Help us double down on what's working, instead of guessing. Takes 5 seconds, totally optional.

Market Overview

Data-driven market structure analysis powered by lab.flashalpha.com - volatility, dealer positioning, and regime assessment across the index complex, refreshed multiple times per trading day. Every number is pulled straight from our API endpoints by deterministic code.

FlashAlpha ResearchAI-assisted

Generated

Validated citations - no literal numbers from LLM

You're reading yesterday's market analysis

Basic unlocks today's post-open analysis (9:45 ET).

Growth unlocks all 3 daily refreshes (open, midday, close) plus actionable trade ideas and “What it means for your trading”.

Growth unlocks the full trading day: midday (12:30 ET) + close wrap (4:15 ET), actionable trade ideas per section, and “What it means for your trading” analysis.

Elevated vol contango with negative VRP — options cheap to realized, tail hedging surging via SKEW at 156.93

Equities rallied on US-Iran diplomatic progress, pushing SPY to 686.58 while VIX eased to 19.12. The term structure sits in contango with SKEW surging to 156.93, signaling aggressive tail-hedging beneath a calm surface. Negative VRP across the complex means options remain cheap to realized moves — a regime favoring structured premium selling with defined risk.

Forward Vol Geometry

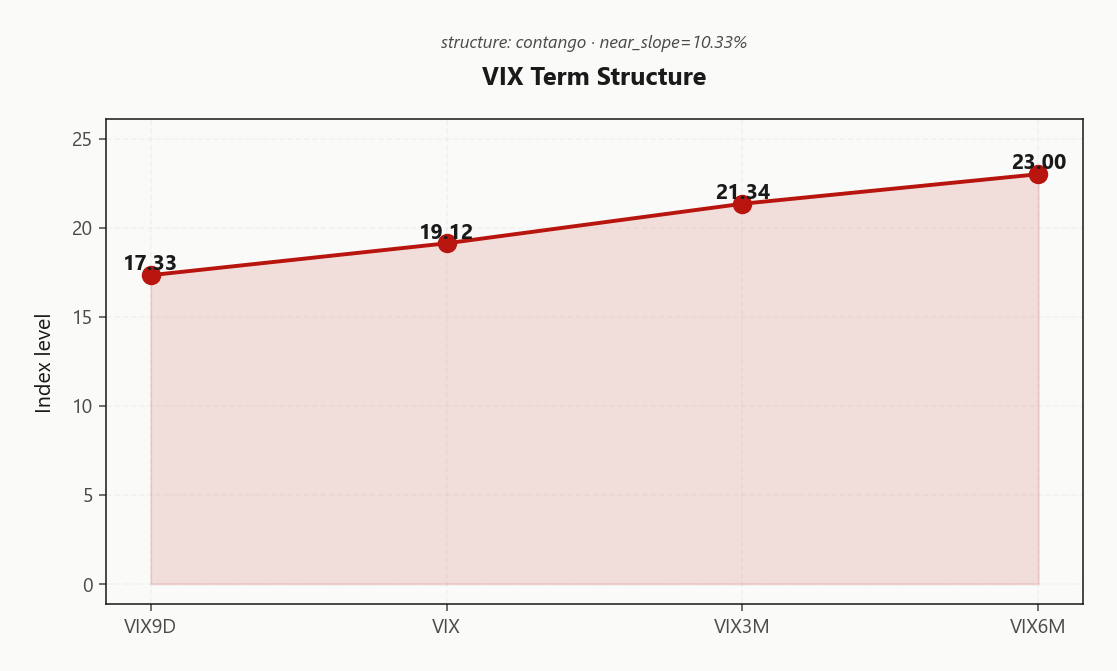

The VIX term structure prints clean contango from front to back — VIX9D at 17.33 sits well below the spot VIX at 19.12, which in turn trails VIX3M at 21.34 and VIX6M at 23.00. The slope is steep enough to generate meaningful roll-down carry for short vol, but the back end's persistent premium warns that the market is pricing sustained uncertainty from the Iran binary well beyond near-term realized.

Forward vol regime reads steep_contango — the belly of the curve, where forward vol peaks before flattening, marks the sweet spot for carry capture. Selling the near-dated suppression against elevated longer-dated forwards maximizes theta-to-vega efficiency. Calendar structures and iron condors anchored in that belly window extract the steepest carry while respecting the curve's embedded warning about geopolitical tail risk further out.

The key nuance: this contango is orderly, not complacent. Near-term vol is compressed by the diplomatic de-escalation bid, but the back end refuses to participate — a market that expects the grind to persist even if headlines stay constructive. Vol sellers are favored, but the curve itself is telling you not to reach for duration.

What it meansSteep contango with VIX9D at 17.33 versus VIX6M at 23.00 favors short vol carry in the belly of the curve, but the persistent back-end premium signals the market is not underwriting geopolitical resolution — size accordingly and avoid selling duration.

Trading readClean contango from VIX9D through VIX6M — the slope is steep enough to generate meaningful carry for short VIX structures. The futures basis confirms rich roll yield. But this contango is a bet on no escalation — the Iran binary could invert it overnight.Forward VIX curve: VIX9D (9-day), VIX (30-day), VIX3M, VIX6M. Upward slope (contango) = calm regime + vol sellers favored. Downward (backwardation) = stress, vol buyers favored. Slope matters more than level.

Realized Vol Structure

Realized vol is running well above implied across the entire index complex, creating a negative VRP regime that complicates the otherwise constructive contango backdrop. SPY ATM IV sits at 14.83% against trailing realized of 19.91, putting the risk premium at -5.08% — options are meaningfully underpricing the moves that are actually printing on the tape. QQQ is even more mispriced at -5.12%, with tech delivering larger swings than the surface reflects.

IWM offers the narrowest gap at -2.29%, making small-caps the closest to fair-value pricing and the least treacherous venue for premium sellers who need to be in the trade. The paradox is stark: the term structure screams carry, but the VRP says you're selling insurance below replacement cost. Short vol here is a bet on imminent realized deceleration — and until HV rolls over below implied, that bet is offside.

For structured sellers, this means tighter wings, smaller notional, and a willingness to let carry compound rather than reaching for credit. Long vol via debit spreads retains edge as long as realized persists — the contango curve will eventually win, but timing that compression against a geopolitical binary is the wrong trade to force.

What it meansNegative VRP at -5.08% for SPY and -5.12% for QQQ signals options are cheap to realized moves — short vol needs realized to decelerate before the carry trade works, favoring defined-risk structures with compressed notional until the VRP gap closes.

Skew Convexity

Put skew across SPY is steep and getting steeper. Quarter-delta skew prints at 5.36% with a smile ratio of 1.42%, reflecting aggressive left-tail hedging demand. The put wing at 18.09% is paying up materially over calls at 12.73% — institutions are bidding downside protection into the rally, not through it.

The cross-index divergence is the actionable signal. QQQ skew sits notably flatter at 1.85%, confirming the hedging bid is concentrated in broad index puts rather than tech-specific protection. IWM skew at 6.83% is the steepest in the complex, flagging small-cap vulnerability to the geopolitical backdrop. Institutional desks are using SPY puts as portfolio-level insurance and paying up for IWM tails while leaving QQQ relatively unhedged.

This divergence creates relative value: SPY put spreads are rich versus QQQ equivalents. Cross-index skew trades — selling SPY put skew against flatter QQQ skew — offer carry if the hedging bid normalizes as diplomatic catalysts resolve.

What it meansSteep, diverging put skew signals institutional tail hedging concentrated in SPY and IWM over QQQ — the market is insuring broad portfolios and small-cap exposure, not tech-specific risk. Relative value favors fading rich SPY put spreads against flatter QQQ skew on any geopolitical de-escalation.

Vol-of-Vol Structure

VVIX sits at 102.63 — squarely in the normal band and notably dislocated from prior geopolitical escalation episodes where vol-of-vol front-ran VIX by days. With VIX at 19.12, the VVIX/VIX ratio is unremarkable, embedding no jump-risk premium and no expectation of an imminent regime break. The vol-of-vol level reads normal, confirming that the options-on-options complex is pricing a grind, not a crash.

This distinction matters for book construction. Sizing guidance flags standard_size — there is no signal to haircut notional or widen wings defensively the way you would if VVIX were printing triple digits above the century mark. The market is telling you elevated implied vol is the new steady state for this geopolitical cycle, not a coiled spring. Carry trades, iron condors, and calendar structures can all run at full allocation without the convexity tax that a hot VVIX regime demands.

Watch for divergence: if VVIX begins to detach upward while VIX holds or drifts, that is the early warning that the grinding regime is transitioning toward binary pricing — and the cue to cut size before the tape forces it.

What it meansVVIX at 102.63 with VIX at 19.12 signals a grinding elevated-vol regime with no embedded jump premium — standard_size is appropriate, and no defensive position adjustments are warranted until vol-of-vol begins decoupling to the upside.

Dispersion Spread

Single-name gamma is stabilizing fast. NVDA, AAPL, MSFT, and AVGO all posted strongly positive GEX shifts in today's session — dealers are flipping from short to long gamma across the mega-cap complex, a tell that single-stock vol is compressing even as the index tape carries a geopolitical premium. SPY ATM IV at 14.83% and QQQ at 18.37% remain rich relative to what constituent-weighted vol would imply — the correlation bid is doing the heavy lifting.

This is a textbook dispersion setup. Index implied vol overshoots because hedgers use SPY and QQQ puts for portfolio insurance, inflating the correlation premium while individual names de-risk underneath. The breadth of the gamma flip — spanning semis, consumer hardware, enterprise software, and streaming — argues this isn't idiosyncratic; it's systematic re-risking at the single-name level.

Lean into the wedge: sell index vol where the correlation premium is fattest, avoid single-name shorts where the gamma shift has already repriced the surface. The edge is in the spread between the two, not in either leg alone.

What it meansIndex IV is running above constituent-weighted vol as the correlation bid from geopolitical hedging inflates SPY and QQQ premiums — favor index premium selling over single-name structures while the dispersion gap persists.

Liquidity & Microstructure

Close-wrap exposure levels — OI concentration, gamma flip, and wall strikes — are in reset for this refresh cycle, leaving options flow as the primary microstructure read. The signal is unambiguous: SPY's put/call volume ratio sits at 1.833 despite a solidly green tape, and IWM is even more skewed at 2.523, marking small-caps as the locus of institutional hedging demand. VIX flow confirms from the other side — a put/call ratio of 0.624 reflects call-heavy positioning as portfolio managers layer vol insurance atop equity longs.

The persistence of protective flow through a rally session is the contrarian tell worth watching. Dealers absorbing this put supply are accumulating short put inventory that converts to mechanical buying pressure on any dip toward concentrated strike zones. When exposure data repopulates on the next intraday refresh, watch for the gamma flip to re-establish — the interplay between that level and the current put-heavy flow map will define whether dealer mechanics reinforce or resist the directional bid.

What it meansInstitutional hedgers refused to lift protection despite positive price action — put-heavy flow across SPY and IWM with VIX call accumulation signals a market that is long but actively insuring the tail, a setup that often marks local bottoms when dealer gamma re-engages.

Trading readClose-wrap exposure data is in reset — the intraday gamma map will repopulate with Tuesday's flow. The key pre-read: heavy put volume ratios across all three index ETFs suggest the gamma map will show put-heavy OI concentration below spot, meaning any dip toward those clusters triggers dealer buying that supports prices.Net dealer gamma exposure at each strike. Green bars = dealers long gamma (dampens moves toward the strike), red bars = short gamma (amplifies moves). Lines show spot, gamma flip (regime boundary), and the highest-gamma call/put strikes (walls).

Dealer Vanna & Charm

Vanna and charm exposures are effectively zeroed out across the index complex. SPY net vanna exposure sits at $0 and net charm exposure at $0 — dealers carry no mechanically forced delta from either vol moves or theta bleed at current levels. This is a rare clean sheet: neither a VIX rip nor quiet weekend decay will trigger the kind of systematic hedging flows that compress or amplify spot moves.

The charm pivot prints at 50, well below spot at 686.58, with bias registering neutral. That distance matters — there is no nearby structural floor where time-decay-driven dealer buying would catch a dip. Spot is untethered from the mechanical anchors that typically dampen intraday range.

For directional desks, this is the cleanest tape in weeks. Price action will track flow and headline catalysts — particularly the Iran diplomatic binary — without dealer gamma acting as a governor. Express conviction accordingly, but respect the absence of the cushion on the way down.

What it meansFlat vanna ($0) and charm ($0) with a neutral pivot bias leave dealers disengaged from mechanical hedging — spot moves purely on flow and news, giving directional trades unusually clean expression in both directions.

Cross-Asset Confirmation

The cross-asset tape is aligned on direction but fractured on conviction. SPY, QQQ at 618.72, and IWM at 265.29 all participated in the rally — no rotational divergence, no sector-level cracks. Yet the MOVE index firming to 74.42 while equity vol compressed tells the real story: the rates market is not underwriting the geopolitical de-escalation thesis with the same enthusiasm. Bond vol rising into an equity bid is a divergence that resolves — and rarely in the direction equity bulls prefer.

Fear & Greed sitting at 41 (fear) despite a green tape confirms this is a relief bounce, not a positioning reset. Institutions are lifting offers while keeping hedges intact — constructive price action layered over cautious sentiment. The MOVE divergence is the canary: if bond vol continues to firm while equity vol rolls over, the reconciliation will come through rates repricing into equities, not the reverse.

What it meansCross-asset regimes are aligned with no SPY-QQQ divergence, but MOVE at 74.42 diverging from equity calm and sentiment pinned in fear territory flag this as a relief rally lacking full cross-market confirmation — watch for rates vol to bleed into equity positioning if the divergence persists.

Scenario EV

The regime scores iron_condor as the highest-EV structure, driven by steep contango across the VIX curve and orderly vol-of-vol at 102.63. With VIX9D at 17.33 rolling into VIX at 19.12, contango roll-down compounds with theta—but only if you target the belly. Optimal DTE sits at 30-45, where forward vol peaks before flattening into VIX3M at 21.34.

The caveat is negative VRP: SPY implied at 14.83% trails realized at 19.91, and QQQ’s gap is wider still at -5.12%. You are selling insurance priced below recent claims—banking on realized deceleration that the Iran binary could delay. Put spreads score materially lower precisely because the short-put leg sits deepest in this mispricing. Keep wings tight, accept narrower credit, and let the defined-risk structure absorb any realized overshoot.

Conviction is moderate at 43—not a table-pounding setup. Size per standard_size guidance; VVIX confirms no jump-risk premium worth dodging.

What it meansDefined-risk premium selling via iron_condor captures contango roll-down and theta at 30-45 DTE, but negative VRP across the index complex means conviction stays moderate at 43—size standard, keep wings tight, and respect that realized has not yet rolled over.

Regime Assessment

The vol regime sits squarely at elevated — Elevated / Watchful. VIX at 19.12 is above the comfort zone but well short of crisis levels, and VVIX at 102.63 confirms no jump-risk premium is embedded. The term structure remains in orderly contango, reinforcing that the market expects this elevated baseline to grind rather than spike. Transition probability to panic over a five-session horizon is negligible.

The half-life of this regime runs 15 sessions — sticky enough to structure around, not fleeting enough to fade. The path to low vol is blocked by the Iran binary: diplomatic resolution compresses the entire surface fast, escalation tips the regime toward panic. SKEW surging to 156.93 while headline vol eases tells you institutions agree — they are trading the regime, not the headline, layering tail protection beneath a surface that looks constructive.

Size for persistence. Trade the Elevated / Watchful regime as the base case and let the geopolitical catalyst resolve on its own timeline.

What it meansRegime classified elevated with a 15-session half-life — elevated vol persists as the base case, with Iran diplomacy the sole binary capable of forcing a rapid regime transition in either direction.

Trading readVIX and VVIX declining together while SKEW surges — a non-trivial divergence. The vol complex is saying: we don't expect a spike (low VVIX), but we're paying up for tail protection anyway (high SKEW). MOVE rising while equity vol falls adds another crack in the consensus. Watch for these divergences to resolve — they usually do, and not always in the benign direction.VIX = equity vol. VVIX = vol of vol (is the fear gauge itself being stressed?). SKEW = cost of tail hedges vs ATM. MOVE = bond vol. Divergences between them (e.g. calm VIX but elevated VVIX) often precede regime shifts.

Actionable Summary

Trade: iron_condor structures in SPY, targeting the 30-45 DTE belly where contango roll-down is steepest. Size at standard_size — VVIX at 102.63 confirms no jump-risk premium worth ducking. Keep wings tight and accept thinner credit: negative VRP across the complex (SPY at -5.08%, QQQ at -5.12%) means you are selling insurance below realized, banking on compression that the tape has not yet delivered.

Avoid: Naked short puts and undefined downside — negative VRP plus a binary geopolitical catalyst makes open-ended risk reckless on any single session. The regime reads Elevated / Watchful, a grinding elevated vol that persists over a 15-session half-life rather than spiking, unless Iran diplomacy collapses.

Watch: MOVE at 74.42 is firming while equity vol compresses — the bond market is not buying the de-escalation narrative as fully as stocks. If that divergence widens, the cross-asset crack arrives through rates, not equities. Charm pivot at 50 anchors dealer flow structure, but exposure data refreshes intraday — levels are guides, not gospel.

What it meansDefined-risk premium selling via iron_condor is the highest-EV expression of a Elevated / Watchful regime running steep contango with negative VRP — but the MOVE divergence and surging SKEW at 156.93 say tail hedges belong in the book alongside any short vol.

Risk-on catalyst as markets price de-escalation — the Iran resolution narrative is single-handedly driving the equity bid and suppressing near-term vol, making it the regime's key binary.

Oil retreating on dialogue hopes is a direct inflation tailwind — if sustained, removes the energy cost overhang that's been supporting elevated realized vol across the complex.

Hormuz blockade details quantify the supply disruption risk — this is the tail scenario that keeps SKEW elevated and makes naked short structures dangerous despite the constructive headline tape.

EU fiscal response to energy price spikes signals the conflict's economic transmission channel is active — subsidies cushion demand-side impact but confirm the supply shock is material enough to require policy intervention.

Oracle's bounce leading a software sector rally signals rotation into beaten-down growth — watch for this to support QQQ gamma stabilization if the bid sustains.

LVMH earnings miss from Iran war impact shows the conflict bleeding into consumer discretionary fundamentals — a second-order effect that argues against treating this as a purely geopolitical vol event.

London closing lower on Iran talk breakdown while Wall Street rallied creates a transatlantic divergence — European markets pricing escalation risk more conservatively than US, a potential morning gap risk for Tuesday.

Get today's live analysis

You're reading yesterday's market overview. Upgrade to Basic and get today's post-open analysis - the same data institutional desks use to set positioning each morning.

Unlock the full trading day

You see the market-open report. Growth gives you all 3 daily refreshes - midday regime shifts, close-wrap positioning, plus actionable trade ideas and "What it means for your trading" analysis.

What Basic includes

Today's market-open analysis

SPY, QQQ, IWM, VIX gamma regime

Key levels - flip, walls, max pain

VIX term structure + VRP analysis

Charts with trading reads

Full API access to lab.flashalpha.com

What Growth adds

3x daily refreshes (open, midday, close)

Actionable trade ideas per section

"What it means for your trading"

Regime shift alerts intraday

Close-wrap end-of-day positioning

Full archive history access

Plans start at $63/mo (billed yearly) · Cancel anytime