Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

All three equity indices closed in positive_gamma with VIX at 18.33 and VVIX collapsing to 95.24, pricing de-escalation despite an active Hormuz blockade. Yet realized vol is outpacing implied across the board ÔÇö SPY VRP at -5.63% ÔÇö creating a tension between the term structure's invitation to sell vol and the actual move set that says options remain cheap. The steep_contango curve says carry is available, but the negative VRP warns the calm hasn't been earned yet.

Regime Assessment

The vol regime sits at elevated ÔÇö Elevated / Watchful ÔÇö with VIX printing 18.33 and the term structure in full contango. A half-life of 15 sessions marks this state as moderately sticky: not entrenched enough to warrant aggressive hedging, but too persistent to dismiss as transient. Base case is gradual normalization toward a lower-vol regime over the coming two weeks ÔÇö the transition probability is moderate, tilted by the market's aggressive front-running of Hormuz de-escalation.

That tilt is the vulnerability. Positive gamma across SPY, QQQ, and IWM with VVIX at 95.24 prices a single-regime outcome ÔÇö orderly decay toward calm. The model assigns low probability to a panic transition within five sessions, but an active naval blockade is precisely the exogenous binary that regime models underweight. If talks collapse, the jump from Elevated / Watchful to stressed is not a drift ÔÇö it is a gap. Size for the base case; hedge for the gap.

What it means for your trading

Regime is Elevated / Watchful with a 15-session half-life ÔÇö gradual normalization is the central path, but the Hormuz binary is an overnight regime-jump catalyst that the contango term structure is not pricing.

Trading readVIX falling while MOVE stays flat and SKEW holds elevated is a mild divergence ÔÇö equity vol is more optimistic than the tail risk market. VVIX collapse to normal confirms no jump premium, but SKEW persistence says the tail has not fully de-risked. Watch for SKEW to follow VVIX down or VIX to follow SKEW up.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

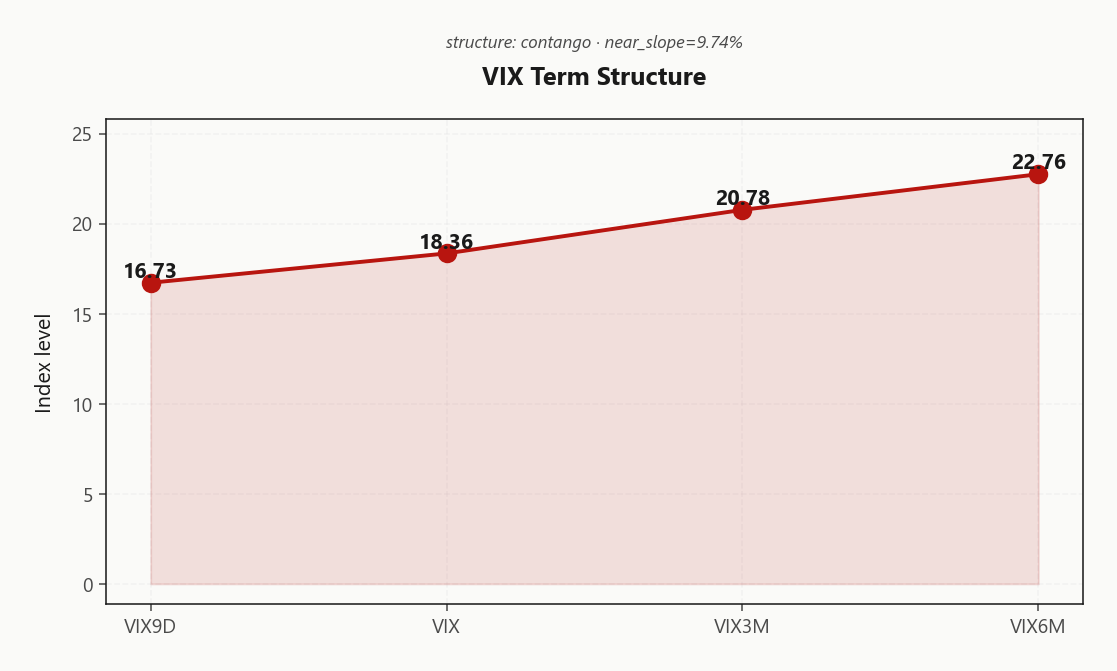

Forward Vol Geometry

The VIX term structure sits in full contango from front to back ÔÇö no inversion anywhere despite an active naval blockade in the Strait of Hormuz. VIX9D at 16.73 trades well below spot VIX at 18.36, which itself slopes up into VIX3M at 20.78 and VIX6M at 22.76. The near-term discount is striking: the front end is pricing de-escalation as fait accompli while the back end retains a measured geopolitical premium. Forward vol regime reads steep_contango ÔÇö the steepest carry gradient sits in the 30-45 DTE window where calendars harvest maximum roll-down.

This is a structurally clean vol-selling setup on paper. But the negative VRP underneath ÔÇö realized outpacing implied across the complex ÔÇö means the contango is offering carry on a vol surface that is already cheap to actual moves. The carry is real; the complacency it breeds is the risk. A collapse in Hormuz talks would invert the front end overnight, snapping VIX9D above spot VIX and unwinding every calendar and short-vol position anchored to this curve shape. Harvest the steep slope, but structure for the snap-back.

What it means for your trading

steep_contango term structure confirms the carry trade is available through the 30-45 DTE sweet spot, but the orderly contango from 16.73 through 22.76 is pricing a de-escalation outcome that remains binary ÔÇö defined-risk structures only until Hormuz resolves.

Trading readClean contango with steep near-term slope says the vol carry trade is available ÔÇö but this is the same structure that existed before every recent shock. The carry is real; the complacency it breeds is the risk. Size for the carry, hedge for the inversion.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

Realized vol is running hot across the entire equity complex and implied is not keeping up. SPY's trailing 20.01 twenty-day realized sits well above ATM implied at 14.38%, producing a VRP of -5.63% ÔÇö options are systematically underpricing the move set the tape has actually delivered. The longer-horizon 15.72 sixty-day realized confirms this is not a single-week anomaly; the gap between what the market is doing and what options charge for it has been widening.

This mispricing is broad-based. QQQ VRP at -5.69% and IWM at -3.33% show every major index exhibiting the same realized-over-implied dynamic ÔÇö ruling out idiosyncratic SPY skew as the driver. The resolution path is binary: either realized compresses as Hormuz de-escalation rhetoric translates into actual vol suppression, or implied must reprice higher to close the gap. Until that resolves, naked short premium is picking up pennies in front of a tape that moves more than the straddle pays for.

The key tension for vol desks: the contango term structure overhead screams sell carry, but negative VRP underneath says the carry is not compensating for the actual delivery risk. Defined-risk structures dominate here ÔÇö harvest the contango through spreads, not through exposed short gamma that the realized tape can run over.

What it means for your trading

Negative VRP of -5.63% in SPY, -5.69% in QQQ, and -3.33% in IWM signals options are cheap to realized moves across the complex ÔÇö favor defined-risk carry structures over naked premium selling until the HV/IV gap closes.

Skew Convexity

Quarter-delta skew prints 3.91% ÔÇö elevated but ordered, consistent with institutional hedging rather than dislocation. The smile ratio at 1.34% confirms puts are paying up relative to calls without the extreme distortion that would signal tail panic. Put quarter-delta IV at 15.58% versus ATM at 13% reflects a standard downside premium ÔÇö desks are buying protection into Hormuz headline risk, not pricing a regime break.

Call quarter-delta IV at 11.67% is notably flat, sitting below ATM. The rally has no upside vol conviction behind it ÔÇö positioning reads as short-covering and geopolitical fade, not fresh directional appetite. When the call wing refuses to bid into a move higher, the smile is telling you the market does not trust its own rally.

Actionable read: put spreads over naked puts. The steep skew means single-leg downside protection overpays for the smile ÔÇö spread structures neutralize that premium while retaining convexity where it matters. Defined-risk hedges are the efficient expression here.

What it means for your trading

Skew is steep but orderly at 3.91% with flat call-side vol at 11.67% ÔÇö the smile favors structured put spreads over naked protection, and the absence of upside conviction says this rally lacks options-market endorsement.

Vol-of-Vol Structure

VVIX collapsed to 95.24, squarely in normal territory ÔÇö the market's clearest vote that the Hormuz tail is fading. The VVIX/VIX ratio at 5.20 confirms single-regime pricing with no jump premium embedded, no bimodal outcome distribution being marked. Vol-of-vol is telling you the options market sees one path forward ÔÇö gradual normalization ÔÇö not the binary blowout the headlines suggest.

standard_size position sizing is appropriate given this backdrop, but the asymmetry cuts one way: VVIX re-expansion from these levels would be violent and immediate if de-escalation talks collapse. A snap-back toward stressed territory reprices vega convexity before anything else moves ÔÇö vol-of-vol trades are the canary, not the laggard. The disconnect between subdued VVIX and an active naval blockade is either prescient or complacent, and you will not know which until Hormuz resolves.

With VIX at 18.33 and VVIX normalizing beneath it, the vol surface is priced for an orderly grind ÔÇö not a shock. Lean into that structure, but keep defined-risk wrappers on any vega exposure. The VVIX bid will return faster than the VIX bid if the geopolitical bet is wrong.

What it means for your trading

VVIX at 95.24 in normal range with a VVIX/VIX ratio of 5.20 signals no jump premium and supports standard_size positioning ÔÇö but the compression is a de-escalation wager that reprices violently if Hormuz talks fail.

Dispersion Spread

Cross-asset regimes are aligned ÔÇö SPY, QQQ, and IWM all sitting in positive gamma with spot above the flip in each name. No inter-index divergence means no rotation signal and no dispersion trade worth isolating. ATM IV follows the expected beta hierarchy: SPY at 14.38%, QQQ at 18.27%, IWM at 21.31%. SPY carries the cheapest implied in the complex, which translates to the steepest VRP drag ÔÇö selling SPY vol here means accepting the worst compensation relative to realized moves.

With correlation locked and dispersion moderate, index-level structures in SPY/SPX remain the cleaner expression over single-name vol selling. Idiosyncratic risk in individual names is not generating enough premium spread to offset the tracking error it introduces. Lean into SPX iron condors where the gamma cushion provides mean-reversion support, and avoid drifting into single-stock vol sales unless a name-specific catalyst creates a discrete edge. IWM's thinner cushion makes it the canary ÔÇö if small-cap gamma cracks first, the aligned regime is breaking down.

What it means for your trading

Uniform positive gamma across the index complex with aligned regimes favors index-level vol structures over single-name dispersion plays; SPY at 14.38% ATM IV is the cheapest and most VRP-exposed leg in the hierarchy.

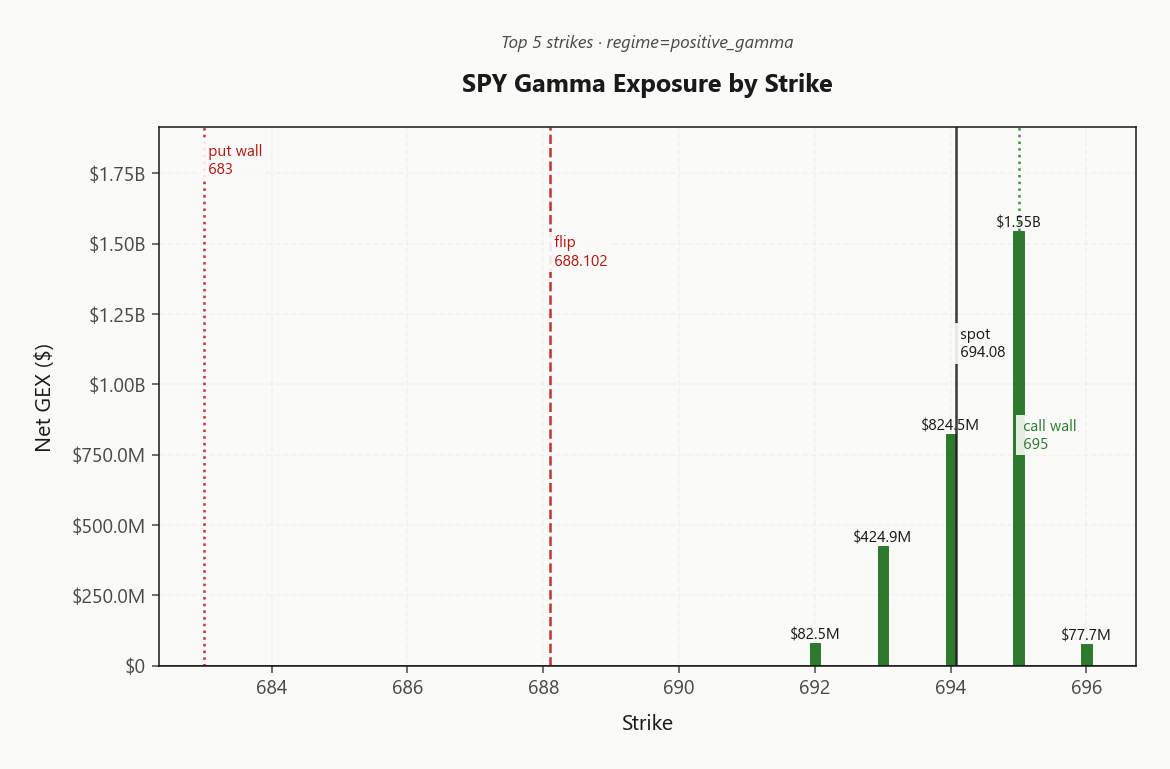

Liquidity & Microstructure

SPY is pressed against the 695.00 call wall with the top strike at 695.00 concentrating $1.55B in net GEX—the magnet defining today’s pin. The gamma flip sits well below spot at 688.10, leaving a wide dealer-long-gamma corridor where every dip draws mechanical buying and every rip meets systematic supply. This is a range-compression engine until a catalyst breaks the pin.

Downside, the put wall at 683.00 marks the first shelf where dealer hedging intensifies—a selloff into that zone triggers accelerating put-side gamma that acts as a natural floor. Highest open interest at 640 is distant from spot and structurally irrelevant to near-term flow, confirming positioning has migrated upward toward the call wall cluster.

QQQ mirrors the setup with its call wall at 630.00 and gamma flip at 590.99—both indices locked in aligned positive gamma with no inter-index divergence to exploit. Fade the range; don’t chase direction.

What it means for your trading

Dealer positioning creates a well-defined box from 688.10 to 695.00 where mean-reversion dominates—fade extremes within this corridor until spot breaks below the flip, at which point dealer flow inverts from stabilizer to accelerant.

Trading readDeep positive gamma concentrated just above spot creates a magnetic ceiling ÔÇö expect dealers to sell rallies into the call wall and buy dips toward the flip zone. The trade is fade the range until a catalyst breaks the gamma pin, not chase direction.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Net vanna exposure (VEX) at -$148.7M sets up an asymmetric accelerant: any reversal in VIX's decline forces dealers to sell delta into a falling tape, compounding downside momentum precisely when the book least expects it. The negative VEX reading means the surface-level gamma cushion is thinner than headline GEX suggests ÔÇö vanna is working against the stabilizer.

Charm (CHEX) at -$519M adds a persistent selling headwind into the close as time decay erodes dated put positions and dealers unwind hedges. This is not episodic ÔÇö it grinds every session until expiry reshuffles the deck.

The charm pivot at 695 aligns with the call wall, concentrating the vanna-charm flow flip into a single strike. Spot sits just 0.132549562 percent away with bias reading neutral ÔÇö directional resolution is imminent. Above the pivot, dealer flow caps rallies; below it, vanna and charm compound into a sell cascade.

What it means for your trading

Negative VEX and CHEX beneath a positive gamma surface create a fragile equilibrium ÔÇö the charm pivot at 695 is the single level where dealer flow direction resolves, and spot is close enough that the next session's opening print likely picks the side.

Cross-Asset Confirmation

MOVE at 74.42 confirms the Hormuz disruption is not transmitting through credit channels ÔÇö bond vol remains subdued with no contagion footprint. Fear and Greed at 47 (neutral) offers no contrarian extreme to lean on; the crowd is pricing neither capitulation nor euphoria, leaving the next directional impulse to the geopolitical tape.

QQQ at 628.31 and IWM at 268.49 both hold aligned positive gamma regimes alongside SPY ÔÇö no inter-index divergence, no rotation signal, just uniform dealer dampening across the equity complex. VIX in negative gamma completes the textbook configuration: equity dealers stabilize while VIX dealers amplify, and the term structure's contango posture ratifies the carry thesis overhead.

The read is clean: this is an isolated energy shock that equities are fading, not a credit event gathering contagion. Geopolitical dislocations mean-revert unless they infect fixed income ÔÇö and MOVE says they haven't. The risk is if they do.

What it means for your trading

Cross-asset confirmation is fully aligned with MOVE at 74.42 ruling out credit transmission and all equity indices locked in positive gamma ÔÇö the Hormuz disruption remains an energy-isolated event until bond vol says otherwise.

Scenario EV

iron_condor scores highest at 39 on our structure screen, threading the needle between a contango term structure that invites carry and a negative VRP that punishes naked exposure. The optimal window sits in the 30-45 DTE range ÔÇö far enough out to harvest the steepest contango roll-down, near enough to avoid warehousing open-ended Hormuz binary risk through mid-May.

The construction logic is straightforward: positive_gamma across the index complex delivers mean-reversion between the 683.00 put wall and the 695.00 call wall, normal VVIX at 95.24 strips out jump premium, and steep_contango forward vol geometry supplies the carry. That trifecta favors defined-risk premium collection ÔÇö not naked selling.

Size conservatively. VRP assessment reads unknown with SPY VRP at -5.63% confirming options remain cheap to realized moves. Layer a put-spread overlay below the 688.10 gamma flip to own the geopolitical tail the term structure refuses to price.

What it means for your trading

iron_condor in 30-45 DTE captures contango carry with defined risk while the negative VRP at -5.63% and active Hormuz headline risk argue decisively against naked short-vol exposure.

Actionable Summary

Primary: iron_condor in SPY/SPX at 30-45 DTE harvests the contango carry while capping Hormuz tail exposure with defined risk. Positive gamma across all three equity indices ÔÇö net GEX at $3.02B ÔÇö means dealer hedging suppresses realized range until the 688.10 flip breaks. Regime reads Elevated / Watchful with VIX at 18.33: not complacent enough for naked selling, not stressed enough for outright protection.

Watch: The charm pivot at 695 is where dealer flow direction flips ÔÇö above it, charm and vanna cap rallies into the 695.00 call wall; below it, vanna accelerates downside toward 683.00. Spot sits 0.132549562 from this pivot with bias neutral, making directional resolution imminent.

Avoid naked short vol ÔÇö VRP at -5.63% confirms realized moves outpace implied across the complex. Hedge via put spreads: skew at 3.91% makes structured protection cheaper than naked puts. Size for gradual normalization; respect the Hormuz binary.

What it means for your trading

Positive gamma cushion favors iron_condor at 30-45 DTE to harvest contango carry, but negative VRP at -5.63% and the Hormuz tail demand defined-risk structures with the 695 charm pivot as the key directional trigger.

Revoking the Iranian oil waiver tightens global crude supply further and reinforces the inflationary undercurrent that the equity rally is choosing to ignore ÔÇö watch energy-sensitive margins and transport names.

IMF cutting the global growth baseline is slow-moving macro deterioration that eventually forces index-level repricing ÔÇö not a trigger today, but it narrows the margin for error on any new shock.

Hormuz blockade becoming operational with ships physically turned elevates this from headline risk to supply-chain reality ÔÇö if it persists, the energy shock transmission to earnings estimates begins within weeks.

UK growth downgrade from war-driven inflation demonstrates the second-order contagion path ÔÇö energy shocks compress growth globally, and European exposure is the credit transmission channel to watch.

Trump floating resumed Iran talks was today's primary rally catalyst ÔÇö the market is aggressively front-running de-escalation, making the downside asymmetric if negotiations fail to materialize.

Bessent walking back rate cut urgency removes one potential offset to the geopolitical growth drag ÔÇö if the Fed will not ease into an energy shock, the equity market has one fewer backstop.

IEA supply-demand warning is the fundamental grounding for why energy inflation risk persists even as equities rally ÔÇö the oil shock math does not support the VIX term structure's calm.

Frequently Asked Questions

What is the current market volatility regime?

VIX is trading at 18.36 with a contango term structure. The Fear & Greed index reads neutral, and cross-asset volatility is aligned across SPY, QQQ, and IWM.

Is SPY in positive or negative gamma today?

SPY is in positive_gamma gamma with net dealer GEX at $3.02B. The gamma flip sits at 688.10, with the call wall at 695.00 and the put wall at 683.00.

Where is the SPY gamma flip level right now?

SPY's gamma flip is at 688.10 against a spot of 694.08. Above flip, dealer hedging is suppressive; below it, hedging amplifies moves.

Is implied volatility rich or cheap versus realized?

SPY's at-the-money implied vol is 14.38% with a volatility risk premium of -5.63%. Negative VRP means options are cheap relative to recent realized moves; positive VRP means insurance is expensive.

What does the VIX term structure say today?

The VIX curve is in contango with VIX at 18.33. Contango signals benign forward expectations; backwardation signals near-term stress.

What's the dealer positioning on QQQ and IWM?

QQQ shows positive_gamma gamma with net GEX at $6.74B (flip: 590.99). IWM shows positive_gamma gamma with net GEX at $187M (flip: 265.96).

Get today's live analysis

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime