Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

Positive gamma across index complex with contango vol curve; geopolitical overhang contained by dealer cushion and fear sentiment

All three equity ETFs sit in positive_gamma territory with spot pinned near the call wall, keeping dealer hedging flows supportive. The VIX term structure in contango with VVIX at 102.60 signals the market is not pricing binary outcomes despite Iran headlines. The tension: near-total 0DTE gamma dominance in SPY means this cushion evaporates at the close.

Forward Vol Geometry

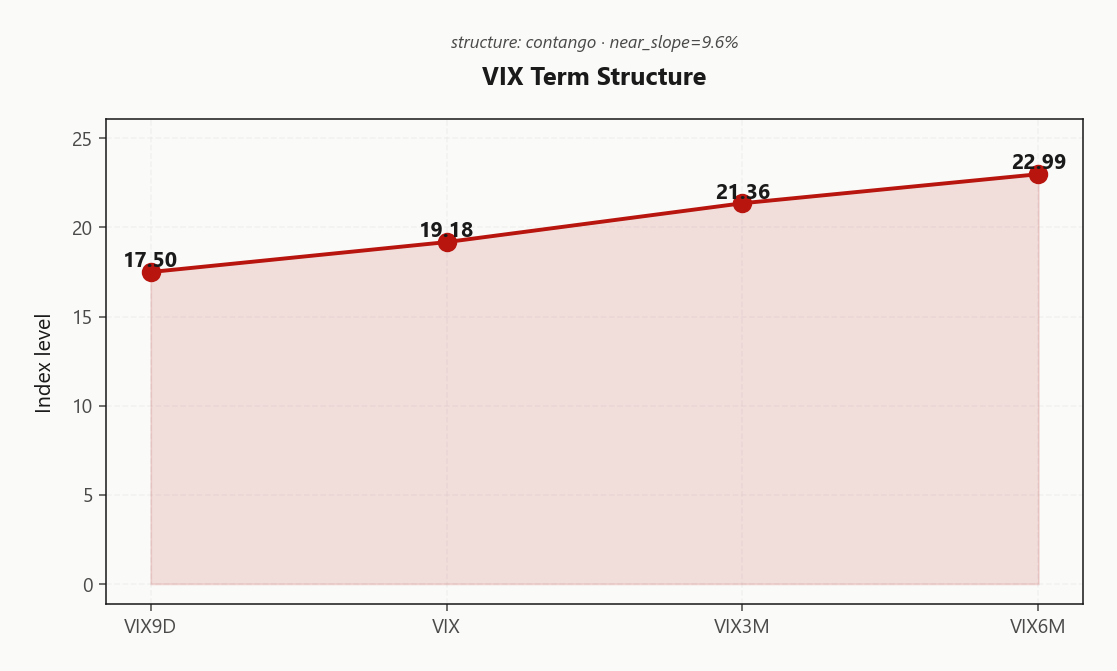

The VIX term structure sits in clean contango from front to back, with VIX9D at 17.50 trading below spot VIX at 19.18 — near-term vol crushed by the suppressive weight of positive_gamma dealer positioning across the index complex. The front end is where gamma does its work: positive dealer hedging flows compress realized moves, dragging short-dated implied vol lower and widening the carry window for front-week sellers.

Further out the curve, 21.36 at the three-month node and 22.99 at six months embed the geopolitical uncertainty premium the front end refuses to price. The steep_contango shape confirms the market expects current suppression to normalize higher — the forward curve is steepest in the front-week to biweekly tenor, making that the optimal roll-down zone for calendar positioning. Short front, long belly captures this gradient while respecting the back-end bid that reflects the Iran overhang's longer tail.

Forward vol regime: Steep contango — vol sellers favored. Near-term sellers collect structural carry, but the steep ascent from spot VIX into the belly warns against complacency — this curve shape inverts fast when a catalyst breaks the gamma cushion.

What it meanscontango term structure with a steep_contango forward curve favors short-dated premium selling backed by the positive_gamma dampening regime, but the widening spread from 17.50 to 22.99 signals the market is renting calm, not owning it.

Trading readClean contango from VIX9D through VIX6M with futures basis confirming — the vol carry trade is on, but it's a grind, not a gift. The steepness says the market expects current suppression to normalize higher. Carry works until it doesn't — the Iran overhang is the catalyst that could invert this.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

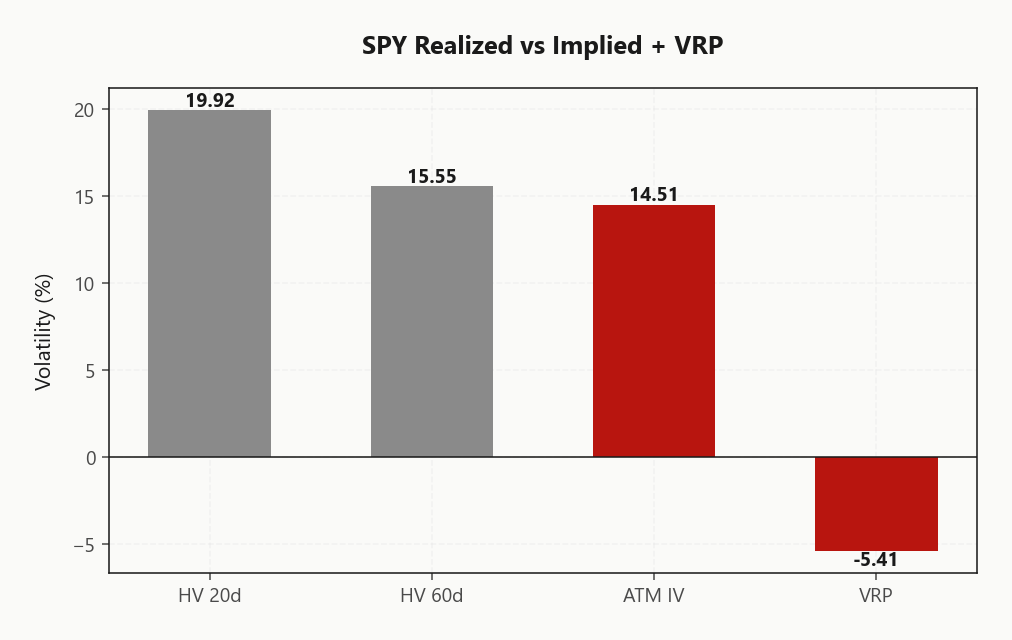

The options market is underpricing what the tape is actually delivering. SPY ATM implied vol at 14.51% sits well below the short-lookback realized at 16.54 and the monthly realized at 19.92, leaving VRP deeply negative at -5.41%. QQQ mirrors the disconnect — VRP at -5% with ATM IV at 18.49% — confirming this is a complex-wide mispricing, not a single-name anomaly. IWM completes the sweep at -2.79%.

The IV-RV spread assessment reads danger_zone: geopolitical shocks have driven realized moves the options surface has not yet absorbed. Contango term structure offers carry, but the short-vol edge is narrower than it appears — the market can move more than options price. Size accordingly, keep wings wider than usual, and treat premium collected as compensation for genuine realized-vol risk rather than free carry.

What it meansNegative VRP across SPY (-5.41%), QQQ (-5%), and IWM (-2.79%) flags a danger_zone environment — options are cheap to realized, making short-vol positions less attractive than the contango structure alone would suggest.

Trading readOptions are cheap to what the market has actually been doing — realized vol exceeds implied across every index ETF. This is a warning for vol sellers: the contango carry is real, but the market can move more than options price. Keep wings wider than usual on any short vol position.HV20 and HV60 are realized volatility over the last 20 and 60 trading days. ATM IV is what the market is pricing now. VRP = ATM IV − HV20: positive means options are expensive vs. recent reality (vol sellers' market), negative means options are cheap.

Skew Convexity

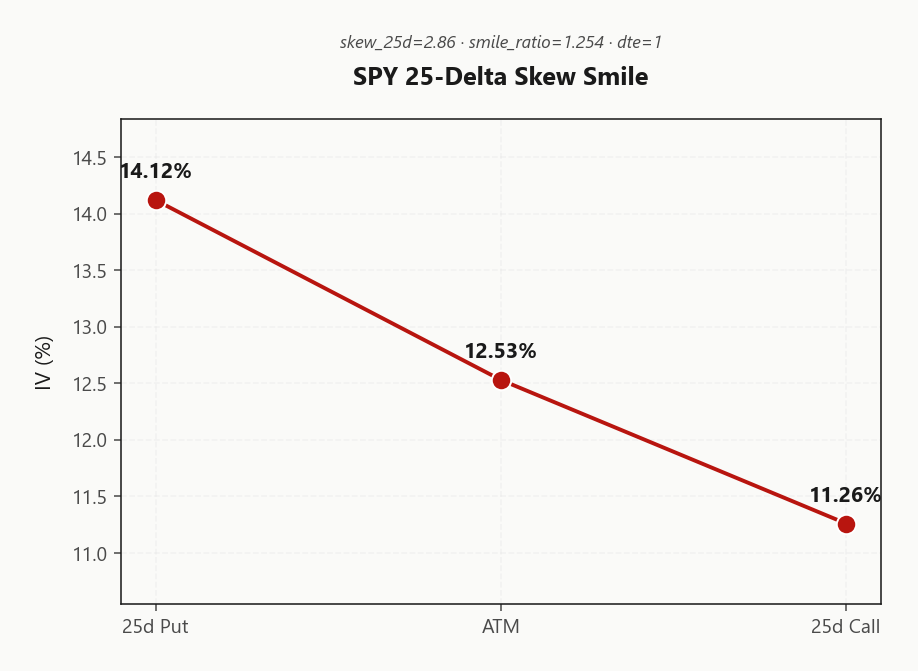

SPY's quarter-delta skew prints at 2.86% with a smile ratio of 1.25% — orderly downside demand, not crash-hedging. Put quarter-delta IV at 14.12% trades meaningfully above ATM at 12.53%, confirming protection buyers are methodical rather than desperate. This skew shape favors put spread structures over naked puts — you're paying for a well-bid left tail without the panic premium that makes spreads prohibitively wide.

The call wing tells the other story: quarter-delta call IV at 11.26% sits compressed against ATM, reflecting no upside conviction in the options market. With the geopolitical overhang dominating sentiment and fear on the Fear & Greed gauge, nobody is leveraging the rally through calls. That flat right wing is an opportunity — upside participation via calls is relatively cheap against this backdrop of suppressed ATM IV at 14.51% and a contango vol curve.

What it meansMeasured left-tail demand with a smile ratio above unity and flat call skew — downside hedges belong in spread form, and the cheap call wing offers asymmetric upside exposure if the positive_gamma regime holds.

Trading readOrderly put skew with a smile ratio above unity says protection buyers are methodical, not panicked. The flat call wing means nobody is chasing upside through options — any rally is being sold into, not leveraged. Spread-based downside hedges beat naked puts here.25-delta skew profile — put IV, ATM IV, call IV. Put wing above call wing means downside protection is richer than upside (typical for equity indices). Flat or inverted skew is a stress signal.

Vol-of-Vol Structure

VVIX at 102.60 sits in the normal range — the options-on-options market is not pricing a binary outcome despite active Iran escalation rhetoric. If the geopolitical overhang were genuinely threatening a regime break, VVIX would be diverging higher while VIX stayed contained — that classic hidden-jump-risk signature is absent here.

VIX at 19.18 with a contained VVIX/VIX ratio confirms orderly vol pricing across the complex. The vol-of-vol surface is telling you the same story as the equity gamma structure: dealers are comfortable, tail hedgers are not scrambling, and the convexity bid remains subdued. This is not the setup where you pay up for crash protection.

Sizing guidance: standard_size. Standard expressions are appropriate — no need to trim notional or widen wings on account of vol-of-vol dynamics alone. The Iran overhang is an equity sentiment event, not a vol regime catalyst.

What it meansVVIX at 102.60 in normal territory with VIX at 19.18 confirms no hidden jump risk — maintain standard_size position sizing and treat geopolitical noise as contained within the current dampening regime.

Dispersion Spread

SPY ATM implied vol at 14.51% sits compressed against a cross-asset tone of —, while the mega-cap constituents driving today's top GEX shifts — AMZN, MSFT, AAPL, META — each carry single-name ATM IVs running roughly double the index level. That wedge between suppressed index vol and elevated component vol is the dispersion signal: correlation is moderate, idiosyncratic risk is priced at the single-name level, and the index stays pinned under its 686.00 call wall.

QQQ ATM IV at 18.49% confirms the tech premium — earnings-cycle event risk across the Mag-cap complex inflates the Nasdaq tape relative to SPY, yet both indices hold positive_gamma with spot above their respective flips. When gamma is positive across the complex and single-name positioning is this dispersed, index-level premium selling is the cleaner expression. Sell the compressed index, respect the idiosyncratic names.

IV dispersion across SPY's strike surface reads {"cross_expiry":2.3,"cross_strike":67.37} — elevated cross-strike spread with contained cross-expiry variance favors short index straddles over single-name directional plays in this regime.

What it meansIndex vol is compressed at 14.51% while single-name movers carry substantially higher implied — prefer SPY/SPX premium selling over component trades when positive_gamma holds across the complex and QQQ's tech premium at 18.49% reflects earnings-cycle idiosyncratic risk rather than systemic repricing.

Liquidity & Microstructure

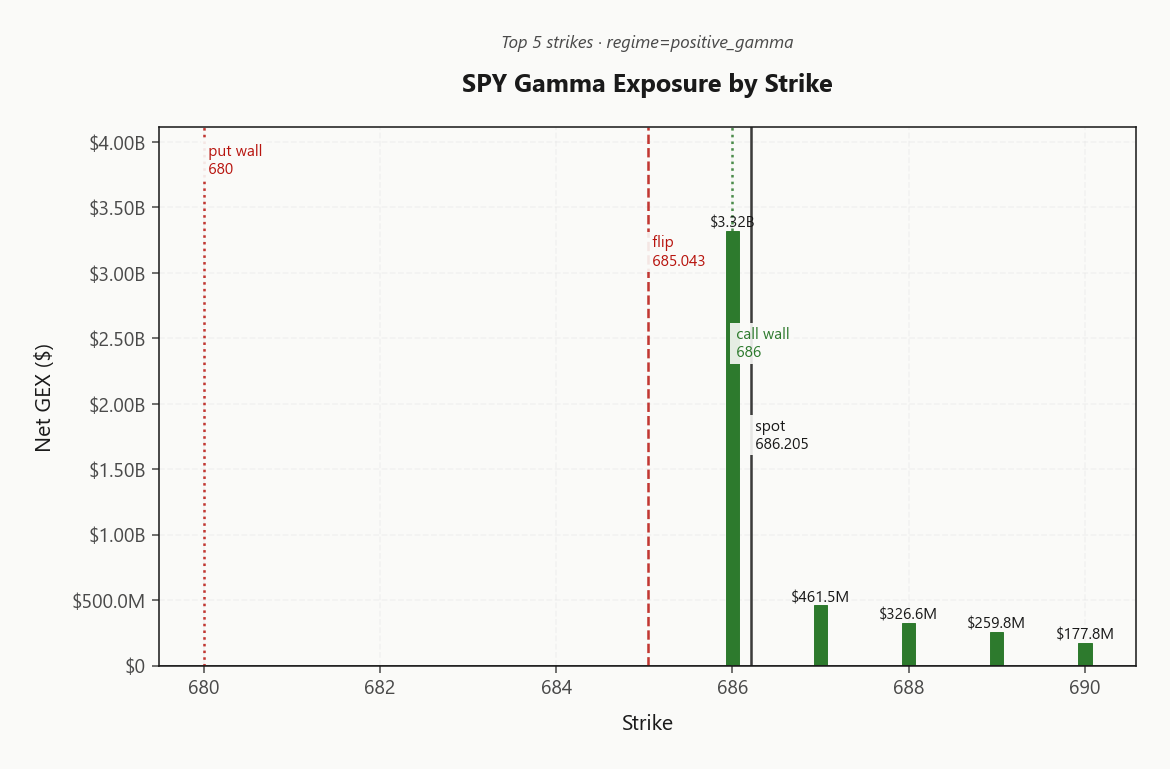

The gamma landscape compresses into a single dominant level: the 686.00 call wall concentrates $3.32B in strike-level GEX, pinning spot and forcing dealers to fade every intraday move. The gamma flip at 685.04 sits just below — breach it and the hedging regime inverts from dampening to amplification with no gradual transition between the two states.

Below the flip, the put wall at 680.00 becomes the first significant downside magnet where dealer selling pressure would consolidate. Longer-dated positioning clusters at the 660 highest OI strike, reflecting institutional hedges placed well below current levels — a structural anchor that would only matter in a multi-day unwind.

The critical fragility: 99.3%% of total SPY GEX is concentrated in today's expiration. This entire support architecture — the call wall pin, the flip cushion, the dealer backstop — evaporates at the close and rebuilds from scratch tomorrow.

What it meansMassive gamma concentration at 686.00 with $3.32B in strike GEX creates a session pin, but 99.3%% 0DTE dominance means tomorrow opens structurally unhedged — plan overnight risk accordingly.

Trading readMassive gamma concentration at the call wall creates a magnetic pin for today's session — dealers buy every dip and sell every rip within this zone. The dropoff below the gamma flip is steep, meaning a break lower triggers an abrupt shift from dampening to amplification with no gradual transition.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

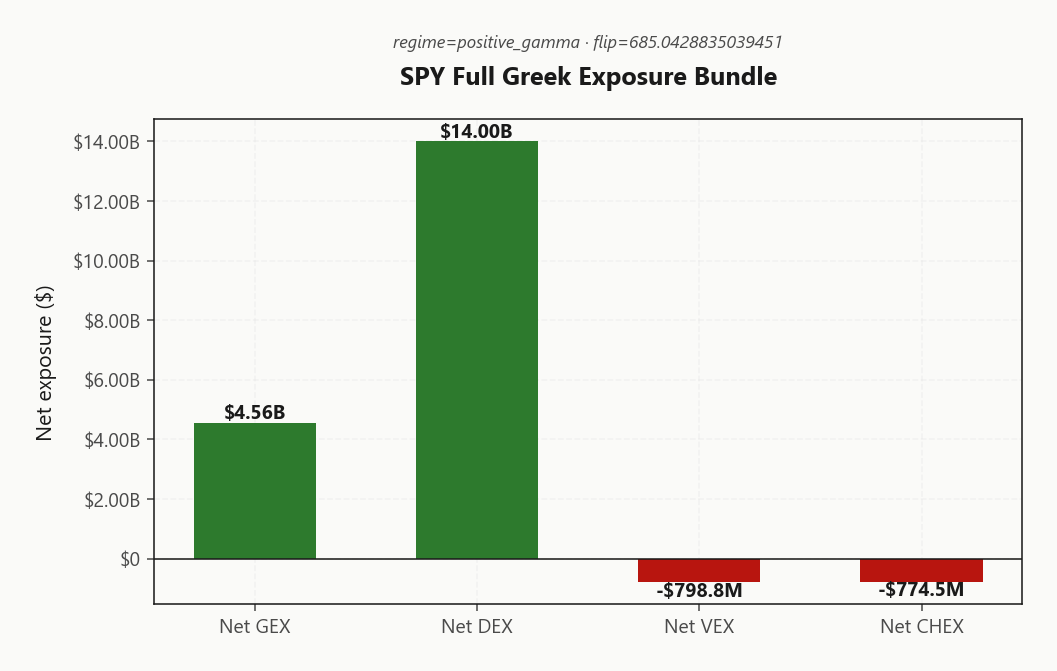

Vanna exposure sits negative at -$798.8M, establishing a clear asymmetry: any vol spike forces dealers to sell delta, compounding downside pressure beyond what gamma alone would imply. With the charm pivot anchored at 686 and spot essentially pinned to it, the current bias registers neutral — but that neutrality is precarious. Net charm at -$774.5M already tilts dealer flow toward selling into the close, layering a persistent headwind on top of the vanna risk.

The danger scenario is sequential: an Iran headline jolts implied vol higher, triggering vanna-driven dealer selling, while charm decay is already pushing the same direction. Below the pivot, both flows accelerate in tandem — a double accelerant with no offsetting bid until the put wall at 680.00. Above the pivot, positive gamma absorbs the shock. Respect the flip zone; the margin between dampening and amplification is measured in ticks, not points.

What it meansVanna and charm are aligned bearish below 686 — a vol spike converts the current neutral stance into an active selling accelerant, making the gamma flip the session's critical threshold.

Trading readGamma says calm but vanna and charm are both pulling negative — if vol spikes on an Iran headline, the vanna accelerant kicks in while charm already leans sell into the close. This is a regime that supports mean reversion UNLESS vol moves first.The full Greek exposure bundle: net GEX (gamma), DEX (delta), VEX (vanna), CHEX (charm). Positive = dealers benefit, negative = dealers hedge against. Relative magnitudes show which Greek is currently dominant for hedging flows.

Cross-Asset Confirmation

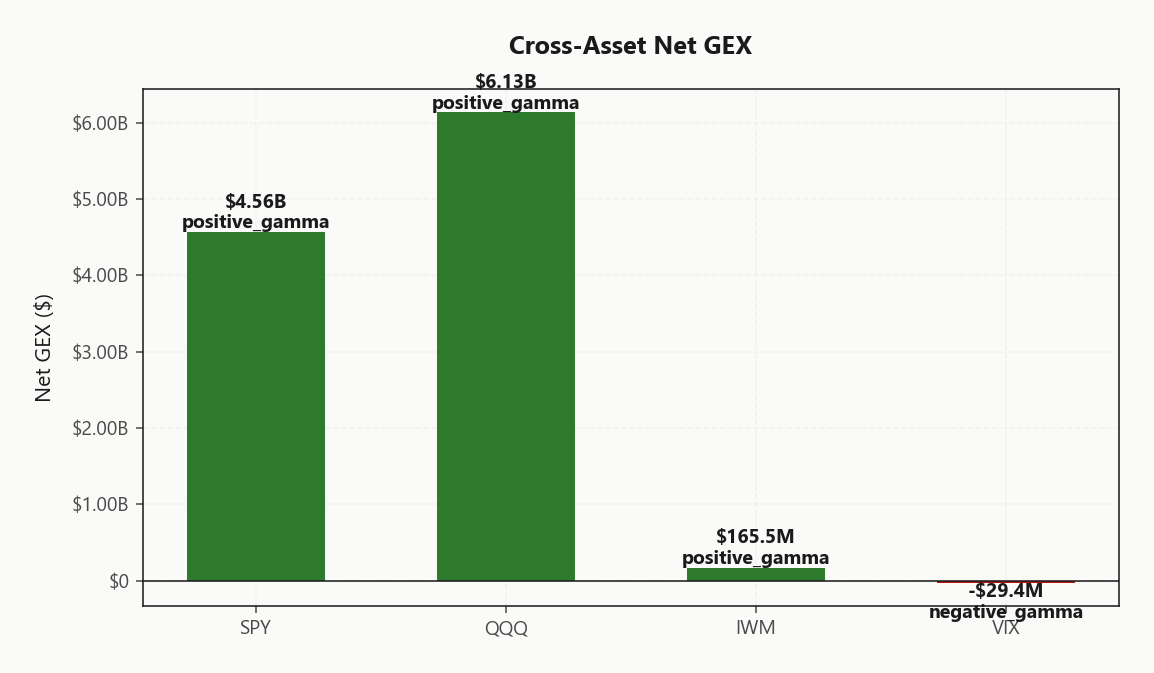

SPY, QQQ at 617.68, and IWM at 265.11 all sit in positive_gamma above their respective gamma flips — cross-asset regimes are —, leaving no divergence trade on the table. Dealer hedging flows are uniformly suppressive across the index complex, and the breadth of that dampening argues against single-index bets today.

The MOVE index at 72.15 confirms bond vol is contained — this is not a rates or credit shock despite the Iran overhang. Fear & Greed reading 41 (fear) shows the crowd is hedged but not capitulating, providing a contrarian cushion that limits further downside without triggering forced buying.

The takeaway: geopolitical noise is an equity sentiment event being absorbed by a structurally supportive gamma regime. Until MOVE breaks higher or index regimes diverge, treat the complex as a single dampened unit.

What it meansUniform positive_gamma across SPY, QQQ, and IWM with MOVE at 72.15 and sentiment at fear confirms this is headline-driven equity fear, not systemic risk — no regime divergence to exploit.

Trading readAll three equity ETFs aligned in positive gamma — no divergence trade today. The uniform dampening effect means individual index selection matters less than structure selection. VIX in negative gamma is the norm and confirms vol itself is the amplified asset, not equities.Dealer net gamma across core index ETFs. Comparing SPY/QQQ/IWM reveals whether the dealer cushion is uniform or divergent — divergence is usually the day's most tradeable signal.

Scenario EV

The scoring framework ranks iron_condor highest at 41, driven by the convergence of positive_gamma across the index complex, a contango vol curve, and VVIX in normal territory at 102.60. This trifecta supports premium collection — dealers dampen intraday moves, contango bleeds front-end IV, and vol-of-vol confirms no binary event premium worth paying for.

The complication is VRP. SPY implied at 14.51% undershoots realized with VRP at -5.41% — assessment reads unknown. Target the 30-45 day window to capture the steepest contango roll-down while clearing the overnight gamma reset. Anchor wings around the 686.00 call wall and 680.00 put wall, but keep them wider than usual to respect the realized overshoot.

Put spread alternatives score lower — orderly skew with a smile ratio of 1.25% does not justify a directional tilt. The charm pivot at 686 holds neutral, reinforcing the non-directional framework.

What it meansIron condor at 30-45 DTE captures contango roll-down while positive_gamma dampens intraday risk, but negative VRP at -5.41% demands wider wings — realized vol is outpacing implied, and the overnight gamma reset strips today's dealer cushion entirely.

Regime Assessment

The vol regime reads elevated — Elevated / Watchful. VIX at 19.18 sits above its long-run median but well below panic thresholds, with the full term structure in contango from 17.50 through 22.99 confirming the market expects current suppression to normalize higher rather than spike. VVIX at 102.60 in the normal range and Fear & Greed at 41 (fear) reinforce the picture: hedged but not panicking, watchful but not bracing for a binary outcome.

The regime's half-life of 15 sessions points to gradual normalization over the coming weeks absent a geopolitical catalyst. Transition probability to panic is low over the near term, while the path back to subdued vol over a broader horizon remains the base case. This is a regime test, not a regime break — the Iran overhang pressures sentiment but has not cracked the structural dealer cushion that keeps all three index ETFs pinned in positive_gamma territory above their respective flips.

What it meansElevated but contained vol regime with a half-life of 15 sessions favors gradual normalization — VIX at 19.18 is decaying toward calm unless a geopolitical escalation breaks the positive_gamma dealer cushion and flips hedging flows from suppressive to amplifying.

Trading readVIX and VVIX declining in tandem while SKEW ticks up — the market is getting calmer on average but paying slightly more for tail protection. This quiet divergence often precedes a directional resolution. MOVE staying flat confirms this is an equity sentiment story, not a rates or credit event.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Actionable Summary

Primary expression: iron_condor in the 30-45 DTE window, centered on the charm pivot at 686. The 686.00 call wall and 680.00 put wall frame your wings. Positive gamma across the index complex keeps intraday mean reversion intact, and contango through the full VIX curve delivers carry into the roll-down — but 99.3%% of SPY gamma is rented via today's expiry, leaving tomorrow's open structurally naked.

Avoid naked short puts. VRP at -5.41% means realized vol is outrunning implied — spreads cap the gap. VVIX at 102.60 in normal range confirms standard_size sizing; no need to pare despite geopolitical noise.

Watch the flip. A close below 685.04 shifts from Elevated / Watchful to amplification, with vanna (-$798.8M) and charm (-$774.5M) both accelerating the sell. Iran headlines remain the binary catalyst — a deal compresses vol hard, escalation breaks the floor.

What it meansThe regime favors defined-risk premium collection via iron_condor anchored at 686, but negative VRP and near-total intraday gamma dominance demand spread structures only — respect the 685.04 flip as the line between Elevated / Watchful and dealer amplification.

Market-defining tone setter — hope for US-Iran resolution is the catalyst compressing vol and keeping risk-on flows alive; failure to progress could unwind the session's gains.

Direct military escalation rhetoric raises the binary outcome probability — this is the tail risk that would break the positive gamma regime if it escalates beyond posturing.

Oracle's sharp bounce signals rotation back into beaten-down software names, suggesting the AI disruption selloff was overdone and risk appetite is broadening beyond mega-cap.

LVMH earnings miss from Iran war impact shows geopolitical risk is now hitting consumer-facing revenue — watch for earnings guide-downs to spread across multinationals.

NATO's refusal to join the blockade isolates US policy and raises the probability of a prolonged standoff — the longer the overhang, the more it weighs on the VIX term structure back end.

IMF meeting coinciding with active conflict creates a policy coordination moment — any hawkish commentary on growth downgrades could shift the MOVE index and rates vol.

OPEC cutting demand forecasts is supply-side confirmation that the conflict is already repricing energy inputs — watch crude vol for second-order equity impact.

Get today's live analysis

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime