Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

The index complex sits in positive_gamma territory with spot pinned near the call wall at 686.00, giving dealers a mean-reversion bias that should dampen intraday swings. But the negative VRP at -5.24% reveals a disconnect — the market is actually moving faster than options imply, and the US-Iran standoff introduces a binary tail that the front end isn't fully pricing. Steep VIX contango (contango) favors structural carry, but sizing discipline is essential with SKEW ticking higher.

Forward Vol Geometry

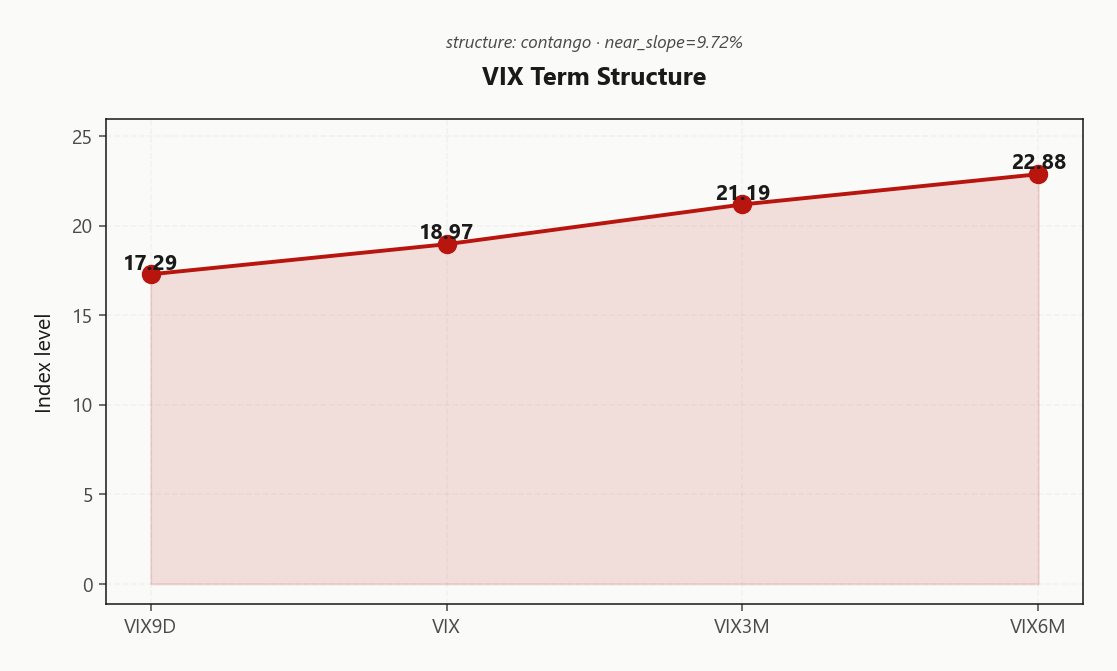

The VIX term structure prints full contango from 17.29 through 18.97 to 21.19 and 22.88 — a textbook steep_contango regime. The front end is suppressed relative to the belly, with VIX9D trading at a meaningful discount to spot VIX, confirming the market expects near-term calm to hold while warehousing uncertainty further out into May. Forward vol in the mid-curve implies acceleration ahead, making the steepest kink in the curve the sweet spot for premium collection.

That steep contango historically favors structural short-vol carry, but the negative VRP at -5.24% complicates the thesis — realized moves are outpacing what the curve implies, thinning the edge. The best calendar opportunity here is selling the front week against buying the monthly to capture the steepest roll-down, but size conservatively. The curve shape says carry; the VRP says respect the realized.

What it meansSteep contango from 17.29 to 22.88 favors short-vol carry, but negative VRP at -5.24% means realized moves are eating premium faster than the curve suggests — demand wider wings and shorter DTE to capture the steepest roll-down.

Trading readClean contango from front to back with steep near-term slope — the vol carry trade is alive but negative equity VRP is a flashing caution. The market expects current suppression near-term but is warehousing uncertainty in the back months around the geopolitical overhang.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

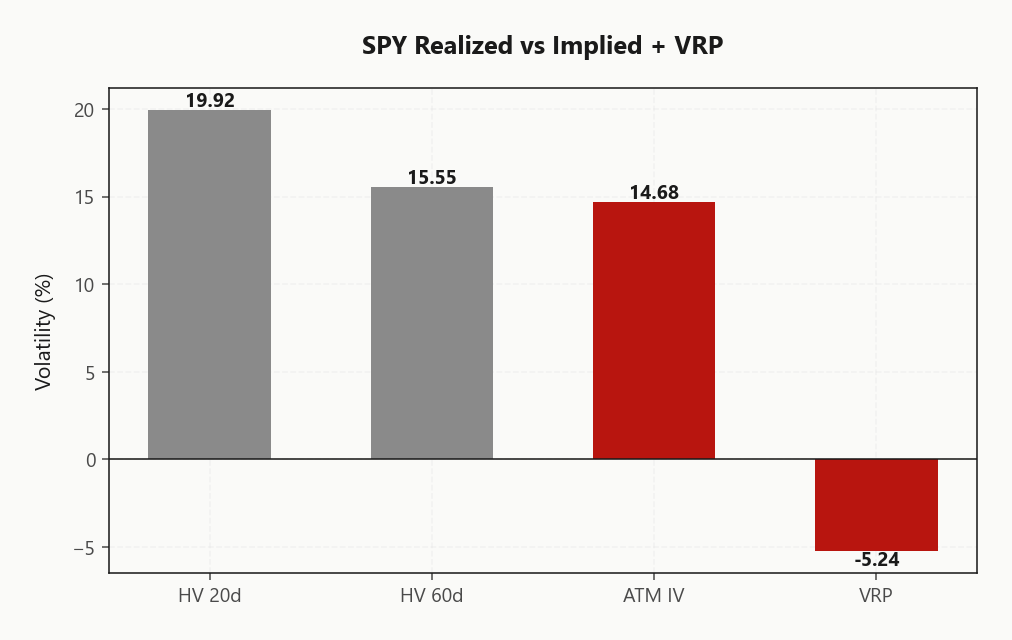

SPY ATM implied at 14.68% prints well below trailing realized at 19.92, producing a VRP of -5.24% — firmly in danger_zone territory. Even the shorter-window realized at 16.54 exceeds ATM implied. The market is moving faster than the options complex is willing to price, and theta is getting consumed by realized before it can accrue.

The pattern is universal but asymmetric in magnitude. QQQ's VRP at -5.7% is the most deeply negative — tech realized volatility is particularly underpriced, making it the strongest candidate for long gamma positioning. IWM at -2.69% shows the narrowest gap, offering the most fairly priced vol surface for sellers willing to bear small-cap idiosyncratic risk.

Net read: if selling premium, demand wider wings and reduced notional across the complex. If buying convexity, the front end offers asymmetric value — particularly in QQQ where the implied-to-realized disconnect is steepest.

What it meansNegative VRP across all three equity indices flags a danger_zone regime — options are universally cheap to realized moves, favoring long vol positioning or at minimum wider wings and smaller size on any short structures.

Trading readOptions are cheap to recent realized across the board — the market is moving more than implied suggests. Short vol strategies are fighting the tape; if selling premium, demand wider wings and accept lower credit.HV20 and HV60 are realized volatility over the last 20 and 60 trading days. ATM IV is what the market is pricing now. VRP = ATM IV − HV20: positive means options are expensive vs. recent reality (vol sellers' market), negative means options are cheap.

Skew Convexity

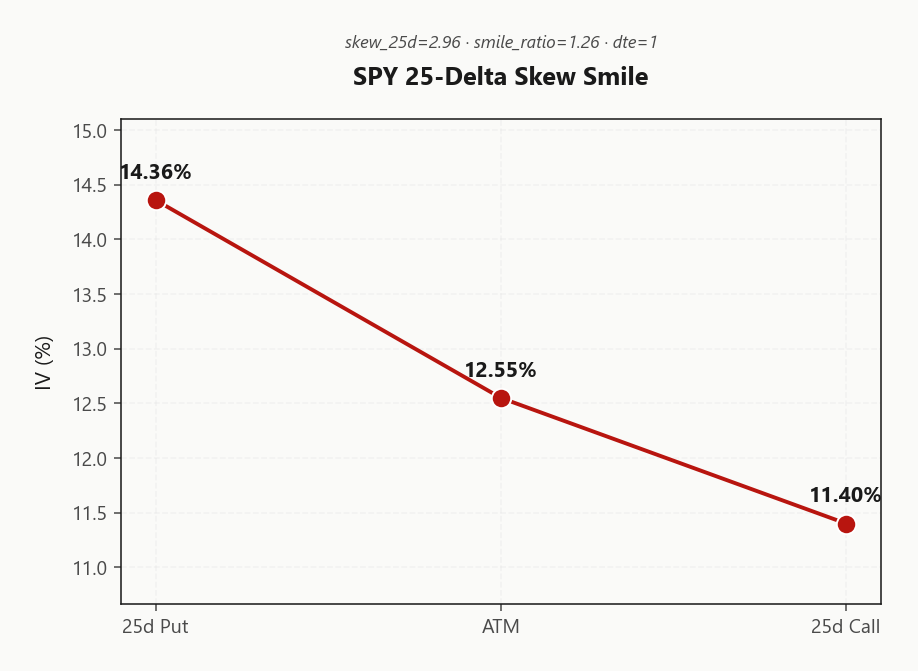

SPY quarter-delta skew at 2.96% with a smile ratio of 1.26% describes an ordered surface — put premium over ATM is elevated but not panicked. The put wing at 14.36% steps down cleanly through ATM at 12.55% to calls at 11.4%, a signature of systematic institutional hedging rather than retail capitulation. This is methodical portfolio protection around the Iran overhang, not a scramble for downside.

QQQ tells a more defensive story: quarter-delta skew at 3.44% exceeds SPY, reflecting tech's outsized geopolitical sensitivity and supply-chain exposure. The steeper put wing signals that real-money accounts are paying up for tech downside selectively. Meanwhile, the call side sits flat-to-cheap across the entire complex — nobody is reaching for upside despite Friday's rally, confirming the bounce lacks conviction.

At this skew level, naked long puts carry too much embedded premium to justify outright. Spread structures — put verticals in particular — extract the institutional hedge bid more efficiently and cap vega exposure. Favor put spreads over outright tails; the skew isn't steep enough to warrant convexity-at-any-price positioning.

What it meansOrdered skew across SPY and QQQ reflects disciplined institutional hedging, not fear. QQQ's steeper surface flags tech as the defensive priority, while flat call skew confirms no conviction in a sustained breakout — lean into spread protection rather than naked puts at these levels.

Trading readThe put wing is bid but not panicked — institutional hedging, not retail fear. Call skew is flat, confirming no conviction in a sustained breakout. Spread structures are more efficient than outright puts at this skew level.25-delta skew profile — put IV, ATM IV, call IV. Put wing above call wing means downside protection is richer than upside (typical for equity indices). Flat or inverted skew is a stress signal.

Vol-of-Vol Structure

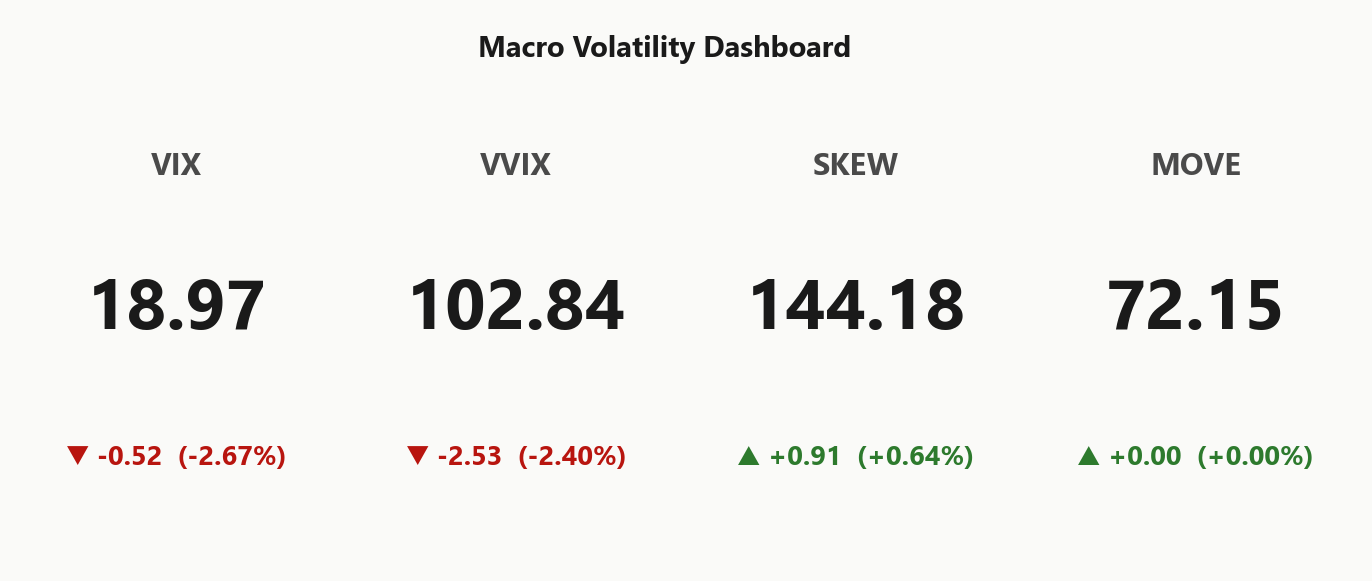

VVIX at 102.84 with VIX at 18.97 produces a VVIX/VIX ratio near 5.42 — firmly in normal territory. The vol complex is not pricing a bimodal VIX outcome despite an active geopolitical conflict and headlines that continue to escalate. No jump-risk premium is being paid here, and VVIX declined session-over-session even as Iran rhetoric sharpened — the market is de-escalating its vol expectations while the news cycle does the opposite.

That disconnect is the opportunity. VIX calls are cheap relative to the tail risk embedded in the geopolitical backdrop, making this the window where asymmetric convexity gets built quietly. Sizing guidance reads standard_size — no need to cut exposure on the vol-of-vol signal alone, but the subdued VVIX should not breed complacency. Use the discount to layer tail hedges rather than ignore them.

What it meansVVIX in normal range despite active conflict creates an asymmetric setup: VIX call convexity is mispriced cheap, and standard_size positioning is appropriate while the window for inexpensive tail protection remains open.

Dispersion Spread

Implied dispersion is compressed. SPY ATM IV at 14.68% understates the uniformity beneath the surface — the top GEX movers (NVDA, AMZN, MSFT, AAPL, GOOGL) all built positive gamma in lockstep on Friday's bounce. This was a high-correlation beta trade, not an idiosyncratic rotation, and cross-strike dispersion confirms the convergence.

Elevated correlation alongside moderate index vol creates a structural edge for index premium selling over single-name strategies. Idiosyncratic risk is not being compensated — pair trades and standalone dispersion plays offer poor risk-adjusted returns in this regime. SPX/SPY iron condors capture the carry without single-stock event exposure that the compressed vol surface isn't pricing.

For richer credit on the same correlation backdrop, QQQ ATM IV at 17.8% offers materially wider premium than SPY. The tech index carries the same positive_gamma regime but prices in more uncertainty — a more efficient vehicle for range-bound structures until mega-cap correlation breaks.

What it meansCompressed dispersion and synchronized positive gamma across mega-cap movers favor index premium selling (SPY/SPX iron condors) over single-name strategies; QQQ at 17.8% ATM IV provides the richest credit for the same aligned correlation regime.

Liquidity & Microstructure

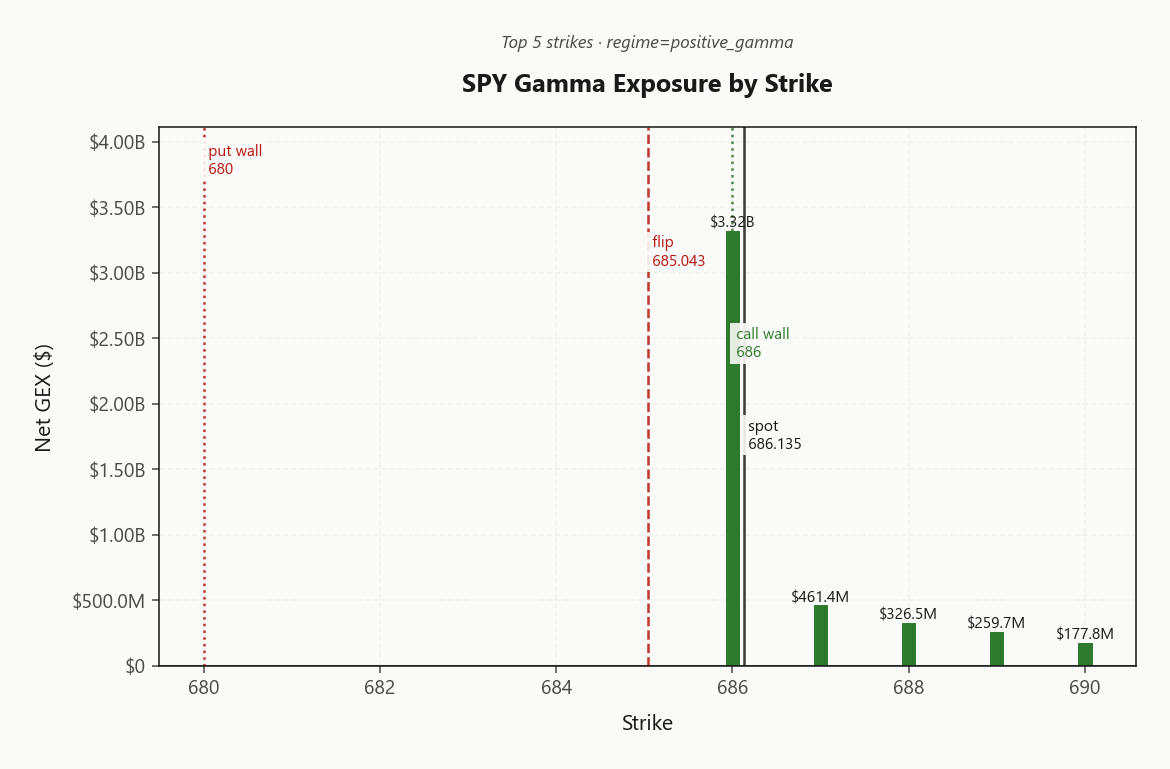

SPY's book is magnetically pinned to the 686.00 call wall, where the top strike alone concentrates $3.32B in dealer gamma — a hard ceiling that will absorb any attempt to break higher. Bulk open interest sits far below at 660, but active gamma is entirely dictated by the near-the-money cluster. The gamma flip at 685.04 sits fractionally below spot, creating a razor-thin cushion: any intraday dip past that threshold flips dealer hedging from suppressive to amplifying. First meaningful support rests at the 680.00 put wall.

The critical wrinkle: virtually all of this gamma is sourced from 0DTE contracts, meaning today's entire support structure evaporates at the close. Tomorrow's tape opens on a blank gamma slate, elevating overnight gap risk materially. QQQ mirrors the fragility — its gamma flip at 616.02 is similarly tight to spot, offering no diversification in the event of a coordinated downdraft across the index complex.

What it meansSpot is pressed directly against dealer supply at the call wall while the gamma flip lingers just below — a stable but fragile equilibrium that resets entirely overnight as 0DTE gamma decays to zero.

Trading readMassive gamma concentration right at spot creates a magnetic pin — dealers will buy every dip and sell every rally within this narrow band. Fade moves toward the call wall, don't chase a breakout until gamma thins above the cluster.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

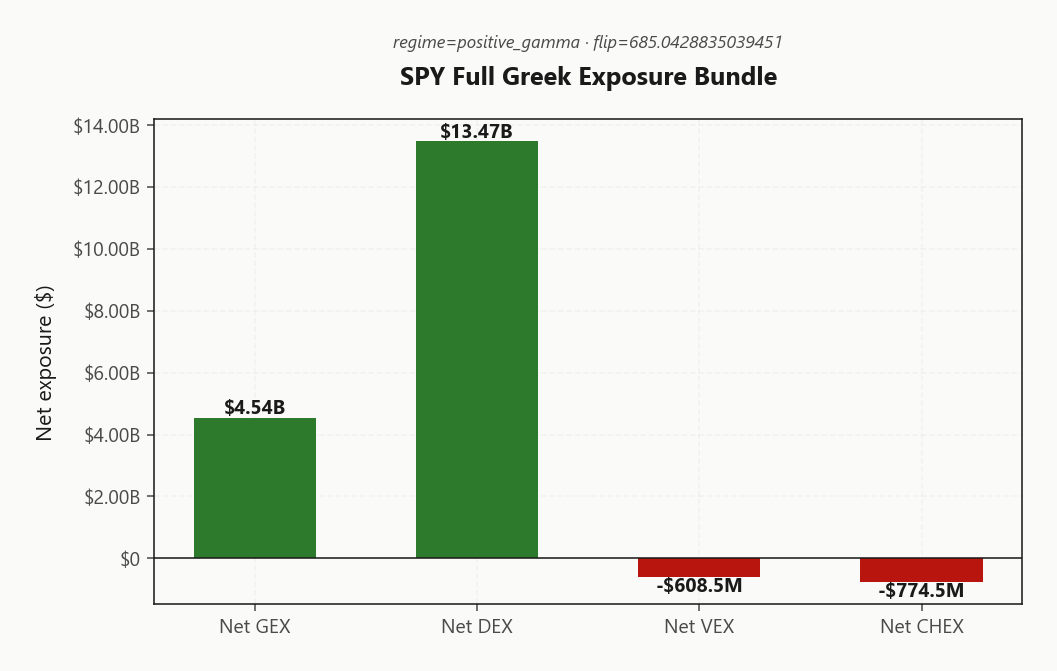

Dealer Vanna & Charm

Net vanna (VEX) at -$608.5M is the accelerant lurking beneath the positive_gamma surface. If implied vol spikes, dealers must sell delta — compounding any downdraft that gamma alone cannot absorb. Charm (CHEX) at -$774.5M reinforces the same directional bias: time decay is pushing dealers to shed exposure into the close, adding offered pressure through the afternoon session.

The charm pivot sits at 686 — the call wall — with spot virtually on top of it. Current bias reads neutral, meaning charm provides no directional edge from here. That neutrality is fragile. Above the pivot, gamma dampens; below it, vanna selling compounds. The entire positive-gamma thesis rests on vol staying suppressed at 18.97.

If VIX breaks higher through the term-structure inflection — where contango steepens from 17.29 toward 21.19 — vanna-driven dealer selling will overwhelm the gamma cushion, flipping the microstructure from mean-reverting to reflexive.

What it meansNegative vanna and charm create a hidden selling bias beneath the positive_gamma regime — stable while vol stays compressed, but a VIX spike converts the gamma cushion into a self-reinforcing downdraft as dealer hedging flips from dampening to amplifying.

Trading readGamma says dampen, but vanna and charm both say sell — the greeks are pulling in opposite directions. If the session stays quiet, gamma wins. If vol spikes, vanna overwhelms and the cushion evaporates. Stable on the surface, fragile underneath.The full Greek exposure bundle: net GEX (gamma), DEX (delta), VEX (vanna), CHEX (charm). Positive = dealers benefit, negative = dealers hedge against. Relative magnitudes show which Greek is currently dominant for hedging flows.

Cross-Asset Confirmation

The MOVE index at 72.15 is subdued — fixed income volatility is not confirming the geopolitical stress the headline tape implies. This is an equity-centric fear event, not a credit shock, and the distinction matters: rate markets are not transmitting contagion into the vol complex. Fear & Greed sits at 40 (fear), cautious but nowhere near the capitulatory extremes that trigger a reliable contrarian reversal — no signal to press longs on sentiment alone.

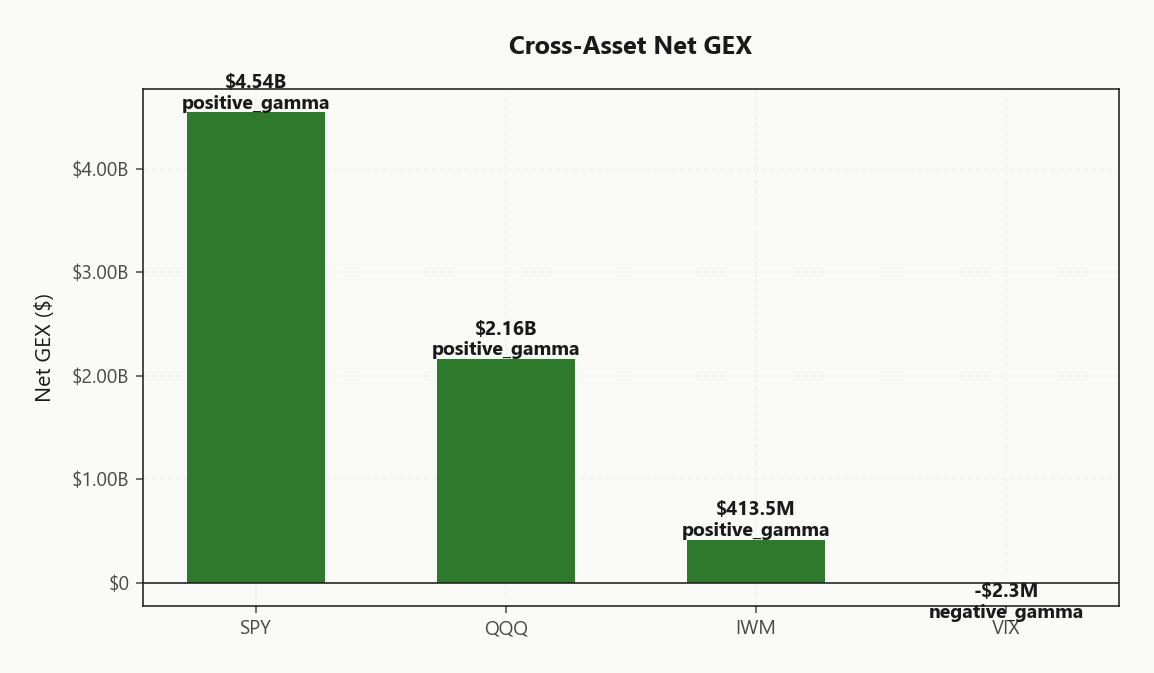

Cross-index gamma alignment is the structural anchor. SPY, QQQ at 617.40, and IWM at 265.03 all sit in positive_gamma territory — a rare synchronized configuration (aligned) that amplifies the mean-reversion thesis across the entire equity complex. When all three indices share the same dealer posture, breakdowns require a catalyst strong enough to overwhelm the dampening mechanism simultaneously.

Geopolitical shocks without credit contagion historically mean-revert within sessions. The Iran overhang is real, but until MOVE reprices or regime divergence emerges, the dealer cushion holds. Fade directional conviction; respect the gamma structure.

What it meansSubdued MOVE at 72.15 confirms no fixed income contagion — this remains an isolated geopolitical narrative. All three equity indices aligned in positive_gamma (aligned) strengthens the structural case for mean-reversion over directional follow-through.

Trading readAll three equity indices in positive gamma — rare synchronized alignment that amplifies the mean-reversion signal. No divergence today; if one breaks first, IWM's thinner gamma makes it the canary in the coal mine.Dealer net gamma across core index ETFs. Comparing SPY/QQQ/IWM reveals whether the dealer cushion is uniform or divergent — divergence is usually the day's most tradeable signal.

Scenario EV

The scoring model favors iron_condor at 45, targeting the 30-45 DTE window where the steep_contango curve offers maximum roll-down. Positive gamma across the equity complex supports the range-bound thesis — dealers dampen moves toward the call wall, and contango in the VIX term structure provides structural carry beneath the position.

The critical caveat: VRP at -5.24% signals realized moves are outrunning implied pricing. Standard wing widths are insufficient — widen aggressively or reduce notional to account for the gap between what options price and what spot delivers. QQQ VRP at -5.7% is even more negative, making tech the epicenter of this mispricing.

Put spreads score 32 as a geopolitical overlay. VVIX at 102.84 confirms standard_size — no need to half-size on vol-of-vol alone. Layer the condor with a put spread hedge below the gamma flip for asymmetric protection against the Iran tail.

What it meansiron_condor preferred in the 30-45 DTE range, but negative VRP (-5.24%) demands wider wings than the positive_gamma regime alone would suggest.

Regime Assessment

The vol regime sits at elevated — Elevated / Watchful — with VIX printing 18.97 and a half-life of 15 sessions. This is the middle ground: elevated enough to demand disciplined sizing, not extreme enough to force a wholesale book repositioning. The sticky half-life implies this watchful state persists through the week barring a catalyst — and the Iran overhang is exactly the kind of exogenous binary that can break a regime overnight.

Probability skew favors stability. The path to panic within the near term is narrow — positive gamma across SPY, QQQ, and IWM dampens the feedback loops that typically accelerate regime shifts, and VIX contango confirms the term structure isn't pricing an imminent break. Conversely, the moderate probability of easing back toward low vol over the coming sessions tells you the market wants to normalize — the gravitational pull is toward compression, not explosion.

Lean into that asymmetry. Wing premium is sellable at this regime level given the low panic probability, but the negative VRP at -5.24% demands wider structures and smaller notional than a pure elevated-regime read would suggest. The regime is watchful — so should your book be.

What it meansElevated / Watchful regime with a half-life of 15 sessions favors measured premium selling at the wings, but negative VRP across the equity complex requires wider structures to accommodate realized moves that continue to outpace implied.

Trading readVIX and VVIX are both easing while SKEW ticks higher — a subtle divergence. The market is paying less for vol but more for tail convexity, a combination that often precedes sharper-than-expected moves. MOVE is quiet, confirming equity-centric risk, not rates contagion.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Actionable Summary

The Elevated / Watchful regime favors iron_condor as the primary structure. Spot sits directly on the charm pivot at 686 — above this level, dealers dampen rallies into the call wall; below it, negative vanna (VEX at -$608.5M) accelerates any downdraft faster than gamma can absorb. Negative VRP at -5.24% across the equity complex means realized moves are outpacing implied — widen wings and cut notional versus what a pure positive_gamma read would suggest.

Steep VIX contango from 17.29 through 18.97 to 21.19 supports structural carry in the 30-45-day window, but VVIX at 102.84 is subdued given the geopolitical backdrop — VIX call convexity is cheap and worth owning as a tail hedge. The gamma flip at 685.04 sits just below spot; any gap through that level flips the entire dealer regime.

QQQ offers richer premium at 17.8% ATM IV with deeper negative VRP (-5.7%) for the same aligned regime. Avoid naked short premium in front-week expiries where daily-expiring gamma resets the microstructure overnight. Fear & Greed at 40 (fear) is cautious but not contrarian — maintain disciplined sizing per standard_size.

What it meansElevated / Watchful regime with iron_condor centered on the 686 charm pivot; negative VRP demands wider wings while subdued VVIX offers cheap tail convexity against the geopolitical overhang.

Equity rally built on Iran resolution hopes creates a fragile consensus — if diplomacy stalls over the weekend, Monday's open could gap against this entire positive gamma structure.

Direct military escalation rhetoric injects binary tail risk that VVIX isn't pricing — the disconnect between blockade language and subdued vol-of-vol is the asymmetric opportunity for tail hedgers.

LVMH's Iran-war revenue miss is the first major earnings casualty from the conflict — watch for contagion into consumer discretionary vol if luxury weakness spreads to US retail names.

NATO refusing the blockade isolates US escalation risk and raises the probability of a unilateral outcome — geopolitical tail becomes harder to hedge via traditional safe-haven correlations.

IMF meeting amid active conflict sets the stage for macro forecast revisions that could reprice the back end of the VIX term structure where uncertainty is already being warehoused.

OPEC cutting demand forecasts is the supply-side transmission mechanism from geopolitics to the real economy — energy vol could leak into equity vol if crude dislocates further.

Get today's live analysis

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime