevated state moderate stickiness; expect a slow bleed lower in vol rather than a snap resolution.

For positioning, this regime favors measured premium selling over defensive hedging — but the persistent SPY/QQQ gamma divergence and deeply negative vanna overhang warrant standard sizing, not levered carry. Compression remains the base case until a catalyst breaks the architecture.

What it means for your trading

Regime is Elevated / Watchful with yellow signal — compression is the base case given only — near-term panic probability and a half-life of 15 sessions, but Hormuz tail risk and negative vanna keep the posture watchful rather than complacent.

Trading readVIX declining while SKEW stays elevated creates a subtle divergence — the market is less afraid of broad moves but still paying for tail protection. VVIX confirming VIX's decline says the vol complex agrees with itself for now. MOVE sitting low separates this from a systemic event — it's equity and energy specific, not credit.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Forward Vol Geometry

The VIX term structure prints clean contango from front to back — VIX9D at 17.26, spot VIX at 18.43, VIX3M at 20.80, VIX6M at 22.71 — an orderly upward slope with no kinks or event inversions despite Hormuz headlines dominating the tape. The near slope at 6.78%% confirms the front complex carries zero panic premium; the market is treating geopolitical escalation as a slow-burn repricing, not a binary catalyst demanding front-loaded protection.

Forward vol regime is steep_contango — Steep contango — vol sellers favored. The steepest implied forward vol sits in the intermediate-DTE range, creating a structural carry opportunity: short-dated premium sellers harvest roll-down as the curve compresses toward spot. VIX futures basis at 12.86%% in contango means roll yield actively subsidizes short-vol positioning. The best carry edge concentrates in the window where term structure slope is steepest before flattening into the belly — that is where iron condor theta capture is maximized relative to gamma risk.

What it means for your trading

Steep contango with no front-end event premium says the vol surface favors disciplined premium sellers harvesting roll-down in short-to-intermediate DTE, while the contango futures basis provides a structural tailwind — but the carry trade requires Hormuz risk to remain priced as a grind rather than flipping to a binary event.

Trading readClean contango from spot through six-month — no inversion, no kinks. The roll yield is structurally positive for VIX short positions and vol-selling strategies. The steep near slope confirms the market expects front-month vol to converge lower. This is the kind of curve shape that rewards patience in iron condors and penalizes early rolls.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

Realized vol is running hotter than implied across the entire index complex, and the market is not paying up for it. SPY ATM IV prints at 14.42% against a twenty-day realized of 19.91, producing a VRP of -5.49% — options are unambiguously cheap to the tape. QQQ carries the widest gap at -6.03%, with ATM IV at just 17.67% despite tech sitting in negative gamma territory where dealer hedging amplifies realized moves. IWM's VRP at -3.32% is the tightest of the three, suggesting small-caps are at least partially repriced to actuals.

The decay signature matters here: SPY's twenty-day realized at 19.91 remains elevated above its longer-window average at 15.68, but five-day realized has already pulled back to 15.09 — the deceleration is underway. The IV/RV spread assessment reads danger_zone, yet steep contango across the VIX curve says the market expects realized to converge down toward implied, not the reverse. That directional bet is the core tension: short-term vol sellers face negative carry until the tape actually calms, but the term structure rewards patience if it does.

Net: options are cheap to recent history, making long premium structures attractive for anyone positioned around a Hormuz escalation catalyst. For premium sellers, the trade only works if you believe realized vol is mean-reverting — and the contango structure argues it is. SPY is the cleaner vehicle given its positive-gamma cushion; QQQ's negative VRP plus negative gamma makes short vol there a fragile proposition.

What it means for your trading

Negative VRP of -5.49% in SPY and -6.03% in QQQ confirms options are underpricing recent realized moves, but declining five-day realized at 15.09 and steep contango argue the gap closes from the realized side — favor patient premium selling in SPY over QQQ where negative gamma compounds the mispricing risk.

Skew Convexity

SPY quarter-delta skew prints 3.37% with a smile ratio of 1.28% — orderly downside demand, not a crash bid. Put quarter-delta IV at 15.48% versus ATM at 13.17% versus call quarter-delta at 12.11% confirms the tilt is measured: hedgers are active but not panicking.

QQQ tells a different story — skew steepens to 4.06%, reflecting concentrated tech tail-hedge flow consistent with its negative_gamma positioning. That steepness makes QQQ the fragile leg if Hormuz headlines escalate. IWM sits at the other extreme: skew at 2.45% with a flat smile ratio of 1.13%, leaving small-cap downside protection unusually cheap relative to peers — worth monitoring as a low-cost tail hedge.

Call skew is compressed across the entire complex. Nobody is paying for upside acceleration despite the rally, which argues for put spreads over naked puts — moderate skew steepness rewards defined-risk structures without overpaying for convexity.

What it means for your trading

Skew geometry is tilted but orderly — QQQ's steeper surface at 4.06% reflects negative-gamma fragility while IWM's flat smile offers cheap tail protection. Put spreads capture the skew premium efficiently; call-side compression signals absent upside conviction.

Vol-of-Vol Structure

VVIX at 98.76 is subdued and declining—-3.77%% on the session—even as Hormuz blockade headlines persist. The VVIX/VIX ratio at 5.36 sits squarely in normal territory, confirming the market prices no bimodal vol outcome and no jump risk worth paying for. This is a green light for standard_size: no need to half-size positions or widen wings defensively when vol-of-vol refuses to validate the geopolitical anxiety embedded in the headline tape.

The nuance worth watching is the VVIX/SKEW divergence. SKEW at 156.93 remains elevated while VVIX compresses—a split that points to persistent structured-product tail demand rather than episodic panic hedging. That distinction matters: structured flow reprices slowly and predictably, panic flow reprices violently. As long as VVIX stays normal while SKEW stays rich, the tail bid is a background hum, not a siren.

The early-warning trigger: VVIX spiking toward extreme while VIX at 18.43 stays flat. That decoupling would signal dealer hedging of hedging—the vol complex losing confidence in its own mean-reversion assumption—and warrants immediate defensive scaling.

What it means for your trading

Vol-of-vol at normal with a VVIX/VIX ratio of 5.36 supports standard_size across premium-selling structures; the elevated SKEW at 156.93 reflects structural tail demand, not panic, and does not contradict the sizing signal.

Dispersion Spread

The index vol spread is telling a clear story: QQQ ATM IV at 17.67% runs meaningfully wide of SPY at 14.42%, pricing the single-stock concentration risk embedded in mega-cap tech. Today's top movers — NVDA, META, AAPL — are all printing positive GEX shifts, but that directional alignment is precisely what the elevated QQQ premium says will fracture. When a handful of names drive the index and dealers are short gamma in negative_gamma, dispersion is the latent risk the spread is flagging.

IWM sits at 21.28% — the highest absolute IV across the complex, yet the tightest gap to its own realized vol, making it the least mispriced on a carry basis. SPY's tighter implied and positive_gamma cushion make it the cleanest vehicle for premium selling. Prefer index structures over single-name plays here: concentrated GEX in the top movers amplifies idiosyncratic risk that index-level gamma smooths out.

What it means for your trading

Wide QQQ-SPY IV spread at 17.67% vs 14.42% reflects fragile single-stock alignment in tech; SPY's positive gamma regime and tighter implied offer superior risk-adjusted carry for vol sellers.

Liquidity & Microstructure

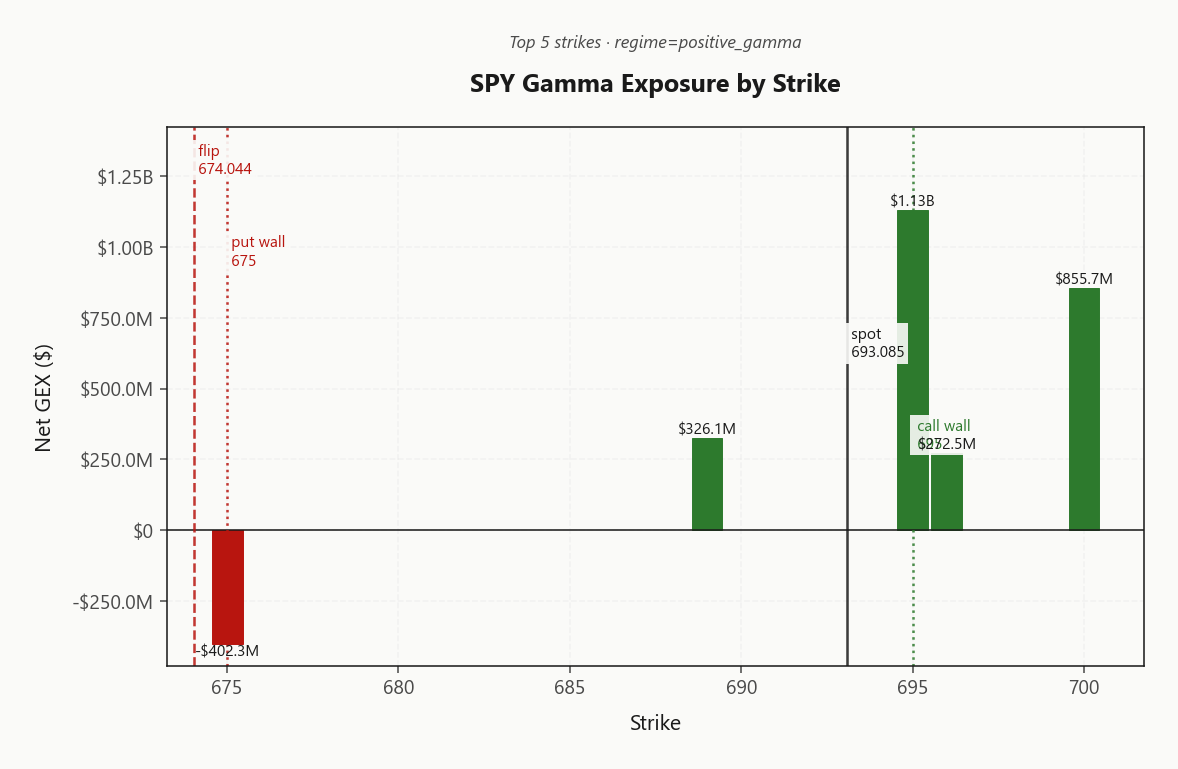

SPY's gamma landscape is stacked at the 695.00 call wall — the top strike at 695.00 commands $1.13B in net GEX, making it the session ceiling dealers will defend. Spot at 693.09 sits just below, compressing the tape into a pin zone. The gamma flip at 674.04 and put wall at 675.00 define the lower cushion, while deep open interest at 530 reflects legacy hedging anchoring the lower strike complex.

QQQ is the fragile counterpart. Spot trades well below its gamma flip at 639.00, leaving dealers short gamma and amplifying directional moves. The put wall at 640.00 offers no meaningful floor — GEX concentration is thin across the strike ladder, so selling pressure feeds on itself without the mean-reversion buffer SPY enjoys.

Intraday microstructure is increasingly 0DTE-driven: expiring options account for 27.9%% of SPY's total GEX versus 52.5%% in QQQ, making tech's tape headline-reactive and momentum-prone while SPY's multi-day positioning still governs.

What it means for your trading

SPY is pinned beneath the 695.00 call wall with deep positive gamma cushion to 674.04, while QQQ's negative gamma below 639.00 means any selling accelerates — the regime divergence makes QQQ the fragile leg for intraday dislocations.

Trading readSPY gamma is stacked at the call wall with the top strike acting as a hard ceiling — dealers will sell into any approach, creating a magnet-and-repel dynamic. Below the flip zone, dealer selling accelerates, so the playable range is between the put wall and call wall. QQQ's thin gamma profile means no such guardrails exist in tech.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Beneath SPY's positive_gamma surface lies an asymmetric vulnerability: net vanna exposure at -$41.58B means a vol spike forces dealers to sell delta into weakness, compounding any drawdown that breaches the gamma cushion. Charm at -$3M layers additional selling pressure into the close, tilting the intraday drift lower as expiring options shed time value. The charm pivot sits at 695 — the call wall — just 0.2763008866% above spot, with a neutral bias that flips supportive only on a clean break higher.

IWM's vanna at -$59.75B is even more negative relative to index capitalization, making small-caps the overlooked vanna risk if a Hormuz escalation headline triggers a broad vol impulse. The transmission chain is clear: geopolitical catalyst spikes implied vol, deeply negative vanna forces dealer delta selling across SPY and IWM, selling pressure overwhelms the positive gamma buffer, and the gamma flip at 674.04 becomes the regime breakpoint rather than a floor.

Mean-reversion holds as long as vol stays compressed — but the vanna overhang is the mechanism by which an orderly tape turns disorderly. Monitor 98.76 for early tremors; charm selling into the close keeps the directional bias mildly negative absent a catalyst to clear the 695 pivot.

What it means for your trading

Positive gamma disguises deeply negative vanna — a vol spike activates dealer delta selling at -$41.58B that overwhelms the gamma cushion, with the charm pivot at 695 as the line between orderly mean-reversion and forced liquidation flow.

Cross-Asset Confirmation

Cross-asset confirmation tilts constructive. MOVE at 74.42 keeps rates vol contained — this is an equity-and-energy story, not a systemic credit event. Fear & Greed printing neutral at 47 offers no contrarian trigger in either direction; the tape is priced for ambiguity, not dislocation.

The regime divergence is the actionable signal: QQQ at 626.50 pinned in negative_gamma while IWM at 268.52 holds positive_gamma with SPY aligned — a two-against-one split (true) that isolates tech as the fragile leg. Money rotating toward value and small-cap gamma cushion over mega-cap exposure is the positioning read.

Critically, the Hormuz catalyst is an oil supply shock — not a funding or credit crisis. Historical analogs favor mean-reversion once diplomatic channels activate, which keeps the base case pointed toward vol compression rather than compounding contagion. Sell QQQ fragility, lean into SPY stability.

What it means for your trading

Contained rates vol at 74.42 and neutral sentiment at 47 confirm this is a sector-rotation environment, not a broad risk-off regime — SPY and IWM positive gamma cushion the complex while QQQ's negative gamma remains the single point of failure if geopolitical escalation broadens beyond energy.

Scenario EV

The iron_condor scores highest at 46, driven by steep contango carry, SPY's positive_gamma cushion supplying natural mean-reversion, and standard_size position sizing per subdued VVIX. Optimal tenor of 30-45 days captures the steepest roll-down on the vol curve where forward vol decays fastest into spot.

Put spreads score 34 as a secondary structure — useful tail insurance given deeply negative vanna exposure at -$41.58B that activates on any vol spike. Avoid naked short strangles while QQQ remains in negative_gamma: the asymmetry is wrong when dealer hedging amplifies rather than dampens directional moves.

Vehicle preference is clear: SPY over QQQ. Positive gamma provides a structural mean-reversion tailwind that compresses realized ranges into your short strikes. Anchor wings at the 695.00 call wall and 675.00 put wall — dealer positioning defines the playable corridor.

What it means for your trading

Sell premium via SPY iron_condor at 30-45 DTE where contango roll-down is steepest; regime is Elevated / Watchful with compression as the base case, so standard sizing holds — no need to scale defensively.

Actionable Summary

Sell premium in SPY via iron_condor at 30-45 DTE, anchoring wings at the 695 call wall and 675.00 put wall. SPY's positive_gamma cushion makes it the cleanest vehicle — dealers buy dips and sell rips, compressing intraday ranges and rewarding mean-reversion structures. Steep contango delivers structural roll-down carry across that DTE window, and normal VVIX confirms standard sizing is appropriate.

Steer clear of QQQ short premium entirely. negative_gamma positioning means any vol spike gets amplified, not dampened — the opposite of what premium sellers need. Naked short strangles are equally unattractive while VRP runs negative across the complex; options are cheap to the realized tape, so the carry math punishes undisciplined sellers.

Watch 695 — the charm pivot and call wall converge there, and a sustained break above flips dealer flow supportive. Islamabad peace-talk headlines are the binary catalyst: a breakthrough compresses vol sharply and accelerates contango carry into your position.

What it means for your trading

Regime is Elevated / Watchful with vol compression as the base case — favor SPY iron_condor structures over QQQ, where negative_gamma positioning turns any geopolitical headline into an amplified move rather than a dampened one.

IMF downgrading global growth over Iran war escalation is the macro headline that validates the elevated regime label — if recession probability rises, the contango carry thesis compresses faster but tail risk reprices higher.

Hormuz blockade sending oil surging is the direct catalyst behind the VRP/IV tension — energy supply shock that hasn't yet translated into equity vol is the gap the market is debating.

Bessent walking back Fed rate cut urgency amid oil surge is a direct rates-vol catalyst — removes the dovish put that equity bulls were counting on, which matters for charm dynamics into quarter-end.

IEA warning on supply cuts and demand destruction frames this as a stagflationary shock — the worst-case regime for equity vol because it removes both the growth and the rates put simultaneously.

India energy squeeze from both Hormuz blockade and Russian waiver expiration widens the geopolitical surface area — multi-front energy disruption is harder to resolve than a single-point conflict.

Islamabad peace talk possibility is the binary catalyst to watch — a breakthrough compresses vol sharply and accelerates contango carry, making it the key event risk for short-vol positioning.

Nasdaq nine-session winning streak context matters for positioning — extended momentum into geopolitical risk creates the exact setup where negative gamma in QQQ becomes dangerous if sentiment reverses.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.41 with a contango term structure. The Fear & Greed index reads neutral, and cross-asset volatility is spy_heavier across SPY, QQQ, and IWM.

Is SPY in positive or negative gamma today?

SPY is in positive_gamma gamma with net dealer GEX at $2.53B. The gamma flip sits at 674.04, with the call wall at 695.00 and the put wall at 675.00.

Where is the SPY gamma flip level right now?

SPY's gamma flip is at 674.04 against a spot of 693.09. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.42% with a volatility risk premium of -5.49%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in contango with VIX at 18.43. Contango signals benign forward expectations; backwardation signals near-term stress.

What's the dealer positioning on QQQ and IWM?

QQQ shows negative_gamma gamma with net GEX at $21.2M (flip: 639.00). IWM shows positive_gamma gamma with net GEX at $850M (flip: 252.50).

Get today's live analysis

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime